NLCP - Losers Of REIT Earnings Season

2023-05-11 10:00:00 ET

Summary

- After covering the Winners of REIT Earnings Season earlier this week, Part 2 of our Earnings Recap focuses on the worst-performing property sectors and common threads shared by these laggards.

- While there were upside standouts and some solid reports within these lagging property sectors, the losers of REIT earnings season included: Office, Mortgage, Land & Agriculture, Retail, and Non-Traded REITs.

- For Office and Mortgage REITs, dividend cuts have begun to mount, with 15 combined reductions between the two sectors this year. Other sectors have seen increases outpace cuts by 44-to-1.

- Commodities disinflation was a major theme for the agriculture-focused REIT sectors - farmland, timber, and cannabis REITs. From their peaks, lumber prices are down 75% and grain prices are down nearly 40%.

- 'Flight to quality' was a major theme this earnings season, with small and micro-cap REITs significantly lagging larger-cap names. For retail REITs, the high-profile bankruptcy of Bed Bath & Beyond overshadowed an otherwise solid slate of reports showing buoyant rent growth.

Real Estate Earnings Recap: Part 2

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on May 7th.

{kind=link}

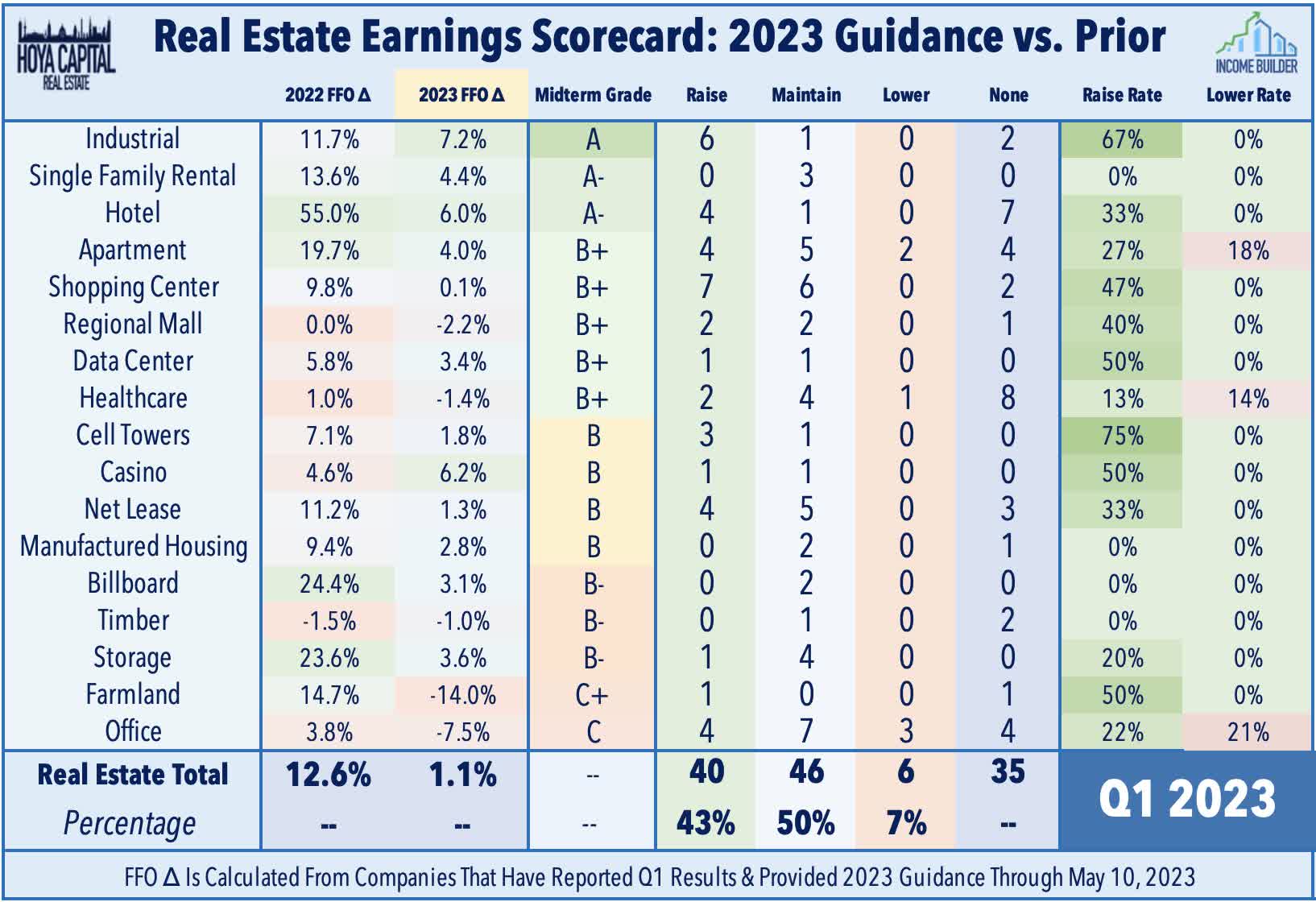

In Part 1 of our Earnings Recap - Winners of REIT Earnings Season - we discussed the nine best-performing property sectors, a list that included Residential REITs, Industrial REITs, Hotel REITs, and Casino REITs. We noted - with some exceptions discussed in this report - REITs delivered surprisingly strong results. Of the 92 equity REITs that provide full-year Funds from Operations ("FFO") guidance, 40 (43%) raised their full-year earnings outlook, while 6 (7%) lowered guidance - a FFO beat rate that exceeded the historical REIT average of 40% for the first quarter. The "beat rate" for the critical property-level metric - same-store Net Operating Income ("NOI") - was actually slightly better, with over 50% of REITs providing upward revisions.

