L - Loews - Not Yet Investable Remains A Hold For 2023

Summary

- While Loews has at least outperformed the market by 0.1% including dividends over the past months since November 3rd, my stance of "HOLD" continues to be correct.

- While the company may be interesting at the right time and valuation, that time is far from the current price - and this forms my current thesis on the company.

- Loews remains a "HOLD" - but here is my company thesis for 2023.

Dear Readers/Followers,

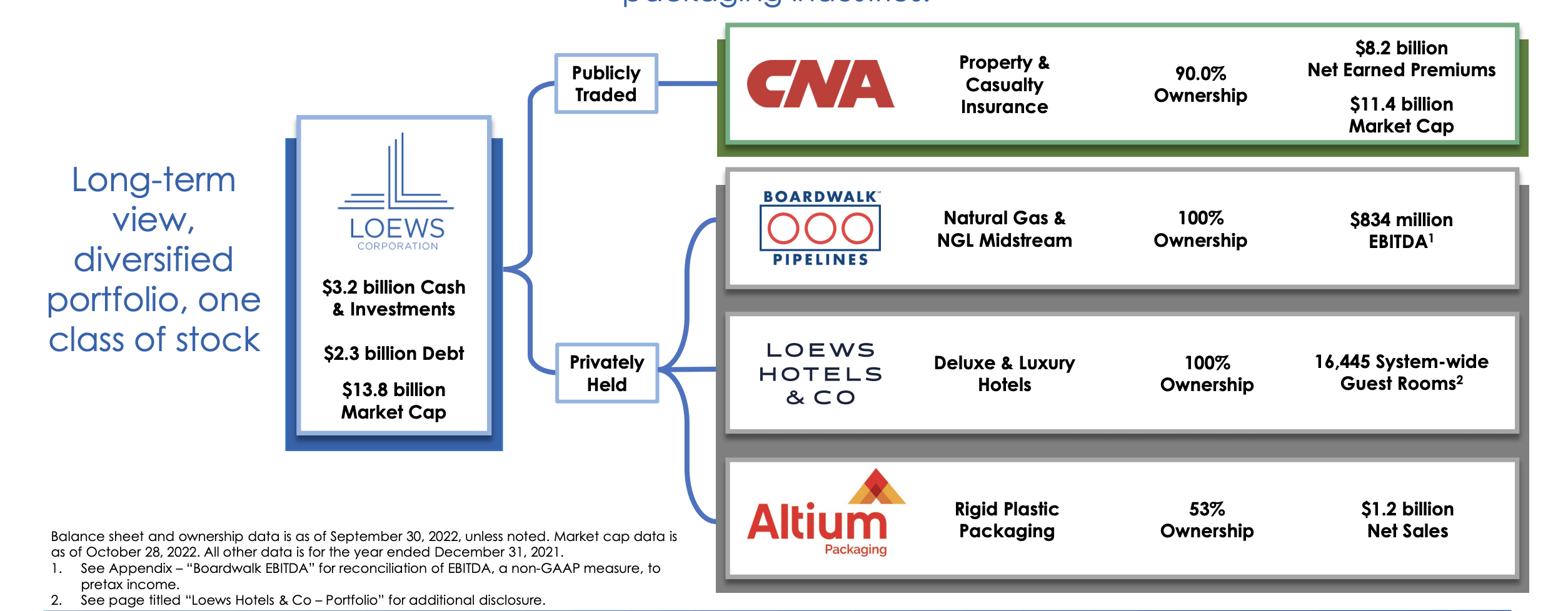

Loews ( L ) isn't a bad company, just a bad valuation. There are a few companies like this - undercovered "Niche" businesses, in this case, it being a P&C insurer in addition to its other business segments. Unlike some Niche businesses, Loews does offer us a dividend for investing in the company, even if that dividend is really quite low - currently, it's 0.42%.

However, the company does come with a solid A-rating for its business and has a non-trivial market cap of $14B. It has low debt and very solid operations overall.

Let's revisit Loews and let me give you my thesis for 2023.

Loews' - An investment for 2023?

I'm not at all opposed to investing in low-dividend companies. I've recently pushed plenty of capital both on the private and corporate side into Tomra ( OTCPK:TMRAY ), and that dividend is below 1.5%. But when I do invest in businesses such as that, I do want the opportunity for significant outperformance to be there to make up for that lack. Loews has traditionally, for as long as I've covered the company, lacked exactly this undervaluation and opportunity.

It's my stance that this continues to be the case here, despite positive results for the company's various segments.

The financial performance for the latest quarter showed highlights of improved underwriting income at the core segment, CNA, and improved results for the hotels. However, there were some losses in the LP, common stock investment, and sales of fixed income due to macro, which no company was really safe from - not even the best and largest of AA-rated reinsurers and global insurers.

