LZAGF - Lonza Group: Painful Cut In Guidance Still A Buy

2023-07-24 05:26:00 ET

Summary

- Lonza Group lowered its 2023 guidance, reducing its forecast and EBITDA margin outlook. This cut implied an H2 margin deterioration.

- Despite that, the company's 2024 outlook remains positive, and we see support for the Contract Development and Manufacturing Organization industry.

- Lonza is cash positive, with an expected EPS growth of 17% until 2026. Our buy rating is then confirmed.

A month ago, we updated our Lonza Group AG (LZAGY) investment thesis. We provided a follow-up note called " Our Thoughts Pre Capital Market Day ," in which we reported a positive company view for the medium-term horizon. In 2023, we were not very optimistic about the Swiss CDMO player and lowered our expectations. Despite that, we decided to maintain our buy rating target based on: 1) EPS growth thanks to a supportive CAGR of the CDMO market , which is forecasted to grow at a double-digit rate, 2) disciplined CAPEX with IRR > 15% and ROIC > 30%, 3) cost pass-through policy, and 4) higher DPS year-on-year. With supportive Q1 financial figures and a new buyback program , we were positively looking at the Capital Market Day scheduled for October 17th . Last week, the company released its Q2 update, quoting our previous publication, "It was an excellent move to forecast higher operating costs and lower Lonza margins for the current year. "

Q2 results

After the Q1 release, Lonza confirmed its 2023 outlook, maintaining an EBITDA margin forecast between 30% and 31%, with a high single-digit top-line sales growth.

