LNSTY - London Stock Exchange: Attractive Stock Market Operator But Too Expensive Here

2023-11-14 22:05:20 ET

Summary

- London Stock Exchange Group is a smaller stock market operator facing competition from other major financial hubs in Europe.

- LSEG has solid fundamentals, including a high gross margin and operations in key areas.

- However, LSEG's margins are significantly lower than its competitors, making it less attractive for investment compared to Deutsche Börse.

Dear readers/followers,

In this article, I'm going to be adding another stock market operator to my coverage spectrum. We're talking about the London Stock Exchange Group ( LNSTY ) ((LSEG)). The company is smaller than some of its competitors, and I argue that with Brexit London doesn't have the same clout as it once did, with Paris, Frankfurt, Amsterdam, and Brussels slowly taking over as some of the major financial hubs. However, I have been increasing my allocation to the overall stock market operators and stock markets in Europe over the past few years - London and England are the latest of this.

London Stock Exchange Group PLC trades under the native ticker LSEG - and this is also the one that I invest in if I am buying the company. So let's see what we have going for us here because this is a qualitative business that for the past 5 months has gone really nowhere.

LSEG has some things going against it - but also some significant advantages to consider.

Let's look at what LSEG has to offer investors, and if it could be an interesting play.

London Stock Exchange Group - The fundamentals

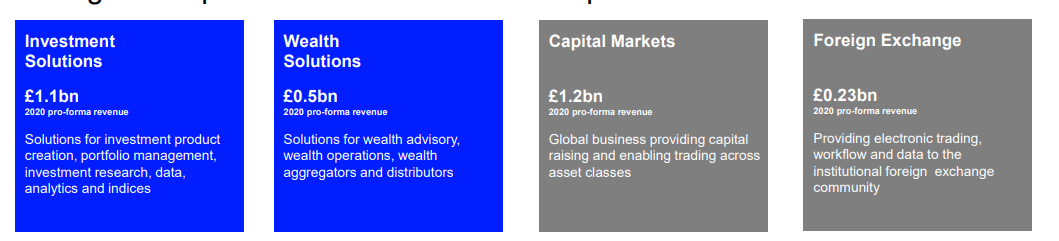

On the surface of it, LSEG has some advantages worth considering. We're talking a solid gross margin of 86%+ and operations in 4 key areas, 2 of which are above a £1B level.

{kind=link}

The fact is, this is one of the oldest stock market companies on the planet. The exchange was founded over 222 years ago, but the company we're writing about was founded just before the financial crisis in 2007, 16 years ago. The exchange at the time acquired the Milan-based Borsa Italiana and in conjunction with this formed the current LSEG company.

Much like other stock market companies, LSEG services the entire value chain with synergies between the offered products and services. LSEG has exposure to capital markets, data & analytics, as well as post-trade services. It's not as strong as Deutsche Börse (DBOEY) and with as leading market positions given Clearstream and other services, but it's still an interesting and profitable operation.

{kind=link}

Much like Deutsche, LSEG expects growth in the high digits from its investment solutions, double-digit from risk solutions for their party, almost no growth (1-2% negative historically) from Trading and banking solutions given the poor margins, and around 4-6% from Data & Analytics, one of its core segments.

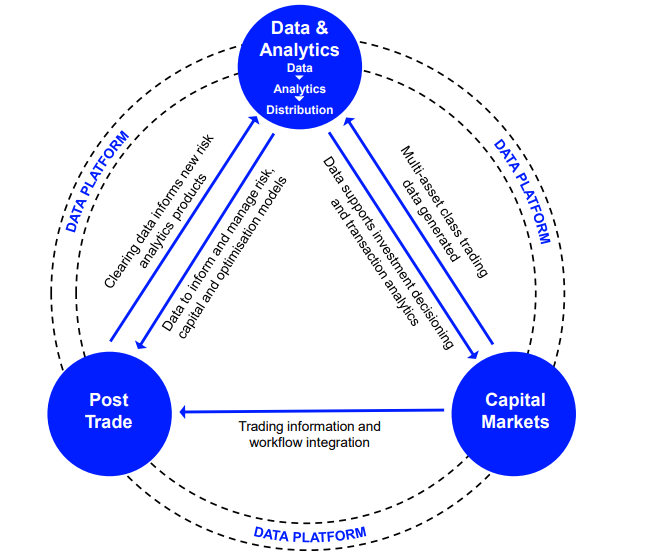

Here is how the company's business works...

