AGNC - Losers Of REIT Earnings Season

2023-11-16 10:00:00 ET

Summary

- After covering the Winners of REIT Earnings Season last week, Part 2 of our Earnings Recap focuses on the worst-performing property sectors and common threads shared by these laggards.

- Unlike the second quarter, which saw a handful of poor reports and unexpectedly steep guidance and dividend cuts, there were no major 'bombshells' this earnings season.

- While there were upside standouts and some solid reports within these lagging property sectors, the losers of REIT earnings season included: Residential, Office, Mortgage, and Self-Storage REITs.

- Expense growth remained stubbornly persistent for residential REITs - which were responsible for the majority of the downward guidance revisions this quarter - with insurance and property taxes surging by double-digits across most markets and segments - while supply growth is an issue for multifamily, industrial, and self-storage.

- Surging interest expense was again the culprit behind the balance of the downward revisions. For lenders, defaults have accelerated, but recovery rates remain high. Conditions remained 'status-quo' in the embattled office sector: weak but not disastrous.

Real Estate Earnings Recap

{kind=link}

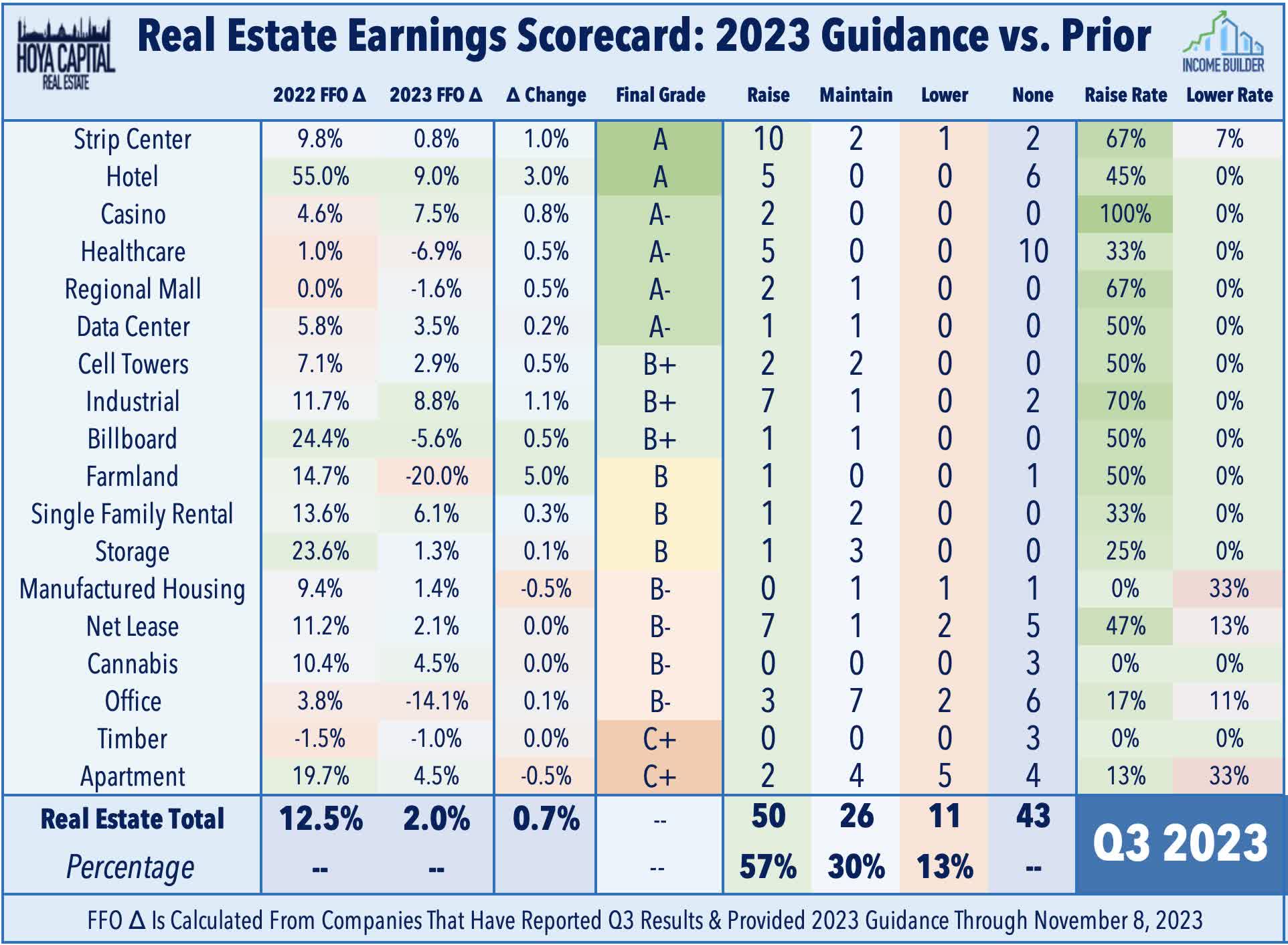

In Part 1 of our Earnings Recap - Winners of REIT Earnings Season - we discussed the nine best-performing property sectors, a list that included Retail, Hotel, and Healthcare REITs. Unlike the second quarter, which saw a handful of truly poor reports and unexpectedly steep guidance and dividend cuts, there were few major 'bombshells' this earnings season. As noted last week, of the 87 equity REITs that provided updated full-year Funds From Operations ("FFO") guidance, 50 REITs increased their forecast, 26 maintained, and 11 lowered their outlook. Among the 61 REITs that adjusted their forecast, 82% were upward revisions, while 18% were downward revisions. By comparison, FactSet reports that 54% of S&P 500 components have raised the full-year EPS outlook, while 46% have reduced their guidance. While there were certainly some upside standouts and some solid reports within the lagging property sectors, the losers of REIT earnings season included Residential, Office, Mortgage, and Self-Storage REITs.

{kind=link}

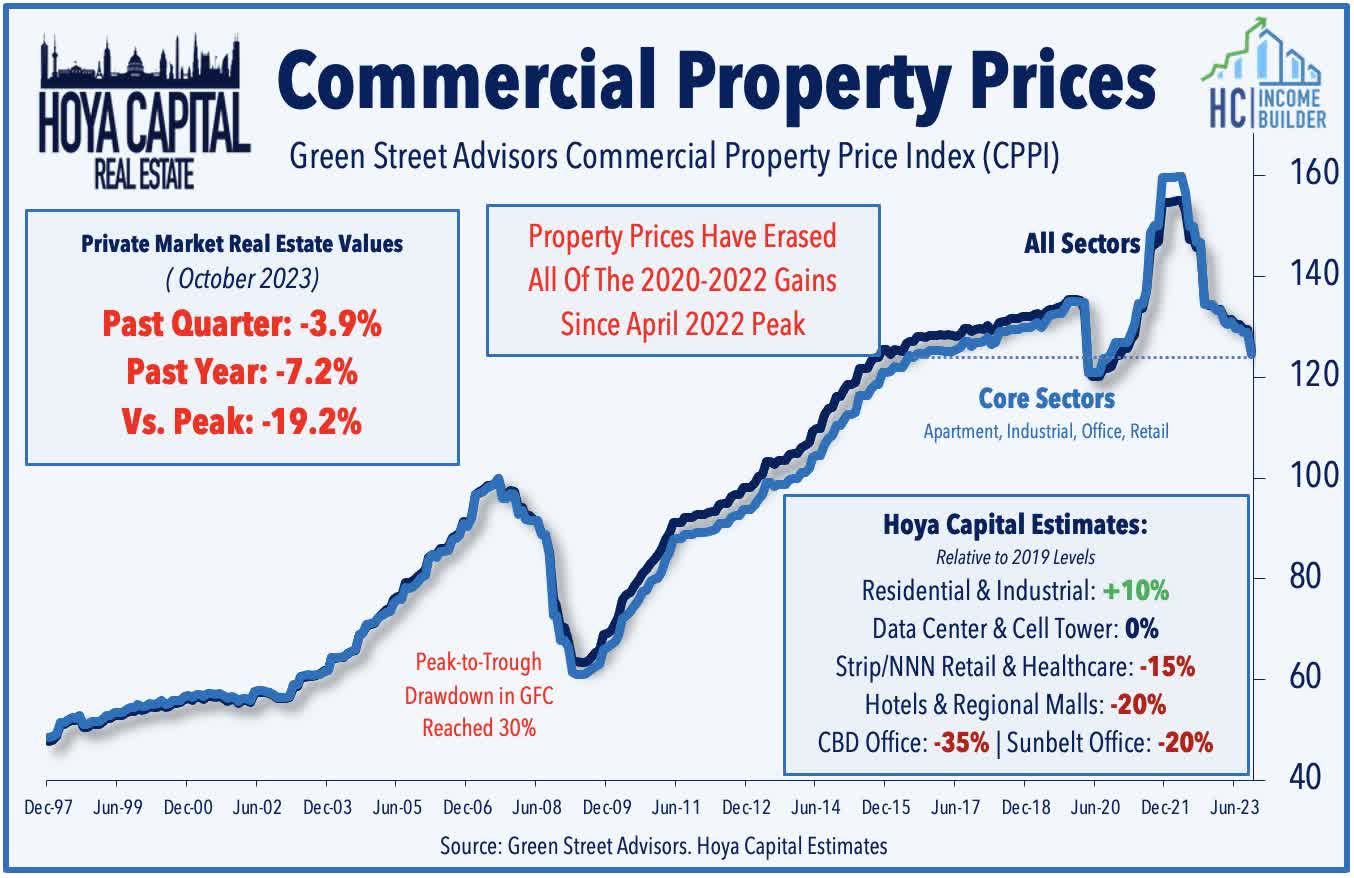

Surging interest expense was again the culprit behind some of the pockets of pain, underscoring the continued challenges facing more highly leveraged private real estate portfolios. Private real estate markets have been slow to "catch up" to the reality of higher interest rates - conditions have been reflected in public real estate markets since early 2022 - but we've begun to see a more evident re-pricing as the refinancing clock ticks ever-louder for private equity sponsors with their backs against the wall. Green Street Advisors' data shows that private-market values of commercial real estate properties have dipped by nearly 20% from the April 2022 peaks - giving back not only all of their pandemic-era gains but also essentially all of the gains from the past decade. Excluding the brief pandemic dip, Green Street's CPPI Index declined in October to the lowest levels since March 2016 - nearly eight years ago. We've noted that the 25% drawdown level is a critical "capitulation threshold" - a level that matches the maximum Loan-to-Value ("LTV") ratio accepted by conventional commercial real estate lenders.

