LBLCF - Loblaw Companies: Robust Growth Outlook But Limited Margin Of Safety In Valuation

2023-12-22 04:06:23 ET

Summary

- L:CA's 3Q23 earnings results show strong revenue growth and solid margins. This trend is in line with its past financial performance.

- The company is expanding its discount stores to capture the growing shift towards discounted products in the market.

- Easing inflation in Canada is expected to boost L:CA's revenue and margins as it stimulates retail spending.

- However, my conservative valuation model indicates that there is a lack of a margin of safety in its share price. In addition, when compared to its competitors, it barely outperformed them. Therefore, I am suggesting a hold rating.

Synopsis

Loblaw Companies ( L:CA ) (LBLCF) operates a diversified food retail business in Canada, focusing on both traditional retail and discount store formats and catering to a wide range of consumer needs and preferences.

L:CA's historical revenue has shown signs of revenue growth recovery with margins expanding annually. Its 3Q23 earnings results also continue to show strong revenue growth and solid margins. Looking ahead, I anticipate that easing inflation in Canada will boost L:CA's revenue and margins as it stimulates retail spending. In addition, there is a shift towards discounted products, and L:CA is actively expanding its discount stores to capture this growth.

However, when compared to competitors, although it has outperformed them in terms of growth, it is in line in terms of profitability. Even though it is trading at a premium P/E, my model indicates only modest upside potential in the single-digit range. The lack of a margin of safety has led me to recommend a hold rating for L:CA.

