LBPH - Longboard Pharmaceuticals: Undervalued Arena Spin-Out Has 2 Data Catalysts Due In 2023

2023-05-22 16:29:06 ET

Summary

- Longboard looks like an intriguing play within the biotech sector.

- The company was spun out of Arena Pharmaceuticals in 2020 - Arena was subsequently acquired by Pfizer in a $6.7bn deal.

- Arena's lead candidate Etrasimod was an S1P Modulator indicated for autoimmune conditions. Longboard is developing a candidate with a similar MoA targeting CNS conditions.

- Its other candidate is indicated for seizures and progressing through a Phase 1a/2b study - clinical data for both candidates arrives this year.

- A market cap valuation of ~$210m at the time of writing seems to undervalue this currently financially secure biotech, whose management has a track record of success.

Investment Overview

Even in the current age of technology driven data and analytics, the drug development industry is a hit and miss business, where speculation, serendipity and even luck play a role in the discovery of new therapies with blockbuster (>$1bn per annum) revenue potential.

With the right drug and some good stewardship around guiding it through the clinical trial process, a small biotech can deliver outstanding returns for investors - just as Arena Pharmaceuticals did when it was acquired by Pharma giant Pfizer ( PFE ) for $6.7bn in December 2021, Pfizer paying a 90% premium to traded share price to gain access to lead drug candidate Etrasimod.

Etrasimod was an oral Sphingosine-1-phosphate ("S1P") Receptor Modulator indicated for immune-mediated inflammatory diseases, already in Phase 3 studies in ulcerative colitis ("UC") and atopic dermatitis ("AD"), and under Pfizer's stewardship a New Drug Application ("NDA") has been submitted to the FDA for approval in UC, based on data from two key late stage trials that met all primary and secondary endpoints. Pfizer believes the drug could eventually pull in revenues >$3bn per annum.

Before Arena was acquired, back in January 2020, management opted to "spin-out" a portfolio of "centrally acting product candidates designed to be highly selective for specific G protein-coupled receptors ("GPCRs")" into a new entity called Longboard Pharmaceuticals ( LBPH ) - the subject of this post.

Longboard was launched with $56m of funding, with former Arena Chief Financial Officer ("CFO") Kevin Lind appointed CEO. According to Longboard's Q123 10Q submission (quarterly report):

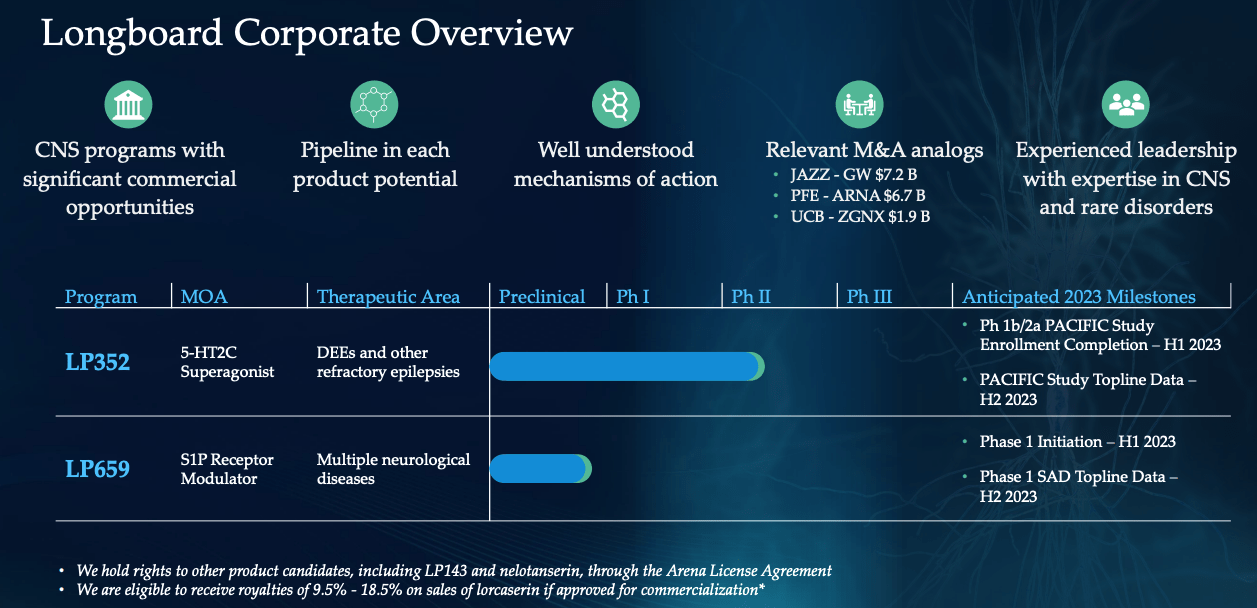

We are currently focused on developing the following product candidates in our pipeline, both of which are licensed from Arena:

