LDI - loanDepot: Tough Market Conditions Make Investing Risky

2023-07-31 08:30:45 ET

Summary

- loanDepot is expected to have positive net income in 2024, but the company is not yet consistently profitable.

- The company has been losing market share and its business model has yet to be profitable.

- loanDepot aims to launch a home equity line of credit (HELOC) to improve operational performance, but the results may take time to reflect on the balance sheet and income statement.

Introduction

loanDepot ( LDI ) has been making strong progress in growing its bottom line and net margins. The market expects net incomes to be positive in 2024 at an EPS of $0.12. This would put LDI at a FWD p/e of 18 which given the growth and the market opportunity the management sees they have valued at $1.5 trillion. But as we are seeking an undervalued play and one that could provide solid returns to investment there is some fundamental rule we need to follow. For me, one of those is to only invest in consistently profitable companies. This leaves out some potential returns from up-and-coming companies like LDI, but a fair trade I am happy to take.

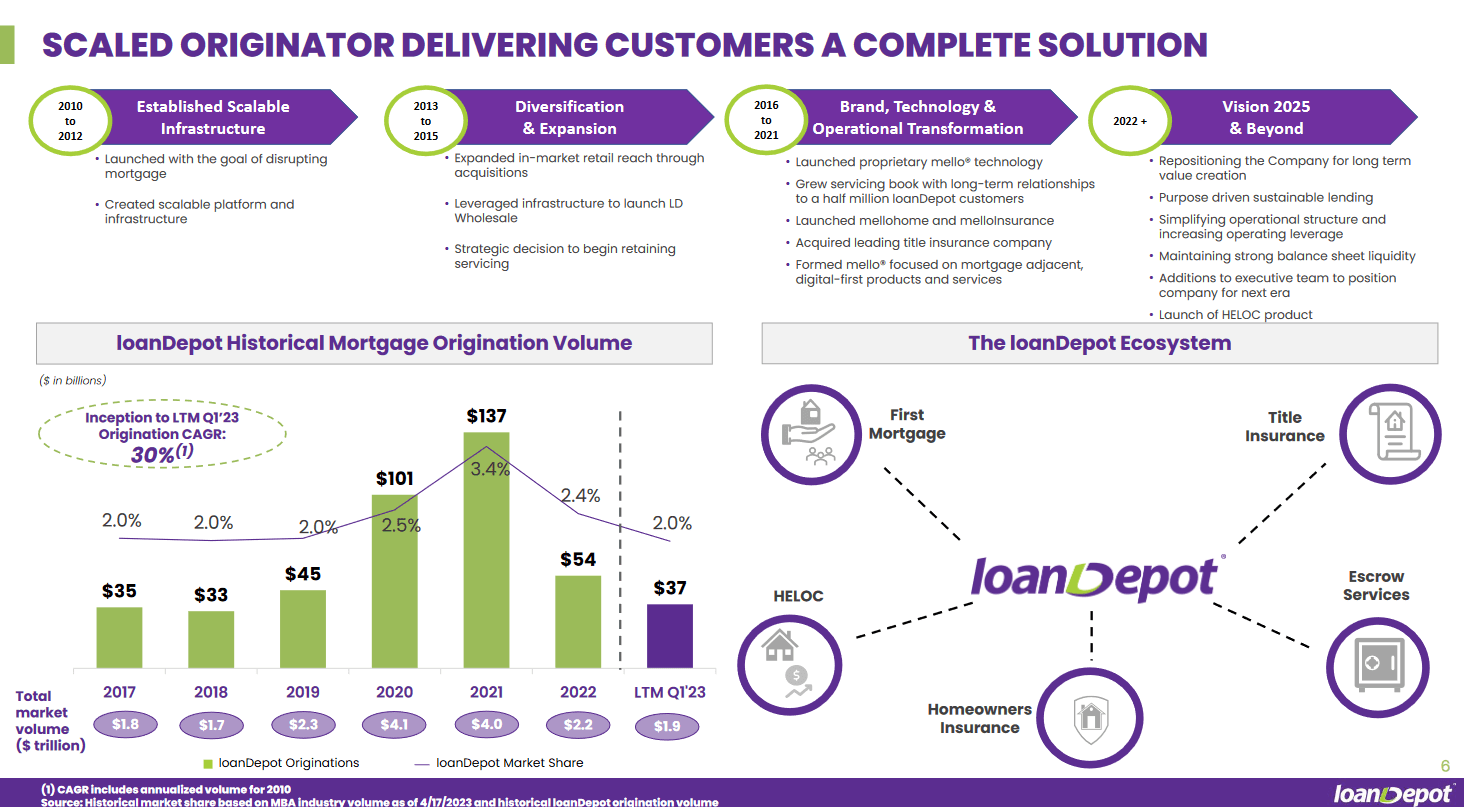

LDI is a company financing and selling residential mortgage loans in the United States. The growth thesis around the company seems quite optimistic as the business model is scalable. But in terms of this translating to a profitable bottom line we aren't there yet, unfortunately. Besides this, what worries when eventually the company does post a positive EPS is the fact they have been losing market share over the years, sitting at 1.5% right now as per their investor presentation . This all concludes with a hold rating for LDI right now in my opinion.

Company Structure

LDI is a relatively new company that has been in operation since 2010. The business revolves around originating, selling, and servicing residential mortgage loans in the United States. Here it offers conventional agency-conforming and prime jumbo but also home equity loans. The headquarters are in Foothill Ranch, California. The market cap has grown a fair to over $700 million but as I have mentioned a couple of times already, their business model is yet to be profitable.

{kind=link}

The company has been growing its ecosystem model and aims to launch a home equity line of credit (HELOC) which will provide the company with record levels of home equity in just as little as just seven days. This growth has made them the third largest mortgage lender in the United States as measured per units of funded loans.