{kind=link}

In Part 2 below, we discuss the nine worst-performing property sectors. While there were upside standouts and some solid reports within these lagging property sectors, the losers of REIT earnings season included: Office, Mortgage, Land & Agriculture, Retail, and Non-Traded REITs. For Office and Mortgage REITs, dividend cuts have begun to mount, with 15 combined reductions between the two sectors this year including 7 cuts this earnings season. Other property sectors have seen increases outpace cuts by 44-to-1 including 7 dividend increases this earnings season. Earnings call commentary suggests that we'll see a handful of additional reductions in the months ahead as over-levered REITs look to redeploy this capital to pay down variable rate debt, but expect these reductions to remain largely within the office and mortgage REIT sectors.

{kind=link}

For retail REITs, the high-profile bankruptcy of Bed Bath & Beyond and lingering recession fears overshadowed an otherwise solid slate of reports showing impressive pricing power and occupancy rates recovering back above pre-pandemic levels. While buoyant rent growth was an upside surprise benefiting retail, residential, industrial, and healthcare REITs, commodities disinflation was a major theme for the agriculture-focused REIT sectors - farmland, timber, and cannabis REITs. From their peaks, lumber prices are down 75%, grains prices are down nearly 40%, cannabis prices have dipped 50%. The effects of the significant rise in interest rate expense also remained a common thread seen across many of these sectors as well - nearly all of which are among the more highly-levered property sectors - with a direct earnings hit amounting to 5-10% of FFO for full-year 2023, and as high as 25% for a small handful of highly-levered REITs.

