KPTCY - Longleaf Partners International Fund Q2 2023 Commentary

2023-07-20 02:00:00 ET

Summary

- Longleaf Partners Funds is a suite of mutual funds and UCITS funds that Southeastern Asset Management, the investment advisor to the Longleaf Partners Funds, created in 1987 as a way for Southeastern employees to invest alongside their clients.

- The Fund’s ability to produce strong relative results is not predicated on a China market recovery.

- The Fund delivered a strong first half, despite relative macro headwinds, and with materially different return drivers than the index.

{kind=link}

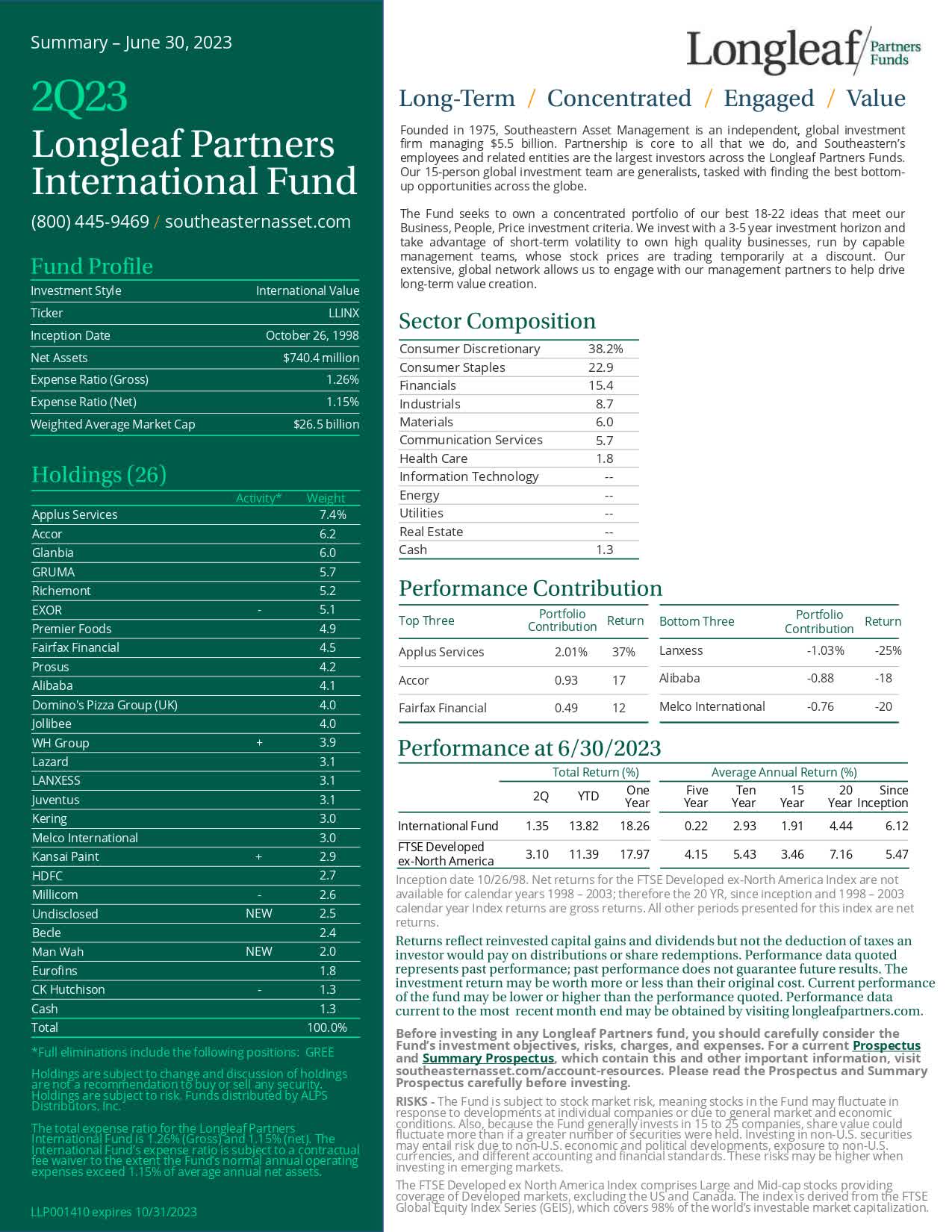

Fund Characteristics

| P/V Ratio |

| Mid-60s % |

| Cash |

| 1.3% |

| # of Holdings |

| 26 |

Annualized Total Return

| 2Q (%) |

| YTD (%) |

| 1 Year (%) |

| 3 Year (%) |

| 5 Year (%) |

| 10 Year (%) |

| Since Inception (%)* |

| International Fund |

| 1.35 |

| 13.82 |

| 18.26 |

| 4.62 |

| 0.22 |

| 2.93 |

| 6.12 |

| FTSE Developed ex-North America |

| 3.10 |

| 11.39 |

| 17.97 |

| 8.65 |

| 4.15 |

| 5.43 |

| 5.47 |

*Inception date 10/26/1998

Returns reflect reinvested capital gains and dividends but not the deduction of taxes an investor would pay on distributions or share redemptions. Performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by visiting southeasternasset.com . The prospectus expense ratio before waivers is 1.26%. The expense ratio is subject to a contractual fee waiver to the extent the Fund's normal operating expenses (excluding interest, taxes, brokerage commissions and extraordinary expenses) exceed 1.15% of average net assets per year.

