APLE - Losers Of REIT Earnings Season

2023-08-15 11:30:00 ET

Summary

- After covering the Winners of REIT Earnings Season last week, Part 2 of our Earnings Recap focuses on the worst-performing property sectors and common threads shared by these laggards.

- While there were upside standouts and some solid reports within these lagging property sectors, the losers of REIT earnings season included: Self-Storage, Hotel, Healthcare, and Specialty REITs.

- Many of the "misses" emanated from the direct and secondary effects of the higher interest rate environment, underscoring the continued challenges facing more-highly-levered private real estate portfolios.

- More concerning was the handful of downward revisions driven by sudden demand softness cited by the most pro-cyclical property sectors: hotel and billboard REITs, indicating that more corporations are in cost-cutting mode. Consumer softness was also seen via an uptick in unpaid mid-tier apartment rents and sluggish storage demand.

- The Sunbelt vs. Coastal bifurcation hasn't completely dissipated, but market-level performance is becoming more localized. West Coast weakness was a common thread across most property sectors, but the New York metro was a notable upside standout. Sunbelt demand remains strong, but pockets of oversupply have become headwinds.

Real Estate Earnings Recap: Part 2

{kind=link}

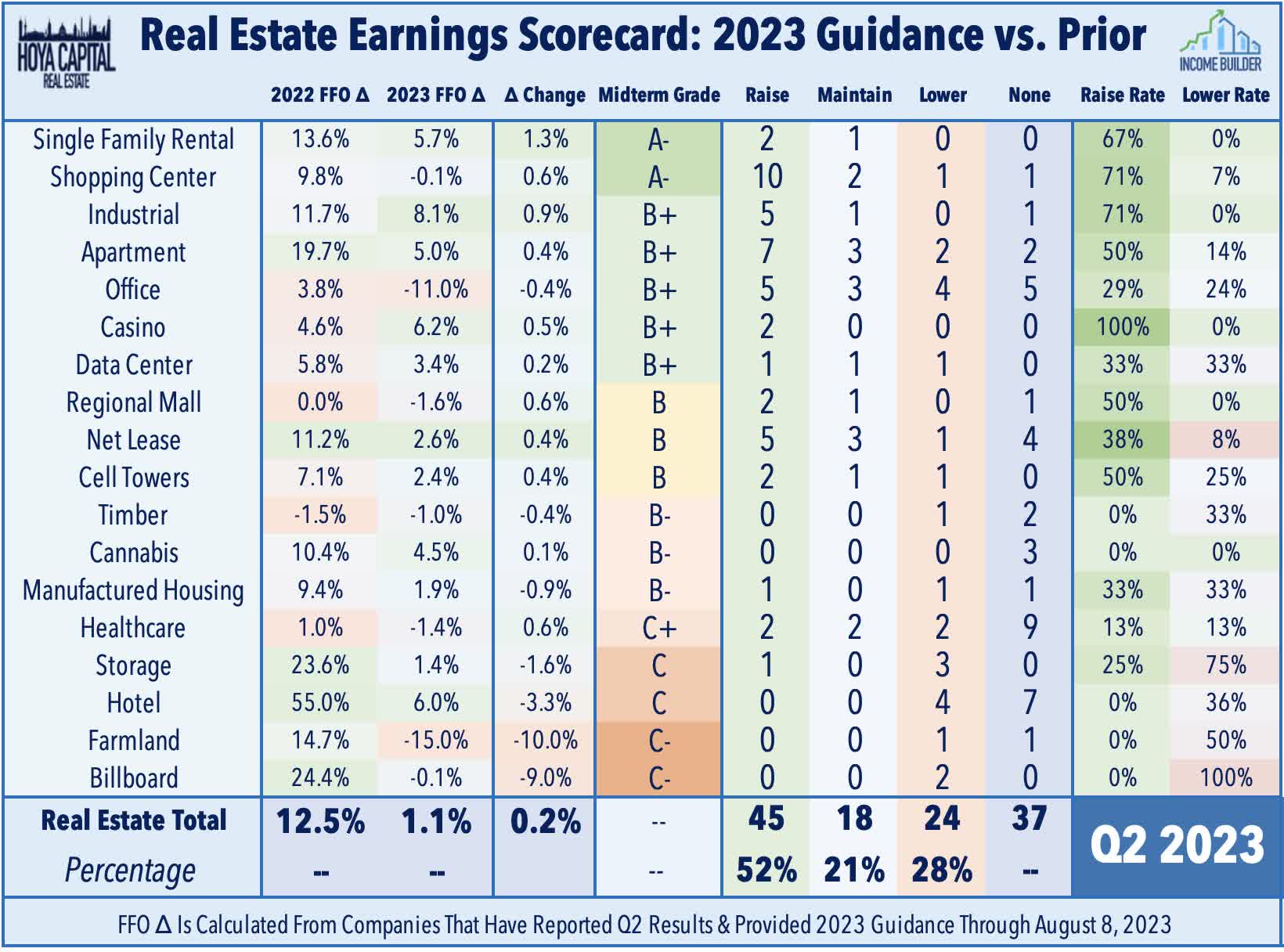

In Part 1 of our Earnings Recap - Winners of REIT Earnings Season - we discussed the nine best-performing property sectors, a list that included Residential REITs, Retail REITs, Industrial REITs, and Data Center REITs. While we were impressed by the strength exhibited by several of these previously beaten-down sectors, we also saw some unexpected weakness from several previously outperforming sectors including Self-Storage, Hotel, Healthcare, and Specialty REITs. As noted last week, of the 86 equity REITs that provide full-year Funds from Operations ("FFO") guidance, 24 REITs (28%) lowered or withdrew their full-year guidance, which was the highest in the REIT sector since the start of the pandemic, but still below the S&P 500 average of 40%. Many of the "misses" emanated from the direct and secondary effects of the higher interest rate environment, underscoring the continued challenges facing more-highly-levered private real estate portfolios.

{kind=link}

Roughly half of the downward FFO revisions were driven simply by higher interest rate expense expectations, with the clearest example being Piedmont Office ( PDM ), which lowered its FFO outlook after refinancing $400M in debt at a sharply higher interest rate - 9.25% compared to its maturing 4.45% note. Other property sectors were hit by the secondary effects of higher rates through increased stress on their tenant base. For Cell Tower REITs - most notably Crown Castle ( CCI ) - higher rates have prompted a downshift in network infrastructure investments which have historically been financed via debt. For healthcare, farmland, and cannabis REITs, many of their smaller and more highly-levered tenant operators have increasingly struggled to pay rent as access to cheap capital has dried up, with Medical Properties Trust ( MPW ) being the prime example of tenant issues bleeding into REIT-level issues. Many skilled nursing, cannabis, and lab space tenant operators are also struggling from a combination of interest-rate-related and industry-specific headwinds.