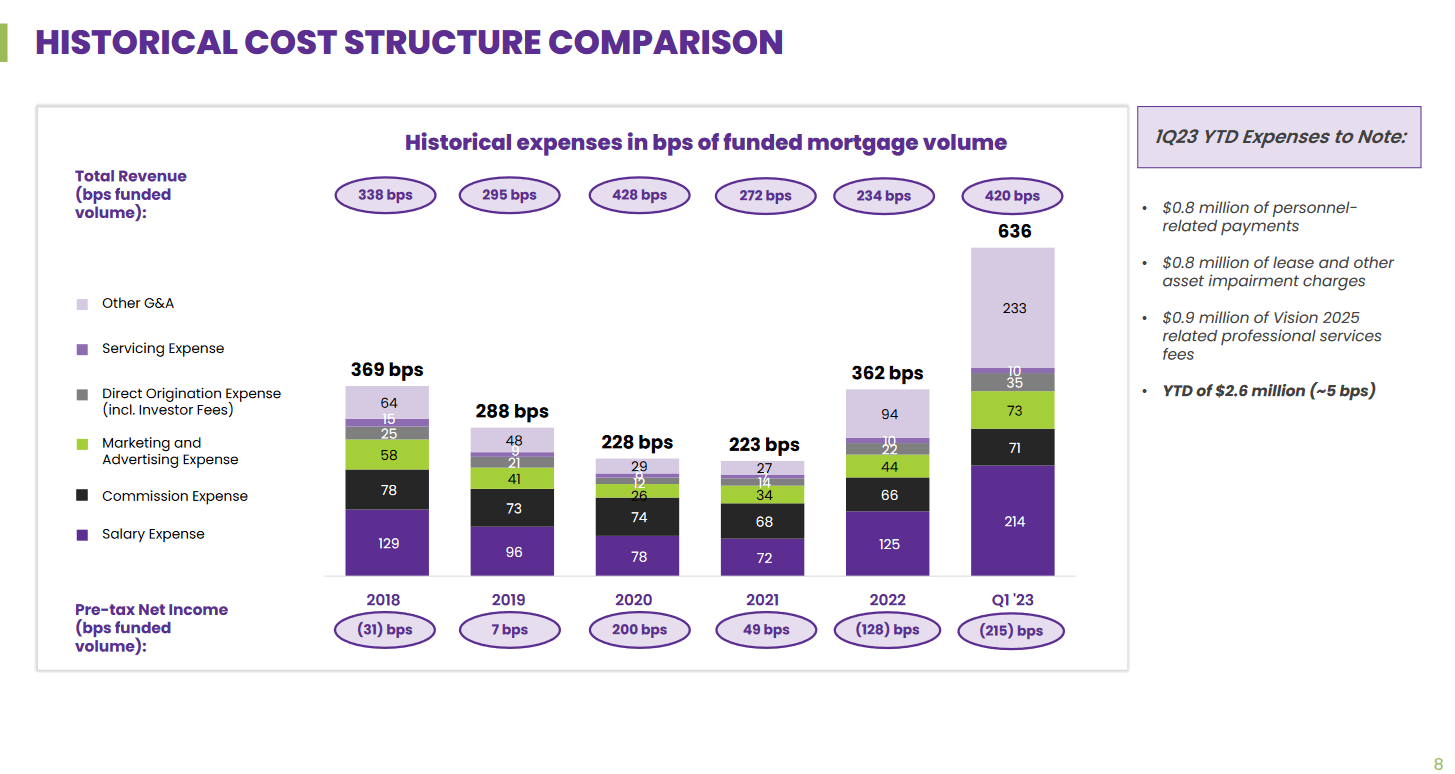

The vision the company has going forward is to slim down the business structure to create better operational performance and stronger margins. This comes as the management seeks a more value-driven growth approach coming from the launch of the HELOC product but also making customer acquisitions efficient. As for when we see the results of this on the balance sheet and income statement is a different question. It still feels like it's a fair bit out, unfortunately.

Earnings Transcript

From the earnings call back in May some comments from the management team highlight some of the conditions there are operating with and what the outlook might be. We are coming up on the next Q2 report on August 8. The higher interest rates are impacting home affordability and also the results of LDI negatively too it seems.

CEO Frank Martell said the following:

-

Overall, as expected, the first quarter of this year remained challenging for the housing market as virtually all participants grappled with the impacts of higher mortgage interest rates, persistent cost inflation, and a lack of available homes for sale.

This highlights the market environment they are in back then. But there seem to be some positives on the horizon and the housing market “ recession ” is already set to recover and do so quickly. The next report seems to be a toss-up between a disappointing revenue result of a fantastic one if LDI can manage to grapple with the market and grow its volumes.

-

Looking ahead, although the affordability and availability of new and existing homes remains challenging for the industry overall, at loanDepot, we expect to continue to benefit from seasonally higher revenues as well as our ongoing cost reduction productivity programs. Together, these positive trends should continue to drive improving financial results over the course of the second quarter and the third quarter of 2023.