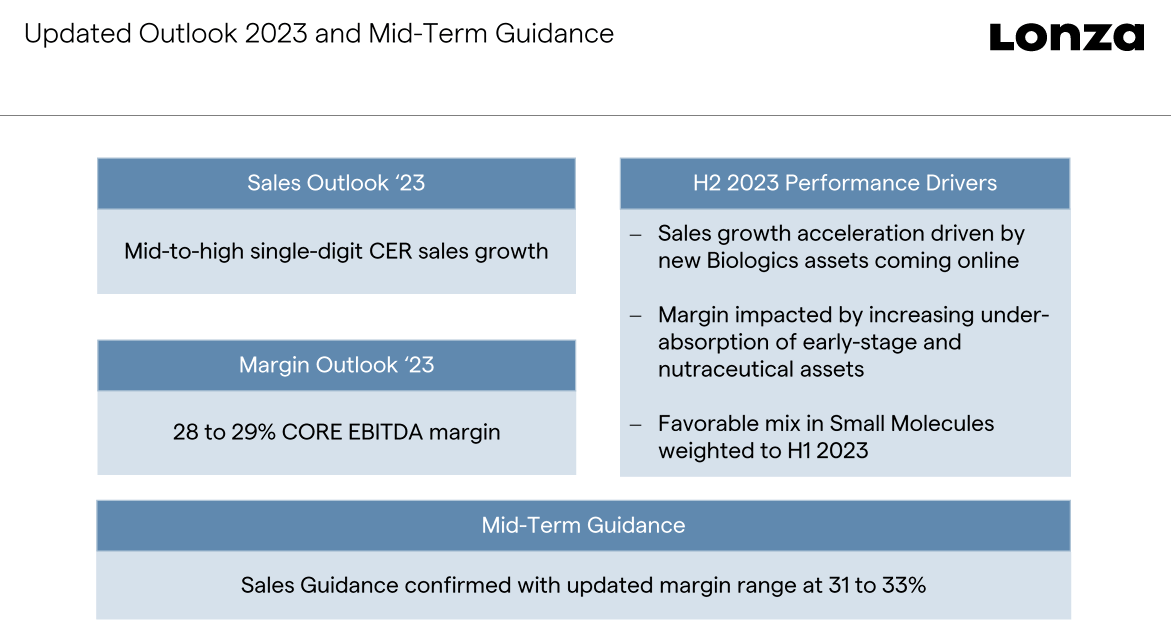

With this release, Lonza 2023 guidances were re-set (Fig 1). Turnover was amended from high-single-digit organic growth to mid-to-high-single-digit growth. And more importantly, the company's core EBITDA margin outlook was also lowered from 30-31% to 28-29%. Despite that, the company confirmed its mid-term 2024 outlook (which is very much in line with our previous indication). Therefore, we are not surprised to see a minus 11% stock price decline at the time of writing. In numbers, this guidance cut implies a further deterioration into the 2023 second part with a lower sales pick-up and margin pressure. According to our analysis, this is likely attributable to early-stage funding challenges in Cell and Gene division (Fig 2). There is also a lower demand for nutraceutical products. Despite that, biologics fundamentals and our long-term buy assumption remain intact. Repetitive losses in profitability targets (and under-delivery) cannot go unnoticed, and even if we believe their results were partially expected, this will turn into a negative Wall Street sentiment over the period. CMD released will be a key value driver for positive share price relief.

