LOMA - Loma Negra: Going Strong In 2023 Thanks To High Local Cement Demand

2023-10-11 01:35:11 ET

Summary

- Cement demand in Argentina has been high in recent months, and 2023 is on pace to be the second-best year for the sector in terms of volumes.

- Loma Negra is the largest local cement maker and is trading at an EV/adjusted EBITDA ratio of 3.1x on a TTM basis.

- In my view, adjusted EBITDA for 2023 is likely to surpass $200 million despite the second part of the year being softer.

- The company has a strong balance sheet, and the dividend yield would be around 8% even if dividend payments get cut in half.

Introduction

Many investors have been avoiding Argentina lately due to the triple-digit percentage inflation, depreciating currency, and political turmoil. Yet, I think there are some compelling investment opportunities in the country and one company that recently caught my attention is cement producer Loma Negra ( LOMA ) due to its 15.9% dividend yield on a TTM basis. While the high dividend yield seems unsustainable, cement demand in Argentina has been strong in 2023 and the company has a low debt load, about half of which is in local currency. In my view, Loma Negra could book an EBITDA of above $200 million in 2023 and my rating on the stock is a speculative buy. Let’s review.

Overview of the business and financials

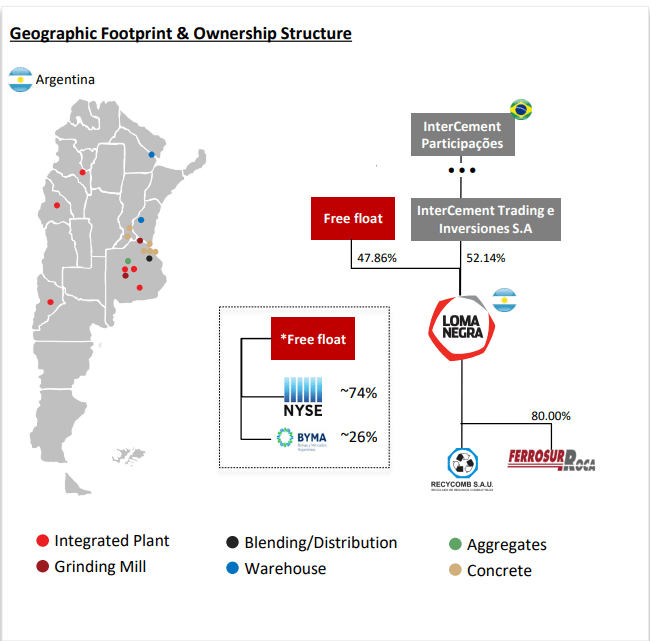

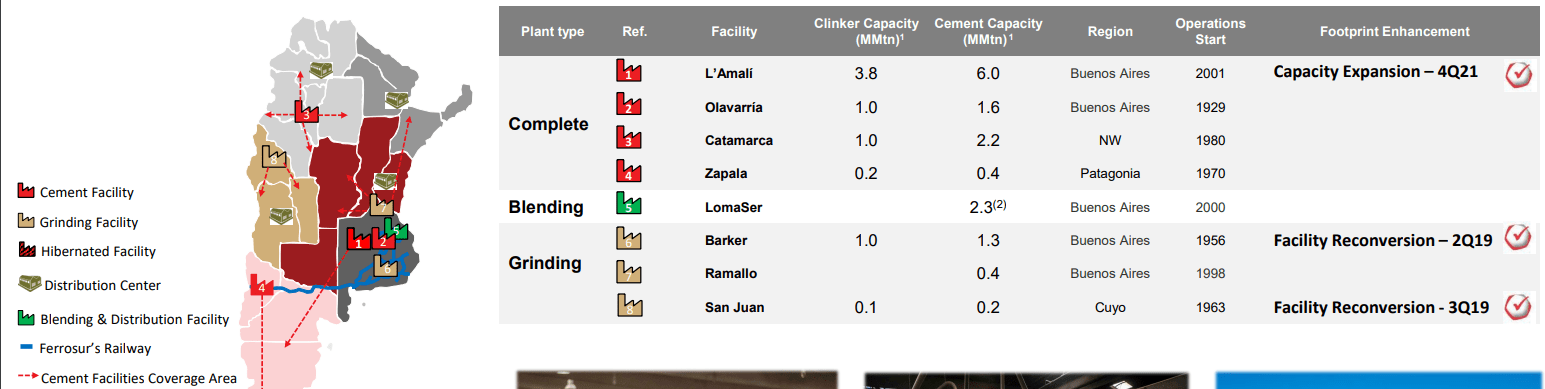

Loma Negra was established in 1926 and is the largest cement and concrete producer in Argentina, with a market share of close to 50% and an annual cement production capacity of 14.4 Mt. The company has a network of eight cement plants and seven concrete plants across the country, 3,200 km of railway concession, and a waste recycling company focused on the production of alternative fuels. It also owns La Preferida de Olavarria quarry in Buenos Aires Province, making it a vertically integrated cement company. Loma Negra’s L’Amali facility is the largest cement plant in Argentina with a production capacity of 6 Mt of cement and the company invested over $300 million to build a second line there in 2021. Loma Negra’s majority shareholder is Brazilian cement maker InterCement, which is owned by Brazilian conglomerate Mover Participacoes (formerly known as Camargo Corea). Loma Negra is listed in Argentina and the USA, and its free float is close to 48%.