{kind=link}

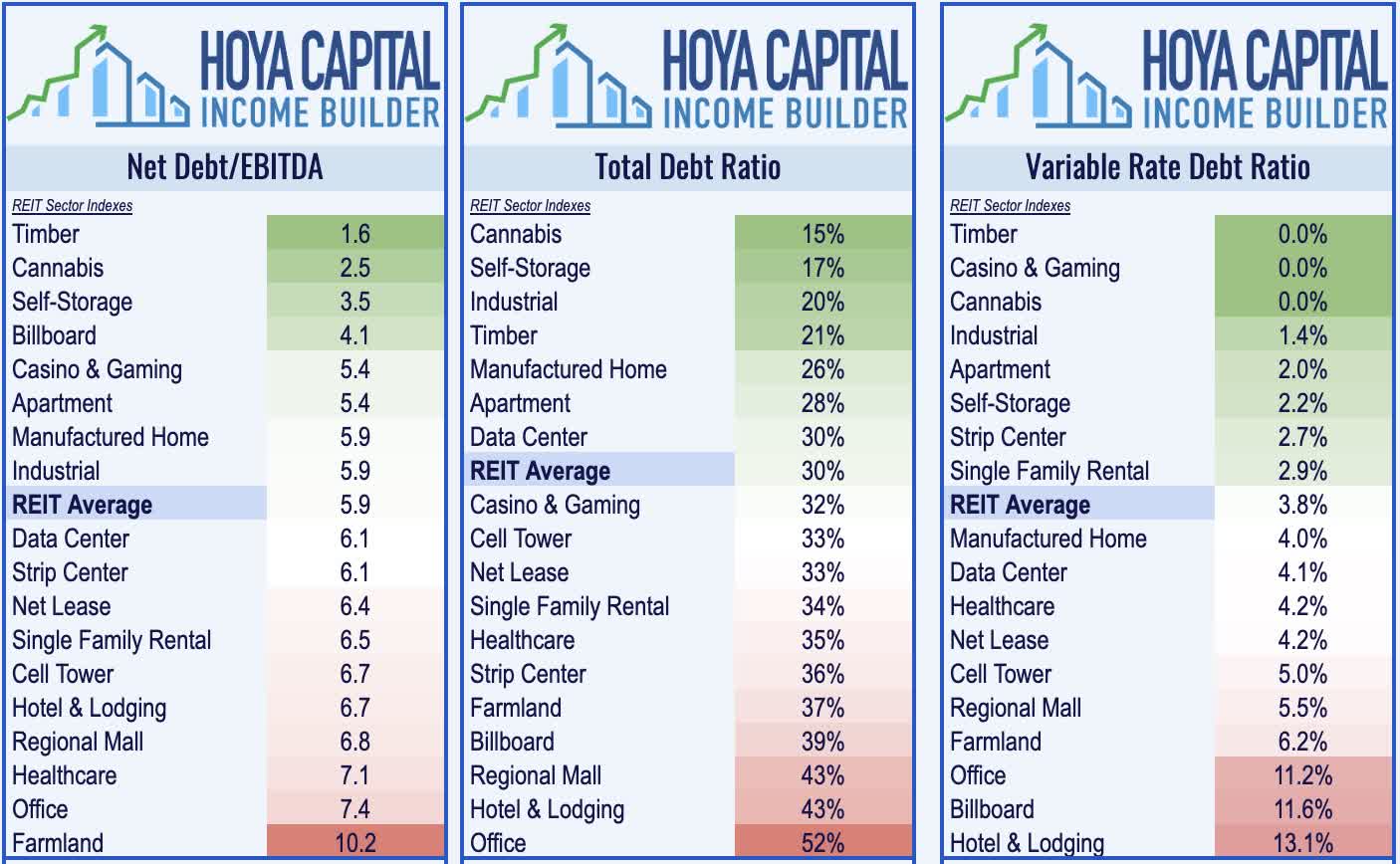

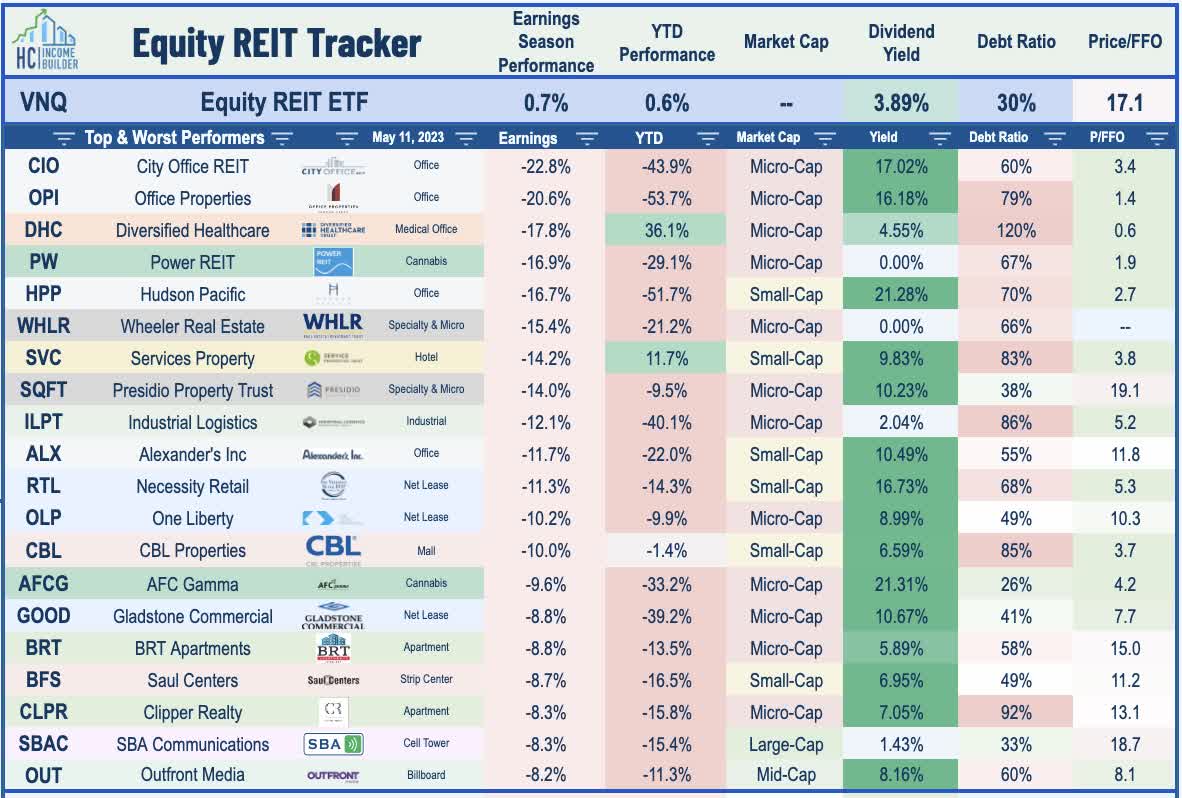

'Flight to quality' was a major theme this earnings season, with small and micro-cap REITs significantly lagging larger-cap names. Thirteen equity REITs declined by more than 10% since the start of earnings season in mid-April and among the 20 worst performers, only one - cell tower REIT SBA Communications ( SBAC ) - has a market capitalization above $10B. Also of note, the 20 worst performers this earnings season have an average debt ratio of 60% - double that of the REIT sector average. Lagging on the downside is the suite of RMR-managed REITs following the controversial merger between Office Properties ( OPI ) and Diversified Healthcare ( DHC ), which has sent shares of both companies sharply lower, while its other two REITs - Service Properties ( SVC ) and Industrial Logistics ( ILPT ) - are also among the worst performers. Other laggards include office REITs City Office ( CIO ) and Hudson Pacific ( HPP ) - which each slashed their dividend by 50%.