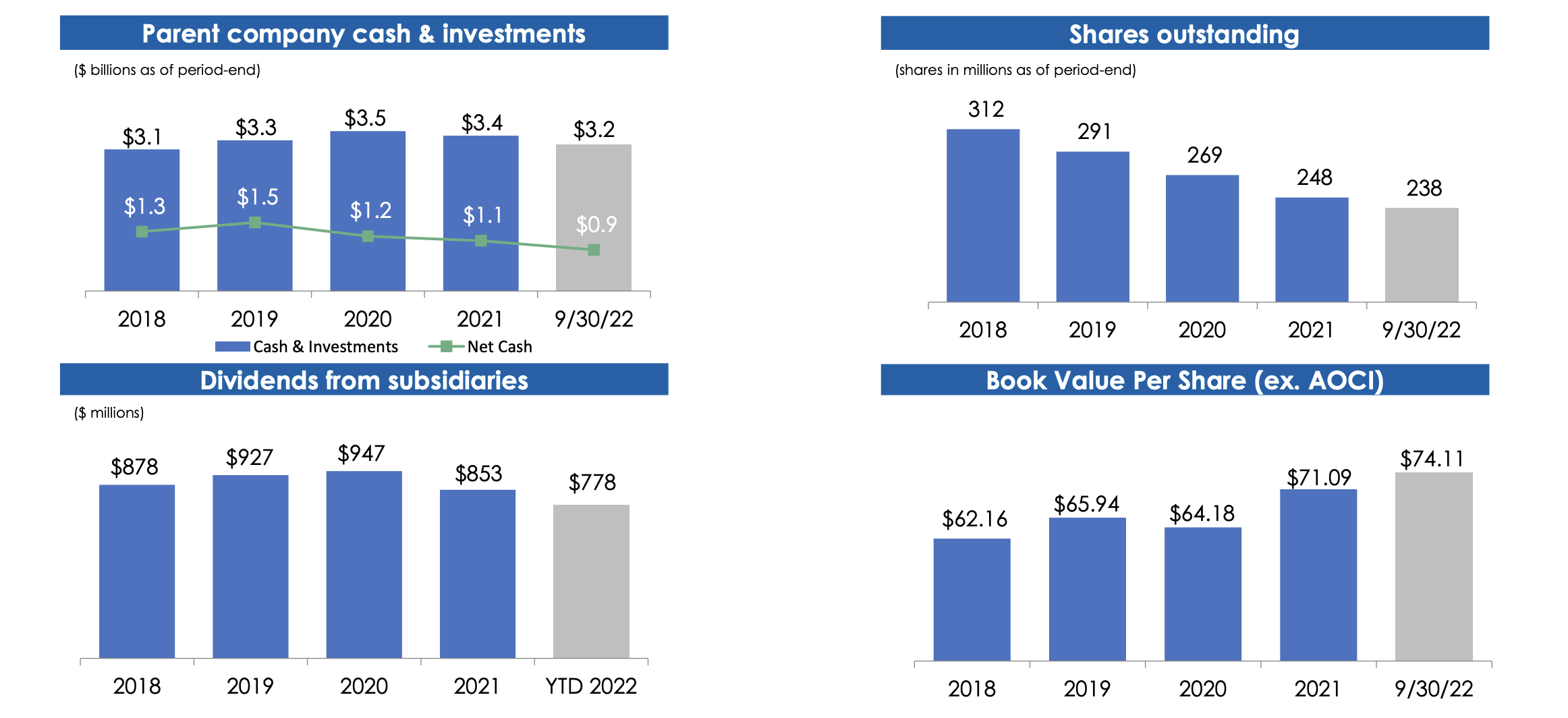

Loews took advantage of what they viewed as undervaluation (though they don't necessarily agree), and bought back 4.1M shares of Loews, as well as 700,000 shares of CNA back at $26M, which together with the Loews buyback is around $250M. Loews also got around $97M from the various subsidiaries it operates.

Like some Scandinavian investment companies, Loews is primarily looking at the collective book value/share of its portfolio compared to what the stock is trading at. Excluding AOCI, the company's BV at the latest quarterly report came in at around $74.11. The fact that the company as of today still hasn't cracked the $60 mark suggests that Loews is trading at a substantial discount to fair value at this time.

{kind=link}

No one is arguing against the company's fundamentals. They're conservative, the management is quite obviously capable, knowing how to allocate capital, with overall strong liquidity. The management of Loews as a company isn't in question, as I'm sure the management does quite well for themselves. That, however, is not the same as the company being a good investment. The company bounces up and down like a JoJo in terms of earnings. Stability is not really heard of here, and while things have gone well here, at the levels we're looking at right now (book value or not), investors have typically been left with RoR to not exactly be happy with. Also, during times of several years, this company is an investment that has generated almost no RoR at all, while at the same market, the market is up well into double digits.