{kind=link}

{kind=link}

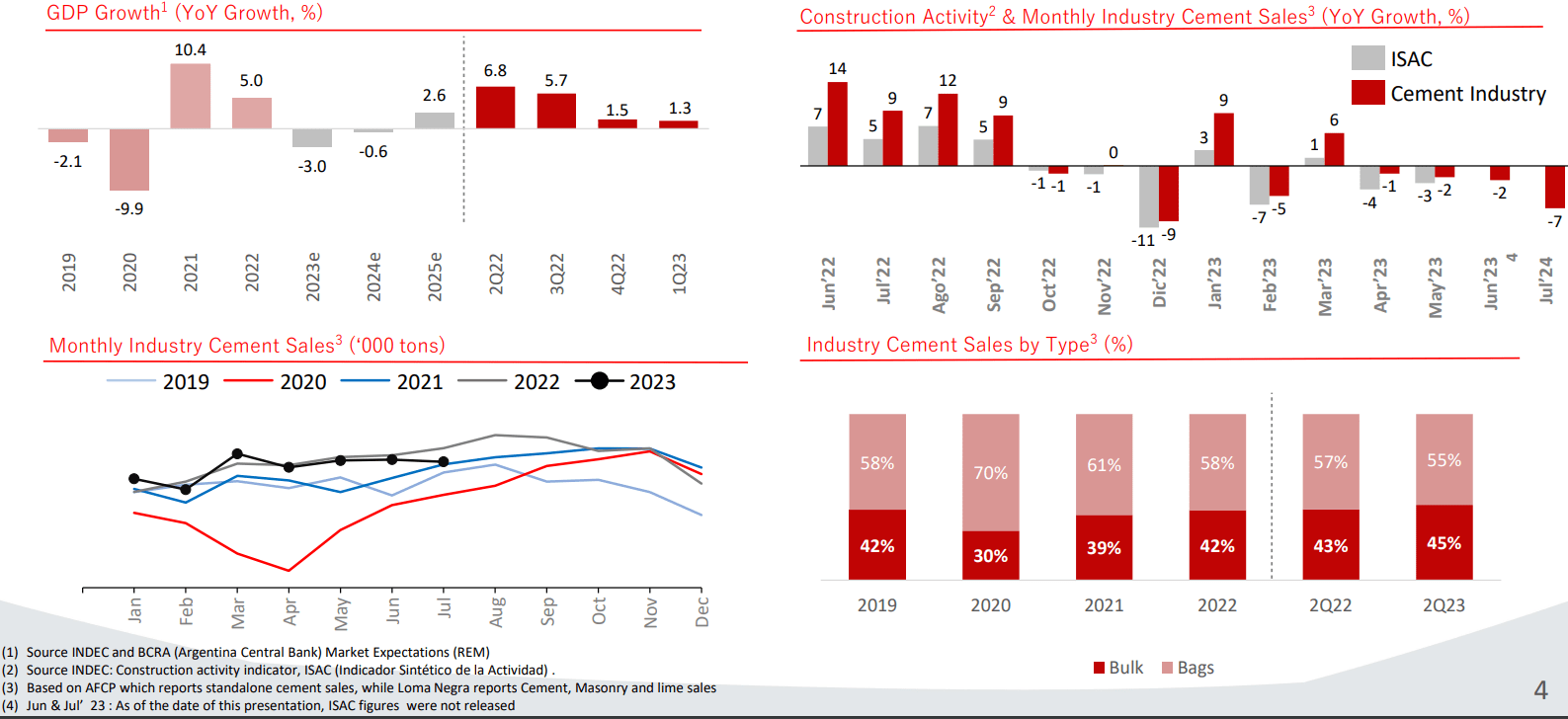

Looking at the cement market in Argentina, the majority of demand comes from individuals who usually gradually buy bags of cement to build or improve their homes, just like in many other countries in Latin America. There is strong brand loyalty here and imports are almost non-existent as cement is one of those products which are economically unfeasible to transport over long distances due to the cost-to-weight ratio. Just like in other Latin American countries, cement sales in Argentina reached record levels in 2022 following the end of COVID-19 restrictions as a result of economic growth and pent-up demand. While the market started to cool off in late 2022, demand has been resilient over the past several months and I expect cement sales in Argentina to remain above pre-pandemic levels in the foreseeable future.