{kind=link}

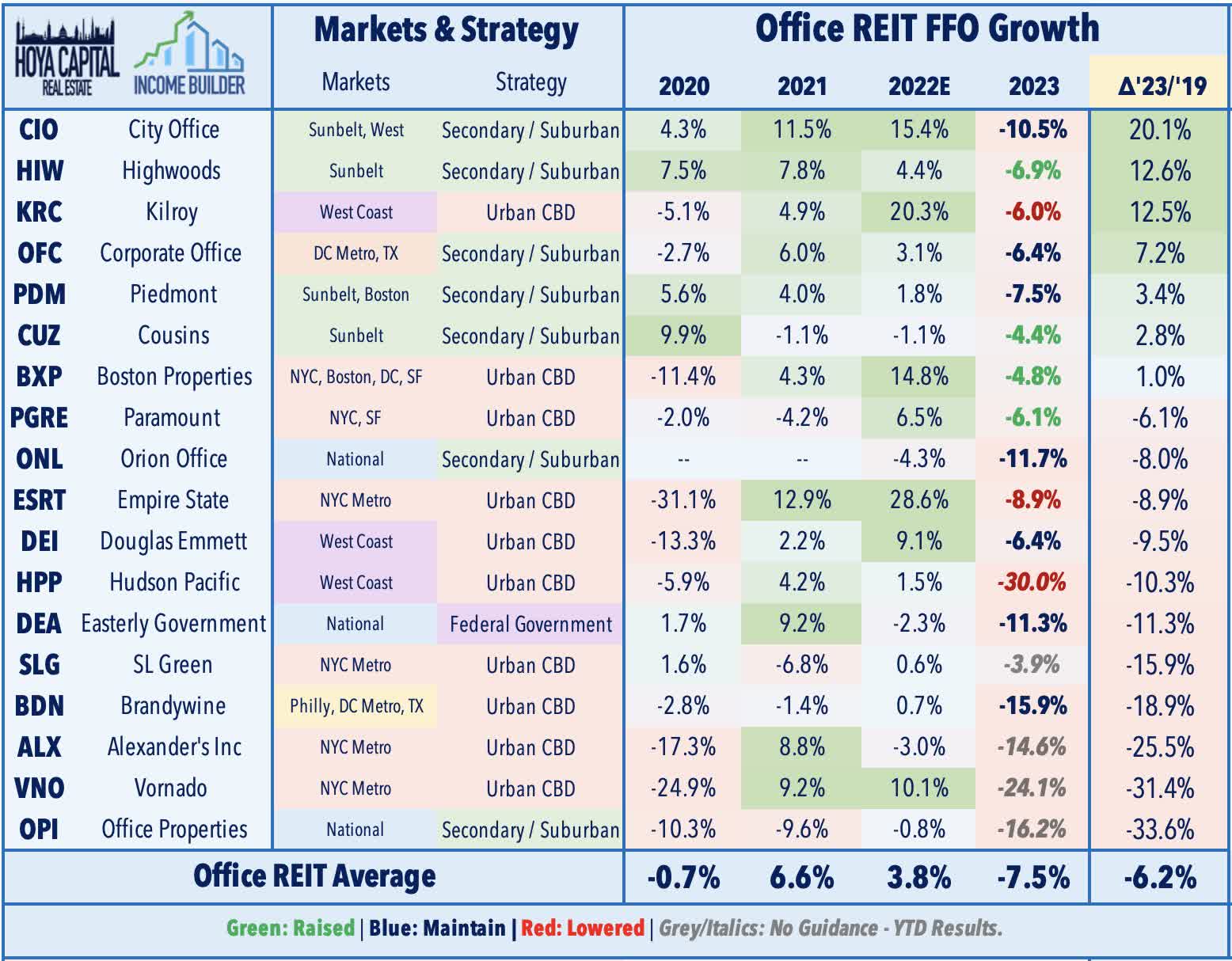

Loser #1: Office REITs

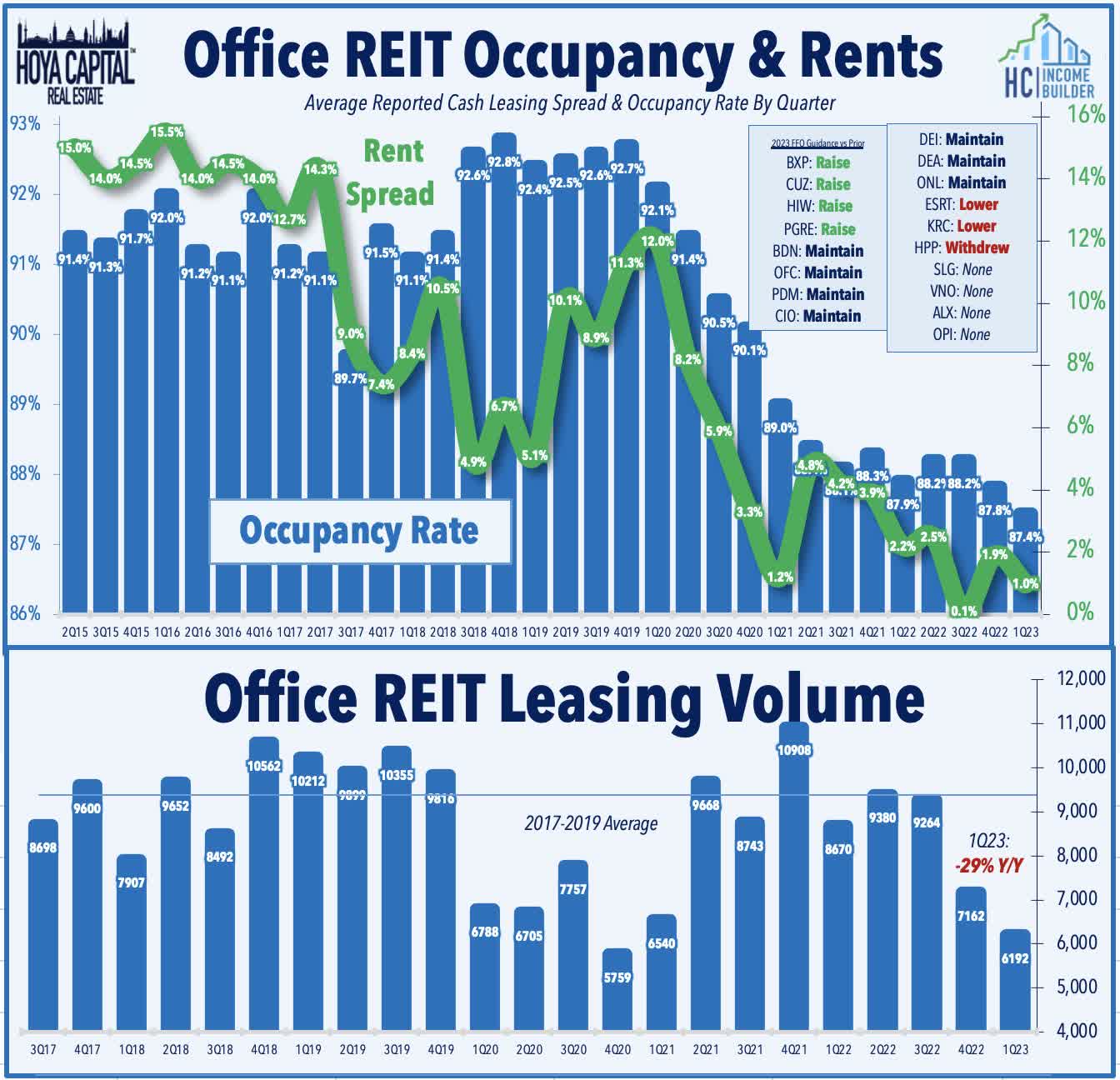

Office : (Final Grade: C) The most "unloved" property sector, office REIT earnings results did little to materially alter the negative narrative. Sunbelt-focused REITs were once again the clear source of relative strength within the sector as the magnitude of the weakness in Sunbelt markets remains far more muted than coastal urban markets, underscored by the guidance increases from the pair of leading Sunbelt office REITs - Cousins ( CUZ ) and Highwoods ( HIW ) - which reported leasing volumes that were only about 20% below pre-pandemic levels. Two coastal-focused REITs raised their full-year FFO outlook: Paramount Group ( PGRE ) and Boston Properties ( BXP ). Vornado ( VNO ) has been in the spotlight after announcing that it will suspend its common stock dividends until the end of 2023 - one of four office REITs to reduce its dividend this earnings season. Two REITs reduced their FFO outlook - NYC-focused Empire State Realty ( ESRT ) and West Coast-focused Kilroy ( KRC ). Overall office leasing activity was lower by 29% from a year earlier and 38% below pre-pandemic 2019-levels while occupancy rates are now about 5 percentage points below their pre-pandemic highs.

{kind=link}

The weakness was particularly acute on the West Coast - and notably in the San Francisco market - a focus of office REIT Hudson Pacific . HPP noted that it signed 344k SF of space in Q1 - down about 30% from a year earlier - at rental rates that were 4.9% below prior rates. HPP - which owns a portfolio consisting primarily of traditional office properties in San Francisco and Los Angeles, markets that were among the strongest before the pandemic driven by robust tech hiring - withdrew its full-year outlook, citing the impact of the Hollywood writer's strike, which impacts its studio segment, which represents about 10% of its portfolio. Data from Kastle Systems - which tracks office utilization rates - shows that San Francisco remains the hardest-hit market by the pandemic-driven WFH era. At the same time, many Sunbelt and secondary markets are seeing mid-week utilization rates at around 75% of pre-pandemic levels, San Francisco has yet to crack 50%.