Historical Financial Analysis

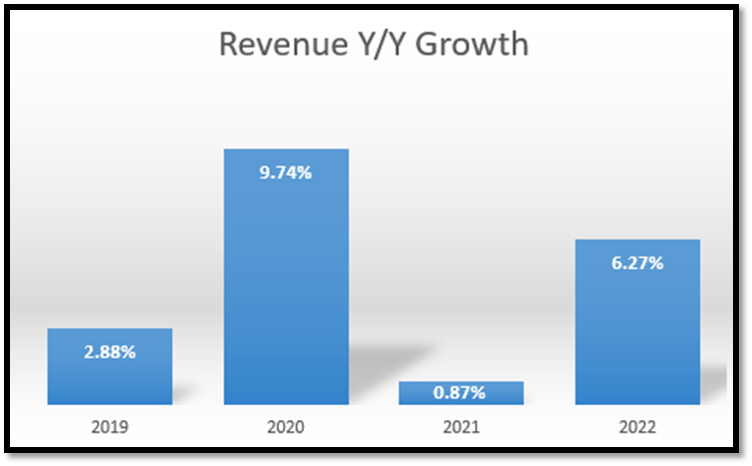

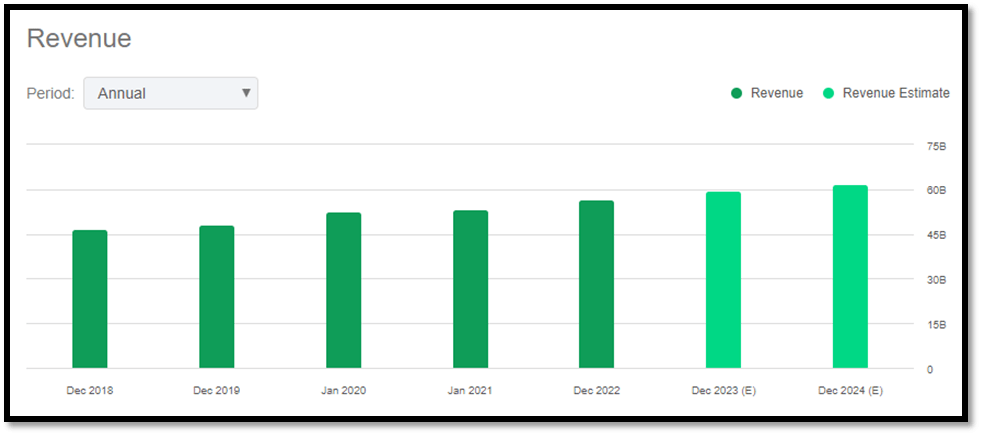

From the following revenue chart, it's clear that L:CA's revenue has been quite volatile. In 2021, revenue growth fell to a four-year low of ~ 0.87%. The reason for the low revenue growth was the inclusion of an additional week in 2020, which added $878 million to that year's revenue. If we exclude this, the adjusted revenue growth is ~ 2.6%, still lower than the growth rate in 2020. This was primarily due to supply chain constraints brought about by COVID and rising inflation. However, in 2022, the revenue growth rate has recovered and reached ~ 6.27%.

2020 was an exceptional year as revenue was boosted by the COVID-19 pandemic. During this period, there was heightened demand in both the food and drug retail sectors as consumers stocked up on essentials due to lockdowns and health concerns.

{kind=link}

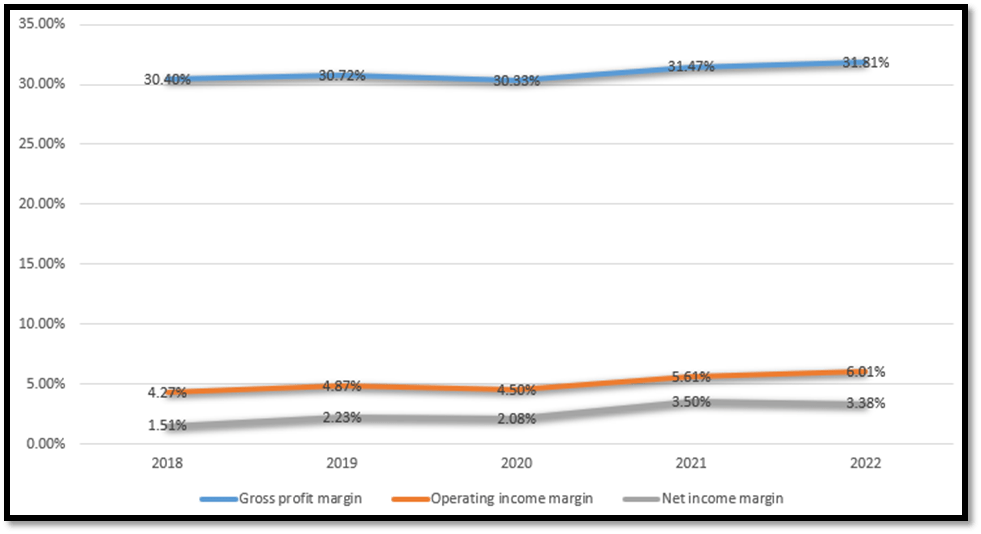

On the profitability side of its P&L, L:CA's gross profit, operating income, and net income margins have been expanding annually. In 2019, the gross profit margin was ~ 30.40%, the operating income margin was ~ 4.27%, and the net income margin was ~1.51%. By 2022, these margins had expanded to ~ 31.81%, 6.01%, and 3.38%, respectively.

{kind=link}

Although margins have expanded, its net income margin remains in the low single-digit range, raising concerns about its solvency. Therefore, I would like to analyze its debt levels to ensure that its balance sheet is healthy.

