NWG - Lloyds Banking Group: Good 2022 Results Raised Mid-Term Outlook But 7x P/E

Summary

- Lloyds Banking Group plc 2022 results this morning support the undemanding expectations in our investment case.

- Return on Tangible Equity was 13.5% in 2022 and guided to be around 13% in both 2023 and 2024. Our forecasts only assume 11%.

- Net Interest Margin will likely remain manageable, and cost growth is moderate. Credit reserves now assume a "mild" recession.

- At 51.2p, Lloyds shares are now trading at below 1x Tangible Net Asset Value, 7x 2022 EPS and a 4.7% Dividend Yield.

- Our updated forecasts indicate a total return of 44% (14.5% annualized) by 2025 year-end. Buy.

Introduction

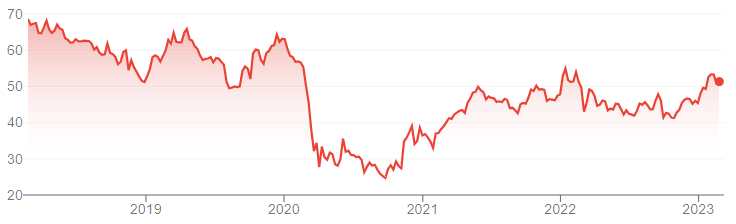

Lloyds Banking Group plc ( LYG ) released 2022 results this morning (February 22). Lloyds shares fell by as much as 3% in London in the morning, but are currently up 0.5% (at 51.2p) as of 14:45 local time.

We reinitiated our coverage on Lloyds with a Buy rating last July, and Lloyds shares have gained 24% (including dividends) since, though they remain significantly lower than before COVID-19:

{kind=link}

2022 results support the undemanding assumptions in our investment case. Return on Tangible Equity was 13.5% in 2022, and is expected to be around 13% in both 2023 and 2024. Cost growth is moderate despite inflation and investments. Net Interest Margin is expected to be higher year-on-year in 2023 (but lower than in Q4 2022), while assets are expected to be "broadly stable." Credit losses continue to be the main risk, though Lloyds has now reserved for a "mild" recession and even a "severe" one would be manageable. Pension contributions will likely be lower from 2023. Another £2bn of buybacks have been announced. Lloyds shares are now trading at below 1x Tangible Net Asset Value, 7x 2022 EPS and a 4.7% Dividend Yield. Our updated forecasts indicate a total return of 44% (14.5% annualized) by 2025 year-end. Buy.

Lloyds Buy Case Recap

Lloyds is the #1 retail bank in the U.K., largely focused on the domestic market, and offer a wide range of products and services to consumers, SMEs, as well as corporates and institutions.

Retail Banking contributes more than 60% of Lloyds' income and profits, while Commercial Banking and Insurance & Wealth were the other segments. Net Interest Income ("NII") represented 73% of total income in 2022, and 66% of Lloyds' gross lending consists of personal mortgages (as of 2022 year-end).

{kind=link}

The core of Lloyds' business is its large low-cost deposit base, where customers often accept lower rates because of Lloyds' brand name and their own inertia, and where unit costs are kept low by economies of scale. Lloyds generates NII from its deposits through lending and a "structural hedge" that functions similarly to a portfolio of fixed-rate bonds.

Credit losses are the main risk, but we expect they should be limited even in the event of a U.K. recession, because Lloyds' lending products have traditionally been targeted at the prime+ part of the market and its mortgage portfolio has conservative Loan-To-Value ratios (averaging 41.6% at 2022 year-end). In the event of a prolonged downturn, we expect Lloyds capital base to remain largely intact, with a return to a solid ROTE later.

Since February 2022, Lloyds has been implementing a new strategy under new CEO Charlie Nunn (who took up the role in August 2021). Key pillars of this strategy include deepening existing consumer relationships, diversify the SME business and selectively expanding Corporate & Institutional offerings. We are cautious about the new strategy, as they mostly seem to involve doing the same things but better (with the exception of a new investment offering), and are skeptical about the top team's relatively weak operational track record.

We had used relatively undemanding assumptions in our investment case, including a 10% Return on Tangible Equity ("ROTE"), worse than both recent performance and management targets, and a 10x exit P/E multiple.

