RSSS - Long Cast Advisers - Research Solutions: Gross Profit Growing Faster Than Revenues

Summary

- The dynamics of “what I look for” applies to our newer investment in Research Solutions, which has about $10M cash and operates at roughly breakeven as it invests in growth.

- In the most recent quarter, RSSS reported its highest quarterly EBITDA in the company’s history.

- Having observed RSSS over the last year and watched it skillfully adapt and upgrade, I’ve gained more comfort in their ability to address the threats and opportunities ahead and have increased our position.

The following segment was excerpted from this fund letter .

Research Solutions ( RSSS )

The dynamics of “what I look for” applies to our newer investment in RSSS, which has about $10M cash and operates at roughly breakeven as it invests in growth.

We’ve owned a small position simply on the change in management to a team I've invested with in the past (new CEO and CFO as of October 2021, which conforms with the company’s F2Q22 period), and I've grown the position as my comfort with their efforts have increased.

RSSS has historically been in the article sourcing business and if you go back far enough, to when it was called Derycz Scientific (named for the founder, Peter Derycz), the company was built around finding, copying and mailing research articles paired with a printing business that provided glossy-ied article reprints for marketing purposes. Over the years it morphed into an online marketplace for transacting PDFs of articles and more recently into a subscription platform for sourcing and managing articles all online.

Why does this business exist? Think about music for a second and listening to pirated copies vs legal licensed music. Large companies in the R&D or intellectual property business need access to research articles both for the purpose of discovery and also for citations. It creates risk for them to not pay for rights to these articles, so they access them using companies like RSSS, which essentially bulk break publishing catalogs in order to sell or rent rights to individual articles needed by their clients.

RSSS CEO Roy Olivier and CFO Bill Nurthen had previously run ARIS , whose core business was “bulk breaking” parts catalogs for automotive and power sports dealers, and they built an entire business around this. Though this is a different industry, the machinations are not dissimilar. (We owned ARIS at ~$3.50 / share, and it sold in 2017 for $7.10 cash, and I wrote a lot about it on my blog . )