{kind=link}

Other "misses" were more company-specific issues, with manufactured housing REIT Sun Communities ( SUI ) being a prime example with its ill-timed expansion into the UK vacation home market ahead of the deepest European housing slump since the GFC - a rare blunder for one of the top-performing REITs of all time - which came alongside an otherwise strong quarter for its core manufactured housing portfolio. While the cooldown in inflation helped on the expense-side for many REITs this earnings season, several large-cap REITs that were heralded last year for their CPI-linked rent escalators - notably net lease REIT W. P. Carey ( WPC ) and casino REIT VICI Properties ( VICI ) - have been on the wrong side of that trade this earnings season as the tailwinds of historically elevated CPI readings are looking increasingly likely to become headwinds by 2024. Commodities disinflation was a major theme for the agriculture-focused REIT sectors - farmland and timber REITs. From their peaks, lumber prices are down 75%, and grain prices are down nearly 40%.

{kind=link}

A bit more concerning was the handful of downward revisions driven by sudden and generally unexpected demand softness cited by the most pro-cyclical property sectors: hotel and billboard REITs - suggesting that more corporations are in cost-cutting mode and seeking to cull non-essential expenses and, perhaps, that workers are seeing less flexibility in "Work From Anywhere" perks as more companies call employees back to the office. Several consumer-facing REITs also observed emerging pockets of demand weakness - particularly from middle and lower-income tenants - most notably from self-storage REITs and 'Class B' apartment REITs, which observed an unexpected uptick in unpaid rents. Meanwhile, the Sunbelt vs. Coastal bifurcation hasn't completely dissipated, but market-level performance is becoming more localized. West Coast weakness was a common thread across most property sectors - weakness that was especially visible in the " ghost town " of San Francisco - but the New York metro was a notable upside standout for nearly all property sectors. Sunbelt activity generally remained stronger than the Coasts, but pockets of oversupply have become headwinds in markets and sectors where development activity faces fewer barriers.

{kind=link}

With real estate earnings season now essentially complete - sans a handful of stragglers that report results over the coming weeks - we compiled the critical metrics across each real estate property sector. In Part 2 of our two-part REIT Earnings Recap, we focus on the "Losers of REIT Earnings Season."

