LDI - loanDepot: Bearish As Mortgage Market Struggles

2023-07-31 17:09:17 ET

Summary

- loanDepot has experienced negative Net Income in recent quarters and this trend is expected to continue. Stock price performance has diverged from negative financial results.

- The US mortgage market is experiencing headwinds from higher interest rates, as loan originations and applications are dropping.

- Management insiders have been selling their own stock, and sell-side analysts have a cautious outlook.

Investment Thesis

loanDepot ( LDI ) stock is up ~50% this year, despite not having a profitable quarter since Q4 21. Analyst consensus points towards another loss this year, and the US mortgage market is experiencing dropping loan applications and originations, which will further impact their top line earnings. The stock's overperformance appears unjustified from a fundamental perspective and is due a sell-off.

Company Summary & Market Outlook

loanDepot primarily operates in the retail mortgage segment, covering the origination, financing, and selling of residential mortgage loans. The firm has built a broad service offering to cover all steps of the purchase and refinance process, from credit score monitoring, to listing search, and various loan products. Over time, LDI has also expanded to cover non-mortgage loan products as well such as unsecured personal loans.

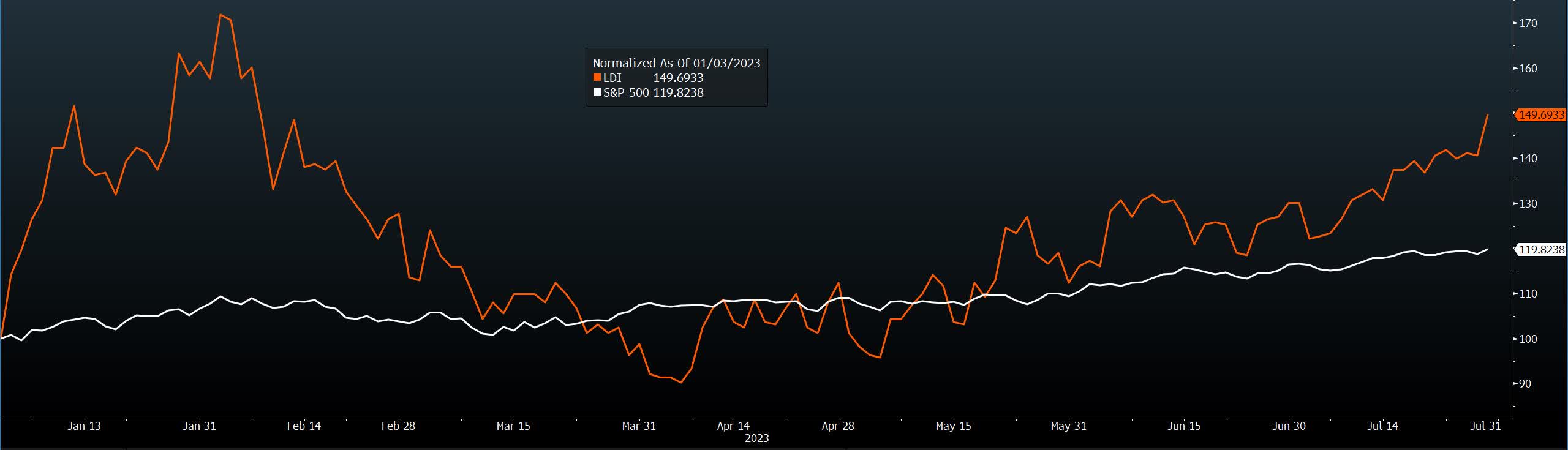

LDI stock has seemingly defied the reality of its negative financial results and tougher mortgage market conditions discussed further below, as the price has risen nearly 50% year-to-date, significantly overperforming the ~20% return by the S&P 500 over the same period. As elaborated in the sections below, this divergence cannot be sustained in the long run, and I expect LDI stock to drop significantly after such a notable rally.

LDI, S&P 500 - Normalized (Bloomberg)

{kind=link}

The aggressive monetary tightening performed by the Federal Reserve to combat inflation has stunted the mortgage market in the US, as the higher cost of financing has priced out many potential home buyers. This in turn negatively impacts mortgage finance firms such as LDI, as the lower loan originations hit their top line.