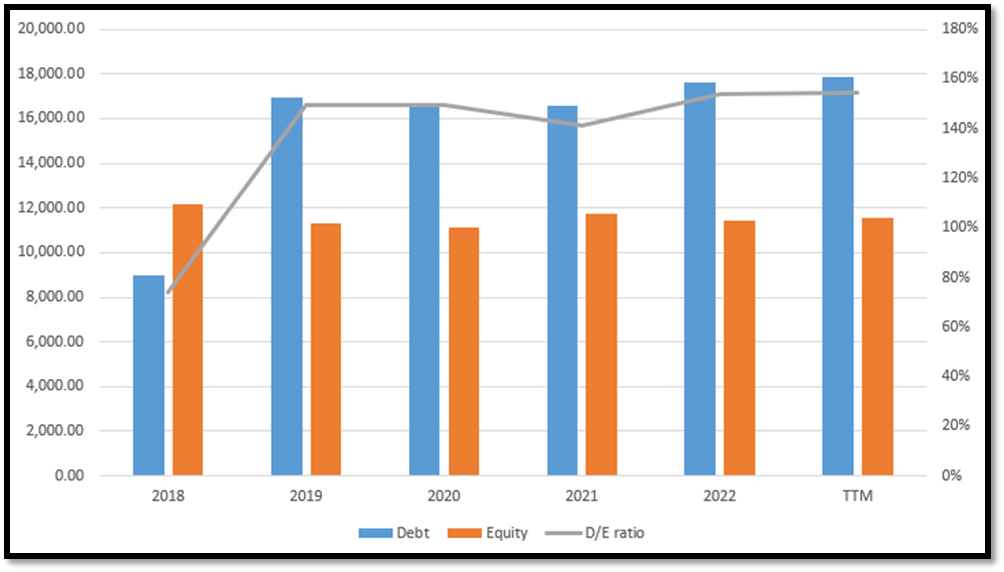

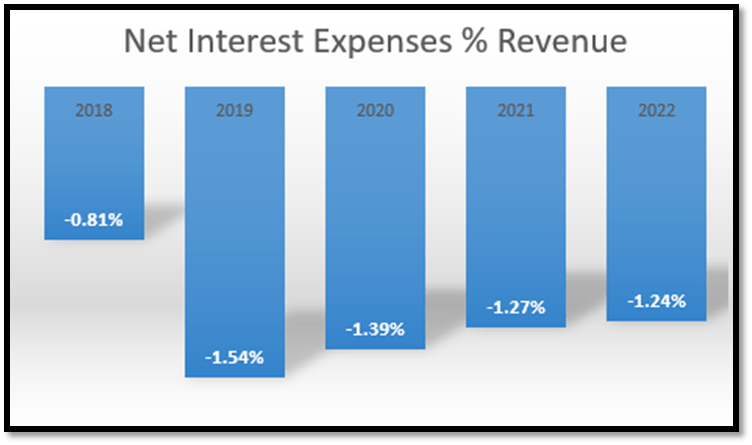

In terms of the debt-to-equity [D/E] ratio, it has remained relatively stable over the last four years. On a trailing twelve-month [TTM] basis, it appears quite stable as well. When I calculated its net interest expenses as a percentage of its total revenue, it was clear that net interest expense does not form a significant portion of its expenses, as it is in the range of ~ 1.3%. However, I would like to see management take active steps to control its debt levels and ensure that they remain stable.

{kind=link}

{kind=link}

Analysis of 3Q23 Financial Results

In my opinion, L:CA reported robust 3Q23 financial results. Its revenue grew by ~ 5% year-over-year from ~$17.38 billion to ~$18.26 billion. Its revenue can be broken down into retail and e-commerce segments. For its retail segment, revenue also grew by ~5% year-over-year, while e-commerce revenue increased by ~13.6%.

The robust revenue growth for the quarter can be attributed to strong performance in both drug and food retail. In drug retail, the growth was driven by cosmetics, health, and beauty products. Pharmacy sales also grew, driven by an increase in acute and chronic prescriptions, including specialty drugs.

For its food retail side, the growth was attributed to higher customer traffic, unit growth, and positive market share momentum. There was also notable success with its hard discount banners, which continued to attract customers.