2022 results and 2023 outlook are much better than our investment case.

Lloyds 2022 Results Headlines

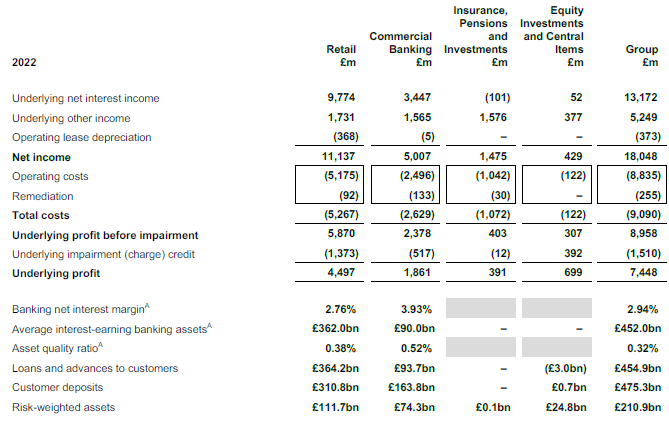

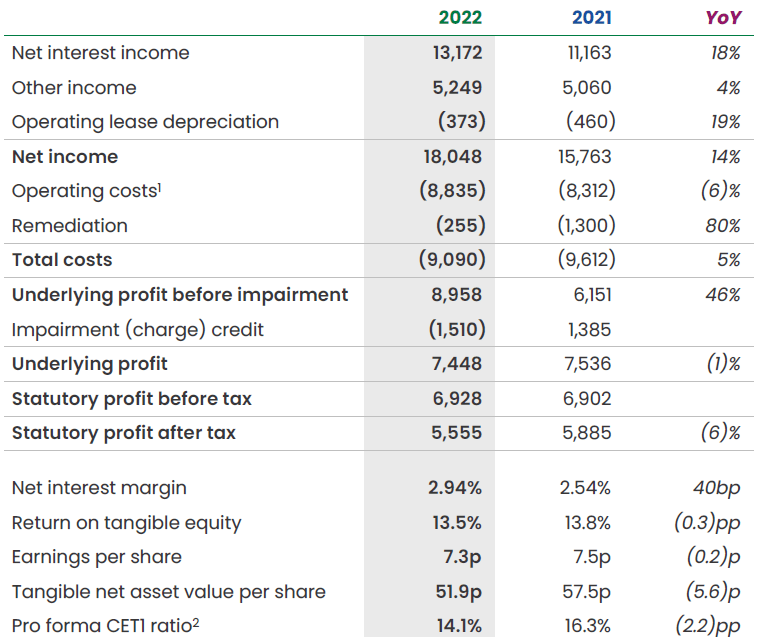

Lloyds achieved a ROTE of 13.5% in 2022, slightly lower than 2021's 13.8%, with a 46% increase in Underlying Profit Before Impairment offset by an £1.51bn Impairment Charge (compared to a release of £1.39bn in 2021):

{kind=link}

Net Interest Income grew 18% year-on-year, mainly due to Net Interest Margin ("NIM") rising 40 bps year-on-year to 294 bps, but also helped by a 1.6% increase in Average Interest-Earning Assets ("AIEA"), with "modest" growth in mortgages and unsecured personal loans offset by continued repayments of COVID-era government-backed loans.

Other Income grew 4% year-on-year, with increases in all 3 segments, including 8% in Retail (more customer activity in current accounts and credit cards), 9% in Commercial (higher markets activity and more transactions) and 12% in Insurance, Pension & Investments (more new business, an assumption change and the Embark acquisition).

Operating Costs rose 6% year-on-year, with "Business As Usual" costs stable at £8.3bn, but new "strategic initiatives & new businesses" costs of £489m.

Remediation Costs were only £255m in 2022, down 80% year-on-year, largely due to a £790m charge related to HBOS Reading in 2021 that did not recur.

Impairment Charge was £1.51bn, with £915m before changes in macroeconomic assumptions and £595m attributed to these changes. 2021's release of £1.38bn was largely due to £1.70bn of releases from changes in macroeconomic assumptions (reversing COVID-related charges), offset by £557m of impairments before these changes.