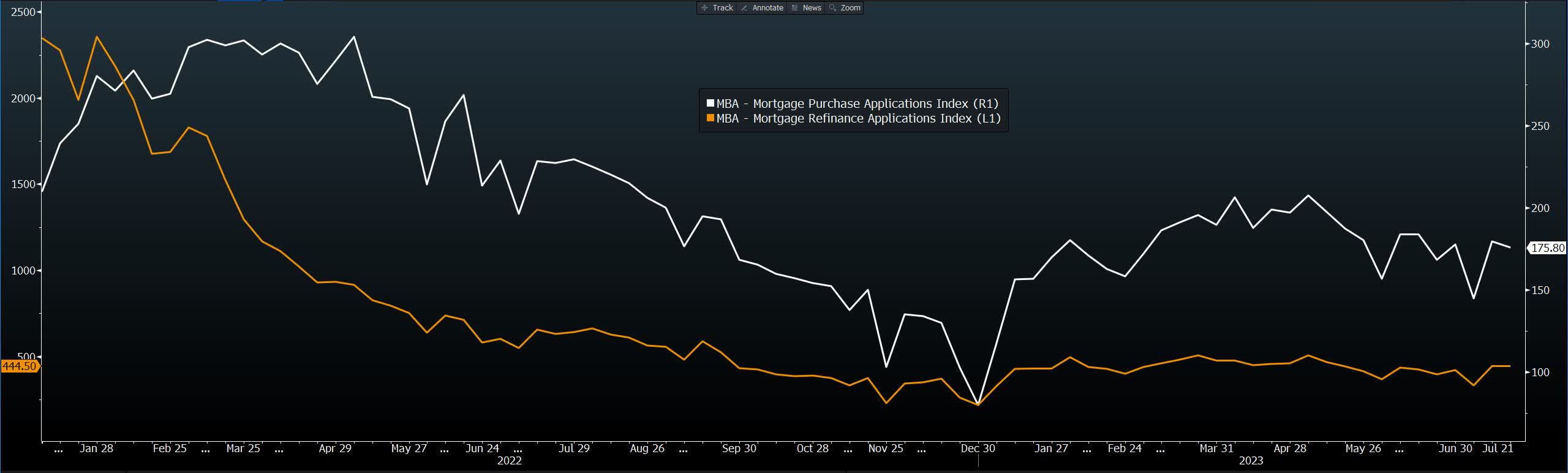

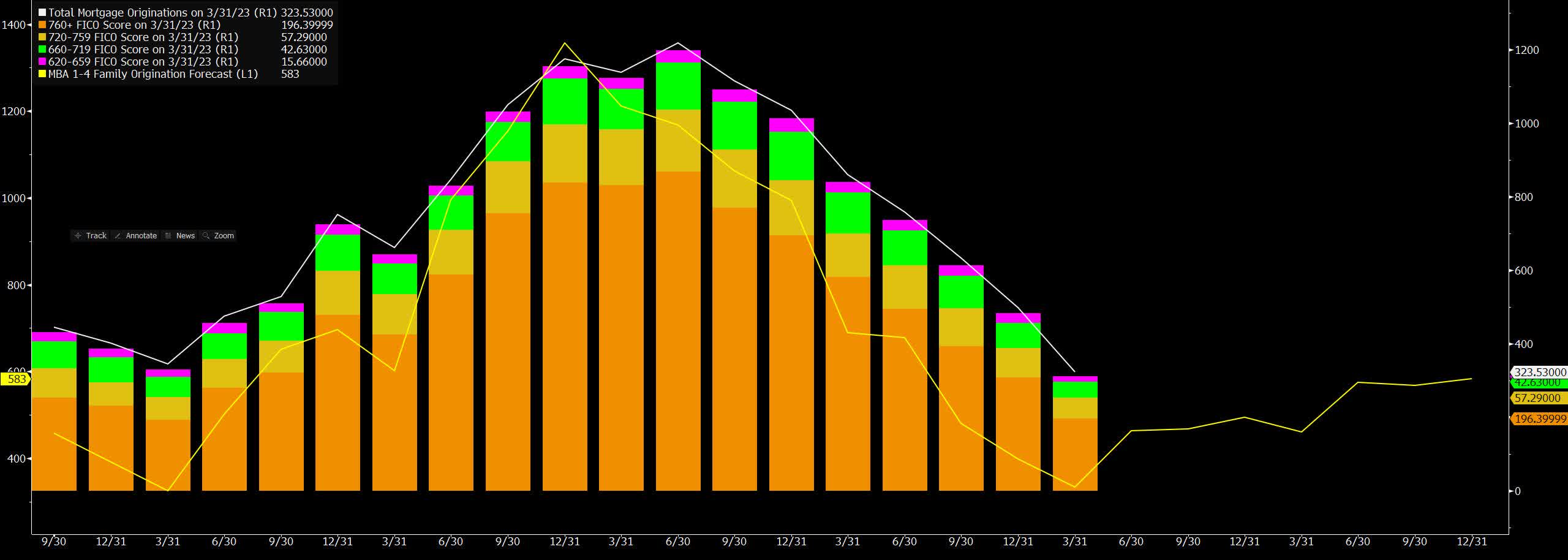

As per the data from the Mortgage Bankers Association, one can see the significant drop in both mortgage purchase and refinance applications from a peak in 2022. Worryingly, this downward trend is being observed across the residential market, as demonstrated by the drop in originations throughout all FICO score groups.

MBA - Mortgage Applications Index (Bloomberg) MBA - Mortgage Originations 2018 - 2023 (Bloomberg)