{kind=link}

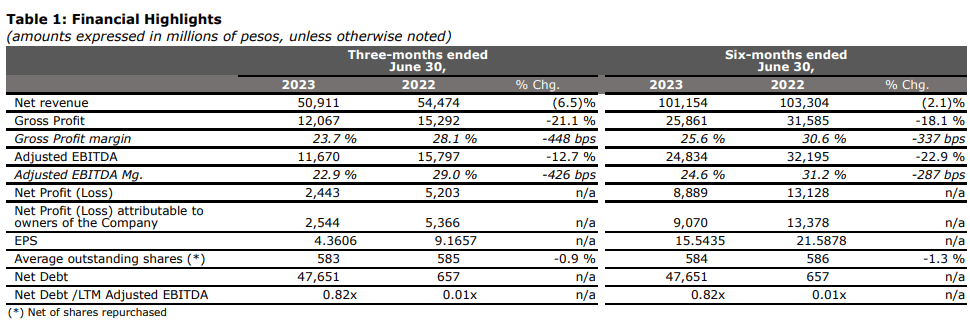

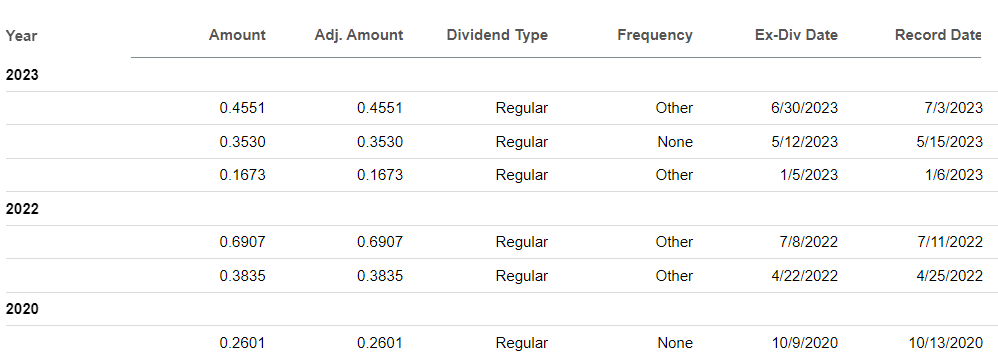

Turning our attention to the latest available results for Loma Negra, I think that Q2 2023 was a decent quarter as sales volumes of cement, masonry, and lime inched down by just 3.6% to 1.6 million tons while net revenue went down by 6.5% to 50.9 billion pesos ($206 million) due to a decline in bagged cement sales and lower selling prices. While the adjusted EBITDA margin decreased by 426 bps to 22.9%, adjusted EBITDA measured in US dollars remained flat at a level of $63 million. That being said, I find it concerning that the net debt/LTM adjusted EBITDA ratio soared to 0.82x from 0.01x a year earlier and 0.37x at the end of 2022. A major reason for this was dividend payments as Loma Negra has distributed around $120 million in three dividends in 2023 to date. During H1 2023, free cash flow was 12.4 billion pesos ($58.3 million).

{kind=link}

{kind=link}

{kind=link}

Turning our attention to the balance sheet, net debt stood at 47.7 billion pesos ($186 million) at the end of June 2023 and was up by about $77 million in a single quarter. While the net debt is rising rapidly, I think that it’s still at low levels and a silver lining here is that almost half of Loma Negra’s $268 million total debt is in Argentinean pesos. With many financial experts expecting the value of the Argentinean peso to keep falling against the US dollar over the coming years, I think that Loma Negra is in a better position to pay off its debts compared to many other local companies. In addition, the company placed during June a $71.7 million US dollar bond maturing in Q4 2025 at an interest rate of 6.5%, proving that it still has access to relatively cheap debt.

Loma Negra