Tangible Net Asset Value ("TNAV") Per Share was 51.9p at 2022 year-end, lower year-on-year largely because of headwinds from accounting changes in the cashflow hedge reserve (7.5p) and pensions & other (3.8p).

Common Equity Tier-1 ("CET1") Ratio was 14.1% (pro forma planned dividends), compared to management target of 13.5% (12.5% requirement + 1% buffer). Lloyds generated 245 bps of capital in 2022 and distributed 185 bps, but its CET1 ratio fell because of the same accounting changes described above.

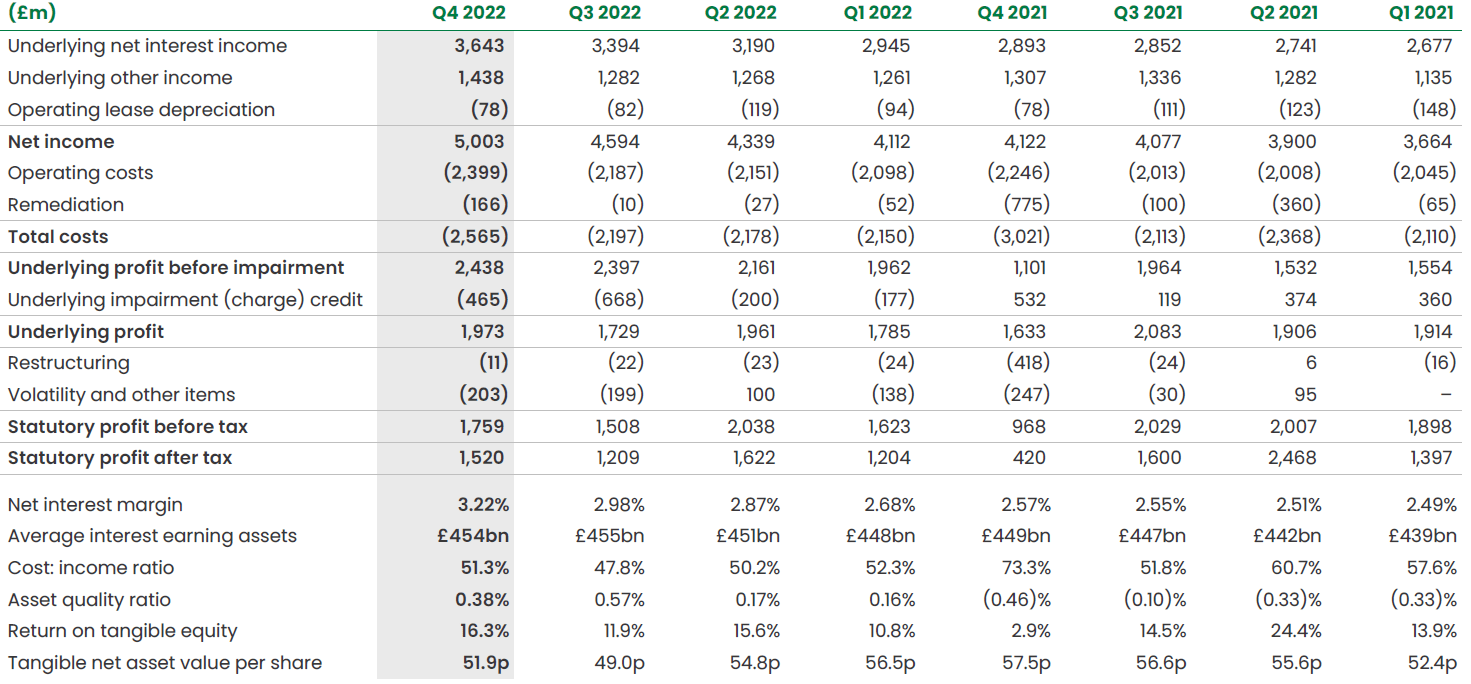

Lloyds' profitability improved through 2022, with ROTE reaching 16.3% in Q4, largely driven by a continuing rise in NIM:

{kind=link}

Management expects ROTE to be broadly stable in 2023 and 2024 as well.

