LYG - Lloyds Banking Group: Hold Rating As Undervaluation And Net Interest Income Grab Attention

2023-12-04 14:55:29 ET

Summary

- Lloyds Banking Group gets a hold rating today, which is aligned with the consensus from the SA quant system. This is rating the stock's ADR which trades on the NYSE.

- Neutral sentiment is driven by tailwinds to revenue and interest income, as well as undervaluation opportunity.

- Offsetting factors include risks of exposure to UK office market, a share price now up from its autumn price dip, and a weak dividend opportunity compared to peers.

Company Snapshot

One way for US-based investors to gain portfolio exposure to UK-based banks is through American Depository Receipts (ADRs), which represent shares in the underlying stock and can be traded on US exchanges, so today I will cover one of those.

Lloyds Banking Group ( LYG ) came across my research desk today as an opportunity to explore in today's note. Some quick facts about this London-based bank include its history going back a few hundred years, ownership of well-established brands like Lloyds Bank and Bank of Scotland, penetration of multiple segments including retail / commercial / insurance /wealth management, and providing 14.3B GBP in funding to first-time home buyers.

Total Rating Score

{kind=link}

Based on the score total in today's note, I'm rating this stock a hold .

Comparing my rating to the consensus on Seeking Alpha today, my rating is aligned with the consensus from the SA quant system:

Lloyds - rating consensus (Seeking Alpha)

Rating Methodology

My simplified and straightforward 8-point approach focuses on a few core areas such as revenue and earnings growth, dividend income opportunity, undervaluation opportunity, a share price presenting a value-buying potential, and identifying a key risk of the company as well as its potential impact to an investor.

Top-Line Revenue YoY Growth

I am looking for any positive revenue growth on a YoY basis, and here is what I found:

In the quarter ending September, the firm achieved $5.3B in top-line revenue vs $3.1B in the prior-year quarter, a 71% YoY increase.

One should mention the significance of the current interest-rate environment in fueling revenue being made on interest-earning assets, while being offset by interest-bearing obligations of the bank. Here is what the firm had to say about that in their Q3 earnings release :

Underlying net interest income of £10.4 billion up 10 per cent with a net interest margin of 3.15 per cent. Net interest margin of 3.08 per cent in the third quarter, down 6 basis points in the quarter given the expected mortgage and deposit pricing headwinds. Average interest-earning assets of £453.5 billion ..

I expect a positive revenue growth scenario to continue into 2024 which should be sustainable for this bank, and supporting my thesis is the following from a November article in Reuters highlighting how the UK's central bank will keep its policy rate steady for a while:

The Bank of England ((BOE)) will keep its Bank Rate at 5.25% until at least July in an effort to combat high inflation, a Reuters poll of economists showed.

As an investor and analyst, though, I am also interested in revenue diversification, so it's worth noting that this firm's Q3 release also mentioned the success of non-interest income:

Underlying other income of £3.8 billion, 8 per cent higher , reflecting continued recovery of customer activity and ongoing investment in the business as we progress against our strategic initiatives.

Net Income YoY Growth

I am looking for any positive net income growth on a YoY basis, and here is what I found:

In Q3 the firm achieved $1.7B in earnings, vs $515MM in the same quarter a year ago, which at first glance appears to be a few hundred percent increase.

So, I also compared this year's Q3 with the quarter ending Dec 2022 when $1.8B of earnings were achieved, so this time around was a slight 5% decline in earnings vs Dec 2022. It is also off of its March 2023 high of $2B in earnings.

Some factors from their Q3 release that have contributed to this:

Operating costs of £6.7 billion, up 5 per cent and in line with expectations.

An impairment charge of £0.8 billion.

Looking forward, inflation I believe could continue to impact operating costs as everything is generally more expensive, but expenses should continue to be offset by revenue growth. If history teaches us anything, we can see from the income statement that revenue exceeded non-interest expenses in each of the last eight quarters, so the key thing for me in considering this stock for my portfolio is whether at a minimum it is continuously profitable, which it has been.