{kind=link}

{kind=link}

Negative Financials

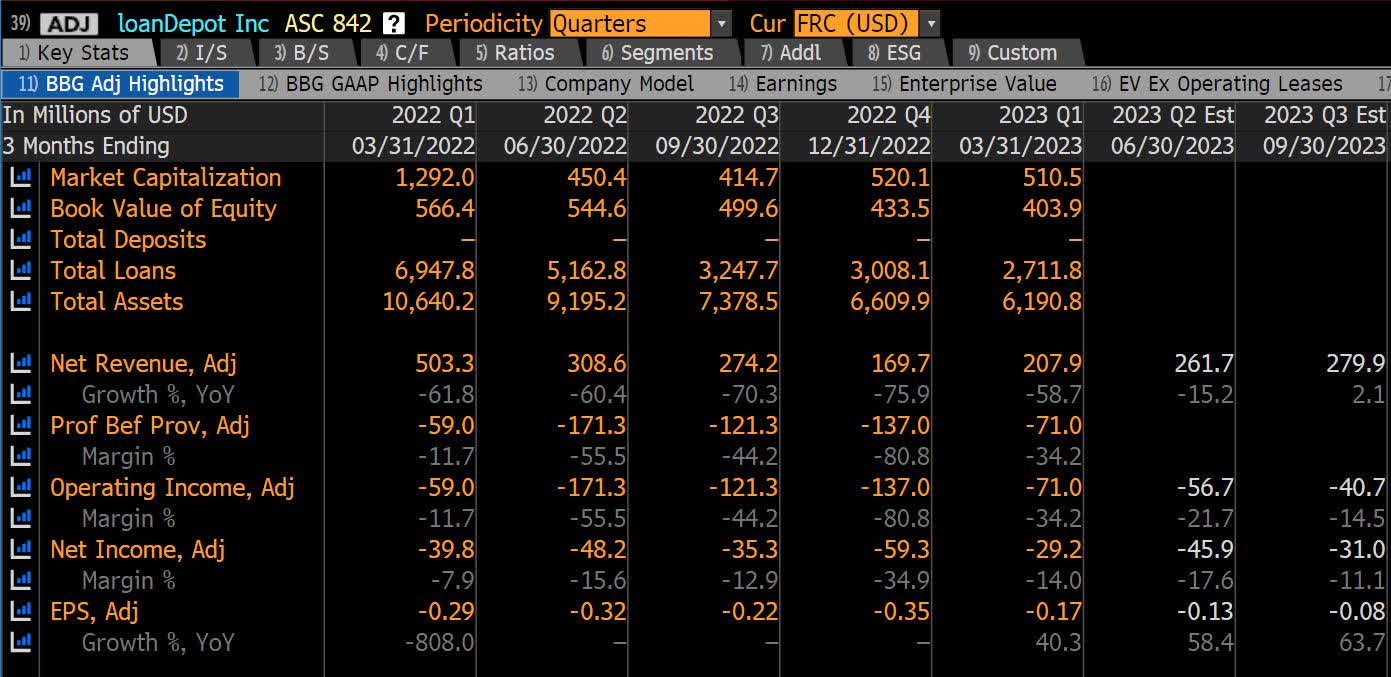

Whilst the stock has managed to perform well this year, the financial results are starkly different and have been for a while. In the last year, LDI has experienced significant drops in market cap, total loans, and total assets. Most worryingly, the firm has experienced multiple periods of negative income throughout the rate hiking cycle of the Fed. In Q1 23, Net Revenues hit $207.9 million, a decent improvement from the $169.7 million generated in the previous period, but still nearly 60% lower on a year-on-year basis. Operating Income in Q1 23 was -$71 million, ~34% worse than the Q1 22 loss, and Net Income was -$29.2 million.

Looking ahead, the Bloomberg analyst consensus forecasts that there will be no return to profitability any time soon. For Q2 23 results, which will be released on August 8th, the Net Loss is expected to widen again to -$45.9 million.

{kind=link}

It is surprising that the stock has turned such a positive performance this year, whilst the financial position has deteriorated across the board in recent quarters. I believe that due to the lagged nature of the Fed's monetary policy, and the interest rate hikes that have been implemented since the Q1 results, there will be extended pain in the US housing and mortgage markets. As a result, I believe the macro headwinds will limit LDI's financial results from improving significantly, which warrants a downward correction in the stock's price.

Rich Relative Valuation & Bearish Analyst Forecasts

LDI Peer Data & BPS Estimate (Bloomberg)

{kind=link}

LDI's negative Earnings Per Share ((EPS)) in recent periods does not allow for a P/E valuation based on relative multiples. However, we can look at Book Value Per Share ((BPS)) and the Price-to-Book Ratio. The Bloomberg analyst consensus for LDI's BPS in fiscal year 2023 is ~$2.33, which we can then apply to the sector peers' average P/B ratio of 0.88x. This provides an implied target price of $2.05, which based on the current stock price of $2.44, represents a negative return potential of -16.15%.

P/B Valuation (Bloomberg)