{kind=link}

...and LSEG essentially does benchmark rates, indices and analytics, workflow and data services (workspace/Eikon), Yield book fixed income analytics, and other strategies - to end users like Asset owners, managers, banks, exchanges, regulators, and servicers.

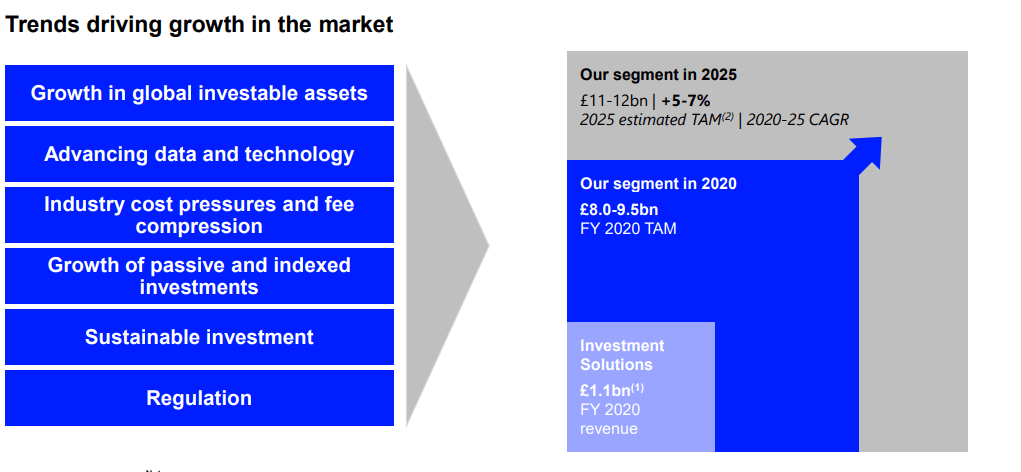

The company's expectation for growth comes from global growth in investable assets, a higher focus on data, cost pressure, and fee compression (benefitting large players). The company's TAM in 2020 was around £9.5B on the high side, with a TAM expectation of £12B in 2025E, a CAGR of 5-7%. These numbers and expectations are for the investment arm.

{kind=link}

The company has a strong portfolio of investment services and products, including FTSE Russel, WM/REFINITIV, Lipper, Workspace, StarMine, and others. Over 99.5% of the company's revenue in these segments is recurring, and over 60% is out of the Americas, with an appealing revenue stream that's 45%+ subscription-based.

Overall, the company's business model seems to be working well.