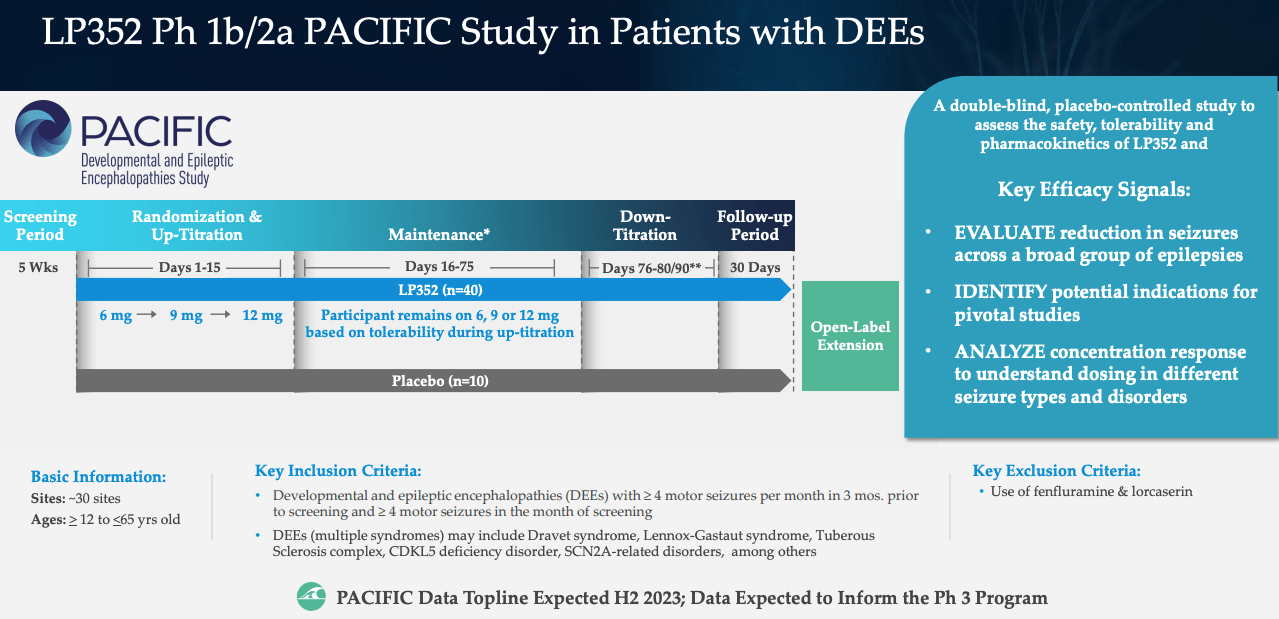

•LP352, an oral, centrally acting, 5-hydroxytryptamine 2C receptor subtype (5-HT2C) superagonist, currently in a Phase 1b/2a clinical trial (the PACIFIC Study) expected to evaluate 50 participants ages 12 to 65 years old with developmental and epileptic encephalopathies (DEEs), which may include Dravet syndrome, Lennox-Gastaut syndrome (LGS), tuberous sclerosis complex (TSC), CDKL5 deficiency disorder (CDD), and SCN2A-related disorders, among others, with study enrollment expected to be completed in the first half of 2023 and topline data expected in the second half of 2023; and

•LP659, a centrally acting, sphingosine-1-phosphate (S1P) receptor subtypes 1 and 5 (S1P1,5) receptor modulator, for which we have submitted an investigational new drug application ("IND") to the FDA after incorporating input from a pre-IND meeting with the FDA, and for which we anticipate initiating a Phase 1 clinical study in healthy volunteers in the first half of 2023 and anticipate topline single ascending dose (SAD) data in the second half of 2023.

Longboard also notes that:

Our small molecule product candidates were discovered out of the same platform at Arena that represents a culmination of more than 20 years of world-class GPCR research

The opportunity for investors is clear. Longboard's market cap is just ~$210m at the time of writing, with the share price trading at ~$9.25. Should the company be successful with either of its lead candidates, LP352, or LP659, it would open up a potentially blockbuster revenue opportunity in each market.