{kind=link}

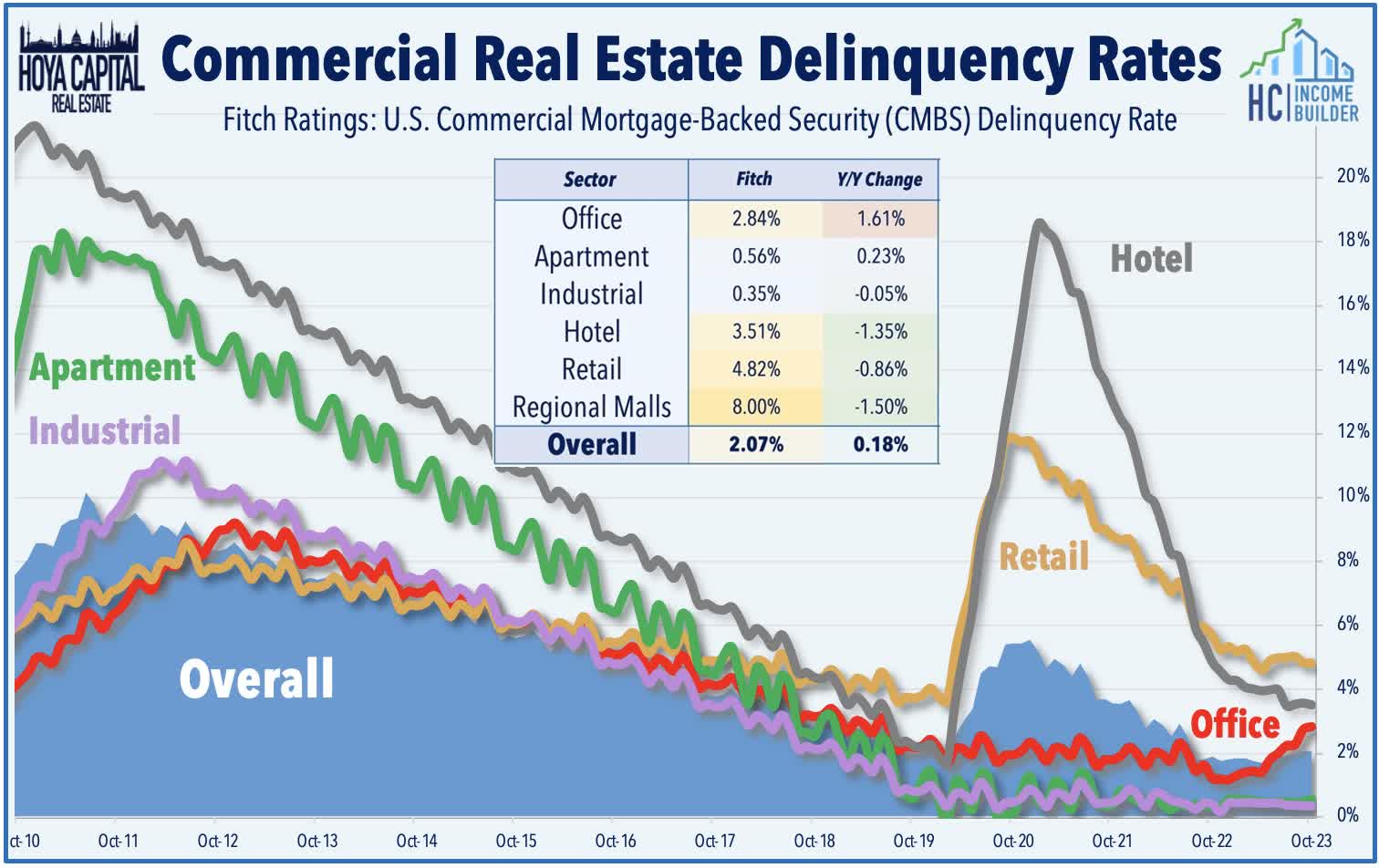

Consistent with the trends we've seen in recent months, transaction activity and default rates typically remain low until this threshold is met, at which point we begin to see a more frenetic pace of activity as the equity balance of the most highly-leveraged sponsors are wiped out, triggering either an outright default or a loan workout. Ratings agency Fitch reports that while overall CRE default rates remained historically at 2.07% in October, the default rate for the office sector has doubled over the past year. Multifamily is the only other sector that has seen an increase in default rates, with many of these defaults coming from "mom and pop" property owners who financed assets with floating-rate bank debt. We're beginning to approach a tipping point for other property sectors and markets, but that's not necessarily a bad thing for public REITs. As noted in our Winners report, well-capitalized public equity and mortgage REITs are positioned to be consolidators in this environment as this capitulation threshold approaches, as these REITs have become the "only game in town" for distressed sponsors given the scarcity of debt capital.

{kind=link}

Apart from the impact of higher interest rates, other "misses" this quarter were more sector-specific or company-specific issues. Expense growth remained stubbornly persistent for residential REITs - which were responsible for the majority of the downward guidance revisions this quarter - with insurance and property taxes surging by double-digits across most markets and segments. While higher rates have tempered development appetite, supply growth has become a near-term headwind for multifamily, industrial, and self-storage as projects that broke ground from mid-2021 through mid-2022 finally reach completion. Meanwhile, the Sunbelt vs. Coastal bifurcation hasn't completely dissipated, but market-level performance is becoming more localized. West Coast weakness remained a common thread across most property sectors - weakness that was especially visible in the " ghost town " of San Francisco - but the New York metro has remained a notable upside standout for nearly all property sectors. Sunbelt activity generally remained stronger than the Coasts, but pockets of oversupply have become headwinds in markets and sectors where development activity faces fewer barriers.