I then look to affirm my valuation target above with the equity research analysts that are surveyed on the Bloomberg Analyst Recommendation page. As per below, we can see ~78% of the analysts have issued a "HOLD" recommendation, however, the median consensus of the 12-month target prices is implying a negative return potential of -14.8%, a figure relatively in-line with the valuation discussed earlier. This helps to reinforce my view that the stock is overvalued, as the sell-side community covering this stock is also either neutral or bearish on LDI at these levels.

LDI - Analyst Recommendations (Bloomberg)

{kind=link}

Management Selling

Using the Bloomberg Management Transactions page, we can look to identify any notable buying and selling patterns to affirm the fundamental thesis. In the case of LDI, there is a clear selling bias by the executive team, with a significant majority and high frequency of sell transactions year-to-date. This can be perceived as a bearish indicator on the stock, as management may not view their own stock prospects as attractive in the medium to long term, and are taking advantage of the higher stock prices to reduce their stakes.

LDI - Management Transactions (Bloomberg)

{kind=link}

Risks

The main risk to this thesis is that the Federal Reserve has likely reached their peak interest rate level, and that we may start approaching a point where general interest rates stabilize and possibly even start drifting lower. This could lead to a rebound in mortgage lender profitability, as consumer affordability for housing and mortgages improves. However, this would be an optimistic view which may take until well into 2024 to materialize notably. In the meantime, any macro sentiment and monetary rate improvements will be offset by the evident challenges that LDI management team are having in scaling back operating costs and managing provisions effectively in this declining mortgage origination market.

In Conclusion

On face value, loanDepot has had a fantastic year so far in terms of their stock performance. However, looking beyond the surface, we can see two major divergence factors that should weigh down on the stock. Firstly, the mortgage market dynamics have steadily been deteriorating from the hawkish monetary policy. Hesitant or priced out buyers and high mortgage rates will negatively impact LDI's top line growth. Secondly, the firm's management has struggled to manage operating costs and turn a profit, this was the case even last year when rates had not reached the peak levels of today. The problems seem to be compounding and justify a bearish view on the stock.

For further details see:

loanDepot: Bearish As Mortgage Market Struggles