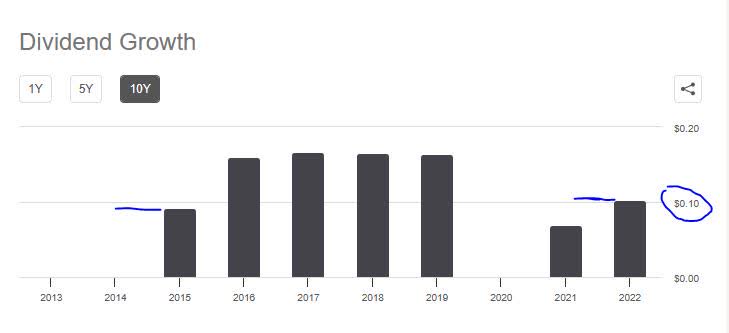

Dividend 10-Year Growth

I am looking for dividend 10 year growth trends, and here is what I found:

{kind=link}

In the data set above, the comparables would be the annual dividend in 2015 of $0.09 vs that of 2022 which was $0.10, an 11% growth (or 1 cent growth) in 10 years).

It should also be mentioned that this stock does not pay quarterly but a semi-annual dividend and from the history it appears the next ex-date could be not until April.

Seeking Alpha Quant also gave the dividend an "F" grade in terms of dividend safety, with concerns over its ability to continue paying the current dividend.

So, the dividend growth is offset by the fact that the dividend itself is so small and only pays semi-annual, as well as being deemed risky, so in this scoring category I am neutral / middle-of-the-road.

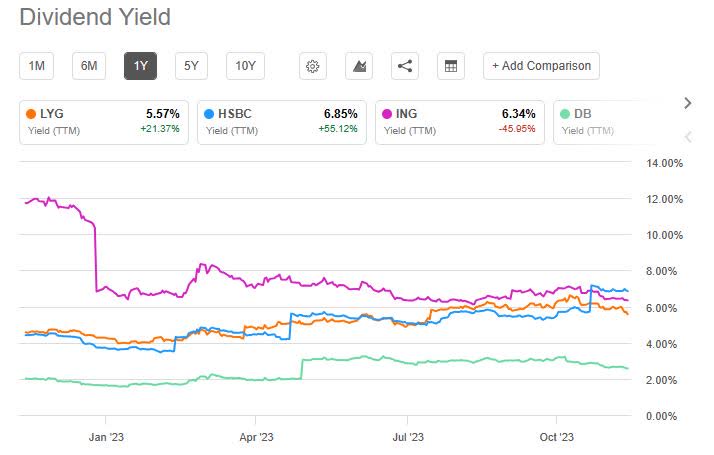

Dividend Yield Above Average

I am looking for a dividend yield above its sector average, and here is what I found:

{kind=link}

In comparing against peers like HSBC ( HSBC ), ING Groep ( ING ), and Deutsche Bank ( DB ), Lloyds came in third place with a trailing dividend yield of 5.57%, while its UK banking peer HSBC led the pack at 6.85% yield.

So, I would not pick Lloyds first for dividend yield when I can get a better rate from HSBC stock. However, a 5.5% trailing yield (currently forward yield is 4.09%) is not a bad deal either so in this category I am adding a point to the hold sentiment in my scoring matrix, as I am down the middle on this one.

Share Price vs 200-day Average

My portfolio strategy prefers dip-buying opportunities when the share price falls below the 200-day simple moving average , so here is what I found:

Using the yChart above and the market closing price on Friday December 1st of $2.25, it appears I missed out on the nice price dip this fall however it is currently hovering around the 200-day simple moving average and still down from its February and April highs.

Considering that revenue saw growth and earnings did not drop by a lot, along with continued potential of net interest income tailwinds, I would not call this a "sell" just yet. However, it seems like a great buy opportunity was missed so I am more inclined to mark a point in the hold category on this one, waiting to see if it will climb at least 5 to 10% above the moving average before pulling the plug and taking a capital gain if I had bought into those autumn dips.

What could drive that price climb would be an earnings beat for Q4, which is not impossible, given the factors I already mentioned.