That's a bit of a problem here.

Part of the issue here is the mixing of companies and ideas under one roof. If it was just the P&C company, I would know easier how to properly value it. It might be that CNA is the better investment here. For the past few years, the company has increased its focus on buybacks and BV/share, which has trended in the right direction for certain.

{kind=link}

The company's underlying operations, especially that of CNA remain qualitative. The combined ratio is even better than some of the larger ones, trending towards the sub-90% in 2Q22. None of the company's subsidiaries are in any sort of financial turmoil or trouble, also reflected by the company's strong credit rating - currently A-rated by S&P Global.

The company does have volatile exposure to segments like lodging and pipelines - two areas of business that have traditionally seen some fairly amazing levels of volatility. It's not as though packaging (Altium), with its input dependencies and SCM problems, has exactly been massively stable either.

In the end, this business doesn't have fundamental problems - but investing in it, despite the BV/share argument, remains a tricky business because it's relatively difficult to put an expectation on what you could make in the medium term. If this was another BV-focused business like Investor AB ( OTCPK:IVSXF ), where I own over $80,000 worth of common shares, I would be a lot more comfortable, because the yield is almost 6x as high, yet the company shares the "well managed" portion of the business with Loews, no doubt about it. Some readers have said, that I don't know how to value or approach businesses like this, but I don't think that's quite true. I think any business with this sort of EPS volatility, no matter how stable the underlying businesses can be argued to be, should be careful when looked at.

{kind=link}

The company has a relatively unique strategy, which is clear once you look at the very flat yield and dividend for Loews. The strategy consists of repurchases, first of all, before investing in the existing subsidiaries using the profits, and third, acquiring new subsidiaries for the business that delivers more growth, allowing more share buybacks, and so forth. This has resulted in Loews retiring nearly 38% of its common shares in less than 9 years, which is extremely impressive, and also the core reason for the climb in BV/share we've been seeing, now pushing above $70/share.

Loews' Valuation for 2023

So, as I wrote earlier - Loews has very interesting trends that remind me of some of my more volatile EU investments, without actually being that massively volatile of an investment (in results, not in valuation).

However, the main challenge that I see with Loews is the trickiness of valuation. A common misconception for this business is that just because the BV is /share, that's where the share price should be. That's just not how it works. I invest in over 15 investment companies and I follow BV/share trends in more than 7 different countries. There are businesses that more or less follow BV/share on a 1:1 basis, and where an investment in a sub-BV/share value is a good investment. But statistically, as I've seen it, that's less than 10% of the selection of the companies I've looked at - and Loews unfortunately, at least not at this time, is not one of them.

This company has gone from being underfollowed to not being followed at all. There are no longer S&P Global analysts or FactSet analysts that consider Loews relevant enough to be followed. This could mean the company could be a bit of a "sleeper" sort of investment - and at the right price, I may indeed be convinced that this is the case.

Just not here, and not at this current price.

All in all, it's hard to shift from the picture where Loews is a company that continually calls to investors for attention, pointing to some very great fundamentals, but that in the end continually and equally fails to actually convince investors of its quality.

Dividends further enhance this problematic picture. At times, I would consider Loews interesting, if the dividend had been above 2% or so, which would make the company somewhat easier to hold during the time it could appreciate to reflect its buyback activities.

I'm going to say again that the company's subsidiaries are some very well-managed businesses, and it goes almost against my fundamentals to keep my "HOLD" stance on Loews, because...after all, it's an A-rated sound business with a dividend. But the way that the business is run isn't necessarily the most advantageous or profitable for investors - especially not with the high-volatility segments of natgas, lodging and insurance as sort of the core of the business. It may be a sound long-term investment if you're willing to wait for the company to compound value by continuing to buyback shares and generate outperformance in such a manner - but at the same time, that would mean that any capital invested here is not able to be invested in other companies.

Companies that do have dividends, that do have valuation at an appealing level, and that do have a combined upside here. I believe this is the reason that Loews, despite its size, is so underfollowed and in the words of some Loews bulls, "underappreciated".

Yes, Loews continues to be underappreciated - but I believe there are strong reasons for this.

My recent PT was $49/share, which comes to around 66% of the current BV/share. What I want would be a 30% discount to the company's BV/share, and therefore I'm going to slightly allow for this to adjust - but even at that valuation, I would still need to look at what the market offers. This also goes in line with peers on an international basis, where I want discounts of 10-40% on BV/share in investment companies. Only the storied Investor AB gets a 100%, 1:1 ratio from me, and that Investment company basically owns large swathes of the entire national economy here in my home country.

Loews is a comparatively Niche business that owns 3 arms in volatile spaces - it's not worth 1:1.

