LXRX - Looking Back In On Lexicon Pharmaceuticals

2023-10-02 02:34:38 ET

Summary

- Lexicon Pharmaceuticals' primary drug candidate, INPEFA (sotagliflozin), has received FDA approval for the treatment of heart failure.

- INPEFA has a broad label and can be used for heart failure patients with or without diabetes, competing with established drugs like Jardiance and Farxiga.

- Lexicon Pharmaceuticals also has other compounds in development, including LX9211 for neuropathic pain and LX2761 for gastrointestinal tract issues.

- With the stock trading just above a buck a share, is this high-risk/high-reward equity worthy of a small investment?

- An investment analysis follows in the paragraphs below.

There are no facts, only interpretations .”? Friedrich Nietzsche

Today, we revisit Lexicon Pharmaceuticals ( LXRX ) for the first time in many moons. After a years-long saga finally managed to have its primary drug candidate sotagliflozin approved by the FDA to cut the risk of cardiovascular death, hospitalization for heart failure, and urgent heart failure visits.

Sotagliflozin, which now will go by the brand name INPEFA, received a broad label from the government agency. Eligible individuals for the drug will include heart failure patients across the full range of left ventricular ejection fraction or LVEF. These include preserved ejection fraction and reduced ejection fraction, and patients with or without diabetes. This should help INPEFA compete against established competitors like Eli Lilly's ( LLY ) Jardiance and AstraZeneca's ( AZN ) Farxiga.

INPEFA is an oral inhibitor, taken once daily. This compound is made up of two proteins responsible for glucose regulation. These are known as sodium-glucose cotransporter types 2 and 1 (SGLT2 and SGLT1). SGLT1 is responsible for glucose and sodium absorption in the gastrointestinal or the GI tract. SGLT2 is responsible for glucose and sodium reabsorption by the kidney.

In one study 'SOLOIST-WHF', INPEFA reduced the ' risk of the occurrence of cardiovascular death, hospitalization for heart failure, and urgent heart failure visits by 33% compared to the placebo '. This study was comprised of just over 1,200 patients. Cardiovascular deaths and heart failure events were also reduced by 50% over the 30- and 90-day discharge periods studied. It was one of two pivotal studies (the other being SCORED) that achieved positive results to treat unique and high-risk patient populations.

FDA approval came on May 26th and the drug hit the market a month later. So, what is ahead for INPEFA, Lexicon Pharmaceuticals, and its shareholders? An analysis follows below.

Company Overview:

Lexicon Pharmaceuticals is headquartered just outside of Houston in The Woodlands, TX. This small biopharma concern is focused on developing and commercializing orally delivered small molecule drug candidates. The stock currently trades around $1.10 a share and sports an approximate market capitalization of $270 million.

In addition to INPEFA, the company has a couple of other compounds in development.

LX9211

This candidate is in Phase II clinical development for the treatment of neuropathic pain. The company is currently planning ' to run a Phase 2b dose escalation study in parallel with a Phase 3 trial '. LX9211 is listed 'a s a potent, orally delivered, selective small molecule inhibitor of adaptor-associated kinase 1 (AAK1)' . The compound has received Fast Track designation for the treatment of neuropathic pain. If developed proceeds according to plans, an NDA for LX9211 would be filed in 2027.

LX2761

This compound is in Phase I clinical development for gastrointestinal tract.

INPEFA - The Competitive Marketplace:

Farxiga is an SGLT2 inhibitor for use in the treatment of type 2 diabetes mellitus, heart failure, and chronic kidney disease. It was first approved early in 2014. The compound did a little over $4 billion in revenues in 2022.

Jardiance did over $6 billion in sales in 2022. Jardiance was originally also approved by the FDA in 2014 to improve glucose control in adults with type 2 diabetes. Since then this SGLT2 inhibitor has garnered additional approved indications that include reducing the risk of cardiovascular death in adults with type 2 diabetes and established cardiovascular disease. It is also used to reduce the risk of death and hospitalization in patients with heart failure and low ejection fraction.

A recent article on Seeking Alpha did a good job comparing these compounds vis a vis with INPEFA within various indications, so I will not rehash the findings other to say INPEFA does look quite promising although obviously it will lack first mover advantage (by many years in fact) and the company has will have a much smaller sales forces that drug giants Eli Lilly and AstraZeneca.