{kind=link}

Loser #1: Apartments

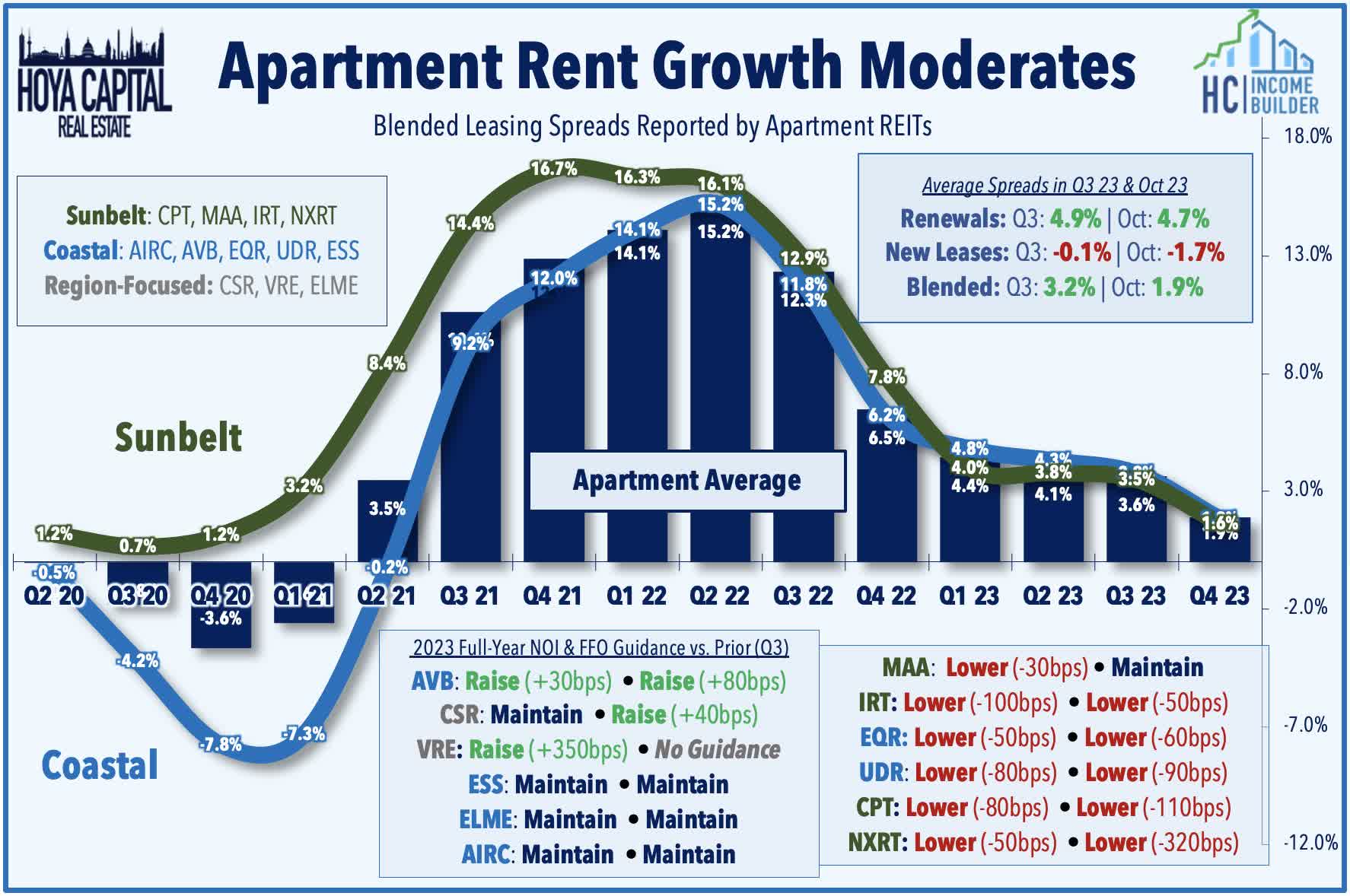

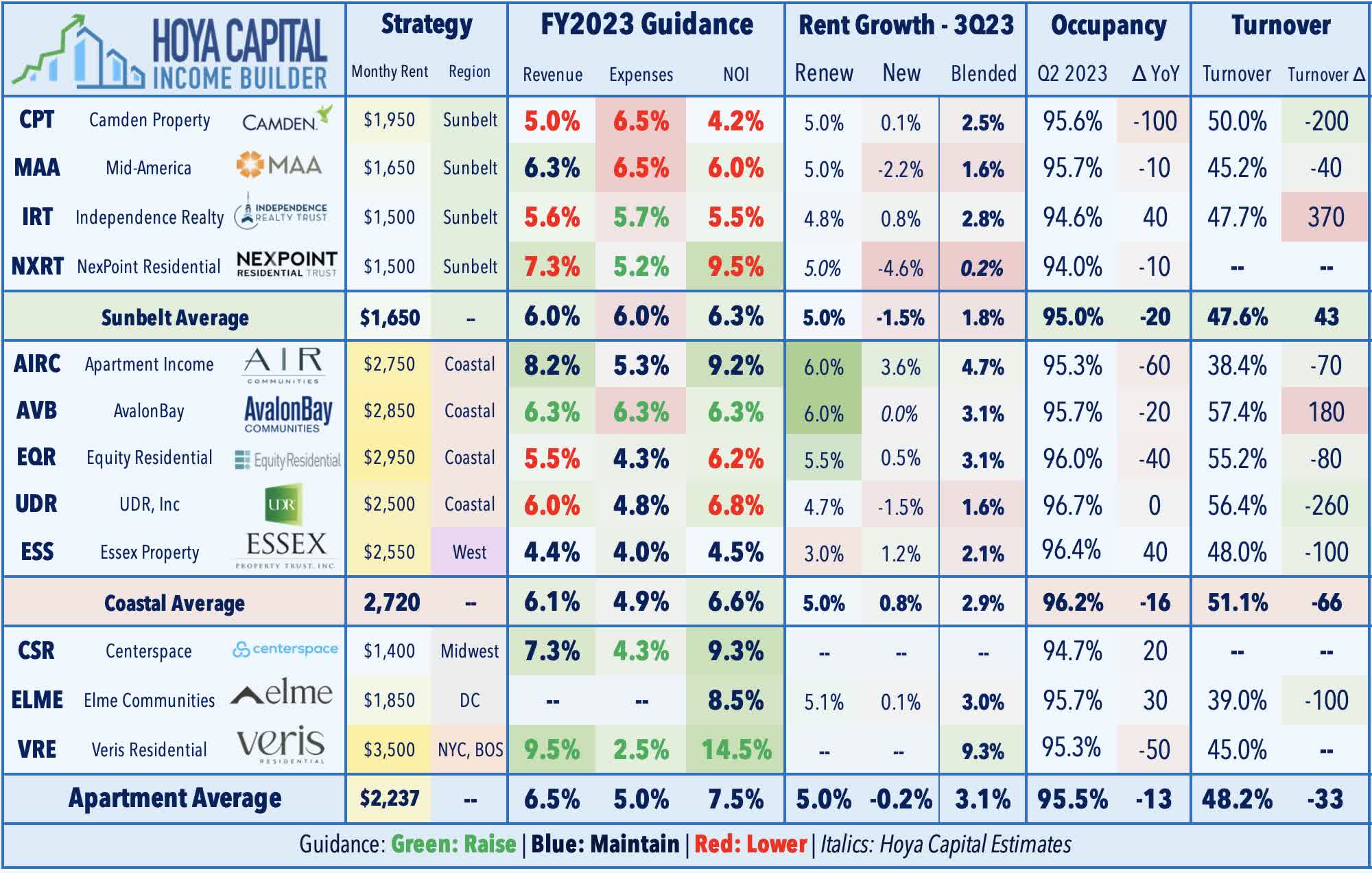

Apartment : (Final Grade: C+) Among the few notable soft spots this earnings season, apartment REITs accounted for nearly half (5) of the total (11) downward revisions to Funds From Operations ("FFO") guidance this quarter. Following a very strong second quarter, fundamentals softened later in the summer, resulting from a combination of modest demand softening, pockets of supply headwinds, and upward expense pressures. Rent growth has moderated from the historic pace seen from mid-2021 through mid-2022, but contrary to the sharply bearish consensus last year, we've seen rent spreads remain positive across most markets, trending towards the typical "inflation-plus" range. Blended rent growth cooled to 3.2% in the third-quarter - comprised of a 4.9% increase on renewal rates, and a 0.1% decline in new lease rates - and cooled further in October, with blended spreads averaging 1.9%. Supply pressures are expected to abate into 2024 given the extremely challenging financing environment for new ground-up development. Despite the uptick in supply, however, occupancy rates remained essentially unchanged from last year, while turnover rates actually declined from last year.

{kind=link}

At the regional level, coastal-focused apartment REITs generally reported stronger results this earnings season as strength from East Coast markets offset weakness out West. AvalonBay ( AVB ) was the upside standout, raising its outlook across the board while noting that it's seeing less supply growth than its peers, given its focus on suburban Coastal markets. Equity Residential ( EQR ) was a notable laggard, lowering its full-year outlook on weakness in its San Francisco and Seattle markets. Apartment Income ( AIRC ) was also a notable upside standout, maintaining its outlook for sector-leading same-store NOI growth of 9.2% in 2023. AIRC also provided an initial 2024 outlook, noting that it expects same-store revenue growth of 3.5%. Supply headwinds are more pronounced in the Sunbelt, driving downward revisions from all four REITs with notably soft results from Camden ( CPT ) - the lone apartment REIT to report negative blended spreads in October.

{kind=link}

Loser #2: Office

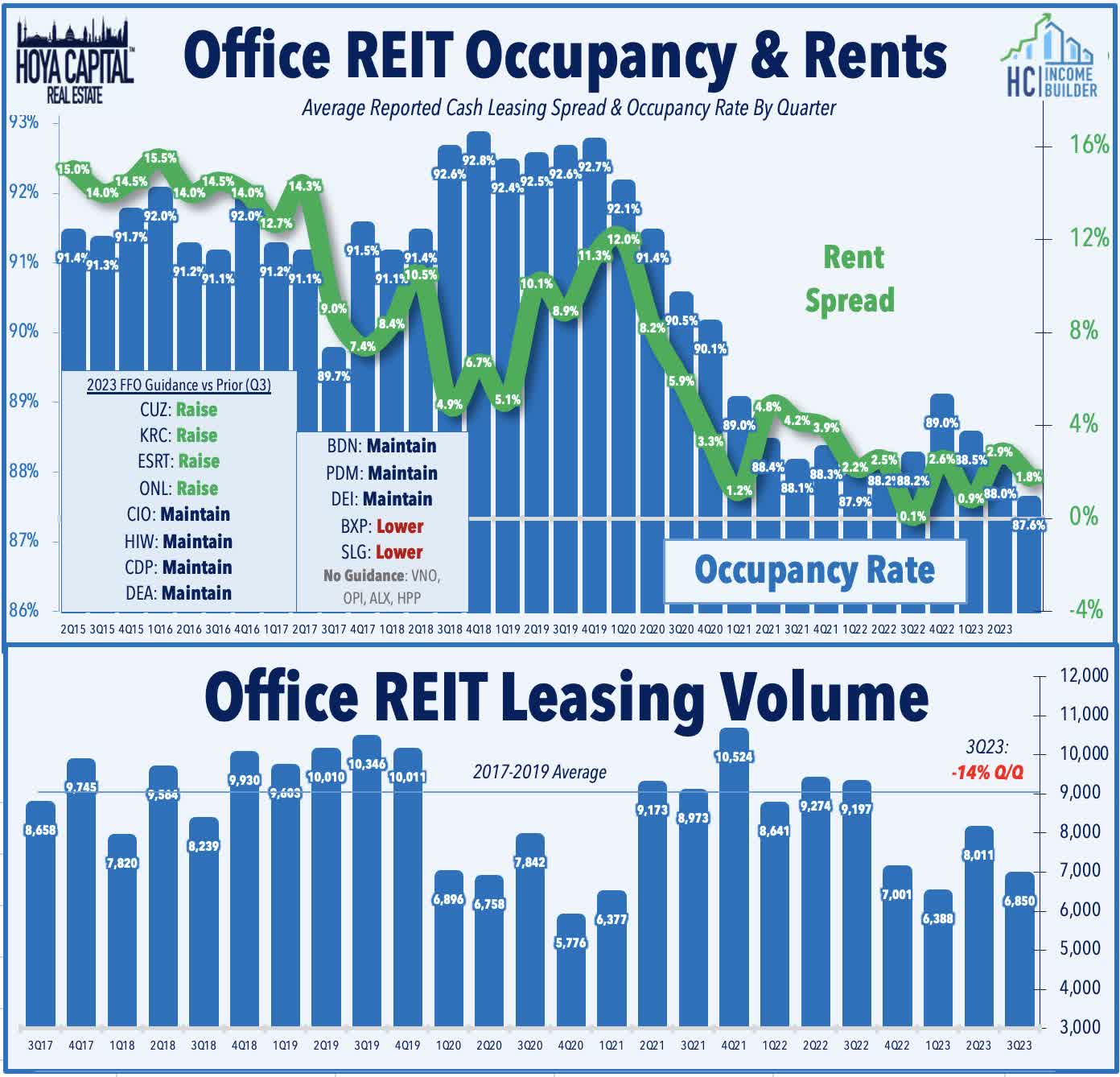

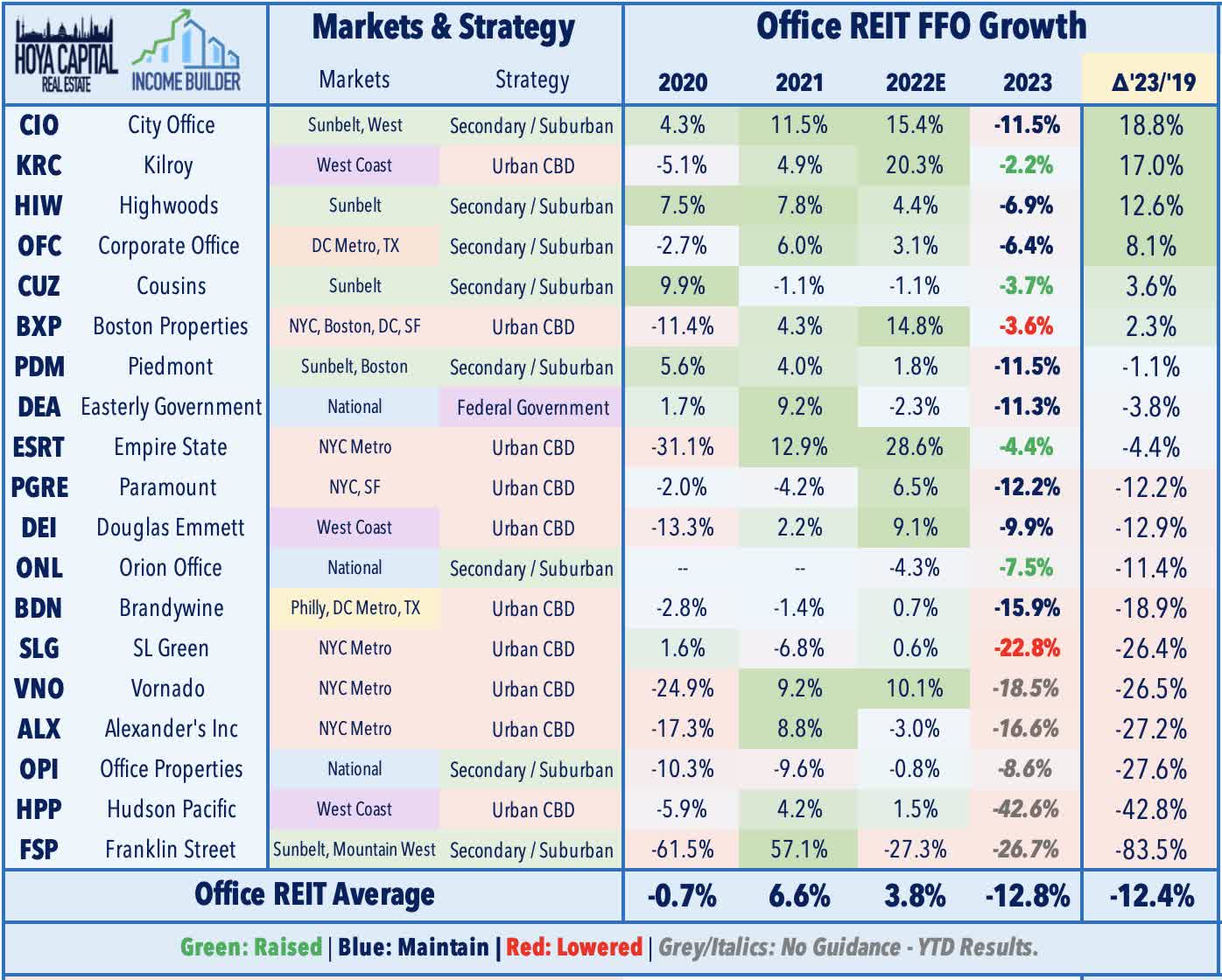

Office : (Final Grade: B-) Results were 'status-quo' for the struggling office sector as daily utilization rates remain "stuck" at around 50% of pre-pandemic levels in coastal urban metros and 75% of these levels in suburban and Sunbelt markets. Unsurprisingly, office REITs earnings results reflected these continued demand headwinds, but Sunbelt and secondary markets continue to exhibit notable - and underappreciated - outperformance over the clearly still-troubled coastal markets. Among the thirteen office REITs that provided full-year guidance, four raised their FFO outlook, seven maintained, while two trimmed guidance. Overall leasing activity was down about 15% from the prior quarter and roughly 25% below the pre-pandemic average from 2017-2019, while cash leasing spreads were essentially flat. Occupancy rates declined to roughly 88% - a new historic low for office REITs - and down from 93% in 2019. We continue to see a wide regional dispersion, as Sunbelt and secondary-focused office REITs reported leasing activity that was only about 10% below pre-pandemic levels, while Coastal-focused REITs reported activity that was 30% below these levels. While NYC has exhibited a solid rebound in recent quarters, particularly in Midtown surrounding suburb transit hub Grand Central, San Francisco is experiencing a continued exodus.