{kind=link}

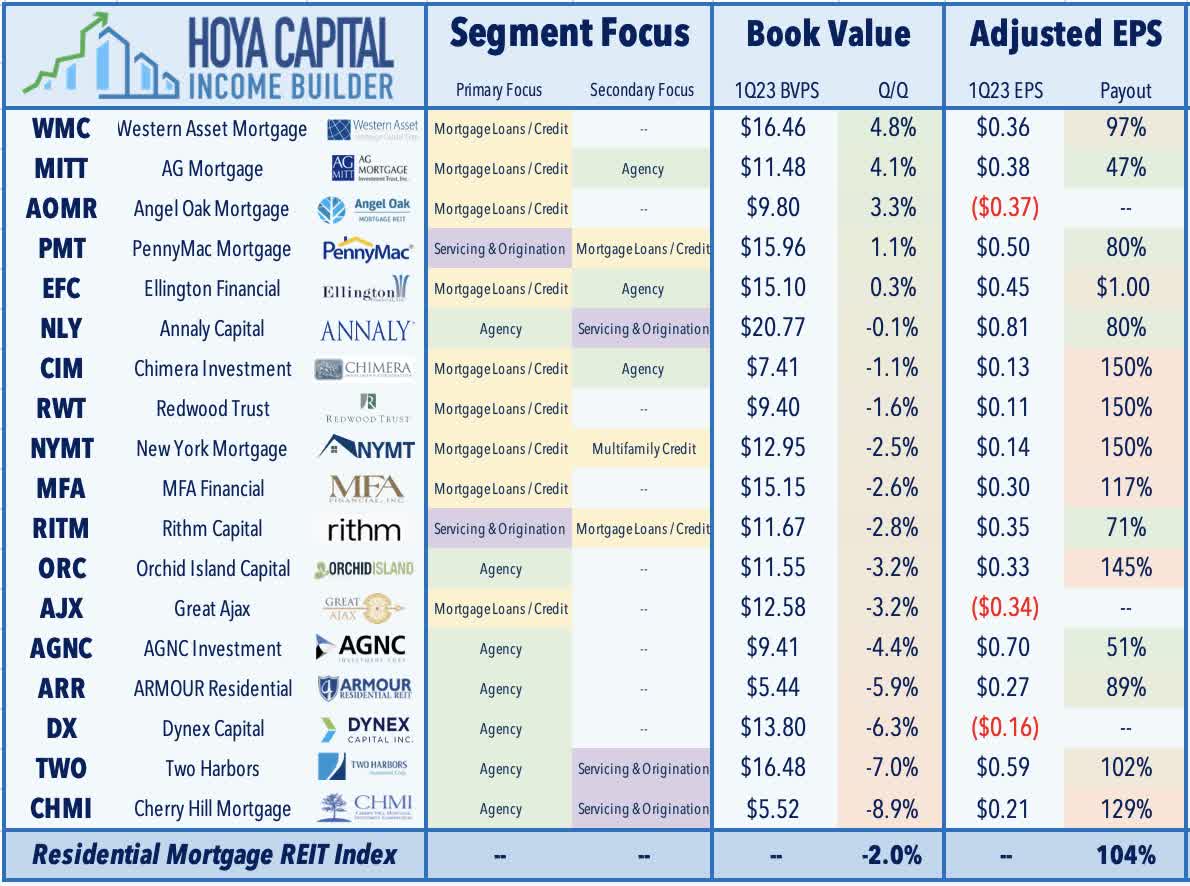

Loser #2: Mortgage REITs

Residential mREITs : (Final Grade: B-) As expected, results have been hit-and-miss given the volatile interest rate environment in Q1 combined with these REITs' typically high leverage and uncertain hedge exposure. Credit-focused mREITs fared better in Q1 - reporting a slight increase in their Book Value Per Share ("BVPS") - led by PennyMac ( PMT ) along with a trio of small-cap mREITs - Angel Oak ( AOMR ), Western Asset ( WMC ), and AG Mortgage ( MITT ). Agency-focused REITs, however, reported an average decline in their BVPS of about 5% in Q1, with Two Harbors ( TWO ) and Cherry Hill ( CHMI ) reporting the steepest declines. Only about half of the residential mREITs reported distributable EPS that covered their Q1 dividend, leading to dividend reductions from Redwood Trust ( RWT ), Great Ajax ( AJX ), and Cherry Hill ( CHMI ). Other REITs that were over 100% payout were more confident in their ability to maintain their dividends. Dynex Capital ( DX ) reiterated that hedge gains "will be supportive of the dividends in 2023" while Orchid Island ( ORC ) commented, "We’re going to keep the dividend where it is."