A few months prior to approval, the analyst firm consensus was that INPEFA could see peak sales of just under $700 million by FY2031 a few months before INPEFA was approved. Notably, Jefferies only projected a bit over $325 million in peak sales for INPEFA. While this level of peak sales would be little more than a rounding error to one of the drug giants, it would still be quite significant to Lexicon given the stock has an approximate $270 million market capitalization.

Analyst Commentary & Balance Sheet:

Just over 18% of the outstanding float in the shares are currently held short. Several insiders including the company's CEO and CFO have made numerous small purchases in the stock since June totaling approximately $250,000 collectively.

After posting a net loss of $44.9 million for the second quarter, the company ended the first half of 2023 with just over $255 million worth of cash and marketable securities on its balance sheet. The company raised just over $70 million in additional capital via a secondary offering soon after the FDA approval of INPEFA. Lexicon has just under $100 million of long-term debt as well. It is important to note that operating expenses increased to $30 million in the second quarter from just $10.7 million as the company added sales personnel and prepared for the rollout of INPEFA.

Since second quarter numbers were posted on August 3rd, both Piper Sandler ($10 price target) and Citigroup ($5 price target) have reissued Buy ratings on the stock.

Verdict:

The current analyst consensus has the company losing 81 cents a share in FY2023 on $8 million in revenues as ramp up of INPEFA has commenced. There is a wide variance of projections in FY2024 from the four analyst firms who have posted estimates. They range from a loss of 65 to 92 cents a share on between $22 million to $90 million in sales.

Management's focus now is ' to establish INPEFA as the standard of care for hospitalized heart failure patients transitioning to outpatient care '. The $64,000 question for investors is how INPEFA will be received in the market and what its sales ramp will look like.

Unfortunately, we won't get real data points on that starting sales trajectory until INPEFA has been on the market for a few quarters at least. This is especially important to see what the cash burn will be given higher operating expenses from adding a sales team against new revenues from INPEFA. While Lexicon recently executed a capital raise in June, another one is very likely in 2024.

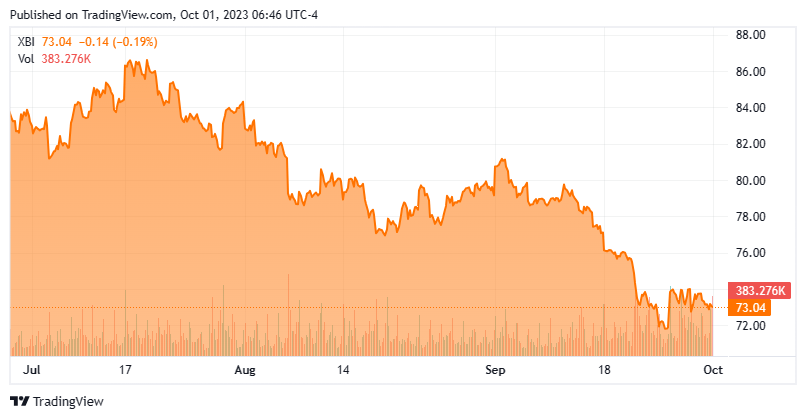

Trepidation around how fast INPEFA gains sales traction is one key factor in the stock's recent poor performance. The other is the very poor performance from small biotech stocks in the third quarter. In the quarter just concluded the SPDR® S&P Biotech ETF ( XBI ) dropped nearly 15%.

{kind=link}

The company is working hard to get coverage approved for this new drug via myriad insurance programs. Lexicon has already put in ' 16 bid submissions covering 198 million lives across both commercial and Medicare books of business .'

Given an enterprise value of approximately $140 million taking into account the company's net cash, the potential value of INPEFA with LX9211 as a potential longer-term wild card seems worthy only of a small ' watch item ' holding for risk-tolerant investors at the moment. My small stake in LXRX continues to be via covered call orders which provide downside mitigation and there is good liquidity in the options against LXRX.

We can complain because rose bushes have thorns, or rejoice because thorns have roses .”? Alphonse Karr

For further details see:

Looking Back In On Lexicon Pharmaceuticals