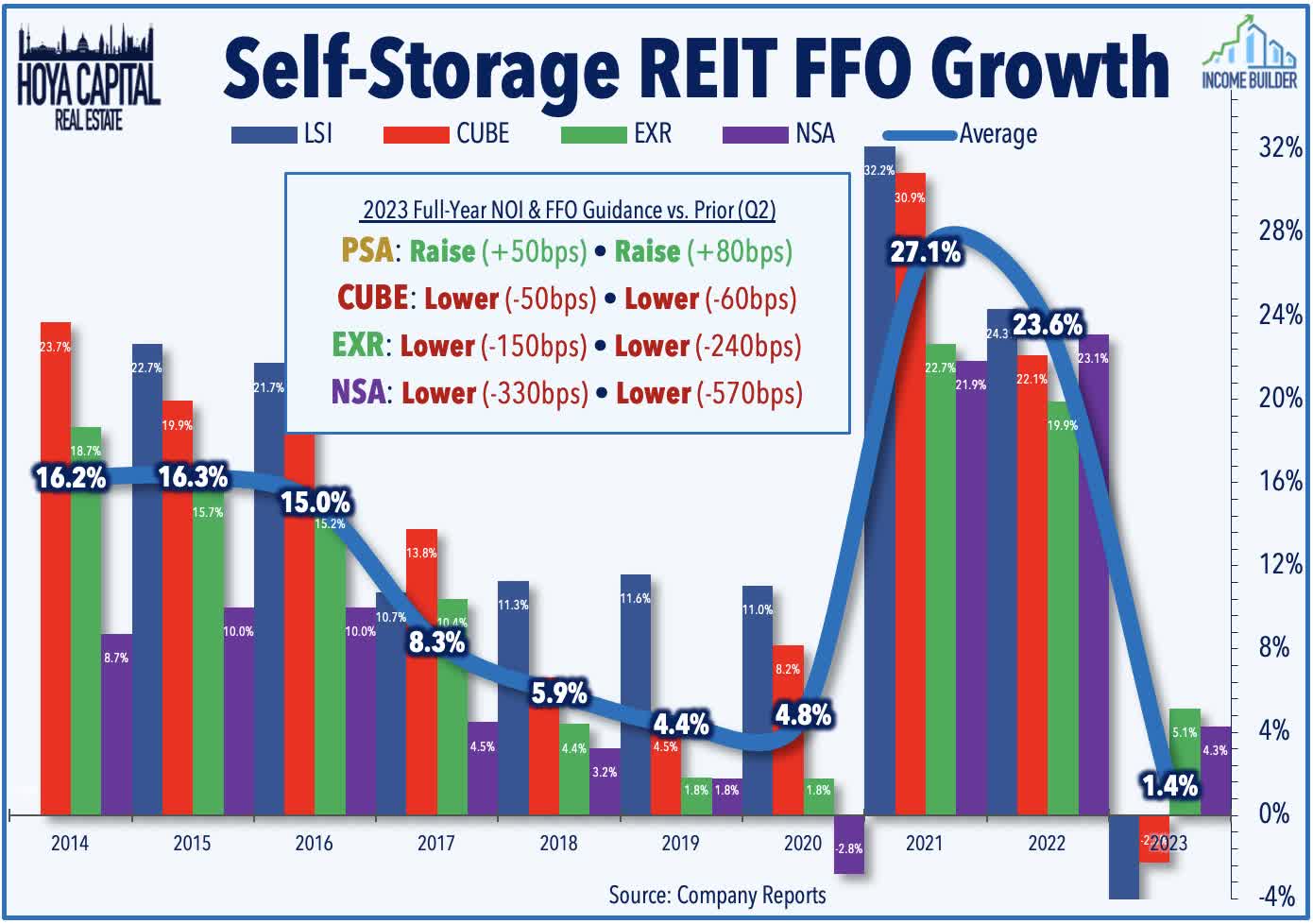

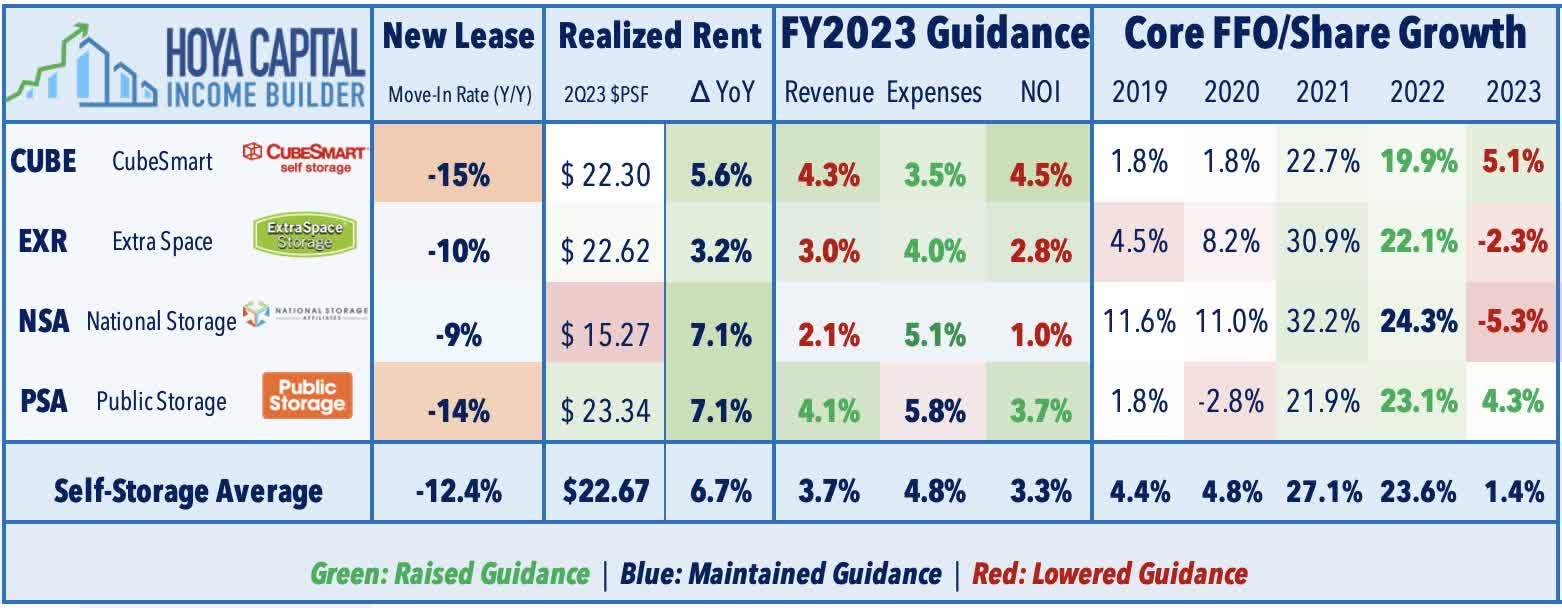

Loser #1: Storage REITs

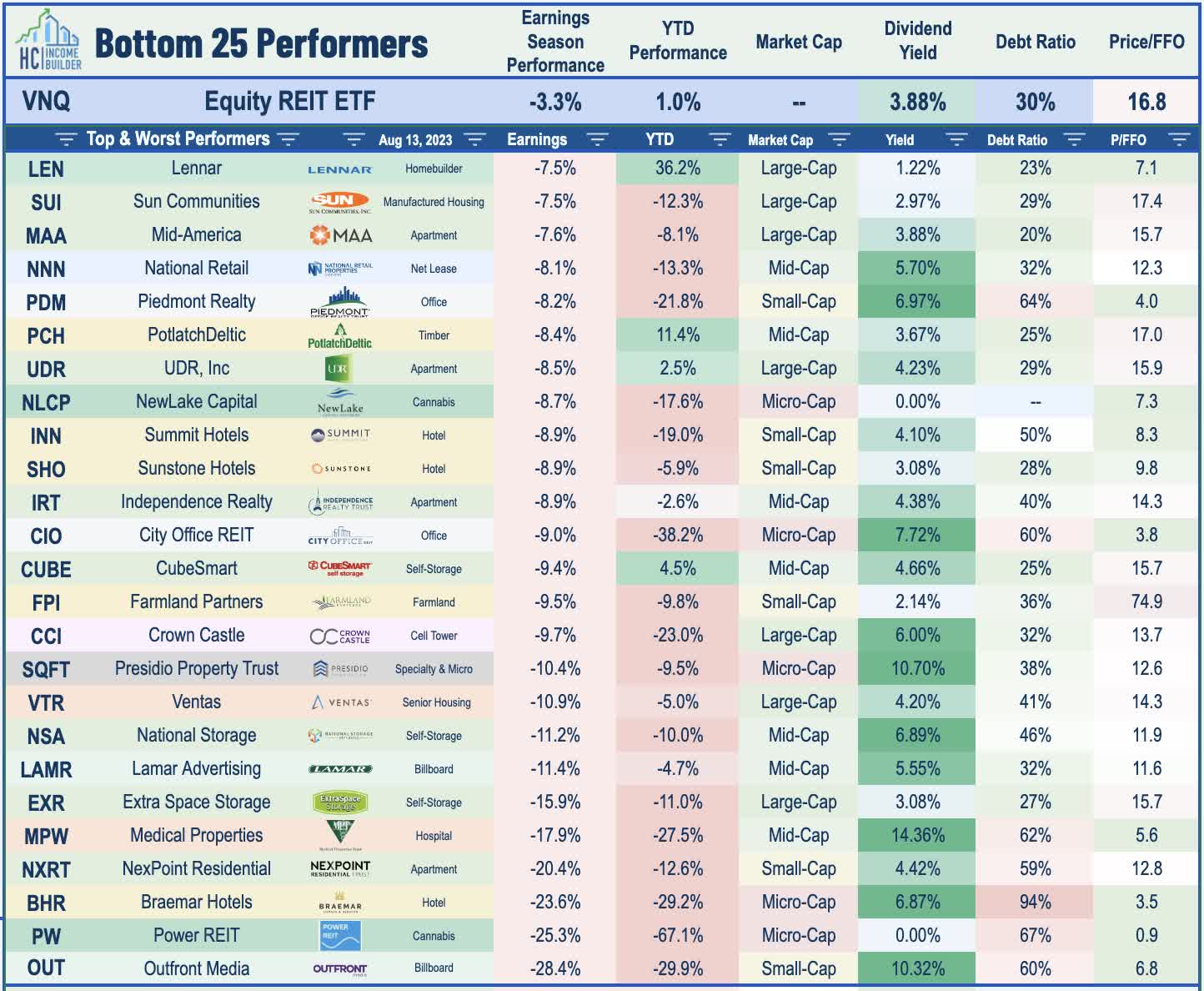

Storage : (Final Grade: C) The sector with the strongest aggregate NOI growth since the start of the pandemic, self-storage REITs have stumbled this earnings season following a weak slate of reports in which three of the four REITs lowered their full-year FFO and NOI outlooks. All four self-storage REITs reported double-digit declines in "street rates" on new customers in Q2, but this pricing weakness was more-than-offset by high-single-digit rent growth on renewal leases, resulting in a total rent PSF increase of about 6.5% during the quarter compared with last year. The strongest report came via Public Storage ( PSA ), which raised its full-year outlook, citing strength in its California markets - one of the lone exceptions to the West Coast underperformance theme. National Storage ( NSA ) - which focuses on cheaper storage units in secondary and tertiary markets compared to its larger peers - reported the softest results of the four storage REITs, noting that it "experienced a softer spring leasing season, and the interest rate environment was tougher than expected." NSA now expects its FFO to decline by 5.3% this year - a sizable downward revision from its prior outlook for 0.4% growth - and expects to report same-store NOI growth of 1.0% - down from its midpoint of 4.25%.