The cost measure that the company is applying I don’t think will be visible until sometime forward. This means that right now the earnings report is likely to be quite flat or disappointing. The cost reduction measures they are taking will need to prove very effective to improve the margins and drive a positive EPS for LDI. Otherwise, a significant drop in the share price seems imminent given the run-up it has had in the last couple of months.

Risk Associated

The path to positive earnings for LDI requires more than just expense optimization; additional strategies and measures are essential to achieve this goal in the current economic landscape.

While expense optimization is undoubtedly a critical step towards improving profitability, LDI needs to address other aspects of its business to achieve sustained positive earnings. This may involve diversifying revenue streams, exploring new markets, or identifying opportunities for growth and innovation.

{kind=link}

The challenging state of the mortgage market poses another obstacle to LDI's turnaround. With some projecting a significant 28% decline in mortgage originations for this year, the company must be prepared to navigate through a prolonged period of reduced demand. A decline of this magnitude in the mortgage market can significantly impact LDI's revenue generation and overall financial performance.

Investor Takeaway

For investors that are seeking a solid mortgage play, I don’t think LDI is there right now. It seems to be quite speculative still and this is of course presenting a lot of risk to investors. The negative bottom line isn't expected to see strong improvements until next year and if interest rates remain high home affordability will continue to be elevated. Such an environment isn't beneficial to LDI and lower volumes are likely. I remain optimistic about the company in the long term. LDI hasn't been in operations for that long and I view them as a long-term play than anything else. The time isn't to buy right now, but the time is to hold onto shares and benefit from when the market conditions do reverse and interest rates go down. To conclude, rating LDI stock a hold.

For further details see:

loanDepot: Tough Market Conditions Make Investing Risky