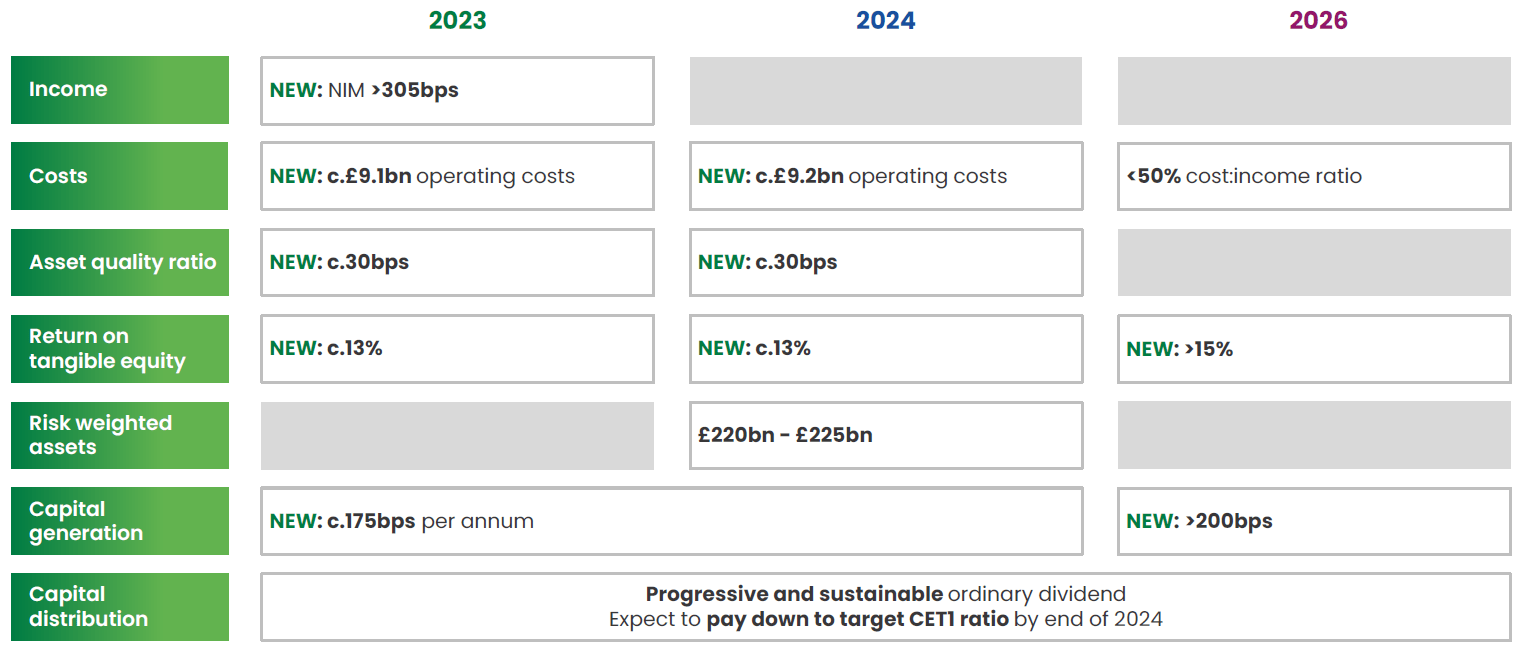

Lloyds 2023 & Mid-Term Outlook

Management issued their 2023 outlook as well as updated medium-term targets for 2024 and 2026:

{kind=link}

2023 ROTE is expected to be "around 13%," i.e., similar to 2022. NIM is expected to be "above 305 bps," higher than 2022 (294 bps) but below Q4 2022 (322 bps). AIEA is expected to be "broadly stable." Operating Costs are expected to be £9.1bn, up 3% year-on-year. Asset Quality Ratio (i.e. credit costs) are expected to be around 30 bps.

2024 ROTE is now expected to be also "around 13%," compared to "above 10%" previously. This is based on better-than-before assumptions on Non-Interest Revenues (including from strategic initiatives), offsetting higher assumptions on costs (£9.2bn vs. £8.8bn before) and AQR ("around 30 bps" vs. "less than 30 bps" before). The £400m higher costs now expected is the net result of £600m in higher gross costs and £200m of new cost savings.