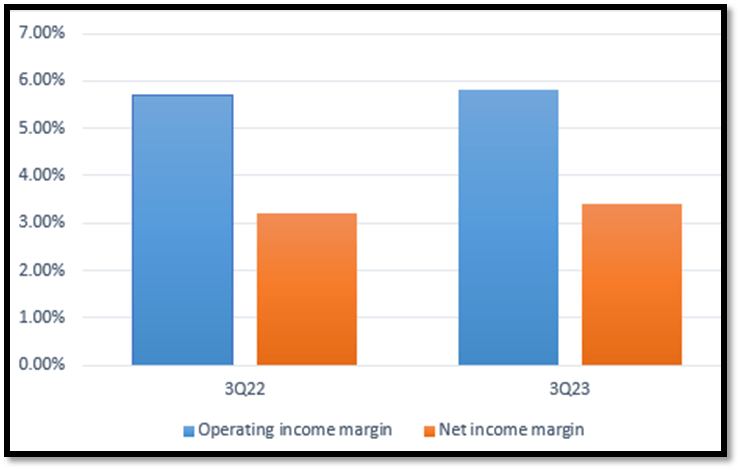

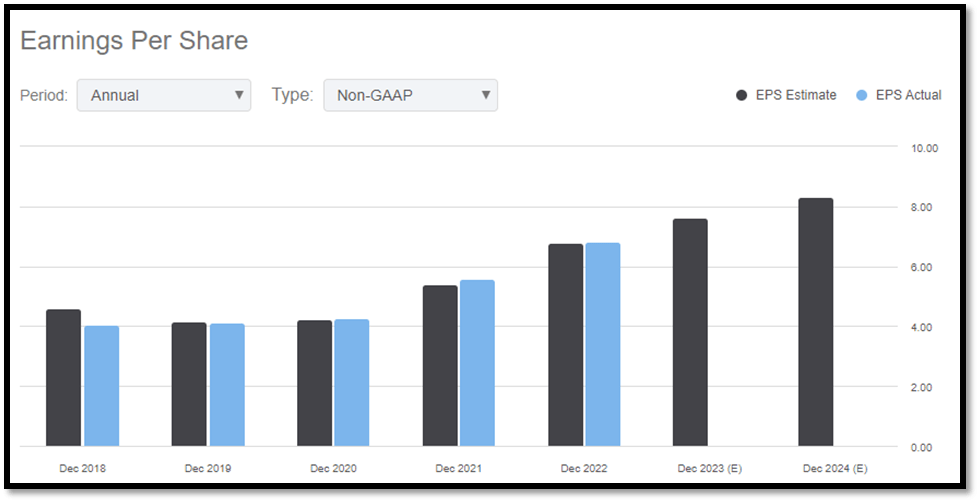

In terms of profitability, 3Q23’s operating income grew by ~ 7.5% to ~$1.06 billion, up from 3Q22’s ~$991 million. Additionally, 3Q23’s net income grew by ~11.7% year-over-year to ~ $621 million, up from 3Q22’s ~$556 million. As a result, the net income margin expanded to ~ 3.39%, from 3Q22’s ~3.19%. Due to strong top-line revenue combined with margin expansion, diluted EPS grew by ~ 15.4% year-over-year to $1.95, up from 3Q22’s $1.69.

Based on the following chart I created, it shows that both margins are expanding year-over-year, but the expansion is quite modest. The reason why EPS was able to grow by ~15.4% year-over-year is due to the reduction of its diluted weighted average common shares outstanding. In 3Q22, it was 329.6 million, but in 3Q23, it was reduced to 318.4 million through share buybacks.

