GMRE - Lock In A 9.5% Yield With Global Medical REIT

2023-06-29 17:14:53 ET

Summary

- Global Medical REIT Inc. has been severely affected by rising interest rates, with its stock down about 50% from its all-time high in January 2022.

- Despite the healthcare sector's struggles, GMRE enjoys a very stable tenancy base with long term leases and 97% occupancy rates.

- While enjoying a 9.5% dividend yield, investors can expect some capital gains to come from the end of the Fed's hiking cycle, which could happen in the 12 months.

I often enjoy reviewing sectors that are out of favour in the market as I believe this is the best way possible to find good deals. In 2023 the REIT sector clearly stands out to me as a prime example for such an endeavour, as many real estate companies find themselves beaten down due to the current interest rate hiking cycle by the Federal Reserve.

Similarly, in the past 18 months or so Global Medical REIT Inc. ( GMRE ) has been severely punished as well: the stock is down about 50% from the all-time high seen in January 2022, and is even down YTD a further 5%. If we use the Vanguard Real Estate Index Fund ETF ( VNQ ) as a proxy for the performance of the REIT sector as a whole, we can see how the company has severely underperformed the sector in the past year, down over 21% compared to about 9.5% drop for VNQ.

YCharts

However, this has created an opportunity because the REIT sector is potentially 6 to 12 months away from an initial rebound if we are of the view that interest rates have nearly peaked, which seems increasingly the case month after month. If that happens, GMRE’s stock price could rebound higher considering that management is also targeting a 50% reduction of the floating rate debt currently on the balance sheet in the near future. Meanwhile, we can enjoy a huge 9.48% dividend yield that is relatively safe thanks to a reliable, high-quality tenancy base and generally long term leases.

Are we heading towards peak rates?

When investing in REITs we cannot ignore the macro, as the sector is very clearly linked to interest rates. The latest on inflation data showed that in the United States inflation slowed to 4% YoY growth, down from a much larger 4.9% recorded in the month of April. As far as month-on-month change, overall prices grew 0.1% for a modest annualized pace of 1.2%. That is for the headline numbers, while the Core CPI reading (which excludes highly volatile elements such as food and energy components) was a bit more stubborn and came in at 5.3% YoY and 0.4% MoM (4.8% annualized). For the purpose of this article, I think it’s important to highlight that the Federal Reserve bases its monetary policy primarily on Core inflation data rather than the headline one as it is believed to be a more reliable dataset, together with other considerations regarding the health of the job market. On this note, it is worth mentioning that many analysts believe that the cracks in an overall tight job market are starting to emerge .