Looking at what to expect for the future, I think that financial results for the second part of 2023 are likely to be weaker compared to the ones for the first half of the year as Argentina’s GDP growth is slowing down and this is likely to negatively affect cement sales. In addition, Loma Negra forecast lower cement demand ahead of the October 22 Presidential elections (see slide 13 here ). That being said, the company expects 2023 to be the second-best year for the local cement sector in terms of sales volumes and in view of this, I think that adjusted EBITDA in US dollars for the year is likely to surpass $200 million. Yet, the current dividend yield seems unsustainable in the long run, and I expect it to drop to about 7-10% by the end of 2024.

Turning our attention to the valuation, Loma Negra has an enterprise value of $903 million as of the time of writing and the company is trading at an EV/adjusted EBITDA ratio of 3.1x on a TTM basis. In my view, Loma Negra should be worth at least 5x EV/adjusted EBITDA considering Argentinean cement demand has been resilient post-COVID and the company has a solid balance sheet. This is equal to around $10.90 per ADR and translates into an upside potential of 77.5%.

Looking at the downside risks, I think the major one is that I could be over-optimistic about cement demand in Argentina over the coming months. It’s possible that local cement sales drop significantly in the near future if Argentina's GDP growth rate continues to decline over the next few months. Another risk here is that the company’s debt climbs to unsustainable levels if Loma Negra continues to distribute dividends that its free cash flow can’t support.

Investor takeaway

Cement demand in Argentina has been high in 2023, though not as much as last year. This sector is among the few bright spots in the country’s economy and among the key beneficiaries of this is Loma Negra, whose adjusted EBITDA stands at $293 million on a TTM basis. The company has a strong balance sheet, and the dividend yield would be around 8% even if dividend payments get cut in half. Cement demand in Argentina has been resilient over the past several months, and I think that Loma Negra’s adjusted EBITDA for 2023 could top $200 million.

For further details see:

Loma Negra: Going Strong In 2023 Thanks To High Local Cement Demand