For context, Epidiolex, a cannabinoid seizure treatment that Jazz Pharmaceuticals ( JAZZ ) - my note here - acquired via its $7.6bn buyout of GW Pharmaceutical - earned $736m of revenues in 2022 in its approved indications of Lennox-Gastaut syndrome and Dravet syndrome in 2022, whilst LP659 - which has the same mechanism of action ("MoA") as Arena's Etrasimod, being an S1P receptor modulator - may be approvable in a wide range of neurological markets. Another member of the S1P drug class - Bristol Myers Squibb's Zeposia, approved to treat Multiple Sclerosis - earned >$250m of revenues in 2022, and is expected by management to drive >$3bn per annum in peak sales.

The question is whether Arena's leadership team can repeat the success of Etrasimod with these two earlier stage assets? If the two lead candidates live up to their preclinical data in the clinic, and progress into late stage studies, given the market opportunities, then Longboard stock ought to rise in value substantially to meet expectations of blockbuster sales.

Arena's stock was worth $50 per share immediately prior to its acquisition at $100 per share, so even pre-buyout the business was valued >$3bn, or >15x what Longboard is worth today.

Of course, with drug development being the hit and miss business it is, there is no guarantee that Longboard can match Arena's success and the presence of some of the same management team that helped develop Etrasimod may even being artificially inflating the value of the company's assets.

In order to find out which of these scenarios is true, clinical data is required, and luckily, shareholders are not expected to have to wait long for study results.

Longboard Portfolio Overview

{kind=link}

As we can see above - per a slide from a recent Longboard Corporate Presentation - for the 5-HT2C superagonist, LP352, management is enrolling patients in a Phase 1b/2a PACIFIC study, from which it hopes to share data this year, whilst for the S1P receptor modulator LP659 a first Phase 1 study will be initiated in H123, with topline data available in the second half of the year.

{kind=link}

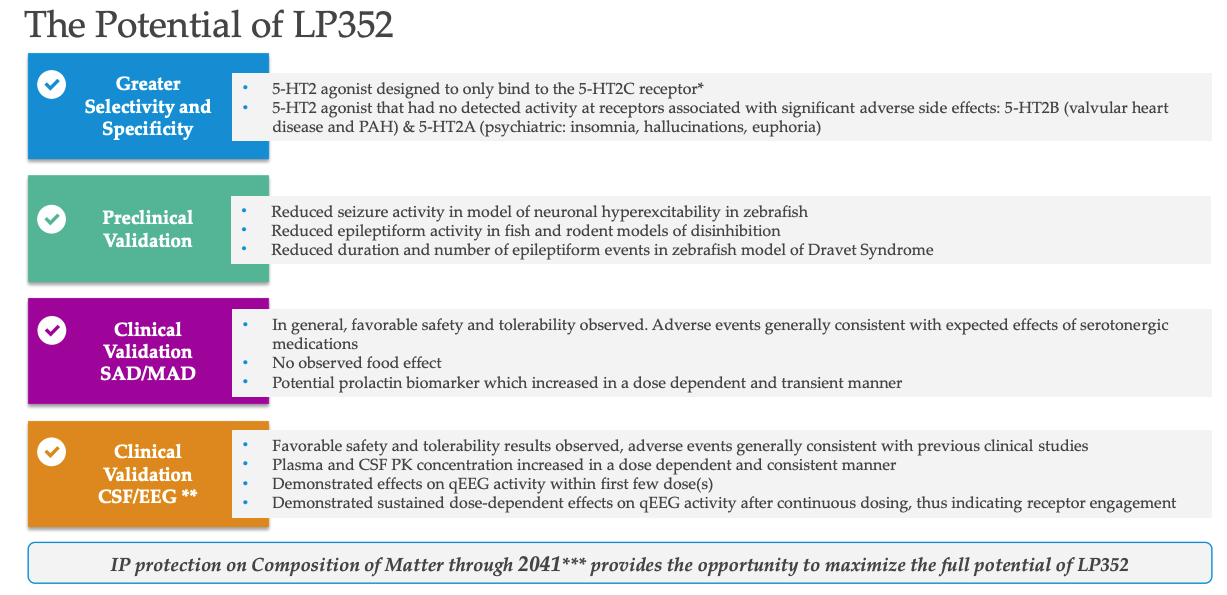

LP352 is a member of the 5-HT2 agonist drug class which also includes the approved drugs FINTEPLA (fenfluramine), developed by Zogenix before it was acquired by UCB in a $1.9bn deal, and forecast to make blockbuster sales, and BELVIQ (lorcaserin), a weight loss drug developed by Arena which was pulled from the market by Japanese Pharma Eisai in 2020 owing to concerns it may cause cancer.