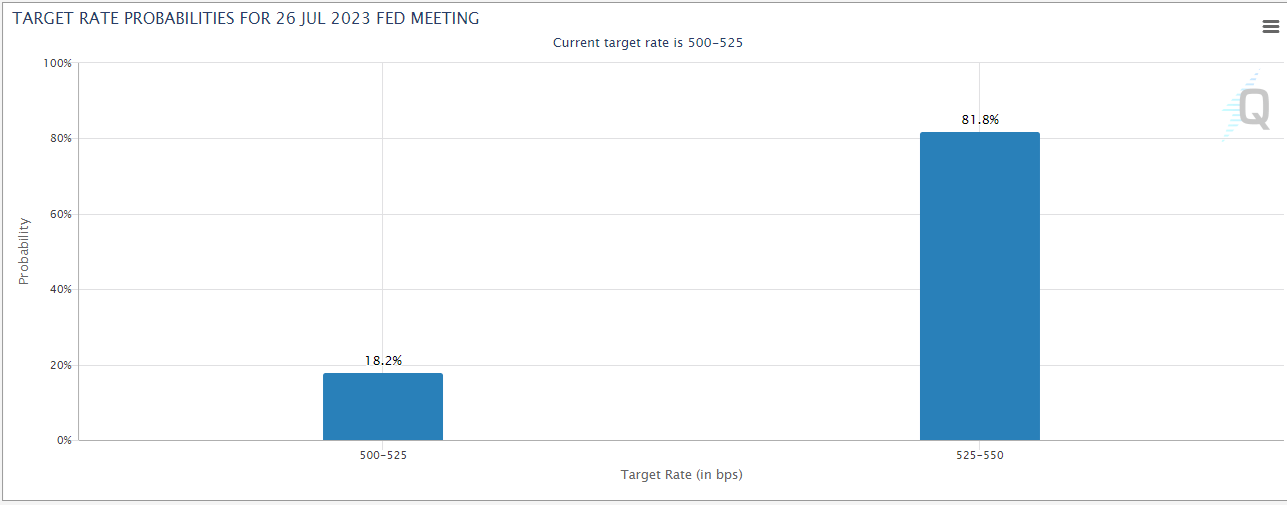

Inflation cooling and labour market slowing down pose well for an end of the interest rate hiking cycle. Indeed the Fed in the June meeting has announced a pause from hiking rates, leaving the benchmark at 5% to 5.25% while signalling however the intention to tighten further in the second half of the year, in an attempt to appear more hawkish than eventually will need to be. As of now, FedTool gives an 81% chance of a 25 bps hike in the next meeting scheduled for the end of July, however a lot will depend on the June inflation data. Nevertheless, everything seems to suggest that we are approaching the peak of this ending cycle, which obviously would be welcome news for such an interest rate-sensitive area of the market such as REITs.

{kind=link}

The markets foresee another 25 bps hike from the Fed (FedWatch Tool)

Beaten down, GMRE seems like a good bet

Now that we know why today could be a good time for investing in REITs in general, let’s see why GMRE seems to be a good bet on the sector.

Global Medical REIT is a small-cap company that focuses solely on healthcare properties. Investors that are familiar with the sector will instinctively assume that GMRE is down primarily for the same issues that have been afflicting other healthcare REITs such as Medical Properties Trust ( MPW ), however that is actually not the case. GMRE management is consciously avoiding overexposure to the hospital sector which is under tremendous pressure since the onset of the COVID pandemic and has spelled trouble for other bigger REITs specialized in big, centralized healthcare providers. However, the market clearly thinks the two companies are somewhat similar as evident by a general correlation between the two stocks.

YCharts

Global Medical REIT's management instead believes that there is a growing trend in the United States that favours de-centralized healthcare, small and mid-sized facilities located outside the big urban centers that can actually better serve the need for an ageing population. GMRE-owned centers are occupied primarily by physicians and are specialized into generic treatments such as gastroenterology, cardiovascular treatment, orthopedics, oncology and the likes.

Most of GMRE facilities are rented on a triple-net lease basis to single tenants. Triple-net leases are an attractive type of lease in which the tenant is actually responsible for basically all the maintenance and tax obligations relative to the building itself. Triple-net leases are generally very attractive as they offer long duration, stable growth (thanks to rent-escalators agreed upon signing the contract) and very low cost as explained above. If it’s true however that they offer stability and shelter from inflation hitting the costs (as they are minimal in nature), it is worth noting however that they can be a double edged sword as the long term nature of these contracts makes it impossible for the landlord to amend them higher to reflect a world with higher interest expenses.

June 2023 Investor Presentations

Over the years the company has built a portfolio of 188 buildings for a Gross Real Estate Value of $1.48 billion. As mentioned above the portfolio consists primarily of medical office buildings and inpatient rehab facilities (86%), while surgical hospitals account for only 6% of the portfolio. Every metric proves that the strategy of targeting suburban, mostly single-tenant facilities works wonderfully: at a time when many other medical REITs are struggling, GMRE can boost 97% occupancy rate, 6 years of weighted average lease term and very high-quality tenants with rent coverage of 4.1x. This last metric is of particular importance because it means that the rent expense basically represents only a quarter of the tenants’ earnings, which is very healthy as it leaves plenty of room for errors. Doctors are also great tenants in recessionary times as generally medical expenses are recession proof.