{kind=link}

Lonza lower 2023 guidance

Source: Lonza Q2 results presentation

{kind=link}

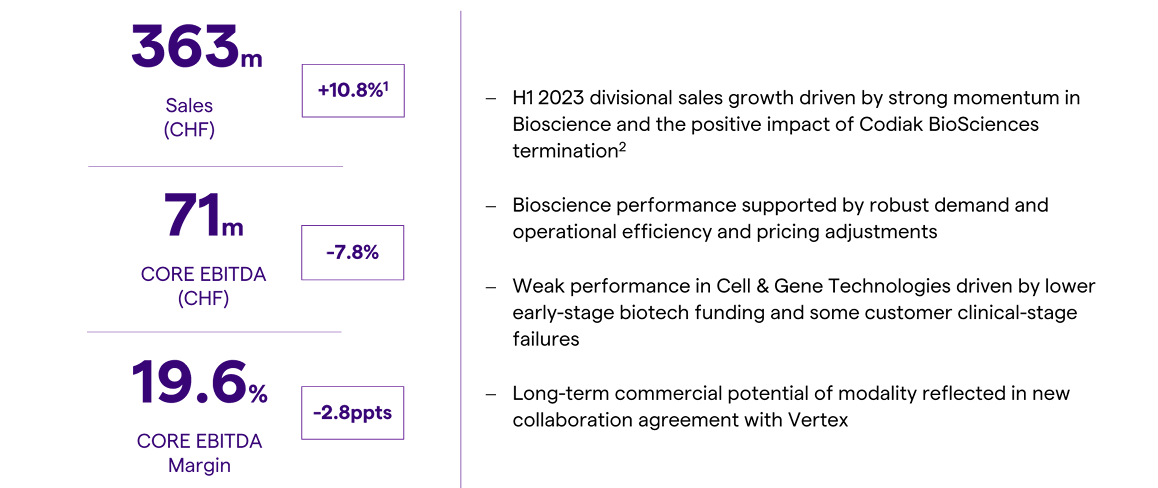

Cell and Gene margin evolution

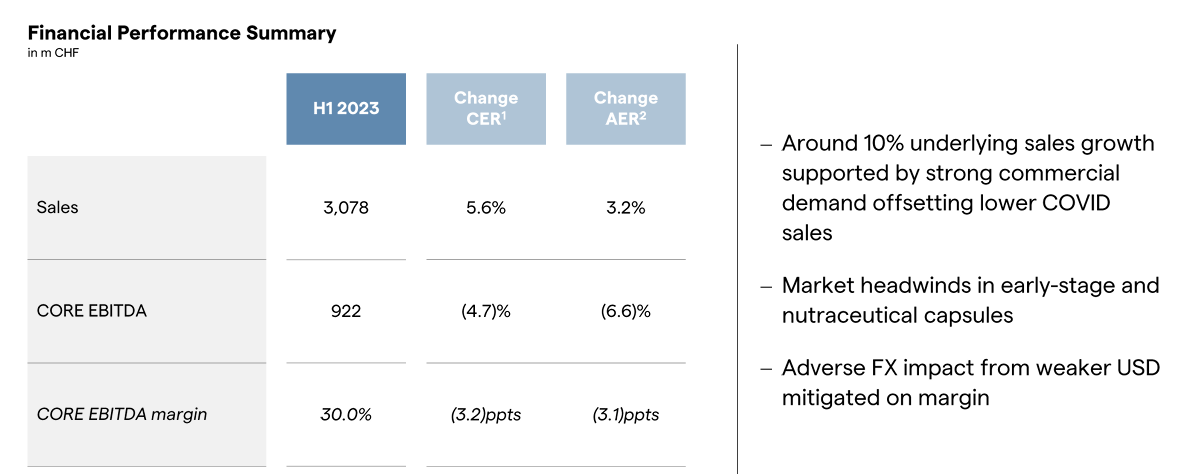

Cross-checking Wall Street estimates, H1 top-line sales were slightly below consensus. The company reported sales of CHF 3.07 billion while analysts CHF 3.12 billion. However, the company's EBITDA margin came ahead with a performance of 30% to CHF 922 million vs the expectation of CHF 915 million. Despite that, we should notice that Lonza lost 310 basis points in profitability compared to last year's period. This was due to the accretive vaccine business margin. Going down to the P&L analysis, net profit reached CHF 411 million and was down by 12% on a yearly basis. We should report higher losses from associates and a negative one-off due to a client asset impairment. Therefore, the core EPS reached CHF 6.12 compared to the expectation of CHF 6.55.

{kind=link}

Lonza H1 Financial in a Snap

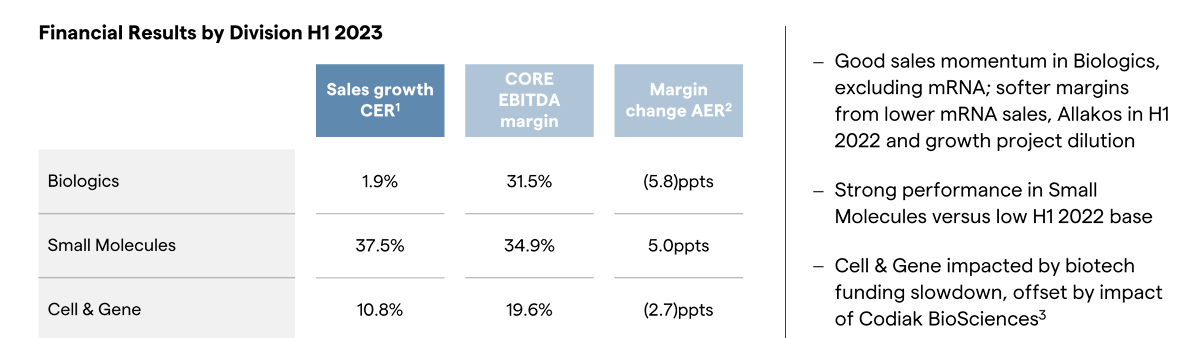

Looking at the divisional split, the Biologics division reported lower sales momentum with a plus 1.9%. This was due to the phase-out of the vaccine segment, which reported a margin decline of -580 basis points to 31.5%. There was a further impact on project delay. Small Molecules was the positive outlier, and the division grew by 38%, with the EBITDA margin up 500 basis points to 34.9%. This was mainly thanks to higher plant loading and a positive currency mix development. Cell & Gene was helped by the Codiak BioSciences termination fee, with the core EBITDA margin down by 280 basis points to 19.6%.

{kind=link}

Lonza divisional split

Conclusion and Valuation

Considering the Q2 results and a painful cut in guidance with a margin reset, we now forecast Fiscal Year 2023 sales at CHF 6.5 billion, with an EBIT margin of 20%. Reporting the CEO's words Lonza's " CDMO business is underpinned by partnership models and long-term contracts for commercial supply that provide a solid foundation for long-term stability and success. We continue to see strong underlying growth momentum, despite lower growth in demand for early-stage services and nutraceutical capsules ." For this reason, our 2024 outlook is still positive, even if we are below the company's guidance. Our 2024 EBIT margin is set at 22%. In our equity bridge calculation, Lonza's net debt reached CHF 564 million with a net cash of CHF 186 million in H1 2023. Operating FCF was negative for CHF 62 million with higher CAPEX deployment. Following these results, our Lonza target price aligns with its average peers with an EV/EBITDA of 22x. Therefore, we decided to lower our target price from CHF 650 to CHF 620. Additional risks in our overweight include product cannibalization, higher competition, lumpy order books, and ramp-up facility delays.

For further details see:

Lonza Group: Painful Cut In Guidance, Still A Buy