2025 ROTE is now expected to be "above 15%," compared to "above 12%" previously.

We believe Lloyds will likely achieve its NIM guidance and probably its cost guidance for 2023. We are more cautious about the rest of their targets, in particular in ROTE.

Drivers Behind Net Interest Margin

The main moving parts behind Lloyds' NIM are deposit costs, mortgages margins, other loan growth and the return on their Structural Hedge. Trends in all four indicate that NIM will likely remain within manageable levels.

Deposit costs will increase somewhat as more of recent rate increases are passed on to depositors, but likely no worse than the 50% deposit beta that management has assumed. Lloyds' deposit fell by just £1.3bn (from £476bn) in 2022, with losses concentrated in more rate-sensitive accounts in Commercial Banking and Wealth:

| Lloyds Deposit Movements (2022) Source: Lloyds results presentation (Q4 2022). |

Q4 2022 saw a larger deposit decline of £8.1bn, but most (£6.4bn) of this was in Commercial Banking, and was partly due to short-term placements reversing and seasonality. Lloyds continue to have a surplus in deposits (with a Loan-To-Deposit Ratio of 96% at 2022 year-end), and Commercial Banking deposits tend not to be eligible for the Structural Hedge. So the limited deposit losses to date should have little impact on the P&L.

Mortgage margins seem to have stabilized during Q4. Completion margin on new mortgages averaged only around 50 bps in Q4, falling further from around 60 bps in Q2-3 and around 85 bps in Q1. However, much of the decline was due to a large volume of low-margin business signed in October, with "much more favorable" margins in November and December (though some of the October business will impact Q1 2023 NIM). Part of the current margin headwind is also due to the maturing of high-margin business written in 2020-21, and this effect should dissipate over time.

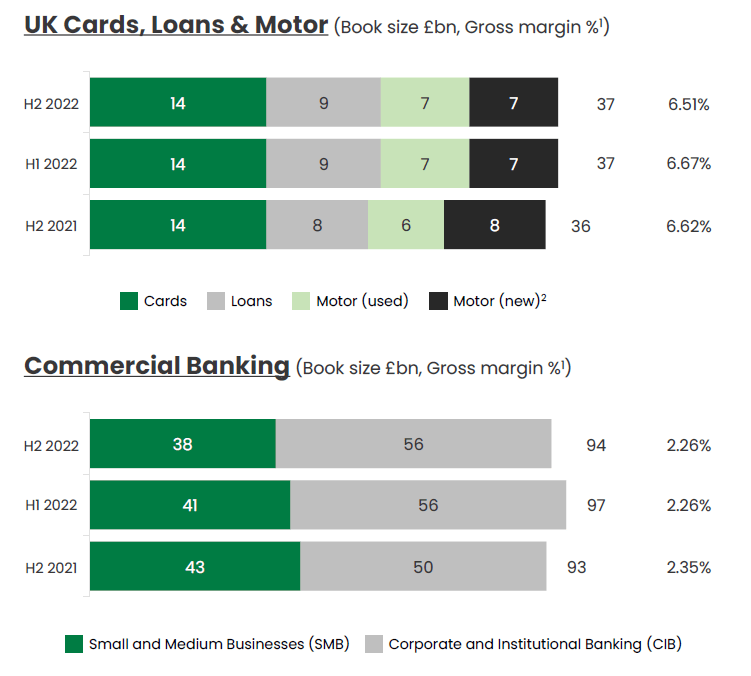

Other loan growth appears healthy, with modest to slightly-growing balances (except in SMBs, due to repayments of government-supported COVID loans), and a small decline in gross margin (likely due to mix shift):

| Lloyds Non-Mortgage Lending (H2 2022 vs. Prior Periods) Source: Lloyds results presentation (Q4 2022). |

{kind=link}

The Structural Hedge has fully deployed its £255bn capacity as of 2022 year-end, but the continuing redeployment of parts of its balance at higher rates is expected to be a significant tailwind for NII, generating £0.8bn in 2023 and "a similar increase again" in 2024 (compared to total income of £18.0bn in 2022).

Management expects 2023 NIM to be stronger in H2 than in H1, but "never below" 300 bps in each quarter, which also adds to our confidence that NIM will remain within manageable levels.