{kind=link}

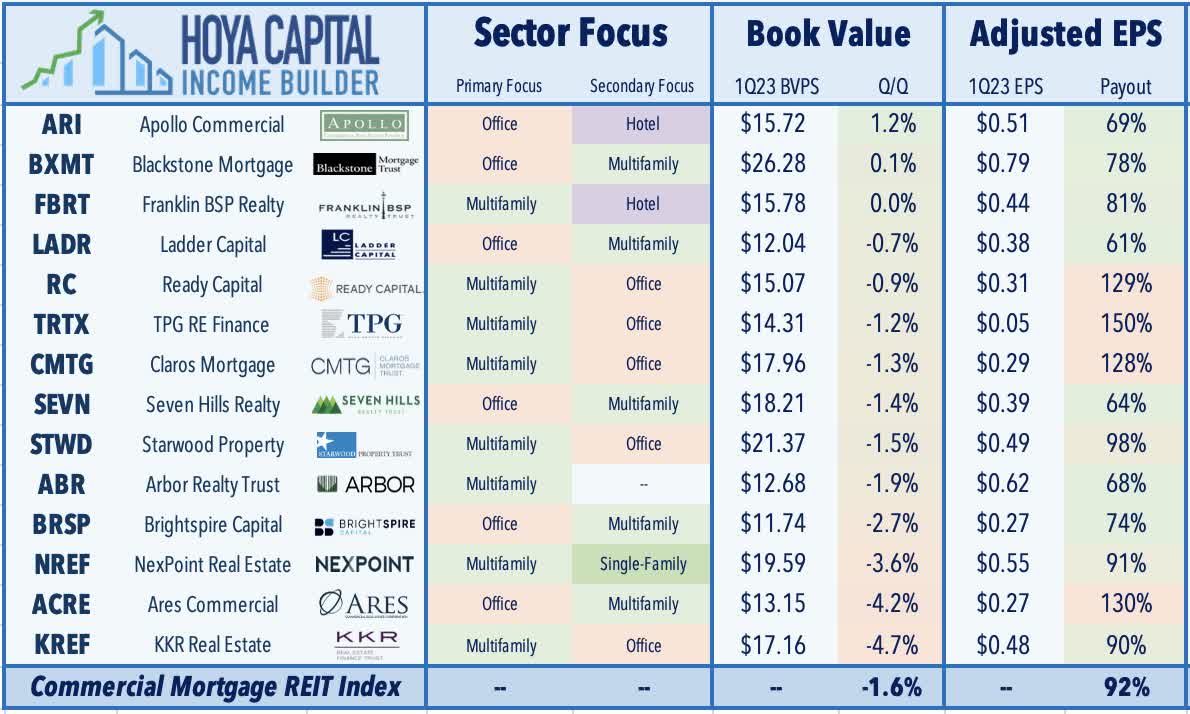

Commercial mREITs : (Final Grade: B-) Arbor Realty ( ABR ) has been the leader this earnings season after reporting strong results and raising its dividend by 5%, the fourth mortgage REIT to raise its dividend this year. Results from a handful of office-focused lenders showed that the grave concern over a wave of office loan defaults might be a bit premature. Blackstone Mortgage ( BXMT ) has been among the better-performers after reporting adjusted EPS of $0.79/share - covering its $0.62/share dividend - and noting that it collected 100% of interest payments in Q1 with no defaults despite its office-heavy loan portfolio. Apollo Real Estate ( ARI ) has also been an upside standout after reporting adjusted EPS of $0.51 - easily covering its $0.35/share dividend - while noting that BVPS increased 5% in Q1 to $15.72. Other office-focused mREITs have seen some cracks in their loan portfolio, however, and have suffered steep declines as a result. TPG Real Estate ( TRTX ) dipped over 20% after it reported adjusted EPS of $0.05 - short of its $0.24 dividend - and noted that six loans with a total balance of $550M are now in nonaccrual status, up from two loans totaling $190M last quarter.

{kind=link}

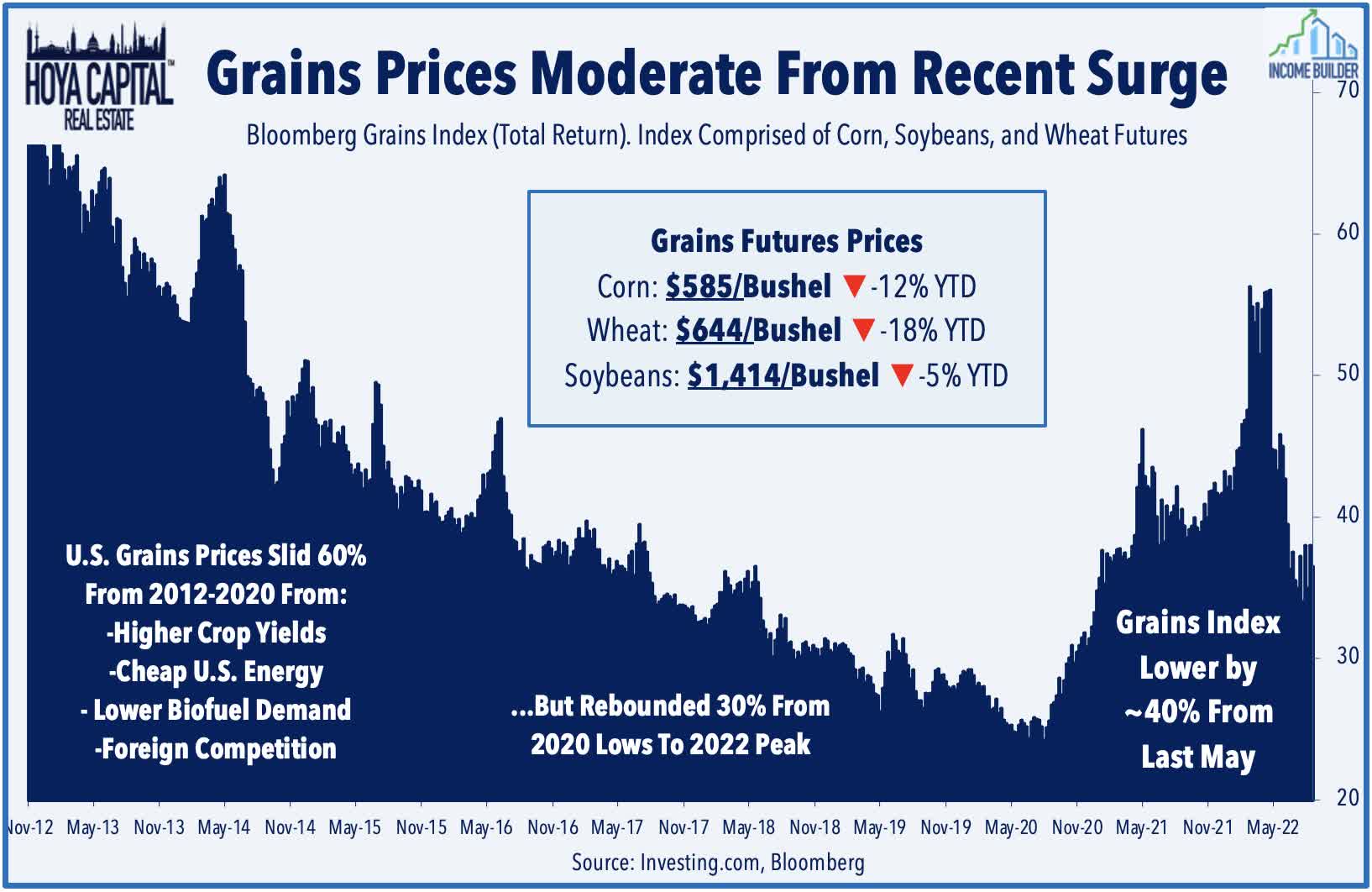

Loser #3: Land & Agriculture REITs

Farmland : (Final Grade: C+) One of the hottest inflation-hedges, farmland REITs have been slammed over the past six months amid a substantial pull-back in commodities prices from their peaks last May. The Bloomberg Grains Index is now lower by about 40% from last year and is now slightly below the average from 2015-2020. Farmland Partners ( FPI ) reported mixed results, noting that it still expects its FFO to decline 30% this year driven by a "triple-whammy" of headwinds: lower crop yield due to drought conditions, low crop price due to normalization effects after a sharp spike early in the Ukraine-Russia war (with particularly sharp price declines on specialty crops), and significantly higher interest rate expense due to FPI's elevated level of variable rate debt exposure. Gladstone Land ( LAND ) reported soft results, noting that its tenant rent collection issues have persisted amid headwinds from lower crop prices and the impacts of flooding in California. LAND reported rent collection issues from 3 of its 90 tenants - one of which was evicted - while the other two are late in their rent payments.