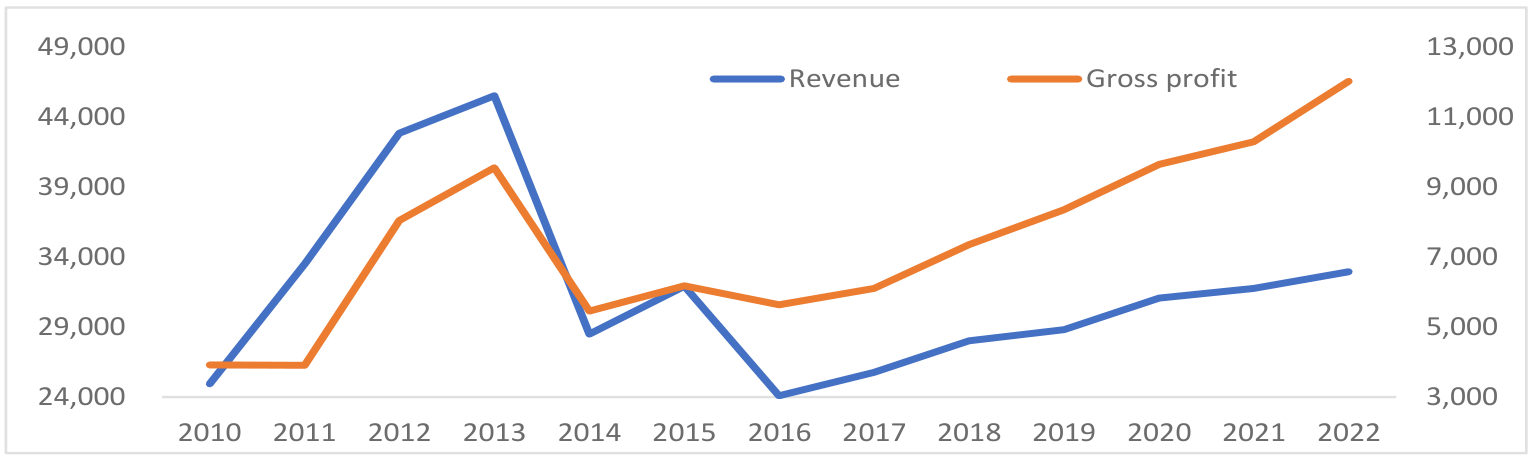

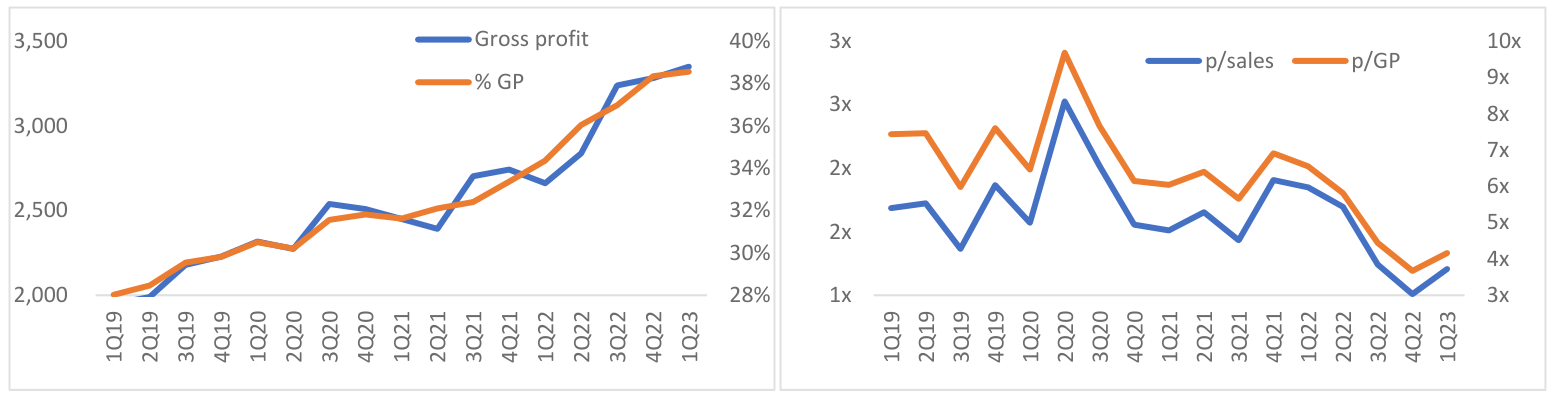

RSSS has long made money selling individual articles – a lumpy lower margin business – and has been transitioning from a per article revenue business to one that provides access to the catalog on a subscription basis, a bit of a self-cannibalization that trades revenue for gross profit. One can observe gross profit growing faster than revenues as this strategy has unfolded.

{kind=link}

I believe the company deserves a higher multiple for their success in implementing the plan, which started under the prior CEO and continues at a faster pace under new management, who I think are more capable and experienced. Yet, since the management change, the market has discounted the valuation despite observed acceleration of growth in gross profit and margins.

I feel comfortable disagreeing with the market here on the discount. But it begs the question, who is selling, and what am I missing? A bit more history. The company IPO’ed in Jan ’09 through the founder’s brother-in-law’s investment co “Bristol Investment Fund”. At the time, those two owned 66% of the company. Their ownership has dwindled over the years to 36% in ’16 and 22% at FY22 and in the intervening years, a “who’s who” of small cap funds (Samjo, 12 West and currently Cove Street) have cycled in and out of the stock. I think a combination of continued BIL selling plus prior owner impatience might explain the availability of shares to purchase, driving down multiples despite recent growth. Macroeconomic conditions, which have weighed on all SaaS related multiples, also contributes no doubt to the recent discount.

{kind=link}

Changes in the industry might also contribute to multiple compression, but I feel equally comfortable disagreeing here. There is a trend in the industry towards “ open access ” , a movement pushing for the end of paywalls for scientific research articles conducted with state or federal funding, which sounds ominous for this business (link has 8-minute video that does a very good putting all this into context, albeit focused on the academic and not commercial space). But if you watch the video note at 5:45 it talks about the need for “new tools for mining research” and at 6:20 “the slow movement of scientific cultural practices … scientists are conservative in changing practices.”

If you think open access will destroy this business overnight, don’t buy the stock. If you think there will be a slow rate of destruction, and possibly none at all in the near term, there’s a case to be made for owning this.

More widely, I think there’s a compelling case for the potential transition not just from an article seller to a subscription platform, but from a subscription platform that supplies articles to one that helps manage and mine them in an open access world. This is the “optionality” on a potentially bigger outcome, and where I think the new management offers compelling value. As an anecdote, a friend works in an industry that requires access to these types of articles and warned about open access, then agreed with the importance of having a management platform in an open access world. Obviously, a single comment like this isn’t foundational, but it gets to the point that the world isn’t black and white; the blurred areas is where markets can be made.

RSSS has announced its intention to pursue some smaller acquisitions and I think in a few years they likely sell to PE, as ARIS did. In the most recent quarter (F1Q23 for the period ended 9/30/22) the company reported its highest quarterly EBITDA in the company’s history. While they won’t do that every quarter, I expect them to build on this base, b/c that’s what better management does.

One other thing better management does is implement a long-term incentive plan that’s aligned with shareholders, which is what this management team did in August ‘22, via a vesting schedule that starts at prices 50% above the current price.

As I said, we’ve owned a small position primarily on my experience with management. Having observed the company over the last year and watched it skillfully adapt and upgrade, I’ve gained more comfort in their ability to address the threats and opportunities ahead and have increased our position. I’m continuing to learn more about the business and will attend some industry conferences in 1H23, whence I’ll offer additional updates.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Long Cast Advisers - Research Solutions: Gross Profit Growing Faster Than Revenues