{kind=link}

At the individual stock level, Sunbelt-focused office REITs were upside standouts, including Cousins ( CUZ ), which reported an acceleration in leasing activity in Q3 and achieved rent growth of 9.8% on renewed leases. City Office ( CIO ) was also among the better performers after reporting decent leasing activity and recording positive re-leasing spreads of 3.1% on these leases. Boston Properties ( BXP ) - the largest office REIT - has also been a strong performer this earnings season despite slightly reducing its full-year FFO outlook, which was offset by strong leasing activity. Of note, BXP reported that its NYC properties are seeing 95% mid-week utilization rates, while Boston is at 74% and San Francisco is at just 45%. West Coast-focused Hudson Pacific ( HPP ) has also rebounded this earnings season on an improved outlook for its movie studio segment - which represents about 10% of NOI - following the resolution of a series of Hollywood labor union strikes. Orion Office ( ONL ) - the office spin-off that results from the Realty Income ( O ) and VEREIT merger - has been a laggard despite raising its full-year FFO guidance, after reporting that leasing activity was non-existent in Q3.

{kind=link}

Loser #3: Residential Mortgage REITs

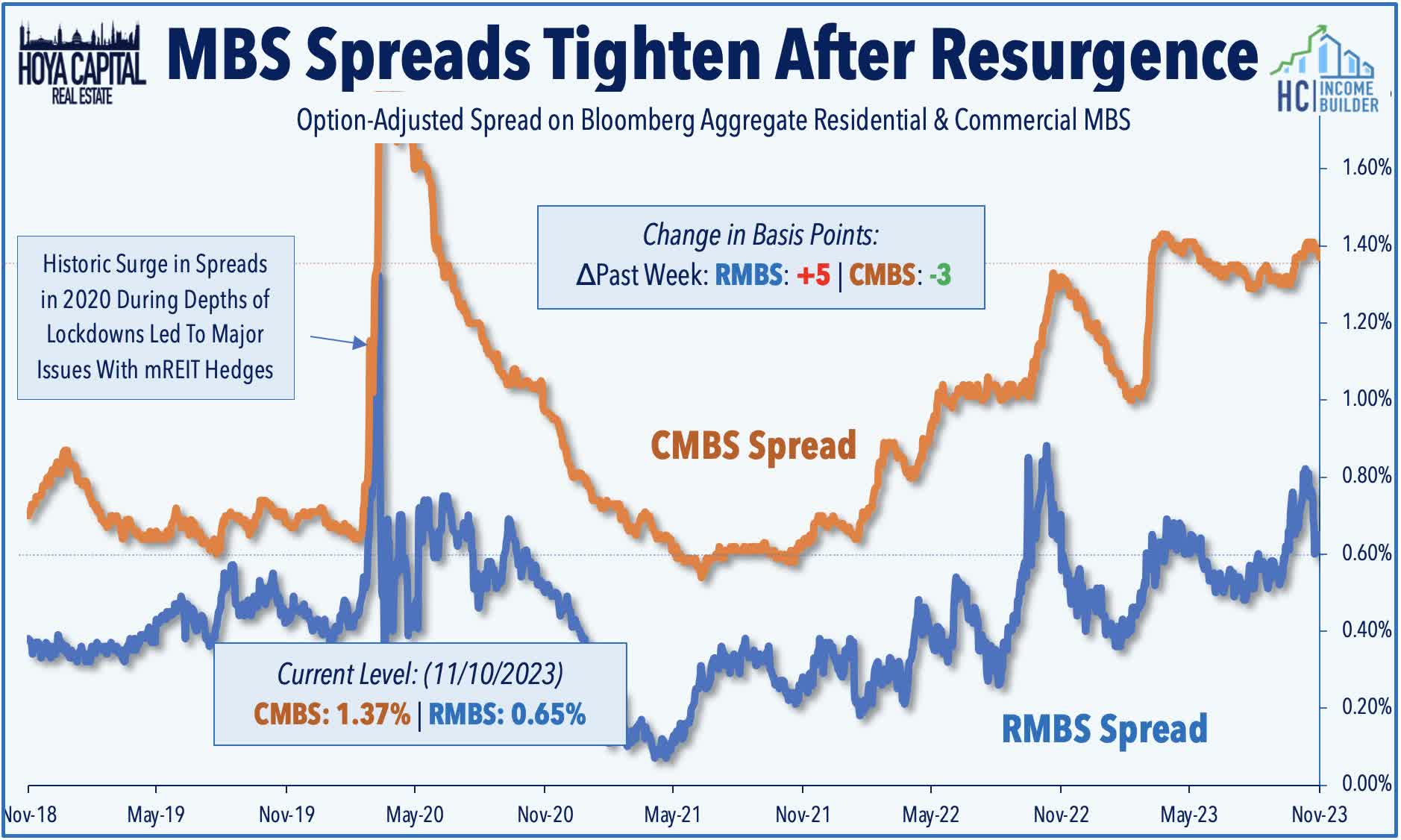

Residential Mortgage REITs : (Final Grade: C+) The (now largely reversed) surge in interest rates and MBS spread-widening wreaked havoc on residential mortgage REITs during the third quarter, resulting in a significant deterioration in book values for mREITs focused on government-backed ("agency") residential MBS. These agency-focused mREITs reported an average decline in Book Value Per Share ("BVPS") of 13.1% during the quarter. AGNC Investment ( AGNC ) - the largest pure-play agency mREIT - reported that its BVPS dipped 14% in Q3, and estimated that its current BVPS as of last week had dipped another 14-15% during October. Among other notable laggards, Orchid Island ( ORC ) - among the most highly-levered mREITs - reported that its BVPS dipped over 20% during the quarter, while ARMOUR Residential ( ARR ) was close behind, reporting a 19% dip in its BVPS. Two residential mREITs announced dividend reductions during the quarter - Chimera ( CIM ) and Great Ajax ( AJX ), bringing the full-year total to 12 -while two mREITs indicated a likely reduction looming in the near future: New York Mortgage ( NYMT ) and ARMOUR Residential ( ARR ).

{kind=link}

Also of note, Great Ajax ( AJX ) plunged after Ellington Financial ( EFC ) called off its planned acquisition, but EFC is "full speed ahead" on its pending merger with Arlington Asset ( AAIC ). Not all residential mREITs were as negatively impacted by the surge in interest rates. PennyMac ( PMT ) - which focuses on the inversely-rate-sensitive Mortgage Servicing Rights ("MSR") business - reported very strong results, noting that its BVPS increased by 1.2% in Q3. Fellow services-focused mREIT, Rithm Capital ( RITM ) has also been a notable upside standout after it reported that its BVPS increased 1%. Results from credit-focused mREITs were mixed, with an average reported decline in BVPS of 5.5% from this cohort. Angel Oak ( AOMR ) was the upside standout among these credit-focused lenders, reporting a decline in BVPS of just 0.5%. AG Mortgage ( MITT ) was also an upside standout, reporting that its BVPS was lower by just 1% in Q3. Despite the wave of dividend reductions this year, residential mREITs still pay an average dividend yield of over 13%.