Longleaf Partners International Fund added 1.35% in the second quarter, taking year-to-date (YTD) returns to 13.82% for the first half. While the portfolio's lack of exposure to Information Technology and overweight to Asian Consumer Discretionary weighed on results, the Fund outperformed the FTSE Developed-ex-North America Index in the first half. The second quarter saw a continuation of our European businesses driving positive returns as the market rewarded positive bottom-up operational and financial progress, while geopolitics and the slower consumption recovery in China remained a drag on the rest of the portfolio.

In Europe, most of our businesses delivered strong financial performance on the back of a challenging year in 2022, and our management teams continued to take steps to create value through intelligent capital allocation and strategic action to crystallize the value of whole businesses and/or underlying assets. Our businesses that have exposure to China (including German-listed business LANXESS ( LNXSF ) ( LNXSY )) were challenged in the quarter amid ongoing negative geopolitical sentiment and a slower-than-anticipated Covid reopening recovery, resulting in disappointing consumer spending. 70% of Chinese household assets are exposed to the property sector, which faces a continued downturn with property sales at 60% of pre-Covid levels. The re-opening boost is unlikely to be enough to reach the 5% growth target for the year. Beijing is taking notice and is expected to pass through policy responses. In the meantime, near-term share price weakness has created an opportunity for our management teams to go on offense. Alibaba ( BABA ) bought back $14 billion worth of shares in the last 14 months (with another $17 billion to go) and announced plans to break itself up into six different businesses to get the value recognized. Prosus ( PROSY ) ( PROSF ) similarly announced a transaction to simplify the business by removing the cross-holding structure with Naspers ( NPSNY ) ( NAPRF ) and has also bought back approximately one-quarter of its free float shares in the last 12 months since announcing its open-ended buyback program.

The Fund's ability to produce strong relative results is not predicated on a China market recovery. Our businesses have strong balance sheets and pricing power enabling them to navigate challenging external environments and consistently generate growing free cash flow coupons. This has translated into solid stock performance for most of our portfolio holdings. In cases where there is a persistent gap between price and intrinsic value, our management partners continue to use all the tools within their power to grow and recognize value via buybacks, spin-offs, and divestitures.

We encourage you to watch our video with Portfolio Managers John Woodman and Manish Sharma for a more detailed review of the quarter.

Contribution To Return

2Q Top Five

| Company Name |

| Total Return (%) |

| Contribution to Return (%) |

| Portfolio Weight (%) (6/30/23) |

| Applus Services |

| 37 |

| 2.01 |

| 7.4 |

| Accor |

| 17 |

| 0.93 |

| 6.2 |

| Fairfax Financial |

| 12 |

| 0.49 |

| 4.5 |

| EXOR |

| 8 |

| 0.47 |

| 5.1 |

| GRUMA |

| 9 |

| 0.45 |

| 5.7 |

2Q Bottom Five

| Company Name |

| Total Return (%) |

| Contribution to Return (%) |

| Portfolio Weight (%) (6/30/23) |

| LANXESS |

| -25 |

| -1.03 |

| 3.1 |

| Alibaba |

| -18 |

| -0.88 |

| 4.1 |

| Melco International |

| -20 |

| -0.76 |

| 3 |

| Millicom |

| -20 |

| -0.7 |

| 2.6 |

| Kering |

| -14 |

| -0.5 |

| 3 |

- Applus Services ( APLUF ) - Diversified Spanish testing inspection and certification ((TIC)) business Applus was the top contributor in the quarter and for the first half. In June, private equity firm Apollo Global made a $1.33 billion bid for the entire business, and there is rumored interest from additional private equity buyers for the company. Throughout our ownership period, we have been engaged with management and the board to encourage getting the value recognized, and the company bought back 10% of the market cap in the past year. Although we believe the Apollo bid undervalues Applus, the private equity interest highlights the strategic nature of this high-quality business within a structural growth industry. We remain closely engaged in this dynamic situation.

- Accor ( ACRFF ) ( ACCYY ) - French hospitality business Accor was another top performer in the quarter and YTD. Accor is a leading global hotel operator in Europe, Asia, and Latin America. The business lagged its North American peers given a slower post-Covid recovery in its key markets but today is reporting revenue-per-average-room (REVPAR) above pre-Covid levels, with strong pricing power and high occupancy rates. During Covid, management internally restructured the business, taking out €200 million in structural cost savings and reorganizing the business into luxury and lifestyle (trophy assets with well-established brands and a strong pipeline) and mid-scale and economy (a cash-generative franchise business). In the quarter, Accor released separate financials for each of these businesses, allowing the market to properly weigh the value of the two underlying businesses.