June 2023 Investor Presentations

The bull thesis

The bull case for GMRE is that a long-term normalization of interest-rates would translate into a reversal to the mean for its stock price, which is currently trading at a Price to FFO of just 9.74x, 34% less than the real estate sector as a whole based on Seeking Alpha compiled data. The company is basically trading at the same level it reached 3 years ago, with the difference that its yearly revenue is almost 50% higher and the FFO grew 120% since then. Historical valuation for the stock was also much higher as between 2017 and 2021 (before the crash) the company averaged a P/FFO of over 17. Therefore, the current price is clearly discounted both compared to the sector as well as with historical trends. Given that I usually aim at a return of 10% for my positions, GMRE appears to be positioned to beat that as almost all the growth is already priced into the dividend, and some capital gains could be unlocked by a repricing higher if interest rates will go lower.

Based on historical performance and considering only 2.1% weighted average rent escalations currently in place for existing contracts, I don’t believe that GMRE can be a reliable dividend growth story, considering that since 2017 the quarterly dividend has only grown about 5% from $0.20 to $0.21. Nevertheless, as the stock has been severely beaten down over the past 18 months or so, the current yield stands at an amazing 9.5% which does not need basically any growth to represent a nice payout while waiting for some capital gains to materialize.

Naturally, as with every investment comes some risk. First and foremost, as previously mentioned GMRE is a small-cap stock and as such is inherently riskier than larger peers, more than ever by being a REIT: scale matters when a lot of borrowing has to be done as part of normal business operations. Interest rates that will stay higher for longer (2+ years) will definitely impact the thesis as eventually the current fixed-rate debt, which is 80% of the total debt on the balance sheet, will need to be refinanced at higher rates. But as I will explain that does not seem the more likely scenario. A potential slowing of the job market coupled with a recession could be risky for the stock price, but the healthcare sector is generally resilient in recessionary times and rent escalators put in place in existing leases will offset the negative effects of higher interest rates.

On the dividend front, the massive yield seems to be rather safe despite a high payout ratio of 92% (TTM data). The primary reason is that as I explained above the tenant base is of very high quality and should be generally reliable even during recessions, while triple-net leases are known for their stability. Nevertheless, investors should bear in mind that a high payout ratio does not leave a lot of room for errors in case interest expenses rise much further and stay high for many years to come.

High interest rates are raising expenses

The company’s debt profile seems also well managed. Being a small-cap GMRE clearly has more difficulty than other larger peers to access cheaper capital funding, nevertheless the company has about $701 million of total gross debt, of which about 80% is fixed rate and the weighted average maturity is 3.7 years for an average weighted interest rate of 4.28%. Not the cheapest, however still healthy considering that interest expenses in the latest quarter amounted to just $8.3 million, well covered by the $15.1 million in Funds from Operations. Moreover, the company has great visibility into the next 5 years as many contracts are very long term. In absence of renewals or acquisitions, the current noncancelable contracts have been summarized by the company in the latest SEC filing.

Annual cash to be received by GMRE on existing leases (May 2023 10-Q filing)

In addition, management is trying to mitigate the impact of the floating rate debt by disposing some of the assets that are tied to it. In the latest earnings call , management called out a target of about $90 million of sales at a weighted average cap rate between 6% and 6.5% that would cut in half the current variable rate debt.

Key takeaways

Global Medical REIT seems to me like a great opportunity as an entry point into the sector. It appears to me that the market has erroneously bundled the stock together with other peers that are more clearly going through a rough patch, while GMRE is enjoying a very stable, very high quality tenancy base.

High interest rates are definitely hurting the company and there is no escape from it, however only 20% of the debt has a variable interest rate and management is actively mitigating its impact by selling some assets and paying it down. The risks here seem to be very well rewarded by a 9.5% dividend yield and a very good chance of some capital gain as well in the longer term while waiting for the interest rate hiking cycle to stop, and eventually even to reverse. As with every small-cap I would encourage investors to further mitigate the risks limiting their portfolio exposure to smaller or more speculative businesses.

For further details see:

Lock In A 9.5% Yield With Global Medical REIT