As such it seems Longboard's challenge with LP352 is to ensure that it is safe - management says the drug has "greater selectivity and specificity" than its predecessors fenfluramine and lorcaserin, due to the fact it targets the 5-HT2C receptor subtype only, whilst the other two also have off-target activity against 5-HT2B and 5-HT2A, whose inhibition can lead to negative cardiac, pulmonary and psychiatric side-effects.

Longboard says there are >25 different Developmental and Epileptic Encephalopathy ("DEE") syndromes, of which only four have approved therapies, and suggests that the 21 uncatered for syndromes could add up to a larger market than the other four - i.e. substantially more than $1bn per annum based on Epidiolex sales alone (assuming it has <50% market share).

LP352 works by modulating hippocampal pyramidal GABAergic neurons to suppress hyperexcitability, although most of the evidence supporting the MoA is preclinical and based on mice and zebrafish models. A Phase 1 study in healthy volunteers has also been conducted, however, with "favourable safety and tolerability results" observed, and management concluding:

We believe the data suggest that LP352 engaged neurotransmitter systems and altered the electroencephalogram ("EEG") spectrum.

{kind=link}

The next stage would be to establish proof of concept in a population of patients with DEEs, and that is what the Phase 1/2 PACIFIC study is designed to do.

The initial topline data from the study is expected H223, before an open label extension period begins with no placebo arm. That readout would seem to be a critical share price catalyst for Longboard - positive data and the prospect of designing a pivotal study would surely result in a doubling of the biotech's valuation, as even when heavily risk adjusted, the future sales potential could be considered >$500m at the least.

On the other hand, problems may be detected, such as a lack of efficacy, given the dose level is restricted by safety concerns associated with prior 5-HT2C inhibitors, or safety concerns themselves. Longboard has built a strong network of patient advocacy agencies that will help to spread the word to physicians should the data look positive, and LP352 has patent protection through to 2041, management says.

In summary, in my view the opportunity here may be considered more promising than usual for a lower valued biotech given management's prior track record of success in clinical studies (albeit with a different drug), the 20+years of R&D that led to the discovery of first Etrasimod, and now LP352, some promising preclinical data, and although funding is relatively low - $76m according to the latest corporate presentation - against a cash burn of only ~$12m in Q123 this seems a financially secure base.