{kind=link}

{kind=link}

Loser #2: Hotel REITs

Hotel : (Final Grade: C) Softer-than-expected results from hotel REITs - along with results from several major airlines - showed signs of emerging softness in the post-COVID travel recovery. Four of the five hotel REITs that provide full-year FFO guidance lowered their outlook, while four of six that provide Revenue Per Available Room ("RevPAR") guidance lowered their outlook. Most REITs cited a slight moderation in leisure demand from record levels, and a modestly disappointing recovery in business and international travel, while the tailwinds from inflationary increases in average daily room rates have dissipated. Host Hotels ( HST ) and Summit Hotel ( INN ) each dipped nearly 10% since lowering their outlook for both FFO and Revenue Per Available Room ("RevPAR"), while Park Hotels ( PK ) lowered its guidance on both metrics as well. Apple Hospitality ( APLE ) - which focuses on the limited-service segment - was the lone hotel REIT to raise its full-year RevPAR guidance. Overall, the six guidance-providing hotel REITs now expect RevPAR to increase by 8.2% this year, down from the 8.6% outlook last quarter. Recent TSA Checkpoint data shows that throughput was at 99% of pre-pandemic levels in July, a slight downshift from the 101% average in the first-half of 2022.

{kind=link}

{kind=link}

Loser #3: Billboard REITs

Billboard : (Final Grade: C-) Citing a late-quarter slowdown in business advertising spending and continued weakness in their public transit segments, both billboard REITs dipped by double-digits after reporting weak results and significantly reducing their full-year earnings outlook. Outfront ( OUT ) has dipped over 25% since reporting that it booked a substantial $500M non-cash impairment on its New York MTA transit segment, an ill-timed 15-year deal signed two years before the pandemic that has proven to be a substantial drag on its otherwise solid billboard business. OUT now expects its full-year FFO to decline "by high single-digits, possibly low double-digits versus 2022" versus its prior guidance of 5% growth, and commented, "after two strong years of growth, the recovery in transit revenues seemingly stalled in the first half of 2023." Lamar ( LAMR ) - which has about 10% of its portfolio in transit advertising vs. nearly 25% for Outfront - has dipped over 10% after it also lowered its full-year FFO growth outlook to -2.4% versus +1.3% previously, noting that recent weakness in national brand spending - especially on the West Coast - has offset resilience in local advertising spending. LAMR commented, "We're not seeing any wheels coming off. It's general softening that's spread a little bit."