{kind=link}

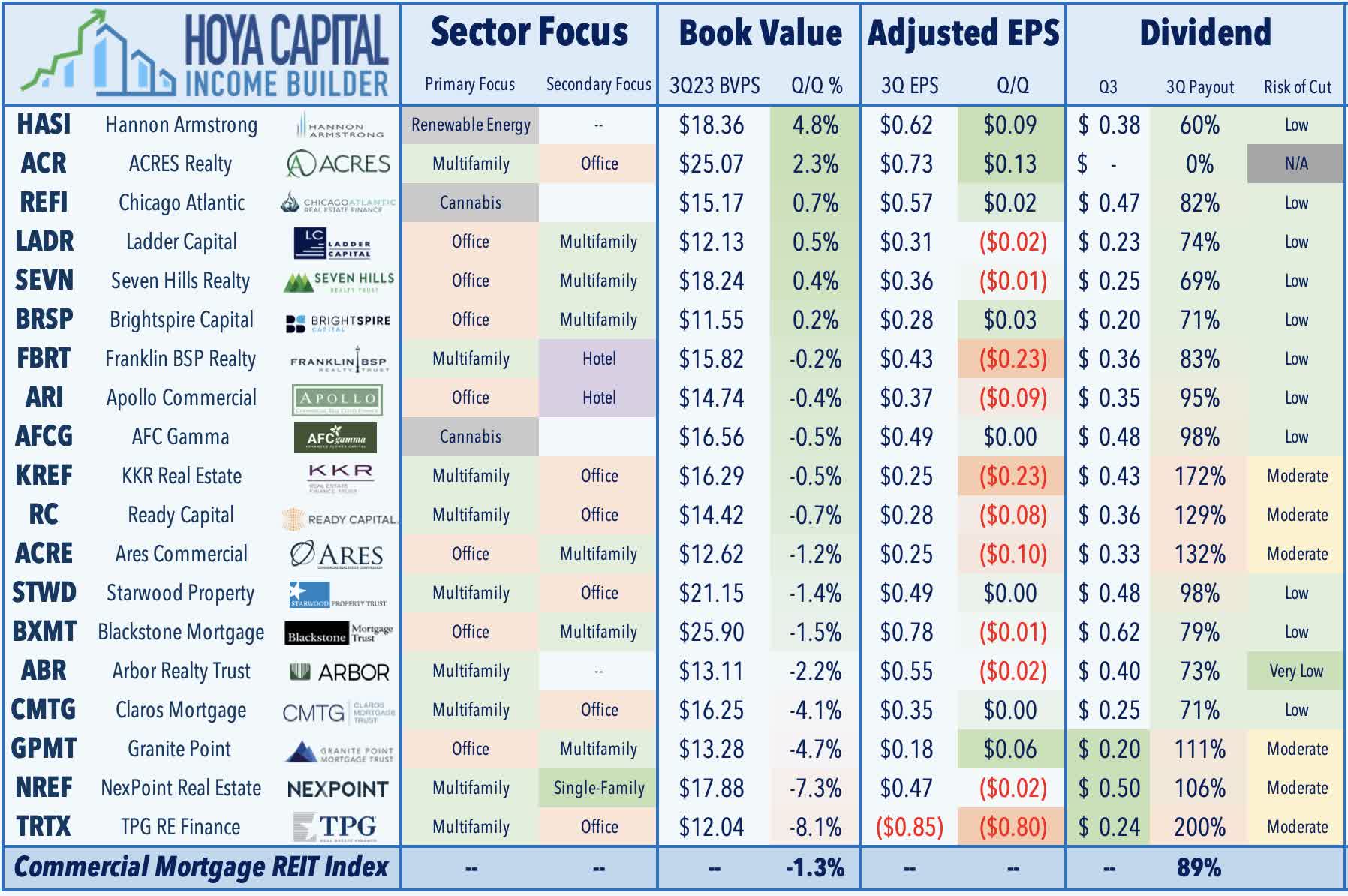

Loser #4: Commercial Mortgage REITs

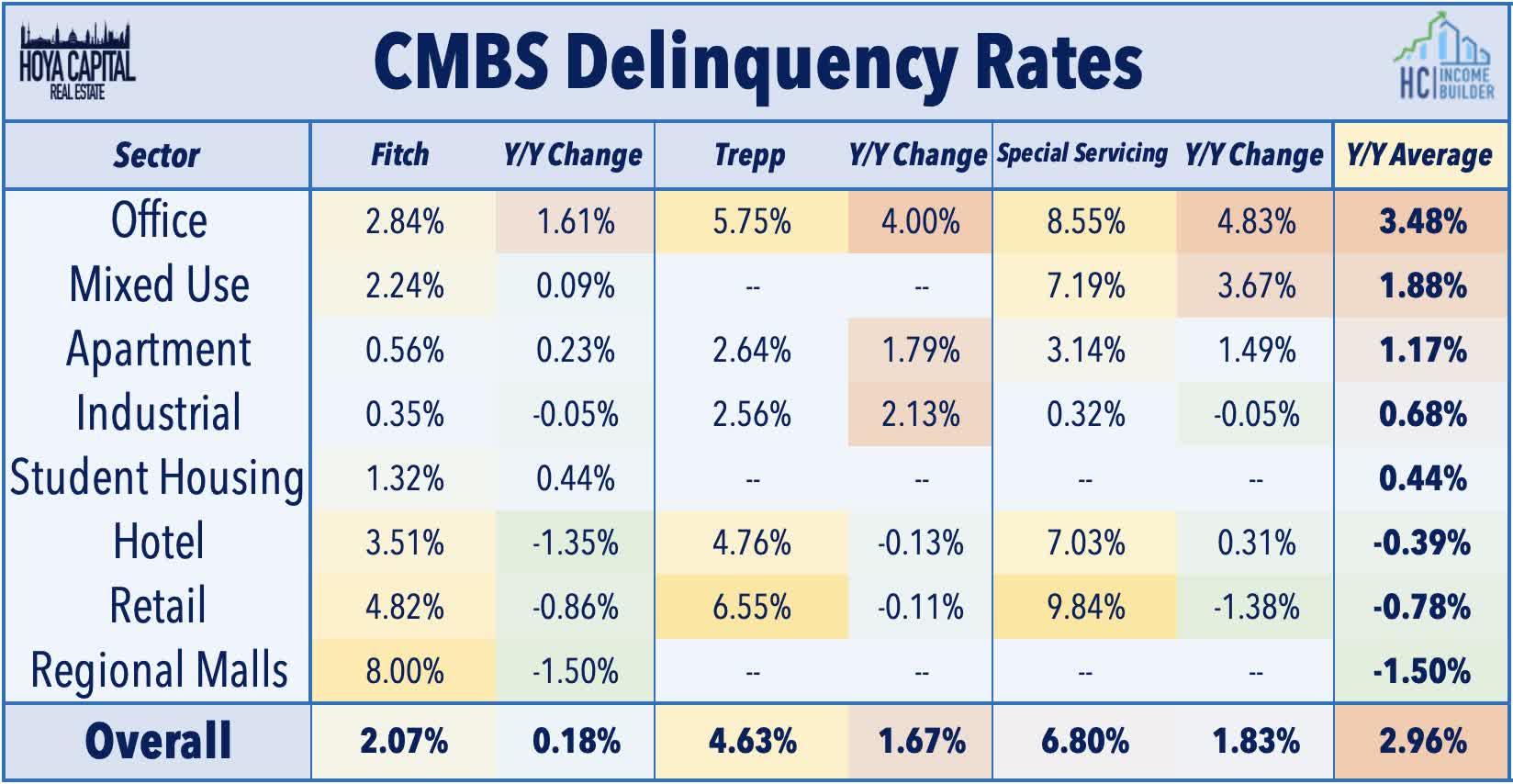

Commercial Mortgage REITs : (Final Grade: B-) On the commercial mREIT side, the movement in BVPS remains far more muted on a quarter-to-quarter basis, with an average decline of about 1% in the third quarter. As noted above, while the narrative on commercial real estate credit is as downbeat as ever, actual loan defaults on CRE loans remain historically low, and the uptick over the past year is almost entirely attributable to office assets. Notably, delinquency rates for hotel and retail assets have actually continued to trend lower over the past year as strong property-level have offset rate-related headwinds on sponsor-level cash flows. Distress is more visible in the earlier stages of delinquency, with Trepp reporting a jump in special servicing rates to 6.8% in October from around 5% in 2022, but given the fact that sponsor leverage rather than property-level fundamentals are often the issue, we're seeing relatively few of these delinquencies progress to an outright default - and when they do, we're seeing healthy recovery rates for lenders.

{kind=link}

All of this is relatively good news for commercial mortgage REITs. The two largest commercial mREITs - Starwood Property ( STWD ) and Blackstone Mortgage ( BXMT ) have been among the stronger-performers this year, and both reported relatively solid third-quarter results as the uptick in office delinquencies continues to be offset by lower-than-expected distress across other property sectors. STWD provided a notably upbeat outlook, commenting, "with the U.S. regional and money center banks having dramatically reduced their real estate lending activities, the lending markets today present tremendous return opportunities. In contrast to many of our public peers, we have actually been deploying capital, and STWD is positioned to become one of the leading private credit alternative firms for real estate and infrastructure lending in the world." Hannon Armstrong ( HASI ) - which focuses on renewable energy lending - has also rebounded this earnings season after reiterating its expectation that distributable EPS is expected to grow at a compound annual rate of 10% to 13% from 2021 to 2024, while dividends are expected to grow at a compounded annual rate of 5% to 8%.