Here is my updated Loews thesis.

Thesis

My updated thesis on Loews is:

- Loews is still a quality business with expertly-managed subsidiaries with through-cyclic earnings stability. The fundamentals here are excellent, and therefore, at the right price, it's a "BUY" even without a potential solid yield - it just needs to be cheap enough.

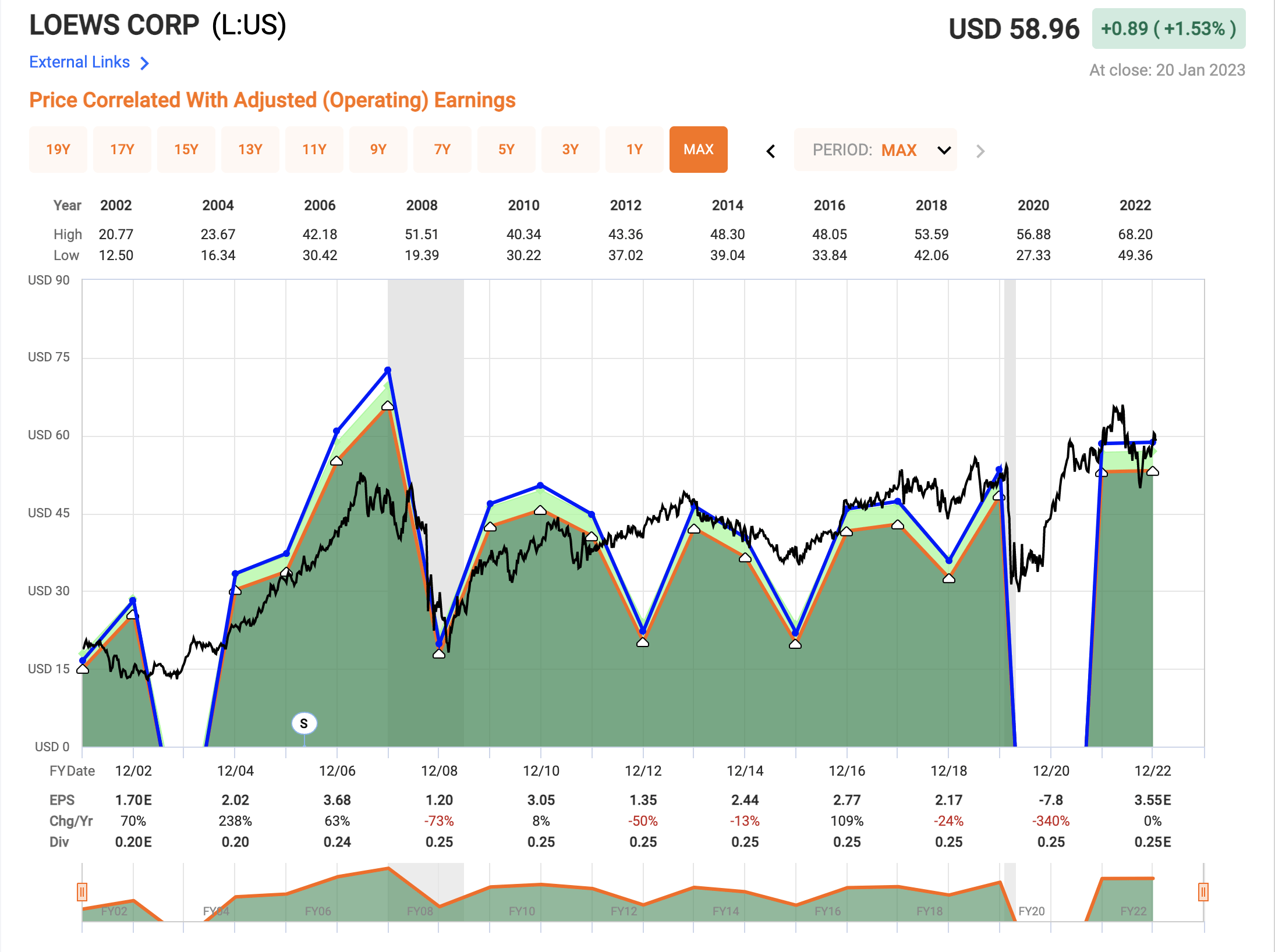

- This company is still overvalued. At any time, when you bought the company at 17-19X P/E, the company has delivered substandard, or below-market returns. The same goes true in some cases for the 15x+ P/E.

- Therefore, my stance is "HOLD" - I'll wait until we're back below $52/share, based on today's book value, and I would want a 30% discount to BV to go in here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Most of the boxes checked here, but there are still some issues - I say "HOLD".

For further details see:

Loews - Not Yet Investable, Remains A Hold For 2023