LP659 - Next-Generation S1P Modulator

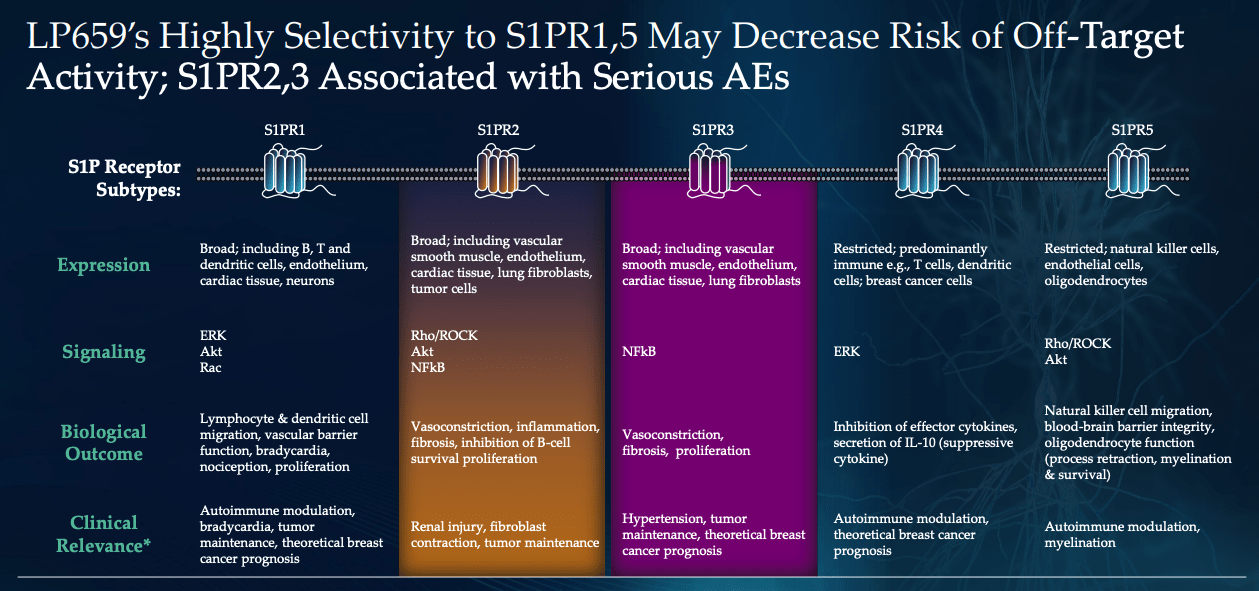

Similarly to LP352, it is the specificity and selectivity of LP659 that may hold the key to its success or otherwise. Apparently, LP659 is "highly selective" to the target, S1P1,5, but has no impact on S1P2,3, implying it may have less negative off-target activity than prior candidates within this drug class.

LP659 differentiation to other S1P modulators (Longboard presentation)

{kind=link}

Management is hopeful that the "high plain to plasma ratio" will allow LP659 to target a broad range of CNS conditions and again, it is good news for investors that first clinical data is promised for this year, even though the Phase 1 study has yet to be initiated.

The reality is that there is limited preclinical data available for a layman investor to gain much insight into how this drug may perform in a clinical setting - and there is plenty of competition in the form of four approved S1P modulators - fingolimod and siponimos - Novartis' Gilenya and Mayzent, ozanimod - BMY's Zeposia, and Johnson & Johnson's ( JNJ ) ponesimod. Arena management was able to deliver Etrasimod clinical data that stood comparison with any approved therapy in an intensely crowded market - Longboard's challenge is to do the same - if successful the upside potential could run into 4-digit percentages.

Risks & Concluding Thoughts - An Intriguing Opportunity From A Successful Core Management Team - With Clinical Validation To Come

From my perspective, I am somewhat surprised that a company spun out of Arena Pharmaceuticals - with two apparently exciting opportunities within drug classes that have delivered numerous approved drug products - is worth as little as <$215m market cap at the time of writing.

Longboard's stock price is actually up 168% on a year to date basis, so we can certainly say the stock price has momentum, although it is down 43% since shares hit all-time highs of >$16 after the company's launch.

It is tempting to wonder if Arena's management - perhaps even aware of impending M&A interest from a Big Pharma - was able to slip its candidates LP659 and LP352 out of the back door before any deal was done, reckoning that they might prove as successful in the clinic as Etrasimod was.

If that was the case, you could further make the case that the market has not fully appreciated the value of two next-generation assets within successful drug classes, and if that thesis appeals to you, buying stock today ahead of two key data readouts before the end of the year, that could have seismic implications for the share price, may seem like a sensible strategy.

Of course, there are several substantial risks to consider. Gaining an approval for one drug does not by any means suggest that your next candidate will be successful. By the law of averages, a Phase 1 stage drug has a less than one-in-five chance of making it all the way to an approval.

In LP352, it seems as though Longboard is battling a tricky safety profile, whilst with LP659 there is scarcely any preclinical data, let alone clinical data, plus a crowded field of pre-approved drugs in this class with very strong safety and efficacy profiles that may prove tricky to match.

Longboard is not cash rich - although I have complete confidence management will be able to raise a triple-digit-million sum at the market on good data from either of its upcoming data readouts, if the data does not support continuing clinical studies of either drug the share price will likely nose-dive in response. The good thing is that Longboard has two assets, both with pipeline-in-a-product potential, management believes, which hedges the risk somewhat.

Despite the risks of disappointing data in the short term, a lack of funding, the amount of progress that still needs to be made in the clinic, and the specific challenges of developing each drug candidate, however, based on my experience analysing biotech companies, Longboard strikes me as having two more-promising-than usual drug candidates, more financial stability, and a better track record of success than most other companies in this sector with a comparable valuation.

With two major data catalysts to come in 2023, I find myself tempted to take a speculative position in Longboard stock. Arena has been a leader in researching and developing G protein-coupled receptors for over 20 years, and this unheralded spin-out is valued substantially less than the opportunity in play, in my view, given the two decades of research that pre-empted the selection of the two lead candidates.

For further details see:

Longboard Pharmaceuticals: Undervalued Arena Spin-Out Has 2 Data Catalysts Due In 2023