{kind=link}

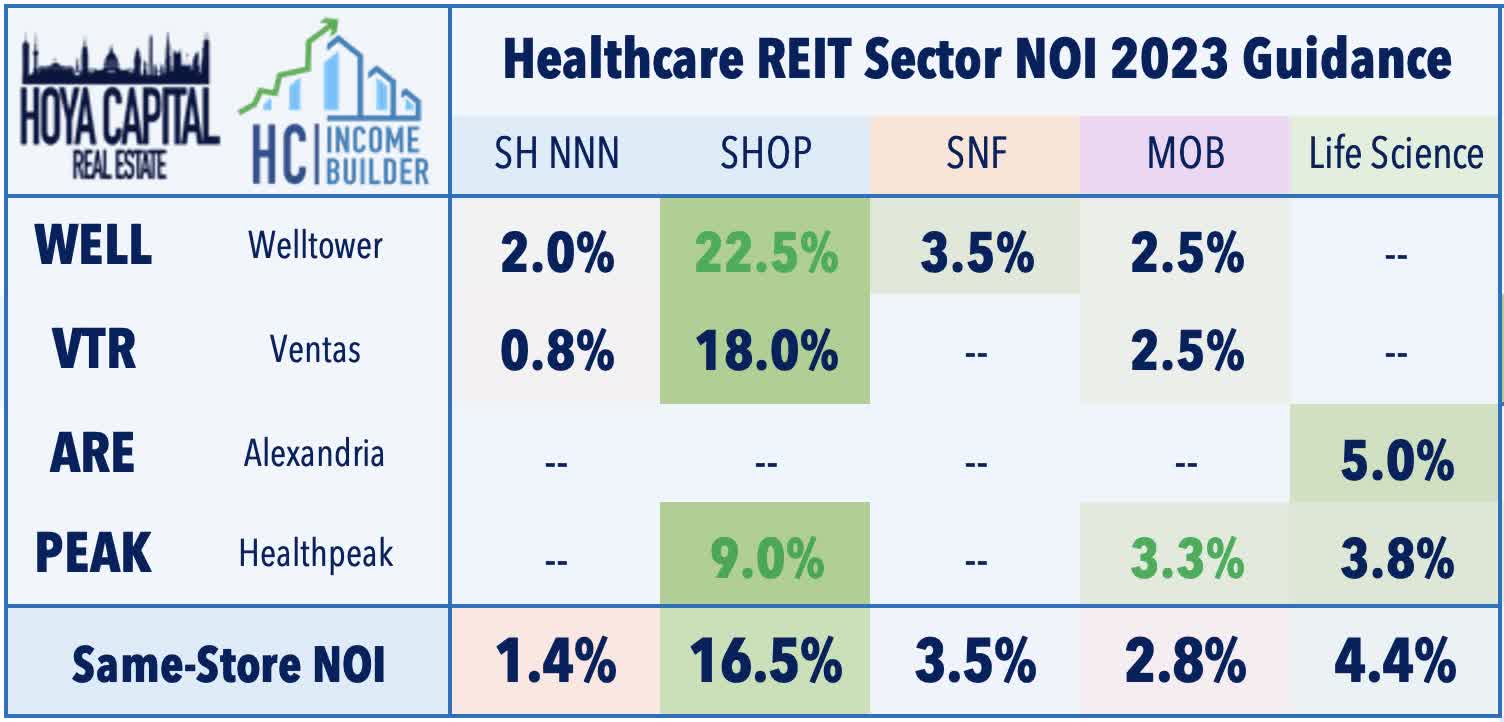

Loser #4: Healthcare REITs

Healthcare : (Final Grade: C+) Hospital owner Medical Properties Trust has dipped more than 15% this earnings season after trimming its full-year outlook and reporting ongoing operating struggles with two of its largest tenants - Steward Health Care and Prospect Medical - which have faced industry-wide headwinds resulting from elevated labor expenses and the waning of COVID-era relief programs. MPW noted that it would contribute up to $140M as part of a $600M credit facility to Steward - its largest tenant at roughly 20% of annual revenues - as part of a private credit lending syndicate. MPW also noted that Prospect - its fourth largest tenant at 6% of revenues - paid equity in lieu of cash for its 2023 rent, an equity interest that was appraised at $655M. Medical office REITs also delivered a weaker-than-expected earnings season. For the five MOB-focused REITs, FFO is lower by an average of 7.3% through the first half of 2023 amid pressure from higher interest rate expenses and a downshift in leasing activity.

{kind=link}

Results were stronger for senior housing and skilled nursing REITs, however, as abating expense pressures have resulted in improved tenant operator performance following several quarters of crisis-level staffing issues. Senior housing REIT Welltower ( WELL ) boosted its full-year guidance driven by another upward revision to its NOI expectations for its Senior Housing Operating Portfolio ("SHOP"). Benefiting from COLA increases, pricing power remains robust as well, with WELL recording record-high rent growth of 6.7% in its occupied facilities, which combined with moderating expense pressures, has driven a meaningful improvement in operating margins. Positively for senior housing REITs, supply growth has finally cooled following a decade of elevated inventory growth, as NIC reported that units under construction amounted to 4.9% of total inventory, which is the lowest seen since 2014. Healthpeak ( PEAK ) also boosted its SHOP guidance to 9.0% - helping to drive a lift to its full-year FFO outlook as well - while Ventas ( VTR ) maintained its FFO and NOI guidance.