{kind=link}

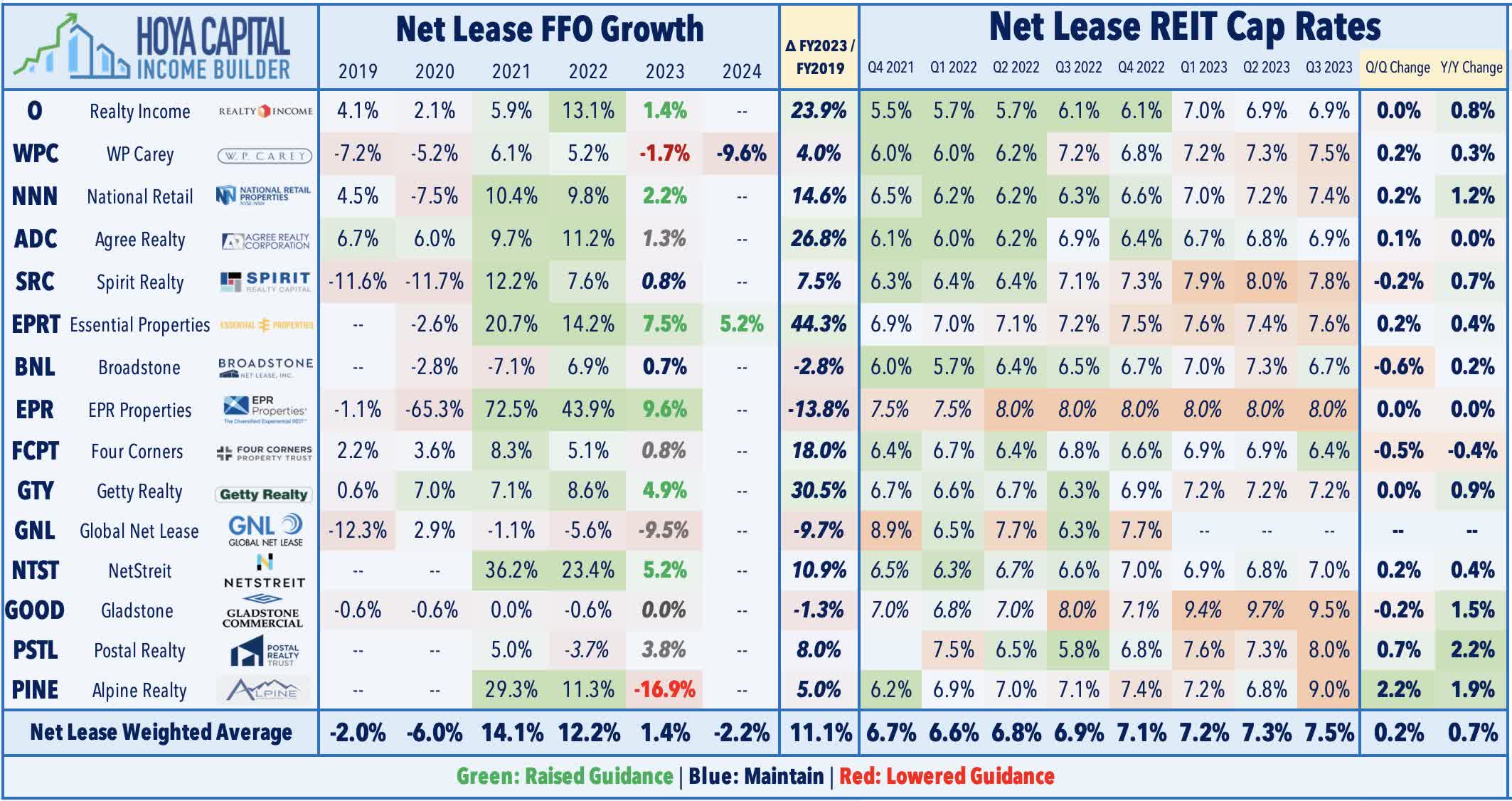

Loser #5: Net Lease REITs

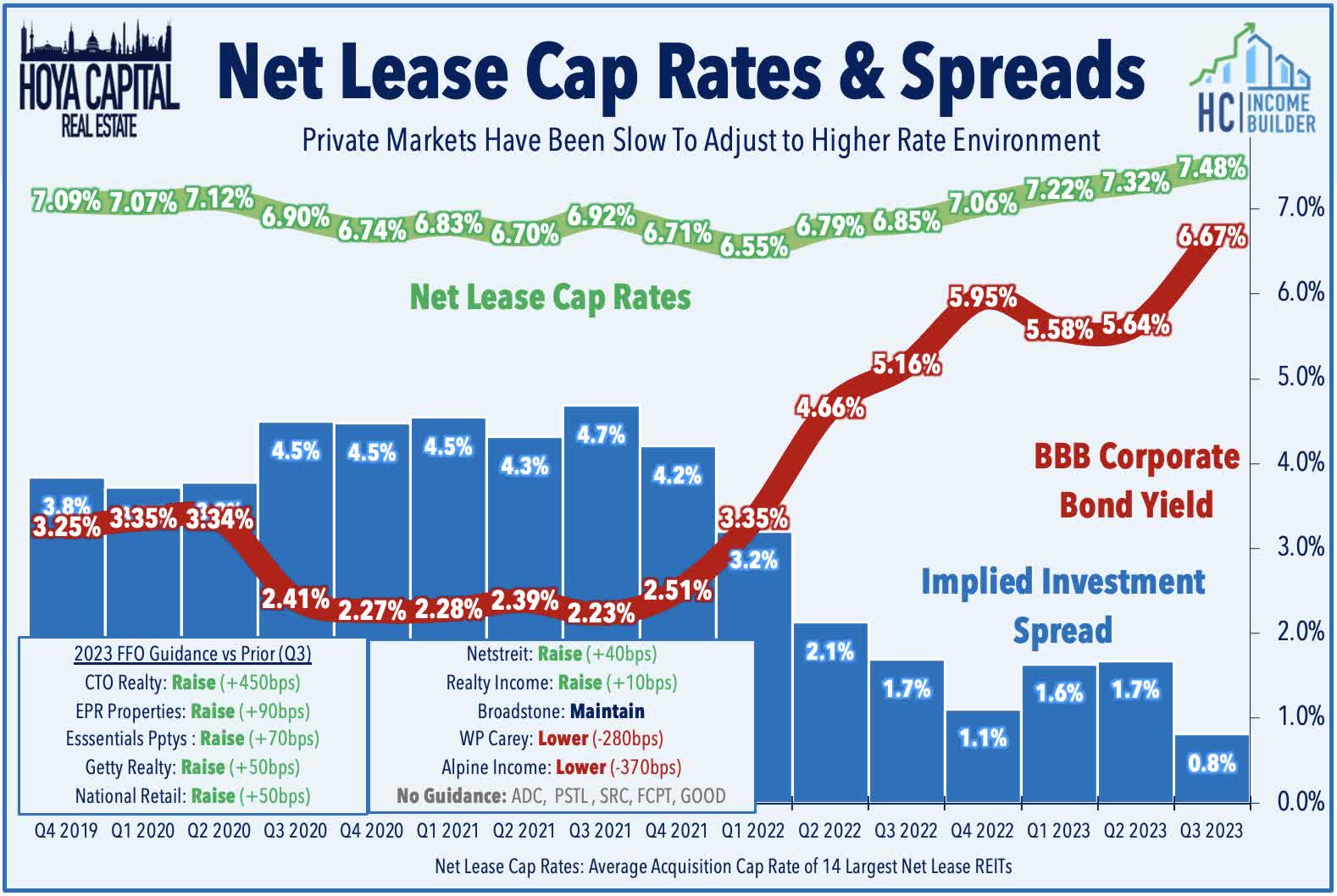

Net Lease : (Final Grade: B) Playing 'chicken' with the Fed? Despite the higher financing costs and stubbornly 'sticky' pricing on private real estate assets, it's full steam ahead for many net lease REITs, which are among the few active buyers left across the real estate industry. Cap rates remained sticky in the third quarter as private market property owners have generally been slow to adjust their valuation expectations to the higher interest rate environment. On average, net lease REIT acquisition cap rates have only about 100 basis points above the lows in late 2021, during which time benchmark financing rates (as implied by the BBB Corporate Bond Yield) increased by roughly 250 bps, which has resulted in significant compression in investment spreads. Seven of the ten net lease REITs that provide guidance raised their full-year outlook, as strong underlying retail performance has helped to offset this more challenging acquisition and financing environment. While most of the mid-cap and small-cap net lease REITs trimmed their acquisitions forecasts, the largest REITs are as hungry as ever, underscored by news that Realty Income ( O ) - the largest net lease REIT - will acquire Spirit Realty ( SRC ) in a $9.3B all-stock deal.

{kind=link}

Upside standouts this quarter included Essential Properties ( EPRT ), which boosted its full-year FFO growth guidance to 7.5% - up 70 basis points - and provided initial 2024 guidance calling for FFO growth of another 5.4%. EPR Properties ( EPR ) raised its full-year FFO growth guidance to 9.6% - up 90 basis points - driven by "significant deferral collections" and the improved outlook related to its restructured master lease agreement with movie theater operator Regal. Netstreit ( NTST ) raised its full-year FFO growth outlook of 5.2% - up 40 basis points. Getty Realty ( GTY ) boosted its full-year FFO growth target to 4.9% - up 50 basis points - while also boosting its dividend by 4.7% to $0.45/share (6.8% dividend yield). Besides W.P. Carey ( WPC ), which trimmed its FFO outlook following its "strategic exit" from office - Alpine Income ( PINE ) was the lone net lease REIT to lower its FFO outlook, pressured by rising interest expense and the bankruptcy of one tenant. Providing additional color on the transactions environment, PINE noted, "the market's very tepid in the standoff between buyers and sellers" and noted that the challenging debt market will be "a factor in creating some opportunities."