{kind=link}

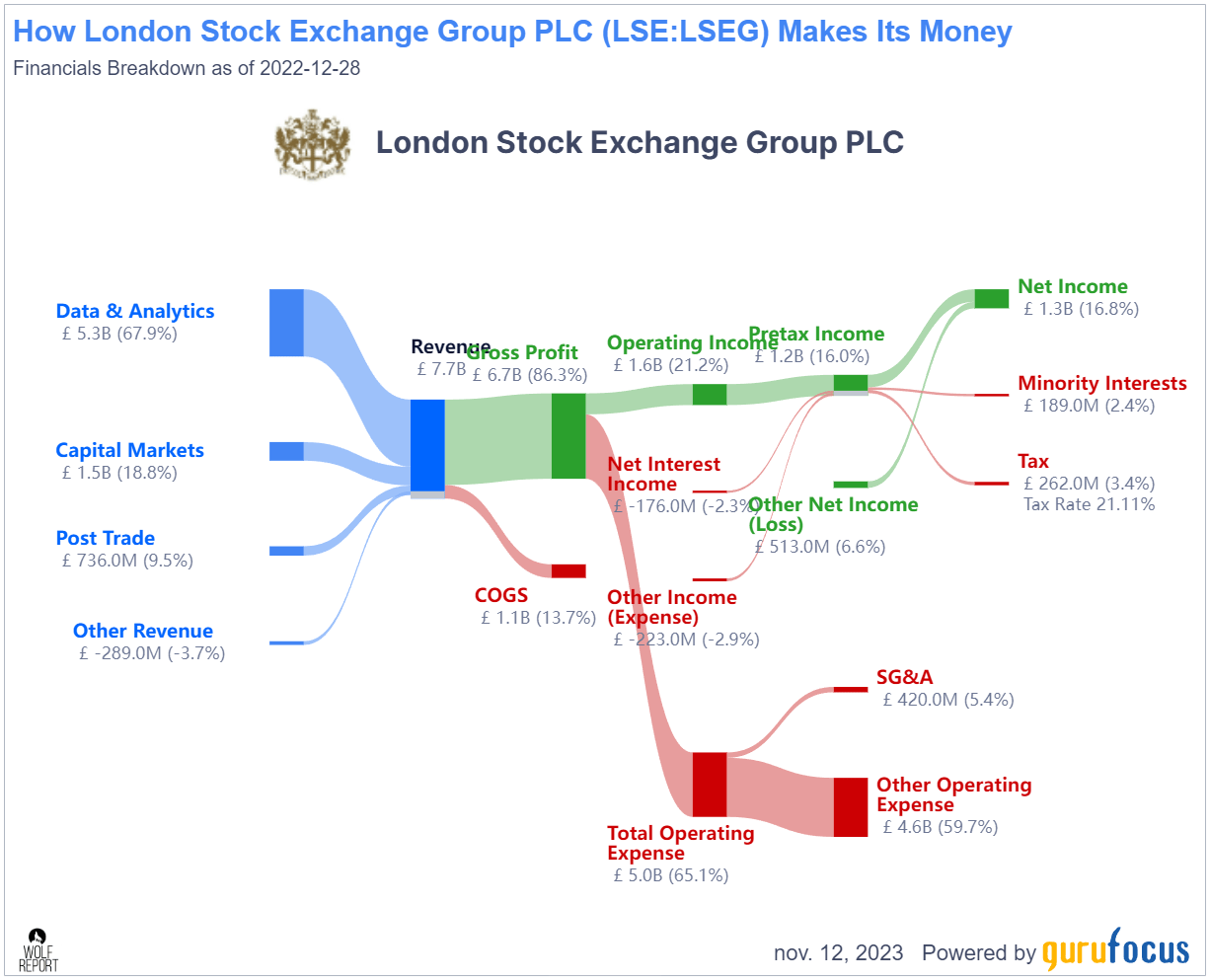

However, also where the cracks in the company's model are coming. Because compared to Deutsche Börse, a far "better" company in terms of margins, the company's margins are around 60% of that of Deutsche Börse in terms of percentage. DB has a net income margin of almost 29%, and LSEG manages less than 17%. That's more than a small difference, and it's why my investment in this segment is heavily tiered towards the Deutsche Börse in Europe in terms of stock market operators.

Some shareholders have even, relatively recently, sold shares of LSEG. Thomson Reuters (TRI) sold 35M worth of shares in the company, which is part of what is putting pressure on the company here.

These sorts of companies have very strong fundamentals, and LSEG is no different here. The company has a credit rating of A, a market cap of over £44B, and very low debt of sub-22% in terms of long-term debt to capital. The company, however, does not offer a yield above 1.5%, currently coming in at 1.3%.

In fact, I would say and will show you in the valuation section, that while there is conceivable upside to the stock, I would say that DB1 has better upside and potential every day of the week. Also, Stock market operators tend not to do well during recessions or downturns, especially when premiumized.