{kind=link}

Loser #5: Cannabis REITs

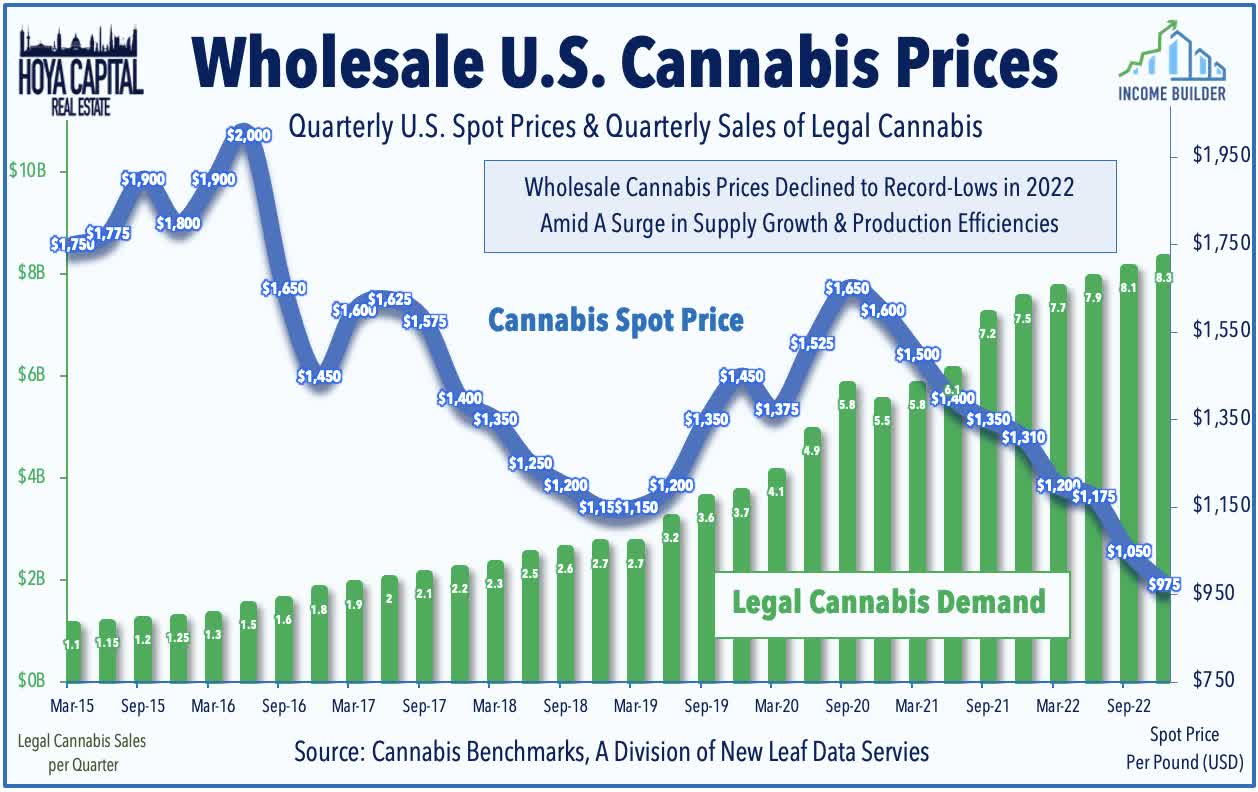

Cannabis : (Final Grade: B) Cannabis REITs have remained under pressure this earnings season amid concern over defaults from their cannabis cultivator tenants, which have been pressured by a trio of headwinds: limited access to capital, lower wholesale cannabis prices, and setbacks on federal legalization. Tenant operator issues generally remained "status quo" this quarter: Innovative Industrial ( IIPR ) reported that it collected 97% of rent in Q2 and in July - down slightly from 98% in Q1 - with Parallel responsible for all of the unpaid rents in excess of security deposits. NewLake Capital ( NLCP ) reported that it collected 92% of second-quarter rents - consistent with the prior quarter - as its third-largest tenant, Revolutionary Clinics, has not paid any rent in 2023. Chicago Atlantic ( REFI ) reported that it experienced its first default since the company's inception this past quarter, noting that borrower has not paid interest since May on its $16.1M balance - representing about 5% of its loan book - but noted that it is "confident that we will be made whole on this loan." AFC Gamma ( AFCG ) reported that it foreclosed on its $10M loan to Evermore (roughly 2% of its loan book) but subsequently sold two-thirds of the facility to a multistate operator at par and expects to have "full recovery on the remaining one-third of our debt outstanding."