Lloyds' 2023 NIM outlook is slightly more conservative than that of NatWest Group plc ( NWG ), whose expectation of "around 320 bps" this year is in line with its Q2 2022 NIM of 320 bps.

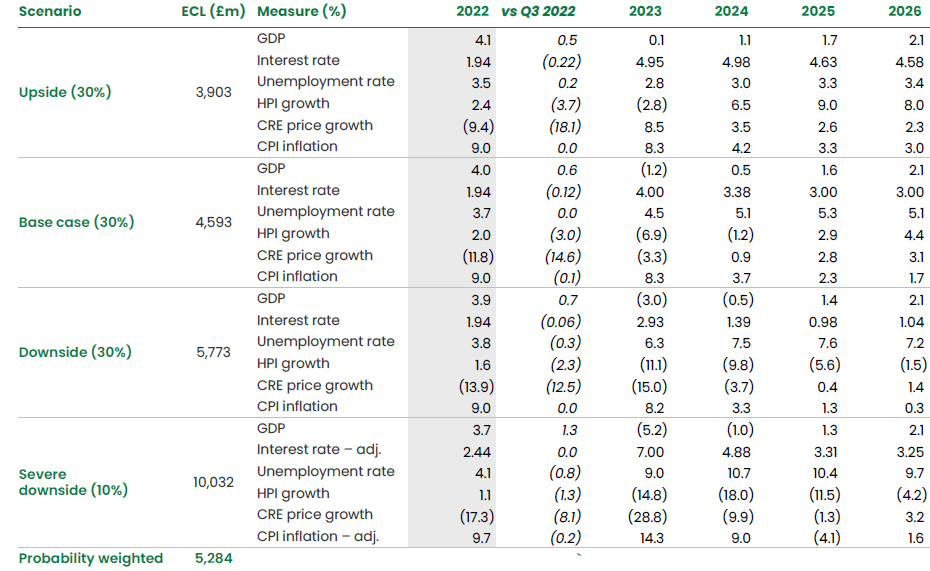

Credit Losses Should Stay Limited

Potential credit losses continue to be the main risk, though Lloyds has now reserved for a "mild" recession and even a "severe" scenario would be manageable.

Lloyds' Base Case is for the U.K. House Price Index ("HPI") to fall by more than 8% in 2023 and for U.K. unemployment to continue to rise and to peak at 5.3% in 2025:

{kind=link}

Lloyds' actual credit reserves (Estimated Credit Loss, or "ECL") of £5.28bn is about £0.7bn higher than its Base Case, being a probability-weighted outcome that also takes into account other scenarios. The Severe Downside Case is expected to bring £10.0bn of credit losses, £4.7bn than currently reserved, though the extra losses represent only 0.5x of Lloyds' 2022 Underlying Profit Before Impairment of £8.96bn.