P/E Valuation vs Average

I am looking for an undervaluation opportunity when it comes to price-to-earnings , and here is what I found:

A forward P/E ratio of 6.45, 36% below its sector average.

Tying this to the financials from the income statement, particularly earnings, consider that Q3 saw an earnings growth vs Sept 2022 and only a slight decline vs Dec 2022. It also grew from Q2 to Q3 by about 12%. At the same time, the share price as already discussed is hovering around the 200 day average and not much above it.

So, I will call this valuation justified and an undervaluation opportunity, giving it a point in the buy side on my scoring matrix.

P/B Valuation vs Average

I am looking for an undervaluation opportunity when it comes to price-to-book value , and here is what I found:

A trailing P/B ratio of 1.01, nearly 9% below its sector average.

Tying this to equity / book value from the balance sheet, we can see an increase in total equity to $54.9B in Q3 vs $51.7B in the prior year's quarter, a 6% equity growth. At the same time, the share price as already discussed is trading just around the moving average. So, in this case I will call this a justified valuation and worth a point in the buy category, since equity rose but the share price did not rise a lot above average.

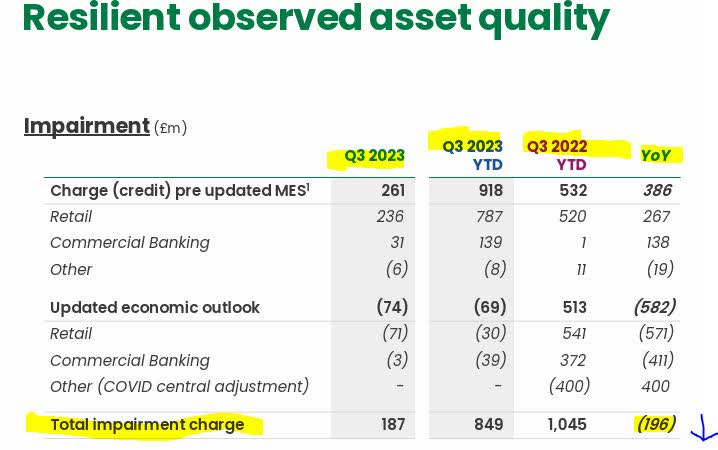

Key Risk

This type of business typically has a key risk of exposure to certain type of assets like loans it makes to customers and particularly loans on commercial property such as offices.

Impairment charges, as you may know, are costs a firm incurs for a drop in the recoverable value of an asset.

The good news is, according to this firm's Q3 results , is that the trend is moving towards a decrease in total impairment charges, which is a sign of improved quality of assets on the books:

{kind=link}

Further, the firm's mortgages that are in arrears are lower than their 2019 levels, however consider that 14% of their CRE portfolio is exposed to office property.

Lloyds - CRE office exposure (company q3 results)

Office property has had its share of bad news. In an early November article in Britain's The Standard newspaper, a major office project in downtown London went into default recently.

The article touches upon some headwinds to the commercial property space:

Rising interest rates have roiled commercial real estate, crimping valuations and pushing up landlords’ relative indebtedness, causing some to default. It has been particularly brutal for developers who have also had to contend with soaring construction costs and uncertainty over future demand.

So, in this case I think the risk profile is somewhere middle-of-the-road and I am putting another point in the hold category for this reason, as I am not overly bullish or bearish on their risk, as their office property exposure is not enormous but not small either.

Wrap-Up

To summarize, Lloyds is getting a hold rating from me as my sentiment is somewhat neutral on this one. Positive factors of revenue growth and undervaluation are offset by impacts to earnings and the risk of exposure to the UK commercial property market in the current environment.

I also would not call it a great dividend play since they only pay semi-annually and at a rate of about 10 cents a share, however the dividend yield being past 4% is a positive, although I think I can do better with some of its peers I highlighted.

Overall, a longstanding bank with name recognition in global banking circles and proven versatility over 100 years, and an opportunity to "hold onto" exposure to foreign banks through an ADR in a portfolio where I would also include US and Canada banks as well for diversification.

For further details see:

Lloyds Banking Group: Hold Rating As Undervaluation And Net Interest Income Grab Attention