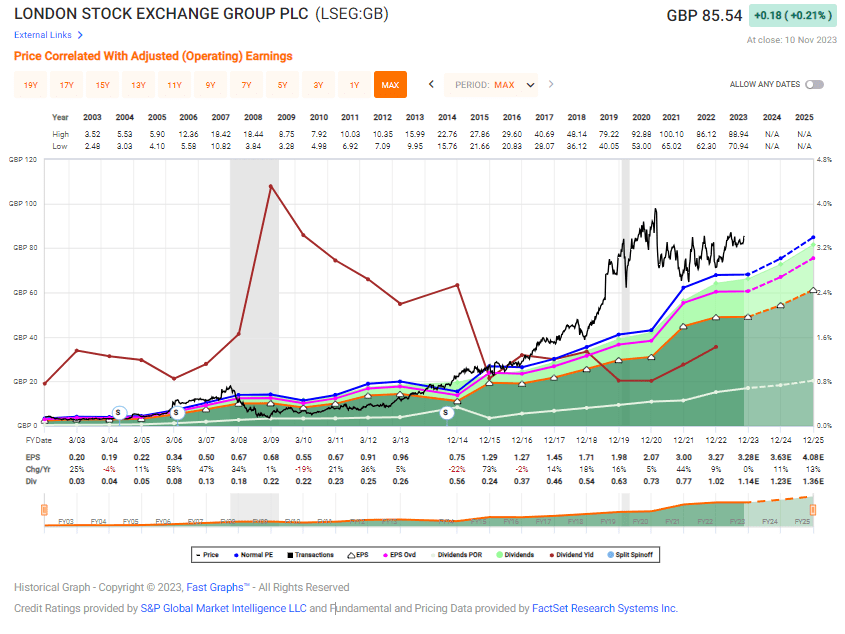

Take a look at what happened when the company traded at more or less exactly the same level it does today before the GFC.

{kind=link}

Even if the company's latest set of results were positive, and they were - with total income growth (excl. recoveries) of 8%, which means that the company is on track to deliver 2023E targets with strength from all segments (particularly post-trade, which saw a growth of 17%), I would still be somewhat cautious here. The company reiterated guidance with margin targets and CapEx targets in line.

However, this does not change the fact that net margins are well below average in the capital markets industry. it also does not change the fact that the company is seeing severe declines in the operating margin and decline in fundamentals. The company's share price, despite these challenges, is at a 2-year high or close to it, and the P/S ratio is also relatively high. Consistent revenue/top-line growth does not help much when the bottom line continues to be sub-par.

Stock market operators are, overall, very attractive investments to make for the long term - but only at the right price. If you'd invested at close to the highs, you'd be negative in terms of returns here.

Let me show you in valuation how I would go about forecasting LSEG here, and why it's not as high a "BUY" as some of the peers here.

London Stock Exchange - Plenty to like fundamentally, but the valuation is about £20/share too high

LSEG trades at an average of around 26x P/E, which is 6-7x P/E above its 20-year normalized P/E of 20x. At the 20x P/E level, the estimated RoR even with a 10.8% annualized EPS growth rate comes to less than 2.5% annualized RoR. Forecasting it at 26-28x P/E, which is what is required to see substantial profit here, results in around 15-16% annualized RoR.

Given that DB1, Deutsche Börse, trades at 17.7x and trades at an upside of 15.28% to 20x, which is in line with its historical average, has almost 1% higher yield, a better credit rating at AA-, better leverage at almost 10% lower, better set of services and products, and a higher historical rate of hitting growth targets. Also, DB1 is estimated to grow at less than half of that of LSEG - and conservative targets are, as I see it, the way to go here.

S&P Global analysts have 17 following the company with financial targets, which range from £81 on the low side and £115/share on the high side with an average of £98. That would imply a 28-29x P/E for this company, which I do not view as likely in the long term.

Out of 17, only 5 analysts are at "BUY" with most either at "HOLD" or not having an opinion on the stock, which doesn't fill me with confidence.

At this time, I would say that the most realistic and positive expectation if you were to invest today would be an annualized RoR of around 4-7% - that's not enough for me, and it shouldn't be enough for you in a market that pays 5-6% risk-free if you look at bond markets, money market funds, and pref stocks today.

Because of this, I am entering this investment and this thesis with a PT of below £80/share for the native, and a conservative "HOLD" rating.

Here is my thesis for the company as it stands today.

Thesis

- London Stock Exchange Group is one of the largest stock market operators in all of Europe. The company is fundamentally qualitative and isn't going anywhere. At the right valuation, I would say this is certainly a "BUY" with a double-digit upside.

- Unfortunately at this price, it takes a 26-28x P/E to see a double-digit 15%+ annualized RoR upside - which is well above the average , and well above the historical average of 19-20x P/E here. I view this valuation as unsustainable in the longer term.

- I give the company a "HOLD" rating here and set my PT at around £72/share. It's a conservative one, but there are better companies to invest in here, even in this sector.

Remember, I'm all about :1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

In short, I do not view the upside as high enough here to interest me compared to far more attractively valued peers. I give the company a "HOLD" here.

For further details see:

London Stock Exchange: Attractive Stock Market Operator, But Too Expensive Here