L:CA's Investor Relations

{kind=link}

Easing Inflation Will Boost Food Retail Sales and L:CA’s Margins

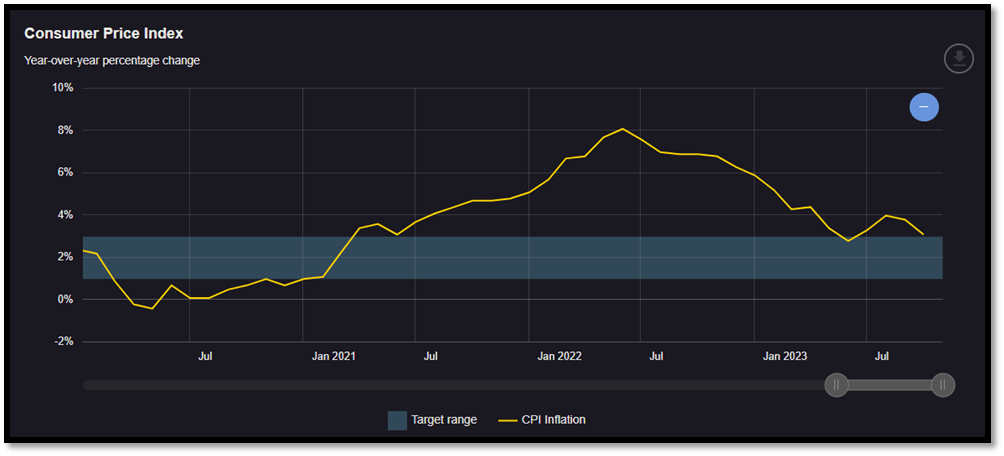

Based on the following inflation chart from the Bank of Canada, it is clear that inflation has been cooling since mid-2022. As of October 2023, the CPI inflation was ~3.1%. To give you a refresher, L:CA is a company that operates in the food retail industry in Canada, and its revenue is sensitive to inflation.

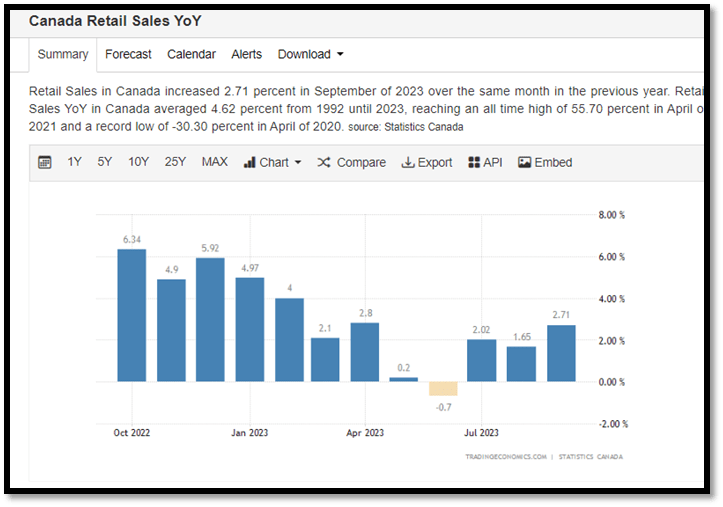

When inflation cools, it means that the price of goods is decreasing as well. Therefore, this makes purchases more affordable and will likely boost retail spending. Higher retail spending will lead to more sales and revenue for L:CA. Looking at the Canada retail sales chart , it clearly shows an increasing trend. In September 2023, retail sales grew by 2.71% year-over-year. Therefore, I expect this recovery in retail sales, driven by lower inflation, to bolster L:CA’s future revenue growth.

In addition to driving future revenue growth, lower inflation has a significant impact on COGS. Lower COGS translate to higher gross profit margins, which will ultimately trickle down to net income margin and EPS. As inflation is well below 2022’s peak, I expect this to have a cooling effect on COGS. Hence, moving forward, I expect L:CA’s margins to either remain consistent or expand further if inflation cools even more.

However, please keep in mind that cooling inflation does not equate to normalized inflation. As you can see, current inflation is still above the central bank's target rate. In addition, no one can predict the direction of inflation. With all these uncertainties regarding inflation and the central bank's interest rate decisions, management stated that consumers are shifting towards discount stores.