- LANXESS - German-listed specialty chemical company LANXESS was the top absolute and relative detractor after announcing a higher-than-expected profit warning in the quarter. The company has faced a triple whammy of industry-wide destocking, exposure to delayed demand recovery in China, and increased energy prices last year, leading to a stock of high-cost inventory that needed to be cleared. We believe the scale of the warning reflects management taking all the pain upfront to ensure it was a "one and done" warning, with the potential for the company to surprise on the upside in the second half. We are not relying upon a recovery in the second half, as there are signs of returning to a more normalized demand environment by the first half of 2024.

Portfolio Activity

In the second quarter, we initiated two new positions, added to Kansai Paint ( KSANF ) ( KPTCY ) (a new purchase in the first quarter), exited Gree, and trimmed a handful of positions. We initiated a purchase in a European-listed business that is a global industry leader and derives the majority of its value from its dominant market position in Asia. The company remains undisclosed while we build the position. We also bought Man Wah ( MAWHF ) ( MAWHY ), one of the leading functional sofa manufacturers in China, a company that we know well and own in our Asia Pacific strategy. Man Wah is the largest recliner sofa maker in China with more than 50% market share in a highly fragmented market. Its share price has been punished amid Chinese real estate weakness, but under the leadership of owner-operator Man Li Wong (who owns >60% of the business), the company has continued to take share and build scale that further strengthens its low-cost advantage over peers. Man Wah has a 6% dividend yield and has been buying back its shares at an 8x price to earnings (P/E). We funded the purchase by selling Gree, the largest air conditioning manufacturer in China, on the back of positive YTD performance driven by strong sales due to a heat wave in China.

We also increased our position in Kansai Paint, a global paint and coating manufacturer with market-leading positions in Japan and India. This is a high-quality industry staple business with no substitutes and strong pricing power in an oligopolistic market. Our management team, under the able leadership of Mori Kunishi-san, has been focused for the last three years on unwinding the complexity of the business by divesting sub-scale operations at value accretive prices, selling cross-holdings and owned real estate, and using the proceeds to buy back discounted Kansai Paint shares. We are excited to see the organization shift from a hierarchy to a meritocracy, and focus on margins, return on equity, and free cash flow generation.

Outlook

The Fund delivered a strong first half, despite relative macro headwinds, and with materially different return drivers than the index. We believe this puts the Fund in a strong position to deliver differentiated future returns. The research team has been busy evaluating existing holdings and identifying new opportunities, resulting in upgrades to the portfolio. Our management teams have been similarly busy, taking steps to get the underlying value of their businesses recognized. Following a period of mid-teens returns, the portfolio ended the quarter with a compelling price-to-value (P/V) ratio in the mid-60s%, indicating significant future potential upside.

See the following page for important disclosures.

Before investing in any Longleaf Partners Fund, you should carefully consider the Fund's investment objectives, risks, charges, and expenses. For a current Prospectus and Summary Prospectus, which contain this and other important information, visit https://southeaste rnasset.com/account - resources . Please read the Prospec tus and Summary Prospectus carefully before investing.

RISKS

The Longleaf Partners International Fund is subject to stock market risk, meaning stocks in the Fund may fluctuate in response to developments at individual companies or due to general market and economic conditions. Also, because the Fund generally invests in 15 to 25 companies, share value could fluctuate more than if a greater number of securities were held. Investing in non-U.S. securities may entail risk due to non-US economic and political developments, exposure to non-US currencies, and different accounting and financial standards. These risks may be higher when investing in emerging markets.

The FTSE Developed ex-North America Index comprises Large and Mid cap stocks providing coverage of Developed markets, excluding the US and Canada. The index is derived from the FTSE Global Equity Index Series (GEIS), which covers 98% of the world's investable market capitalization.

P/V ("price to value") is a calculation that compares the prices of the stocks in a portfolio to Southeastern's appraisal of their intrinsic values. The ratio represents a single data point about a Fund and should not be construed as something more. P/V does not guarantee future results, and we caution investors not to give this calculation undue weight.

Free Cash Flow ((FCF)) is a measure of a company's ability to generate the cash flow necessary to maintain operations. Generally, it is calculated as operating cash flow minus capital expenditures.

Price / Earnings (P/E) is the ratio of a company's share price compared to its earnings per share.

Return on equity (ROE) is a measure of profitability that calculates how many dollars of profit a company generates with each dollar of shareholders' equity.

As of June 30, 2023, the top ten holdings for the Longleaf Partners International Fund: Applus Services, 7.4%;

Accor, 6.2%; Glanbia, 6%; GRUMA, 5.7%; Richemont, 5.2%; EXOR, 5.1%; Premier Foods, 4.9%; Fairfax Financial, 4.5%; Prosus, 4.2%, and Alibaba, 4.1%. Fund holdings are subject to change and holdings discussions are not recommendations to buy or sell any security. Current and future holdings are subject to risk.

Funds distributed by ALPS Distributors, Inc.

LLP001445

Expires 10/31/2023

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Longleaf Partners International Fund Q2 2023 Commentary