{kind=link}

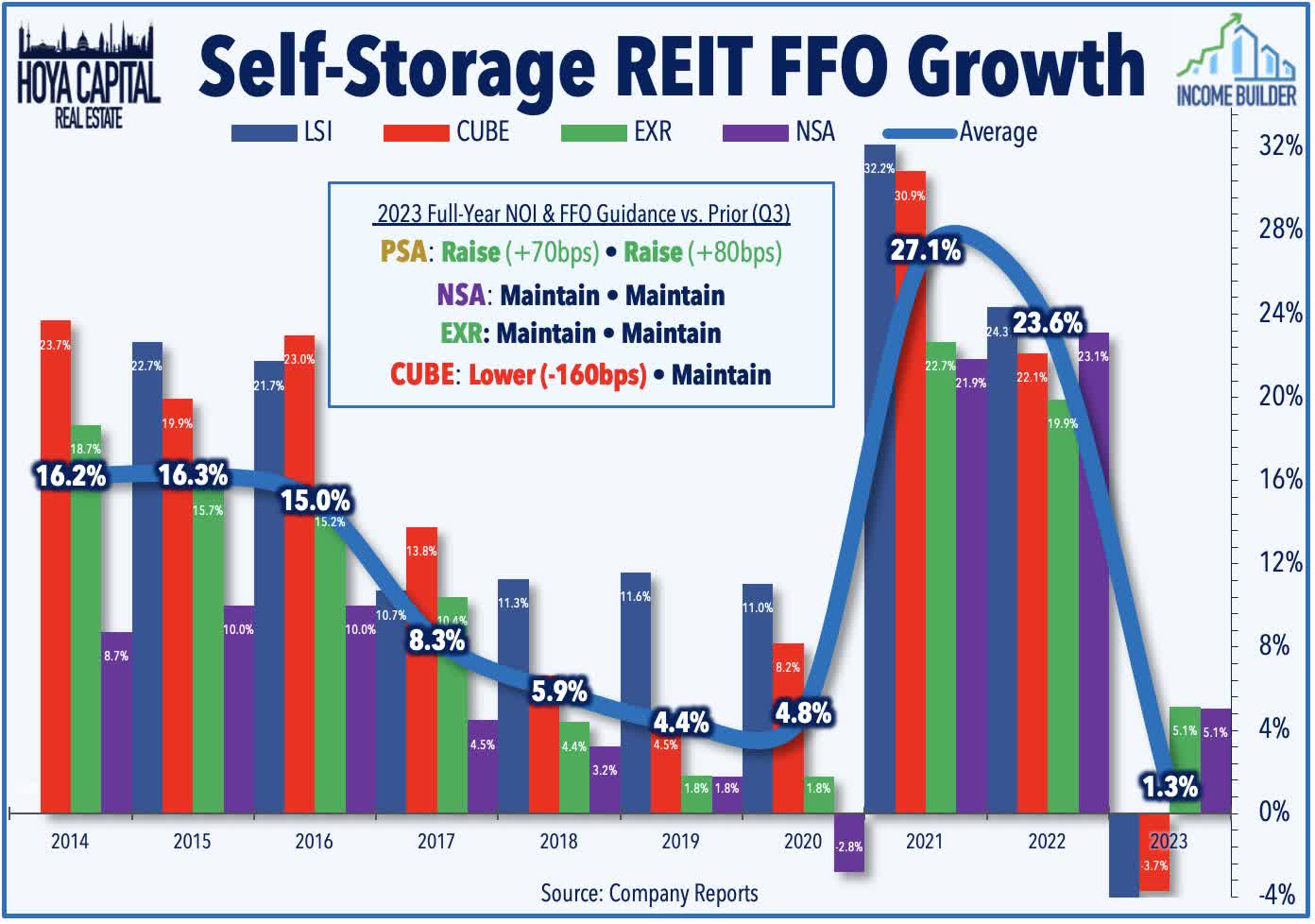

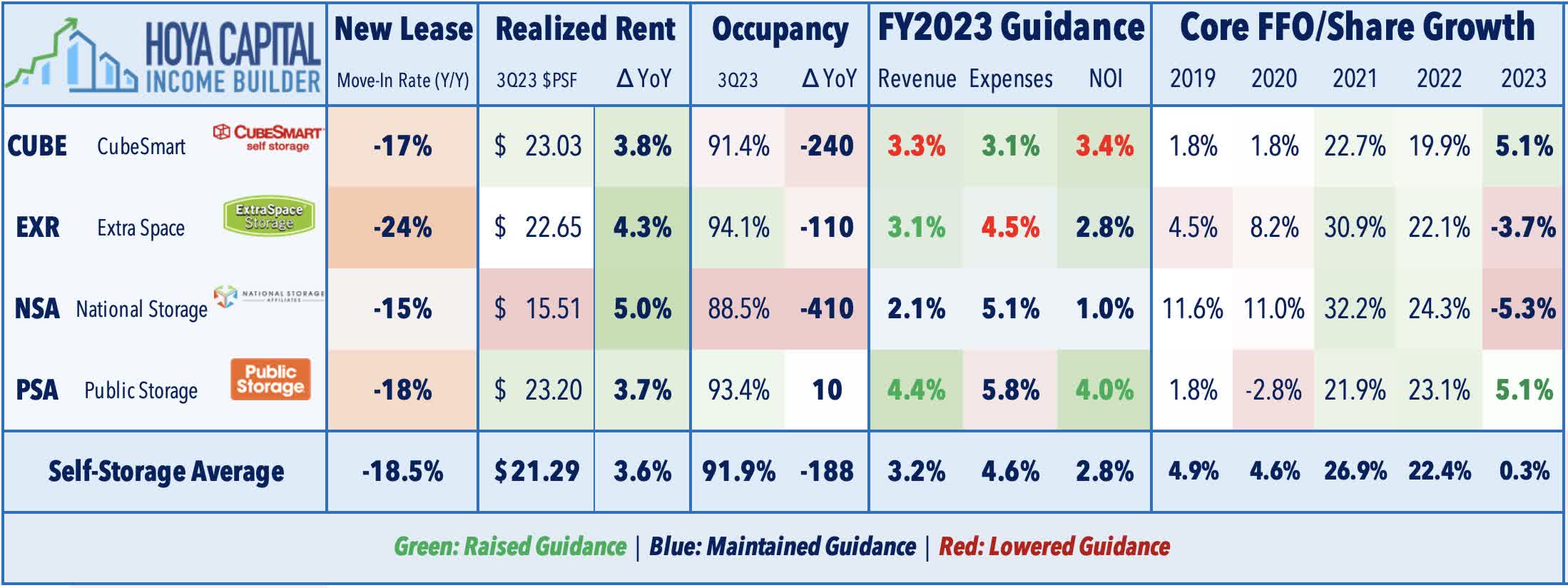

Loser #6: Storage

Storage : (Final Grade: B-) The sector with the strongest aggregate NOI growth since the start of the pandemic, self-storage REITs have faced more challenging fundamentals this year as the pandemic-era boom in housing activity - which fuels demand for self-storage - has moderated amid the surge in mortgage rates. Third-quarter results were not nearly as weak as the prior quarter, but headwinds on both the supply-front and demand-front persist heading into 2024. As with Q2, all four self-storage REITs reported double-digit declines in "street rates" on new customers in Q3, but this pricing weakness was more-than-offset by mid-single-digit rent growth on renewal leases, resulting in a total rent PSF increase of about 4% compared with last year. While 'sticky' demand and steady rent growth on existing tenants is a feature of the sector, the pricing gap can only extend so far before tenants pack up and move to another nearby facility, offering ample concessions and lower rent. Occupancy rates declined to 91.9% in Q3 - the first quarter below the comparable pre-pandemic level from 2019 - and we'll likely see this dip further as supply growth remains elevated through mid-2024.

{kind=link}

The strongest report came via Public Storage ( PSA ), which raised its full-year NOI and FFO outlook, citing continued strength in its California markets - one of the lone exceptions to the West Coast underperformance theme, as restrictive zoning has limited new self-storage development in recent years. Extra Space ( EXR ) has surged this earnings season after reporting rapid progress on its integration with Life Storage - which it acquired in July - and noted that it has reached its anticipated G&A expense savings run rate, and is on pace to reach its total synergies by next quarter. National Storage ( NSA ) has also seen a solid rebound in recent weeks after maintaining its full-year outlook and commenting that its "toughest comps are behind us as far for street rate and year-over-year occupancy." CubeSmart ( CUBE ), meanwhile, reported strength in its suburban NYC markets but noted that the overall pricing environment "really started to change in a meaningful way in September and into October... [which] necessitated us to lower pricing on new customers more than we previously thought."

{kind=link}

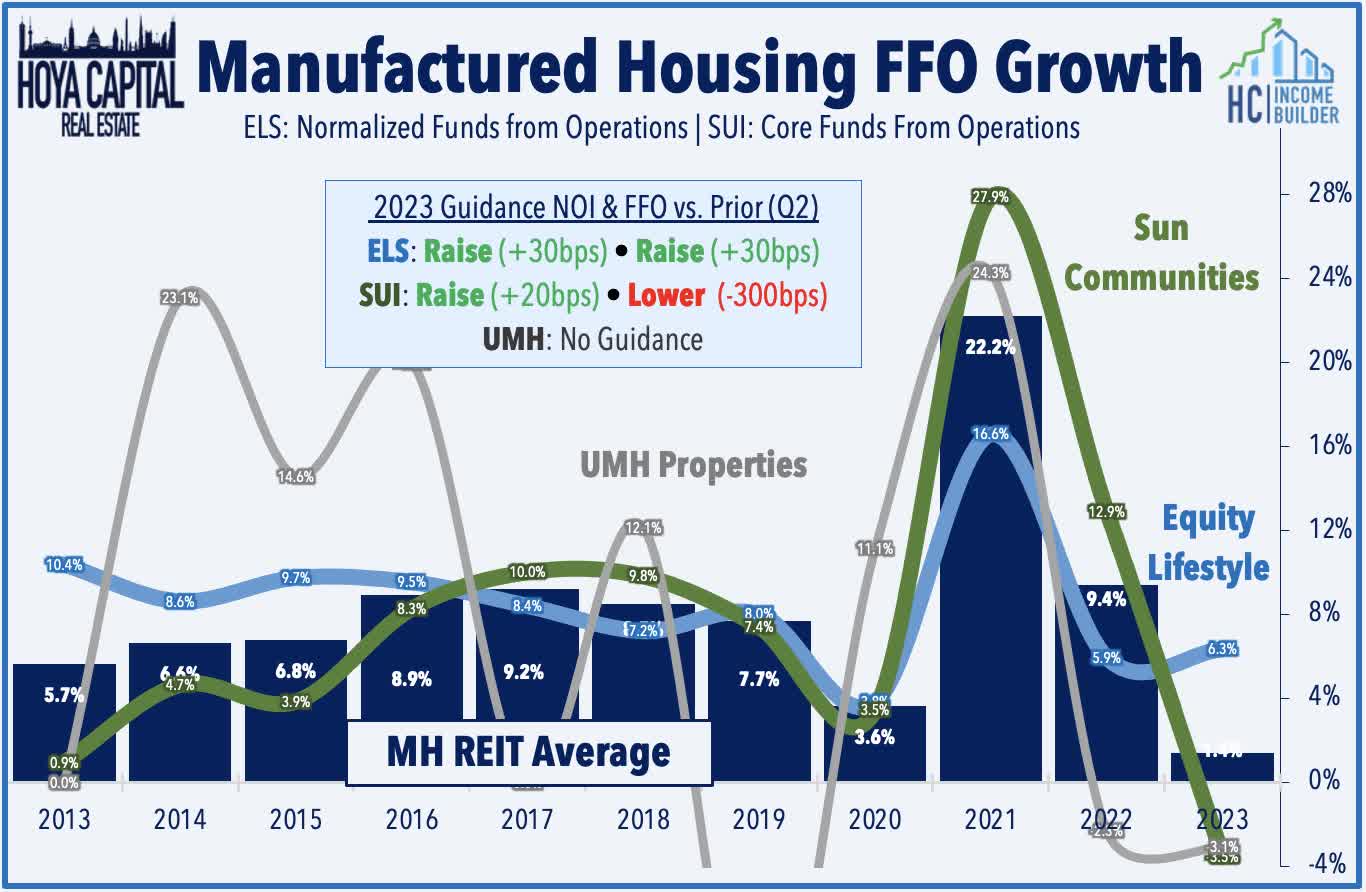

Loser #7: Manufactured Housing

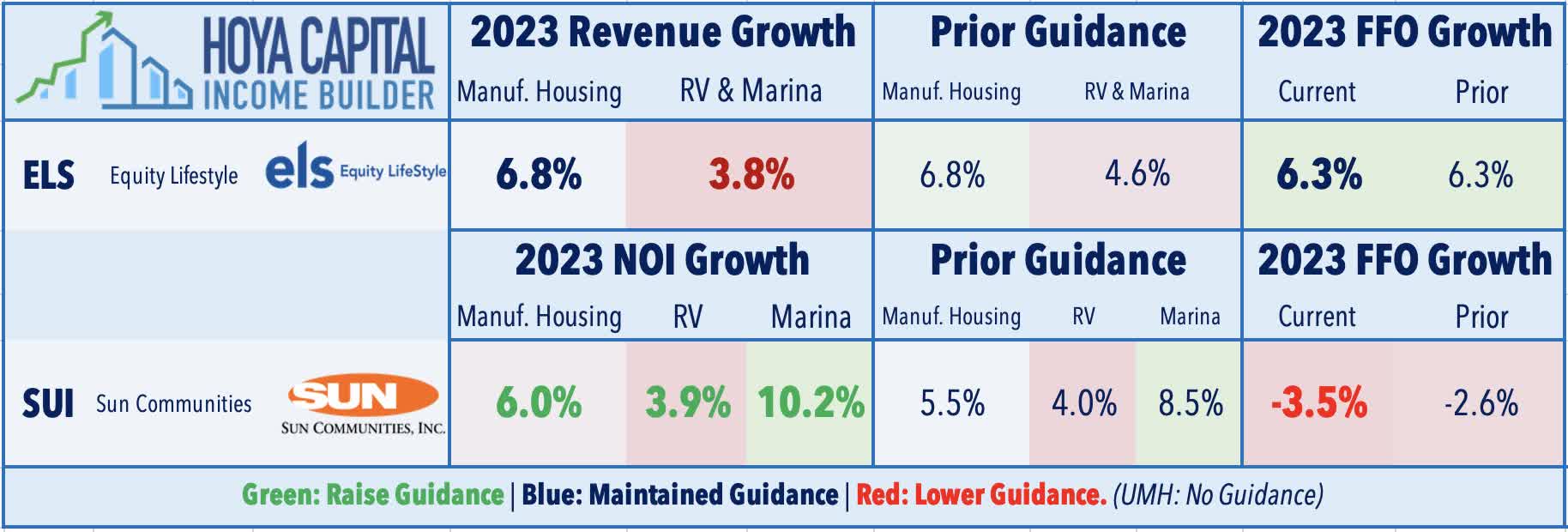

Manufactured Housing : (Final Grade: B-) Similar to self-storage REITs, the previously high-flying manufactured housing REIT sector has fallen on tougher times this year, but third-quarter results were stronger than the downbeat Q2 earnings season. Sun Communities ( SUI ) has rebounded this earnings season after reporting solid results, as strong property-level fundamentals in the U.S. offset ongoing weakness in its international segments. SUI boosted its full-year NOI growth outlook for each of its three U.S. business segments, projecting growth of 6.0% in its core MH portfolio, 3.9% in its RV segment, and 10.2% in its marina segment. Sun also established preliminary guidance for 2024, noting that it expects MH rent growth of 5.4%, RV rent growth of 6.5%, and marina rent growth of 5.6%. Sun's ill-timed international expansion into the UK last year continues to weigh on its FFO, however, as continued weak home sales performance in its Park Holiday portfolio and a separate default on a $361M loan to a different UK MH operator prompted a downward revision to its FFO forecast.