{kind=link}

{kind=link}

L:CA’s Strategic Initiatives to Capture the Shift Towards Discount Store

As mentioned by management, there is strong evidence and a trend indicating that consumers are shifting their shopping to hard discount stores . This was evident as L:CA’s discount banners continued to outperform, showing higher traffic and market share growth. The reason for this shift in consumer behavior is due to their response to economic uncertainty. Although inflation has cooled, the current level of inflation is still above the target rate, hence causing uncertainty.

Quote : “We believe the outperformance of our discount stores will continue as Canadians continue to seek value to help manage through the challenges of this extended period of high inflation and economic uncertainty.

To further support this thesis, Dollarama ( DOL:CA ), a business that operates a chain of dollar stores in Canada, reported in its recent 3Q24 results that net income grew by 31.4%. This growth was attributed to strong consumer demand for affordable products. Hence, there is a clear trend that the uncertainty is shifting consumers towards discounted products. Therefore, I believe L:CA’s strategic decision to expand its discount store count is going to support its future growth outlook.

Comparable Valuation

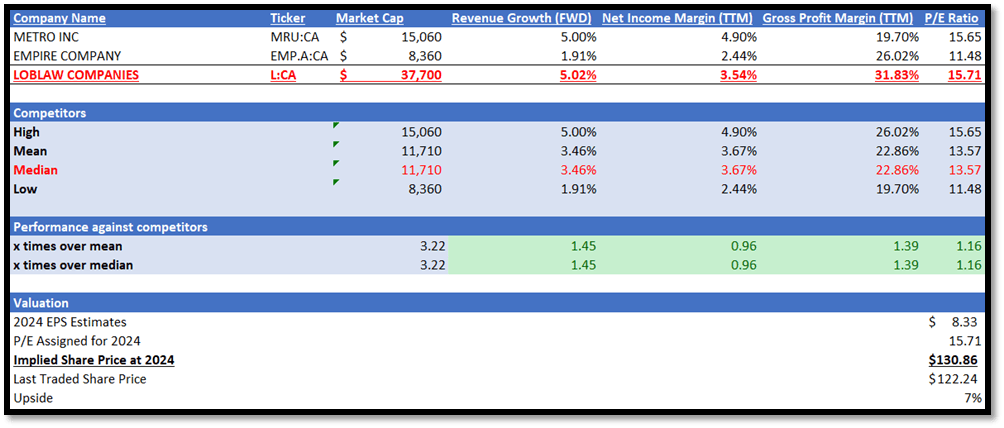

L:CA operates in the food retail industry in Canada. I have listed down the two closest competitors I can identify that operate in the same industry as L:CA in my valuation model below. For my comparable valuation, I will be comparing L:CA against its competitors in terms of revenue growth outlook and profitability.

In terms of market size, L:CA is significantly larger than its competitors. L:CA has a market capitalization of ~$37.7 billion, while its competitors’ median is ~$11.71 billion. This means that L:CA is 3.22x larger than them.

Despite being more than three times larger, its revenue and profitability performance are almost in line with its smaller counterparts. In terms of forward revenue growth outlook, L:CA is expected to grow by ~5.02%, while its competitors’ median is not far behind at ~3.46%.

Although L:CA has a much higher gross profit margin TTM of ~31.83% versus its competitors’ median of ~22.86%, its net income margin TTM is in line with its competitors. L:CA’s net income margin TTM is ~3.54%, while its competitors’ median is ~3.67%.