{kind=link}

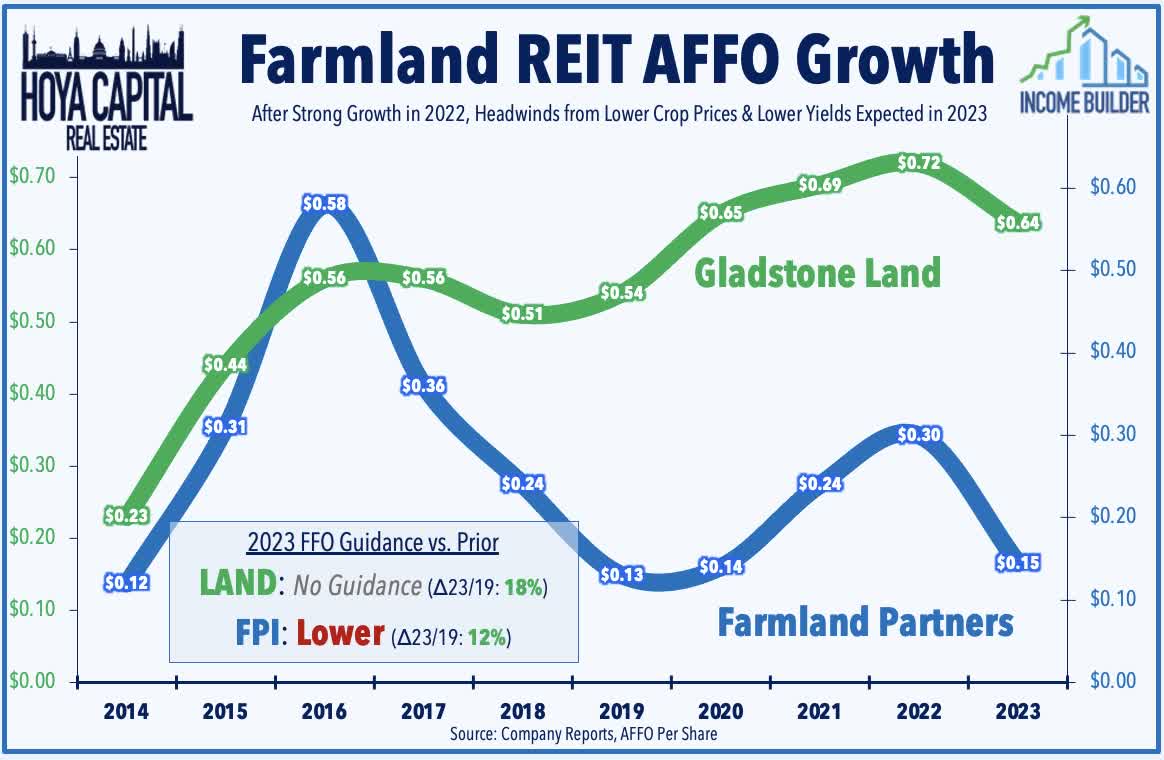

Loser #6: Farmland REITs

Farmland : (Final Grade: C-) One of the hottest inflation-hedges last year, farmland REITs have been slammed over the past nine months amid a "triple whammy" of headwinds - lower crop yield due to extreme weather, lower crop prices, and significantly higher interest rate expense. Small-cap farmland REIT Farmland Partners ( FPI ) has been a laggard this earnings season after significantly lowering its full-year FFO outlook prompted by rising interest expense. FPI now expects its full-year FFO to dip over 50% this year compared to 2022, but to levels that are still about 12% above its full-year 2019 FFO before the pandemic. G ladstone Land ( LAND ) reported stronger results, but tenant issues persist, with the company noting that it had to remove one of its 90 tenants due to nonpayment, while a second tenant has been late on rent and "sounds like they're might decide to close up shop." Drought conditions in the West have largely subsided, however, removing one prior headwind.

{kind=link}

Loser #7: Manufactured Housing REITs

Manufactured Housing : (Final Grade: B-) After snapping a decade-long streak of outperformance over the REIT Index last year, MH REITs are pacing for a second-straight year of underperformance, but property-level fundamentals in the core manufactured housing segment are certainly not to blame. Sun Communities ( SUI ) - the best-performing REITs in the 2010s - appears to have made an operational misstep with its push into the European market, a segment that has posted disappointing performance since its acquisition in mid-2022. SUI lowered its full-year FFO outlook as upward guidance boosts to its core manufactured housing and marina outlook were more than offset by a significant downward revision to its UK Home Sales NOI forecast. Equity LifeStyle ( ELS ), however, raised its full-year FFO and NOI guidance, "driven by continued strength in annual revenue and reduced expenses throughout our portfolio." ELS was given an added boost by its inclusion in the S&P 400 Index , replacing Life Storage. While COLA increases have helped to drive record-high rent growth across the MH portfolio, the RV segment has been a recent issue for both SUI and ELS after several years of stellar performance.

{kind=link}

Loser #8: Cell Tower REITs

Cell Tower : (Final Grade: B) Earnings season began on a sour note with Crown Castle lowering its full-year adjusted FFO outlook citing a "significant" slowdown in carrier network spending. We were surprised by CCI's sudden downbeat industry commentary, with CCI commenting that "the initial surge in tower activity [related to the 5G rollout] has ended." Subsequent results from American Tower ( AMT ) and SBA Communications ( SBAC ) - both of which raised their full-year revenue and FFO guidance - allayed some industry-level concerns and provided evidence to our suspicion that CCI's downbeat tone may have been related to its later-announced restructuring plan to reduce costs - which includes a reduction in employee headcount by about 15%. Combined, cell tower REITs upwardly revised their full-year FFO outlook by an average of roughly 0.5%. Last week, we published Cell Tower REITs: Toxic Telecom, which noted that industry headwinds are rooted primarily in the ongoing disintermediation of legacy wireline business segments towards fully wireless deployments and the mounting competition on the two industry juggernauts. This disintermediation has trended on a path from wired to wireless infrastructure, disruptions which actually serve to further solidify the longer-term favorable competitive positioning of cell tower REITs.

{kind=link}

Recap: Decent Quarter, With Exceptions

After covering the Winners of REIT Earnings Season last week, Part 2 of our Earnings Recap focused on the worst-performing property sectors and common threads shared by these laggards. Many of the "misses" emanated from the direct and secondary effects of the higher interest rate environment, underscoring the continued challenges facing more-highly-levered private real estate portfolios. As we've covered extensively in our State of the REIT Nation reports, most REITs have been preparing for this exact kind of dislocated macro environment, perhaps to the frustration of some investors that turned to higher-leveraged and riskier alternatives in recent years across private markets - including the non-traded REIT platforms discussed above. Considering the pain being felt by some of the more highly-levered public REITs, it's not hard to imagine the looming crisis facing many private market players that lack access to cheap, long-term fixed-rate unsecured debt. External growth for public REITs remains challenged for now, but REITs that played it safe during the "boom times" will likely have opportunities as reality sets in for many over-levered private-market property owners who weren't prepared to handle either higher rates or lower property values.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Losers Of REIT Earnings Season