{kind=link}

Elsewhere, Equity LifeStyle ( ELS ) maintained the midpoint of its full-year growth FFO outlook at 6.3% and maintained its full-year outlook for MH same-store revenue growth at 6.8%. Excluding the struggling transient RV component, full-year revenues in the RV & Marina segment are expected to increase 8.6% for the year. ELS also noted that it will begin sending renewal offers to its MH residents this month for the 2024 period, with average rent increases of 5.4%. ELS has set annual rates on 95% of its annual RV sites, with average rent increases of 7.0%. UMH Properties ( UMH ) - which does not provide full-year guidance - reported in-line results this quarter, as strong property-level performance offset the impacts of higher interest expense on its relatively highly-levered balance sheet, which still has about 20% of its debt subject to floating interest rates. UMH also noted that it is sending out rent increases for 2024 in the "5% to 6%" range and maintained its target to achieve sequential quarterly occupancy gains of 25 to 50 basis points.

{kind=link}

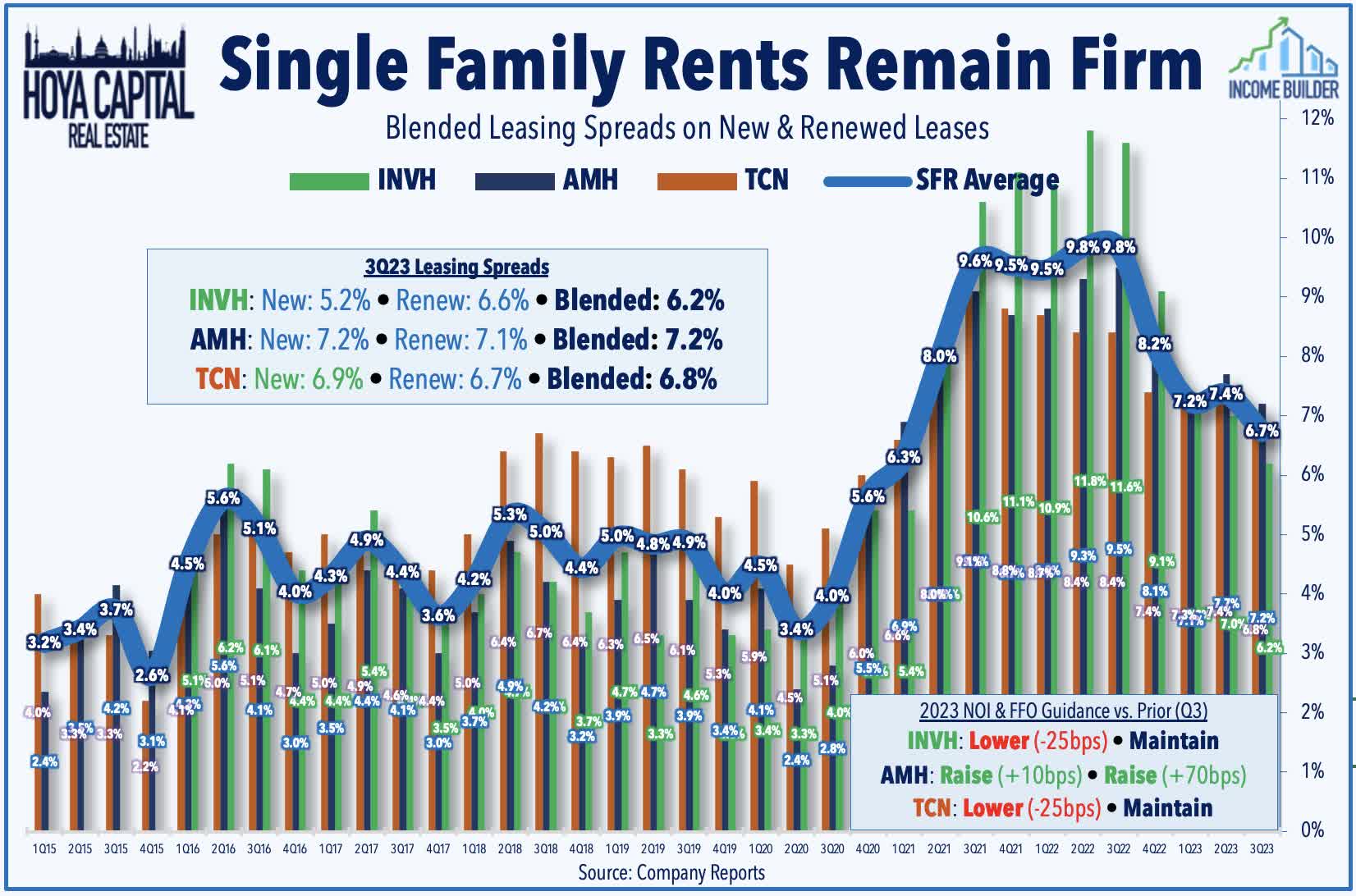

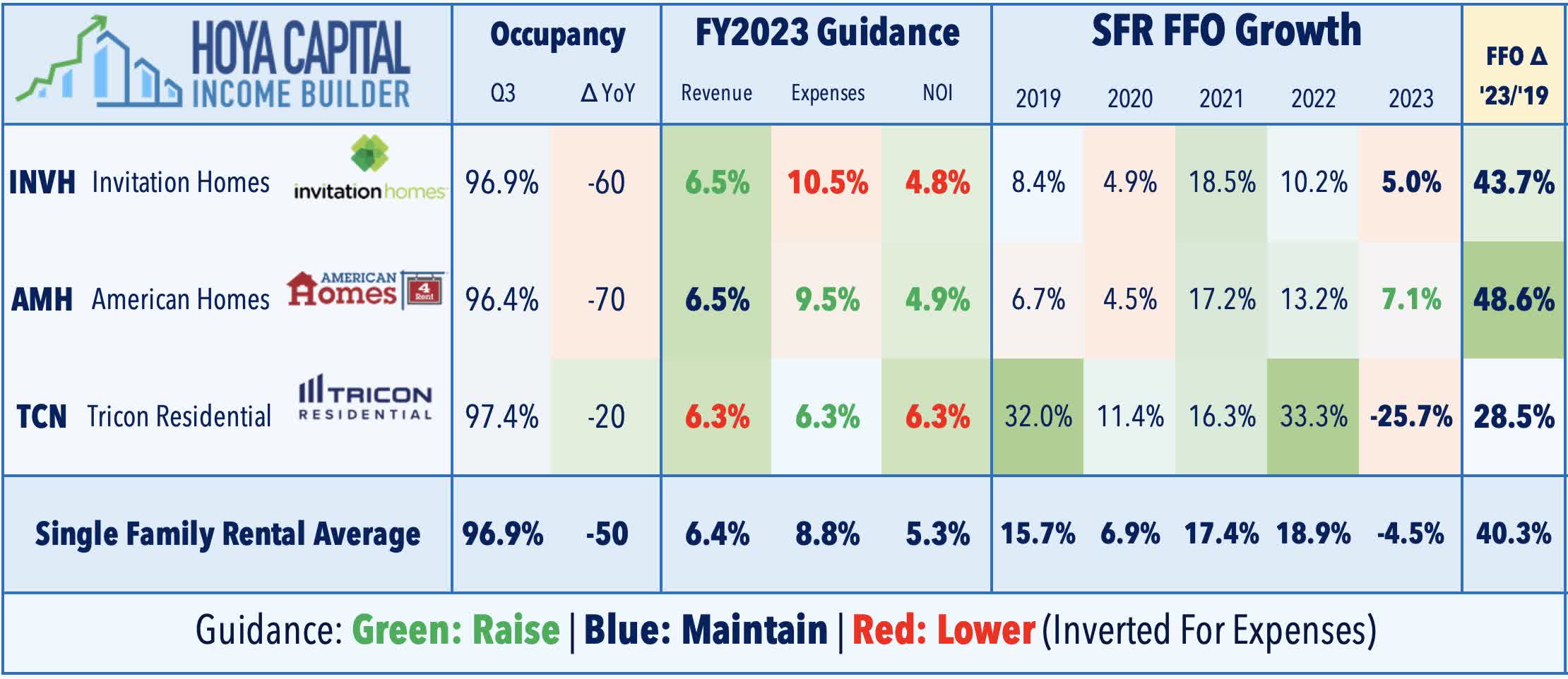

Loser #8: Single-Family Rental

Single-Family Rental : (Final Grade: B) Rent growth trends have been quite a bit stronger on the single-family side - which is not facing the same supply headwinds as their multifamily peers - but expense pressures remain a headwind. Invitation Homes ( INVH ) - the largest single-family housing owner in the U.S. - reported mixed results and trimmed its full-year NOI outlook on higher property taxes and insurance expenses. INVH maintained its full-year AFFO outlook - which calls for 5.0% growth this year - but trimmed its same-store NOI guidance to 4.8% - down 20 basis points. INVH expects same-store expenses to rise 10.5% this year, and reported that property tax expense was higher by 13% year-over-year, while insurance expense was 15% higher. Leasing trends remained solid, however, with INVH recording blended leasing spreads of 6.2% comprised of 6.6% increases on renewals and 5.2% increases on new leases. While new homeowners can now expect to pay in excess of 8% on a new mortgage, INVH noted that it raised $800M in Q3 at an average interest rate below 5.5%. This cost of capital advantage facilitated a robust quarter of acquisitions, with INVH buying 2,291 homes for $854 million.

{kind=link}

Sunbelt-focused American Homes ( AMH ) was the upside standout of the group, reporting strong results and raising its full-year outlook. AMH now expects full-year FFO growth of 7.1% - up 70 basis from last quarter - and expects same-store NOI growth of 4.9% - up 10 basis points from last quarter. Providing some initial commentary on 2024, AMH noted that it expects rent growth to be "better than historical averages" and noted that it has continued to throttle the increases on renewal leases, estimating that its "loss to lease" is still 4% below market rents. Tricon Residential ( TCN ) - the smallest and most highly-levered of the three SFR REITs - has rebounded this earnings season on the heels of the interest rate retreat. TCN maintained its full-year FFO outlook, which calls for its FFO to revert back to 2021-levels following last year's 30% increase, a decline due entirely to higher interest expense. TCN slightly trimmed its same-store revenue growth target to 6.25% from 6.50% to reflect "softer rent growth on new move-ins" but favorably revised its expense outlook to reflect a "successful reduction of controllable expenses, including property management, repairs, maintenance and turnover." TCN also trimmed its full-year outlook for home acquisitions to 1,850 from 2,000 to "allow for lower leverage parameters" in its JV investment programs.

{kind=link}

Recap: Strong Quarter, With Few Exceptions

After covering the Winners of REIT Earnings Season last week, Part 2 of our Earnings Recap focused on the worst-performing property sectors and common threads shared by these laggards. Unlike the second quarter, which saw a handful of poor reports and unexpectedly steep guidance and dividend cuts, there were no major 'bombshells' this earnings season. Among the soft spots, however, expense growth remained stubbornly persistent for residential REITs - which were responsible for the majority of the downward guidance revisions this quarter - with insurance and property taxes surging by double-digits across most markets and segments - while supply growth is a modest near-term headwind for multifamily, industrial, and self-storage. Surging interest expense was again the culprit behind the balance of the downward revisions. For lenders, defaults have accelerated, but recovery rates remain high. External growth for public REITs remains challenged for now, but REITs that played it safe during the "boom times" will likely have opportunities as reality sets in for many over-levered private-market property owners who weren't prepared to handle either higher rates or lower property values.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Losers Of REIT Earnings Season