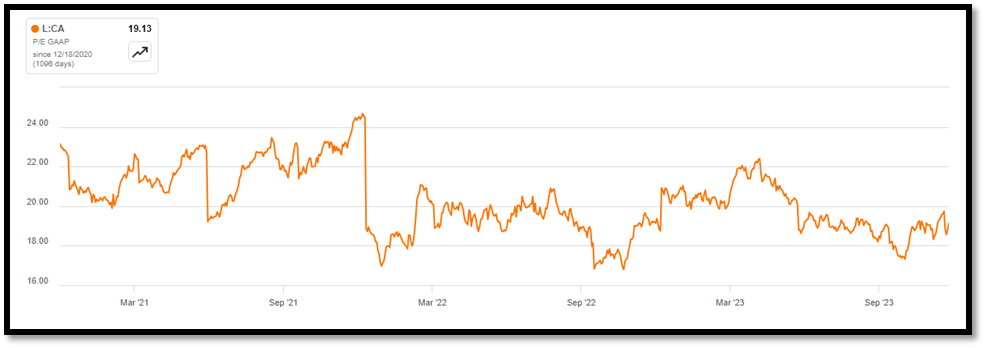

However, due to its higher forward revenue growth outlook, L:CA’s P/E ratio is currently trading at ~ 15.71x, which is 16% higher than its competitors’ median of 13.57x. In addition, the financial strength and growth catalysts of L:CA that I have discussed above also support this premium multiple.

{kind=link}

The market estimates that L:CA's revenue for 2023 is expected to reach $59.53 billion and $61.59 billion for 2024. In terms of EPS, 2023 is expected to report an EPS of $7.64 and $8.33 for 2024. Given the strength of L:CA's financial results and the growth catalysts I have discussed in depth above, this supports the market's revenue and EPS estimates.

By applying its current P/E ratio of 15.71x to its 2024 EPS estimates, my 2024 price target is $130.86, which represents an upside potential of only 7%. Although L:CA's current P/E ratio is below its 3-year average, I am sticking to this to remain conservative. Additionally, it is already trading at a 16% premium compared to its competitors. At its 3-year average of ~20x, it would represent a premium of ~47%, which I believe to be too steep.

Although L:CA is a good company with robust revenue growth and is consistently making strategic initiatives to grow the business, the modest ~7% upside potential does not provide enough margin of safety. With a forward revenue growth outlook slightly outperforming and net margins in line with its smaller competitors, I am recommending a hold rating for L:CA as of now, as the risk-to-reward ratio is not attractive enough for me at this moment.

{kind=link}

{kind=link}

{kind=link}

Upside Risk

One potential upside risk to my hold recommendation would be inflation. If inflation were to cool down and reach the central bank's target rate, it might prompt the central bank to stop interest rate hikes or even possibly reduce them.

In this scenario, a few things are likely to happen. Lower interest rates lead to lower interest expenses, therefore boosting L:CA’s margins. In addition, it also means more disposable income for consumers. This, in turn, might swing consumers back from discount stores to higher-end products, thus making L:CA's focus on discount stores less lucrative.

Additionally, lower inflation tends to boost retail sales, which means higher revenue growth for L:CA. Furthermore, it lowers COGS, which will bolster margins again. In such a situation, it will turn the market expectation for L:CA bullish, leading to share price appreciation.

Conclusion

In conclusion, L:CA’s revenue over the past four years has been volatile due to the COVID-19 pandemic, but 2022’s revenue growth has shown signs of recovery and stabilization. In addition, its margins are also expanding annually. For its latest 3Q23 result, it continues to show strong revenue growth and margins, driven by strong performance in both drug and food retail.

Moving ahead, I expect the cooling inflation in Canada to bolster L:CA’s future revenue, as lower inflation will spur retail spending. Furthermore, lower inflation leads to lower COGS, which will strengthen L:CA’s margins. Although inflation is cooling, it is not completely resolved yet, as it is still above the central bank's target rate. Due to this uncertainty, L:CA and DOL:CA have witnessed a shift in consumer spending towards discounted products. L:CA is preparing to capture growth in this area by expanding its number of discount stores.

Despite all the tailwinds, my conservative valuation model only suggests a modest upside potential in the single-digit range. With a lack of margin of safety, I am recommending a hold rating for L:CA at the moment.

For further details see:

Loblaw Companies: Robust Growth Outlook But Limited Margin Of Safety In Valuation