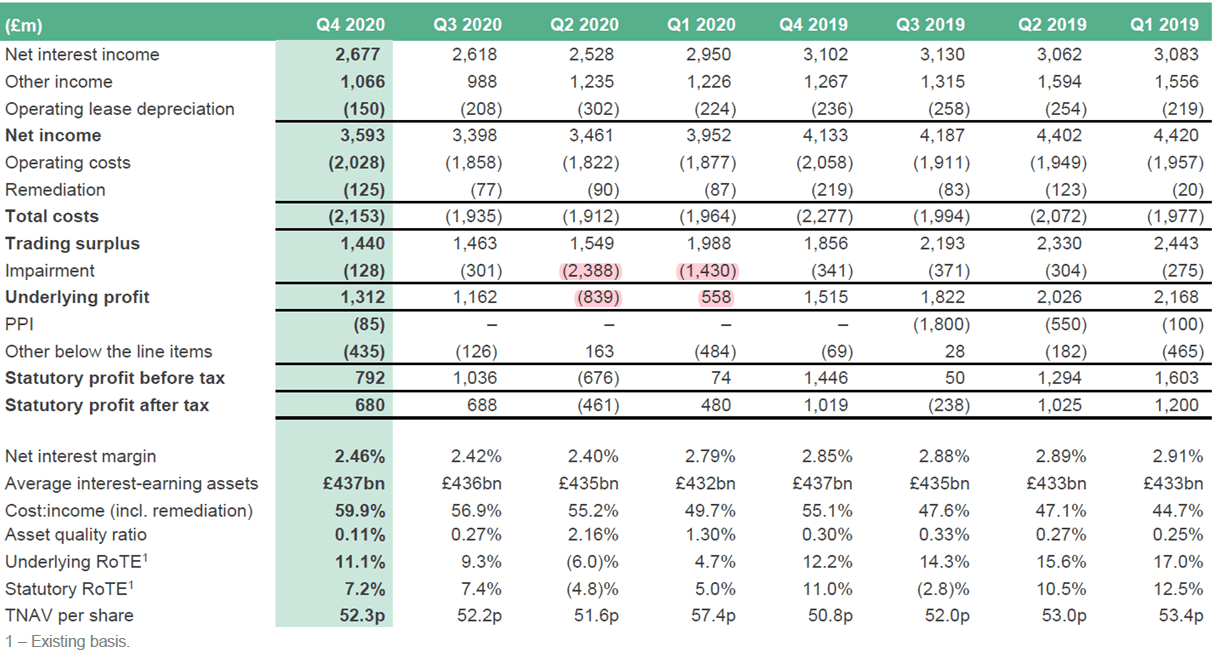

2020 provides a precedent: Despite disruption by COVID-19 and large credit reserve builds, Lloyds only made an underlying loss (of £839m) for one quarter and was profitable for the year (with an underlying profit of £2.19bn):

{kind=link}

A severe downturn in the U.K. is not our expected outcome, and we will likely not invest in Lloyds if it is. However, even in that event, we expect Lloyds' capital base to remain largely intact, enabling a return to a solid ROTE thereafter.

Lower Pension Contributions From 2023

Pension contributions will likely be lower from 2023.

Lloyds contributed £2.2bn to its pension schemes in 2022, as part of a 2021 agreement with pension trustees that it contributes £800m plus an amount equal to 30% of shareholder distributions each year.

The pension deficit was down to £2.2bn at 2022 year-end (from around £4bn the year before), the next tri-annual review is expected to be agreed by the end of Q3 2023, and management expects future contributions to be lower:

"The Group has discussed with the Trustee the likelihood that further variable contributions will not be necessary in 2023 and beyond … The Group also expects that future contributions will become increasingly contingent in nature."

Lloyds results press release (Q4 2022).

Lower pension contributions will enable higher dividends and/or more share buybacks.

Lloyds Stock Valuation

With shares at 51.20p as of 14:45 local time, Lloyds stock has a valuation of:

- 0.99x P/TBV, relative to Q4 2022 TBV of 51.9p per share

- 7.1x P/E relative to 2022 EPS of 7.2p

- 10x P/E relative to our assumption of a medium-term ROTE of 10%

- 4.7% Dividend Yield, relative to 2022 dividend of 2.40p (raised 20% year-on-year).

Share repurchases have been a regular part of capital allocation. A new £2.0bn buyback program was announced with 2022 results, equivalent to 6% of the current market capitalization, and followed a similar £2.0bn program in 2022.

Lloyds Return Forecasts

We increase our ROTE forecasts and reduce pension contributions, but keep other assumptions unchanged:

- ROTE to be 11% in 2023-25 (was 10%)

- Dividends, buybacks and pension contributions to be 94.5% of Net Income

- Dividend to grow 5% annually (unchanged)

- Pension contributions to be £800m (was £800m + 0.3x shareholder distributions)

- Buybacks to be conducted at 1.2x P/TBV (unchanged)

- P/E to be 10x at 2025 year-end (unchanged).

Our new 2025 EPS forecast of 6.59p is 14% higher than before (5.76):

| Lloyds Illustrative Return Forecasts Source: Librarian Capital estimates. |

With stock at 51.20p, we expect an exit price of 66p and a total return of 44% (14.5% annualized) by 2025 year-end.

Is Lloyds Stock A Buy? Conclusion

We reiterate our Buy rating on Lloyds Banking Group.

For further details see:

Lloyds Banking Group: Good 2022 Results, Raised Mid-Term Outlook, But 7x P/E