{kind=link}

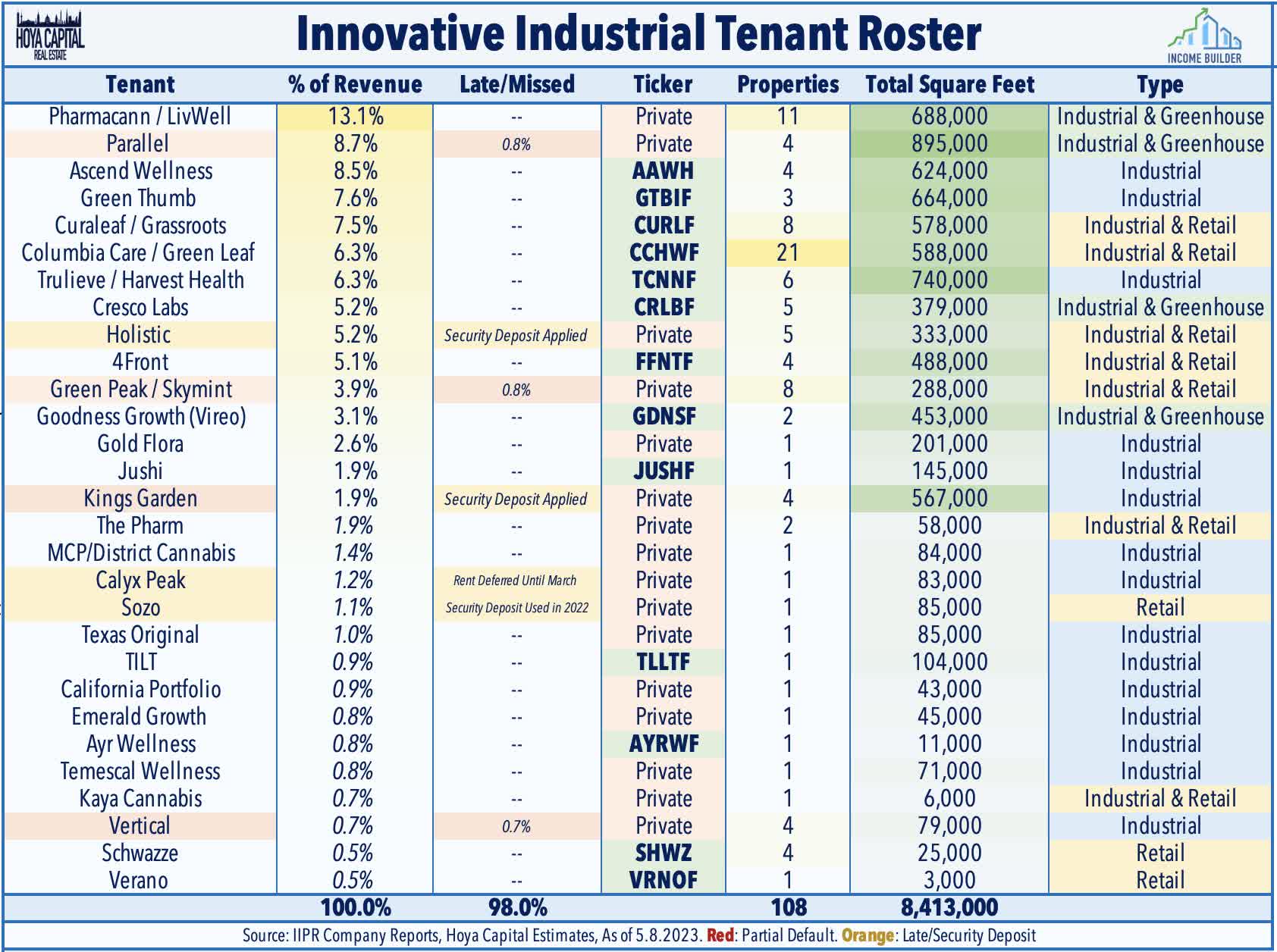

Cannabis : (Final Grade: B) Tenant concerns have continued to pressure cannabis REITs this year as their cultivator operators have been smoked by plunging wholesale cannabis prices, tightening credit availability, and setbacks on federal legalization. Innovative Industrial ( IIPR ) reported solid results this week, noting that its rent collection rate improved to 98% in Q1 - up from 94% in Q4 - with no additional tenants named as non-payers. The improved collection rate in Q1 was driven primarily by applying security deposits on leases of Green Peak, Parallel, and Holistic and through the sale of its properties leased to Vertical. The remaining 2% of uncollected rents was comprised of approximately $1.1M from Parallel and Green Peak and $470k for rent prior to the sale of its Vertical properties. NewLake Capital ( NLCP ) reported rent collection of 90% in Q1, noting that Revolutionary Clinics (10% of its rental income) has not paid rent in 2023, citing "two unfortunate harvest related issues in 2022 and delays in opening adult use dispensaries." AFC Gamma ( AFCG ) reported that it has 1 borrower on nonaccrual, which represents 0.9% of its portfolio.

{kind=link}

Loser #4: Retail REITs

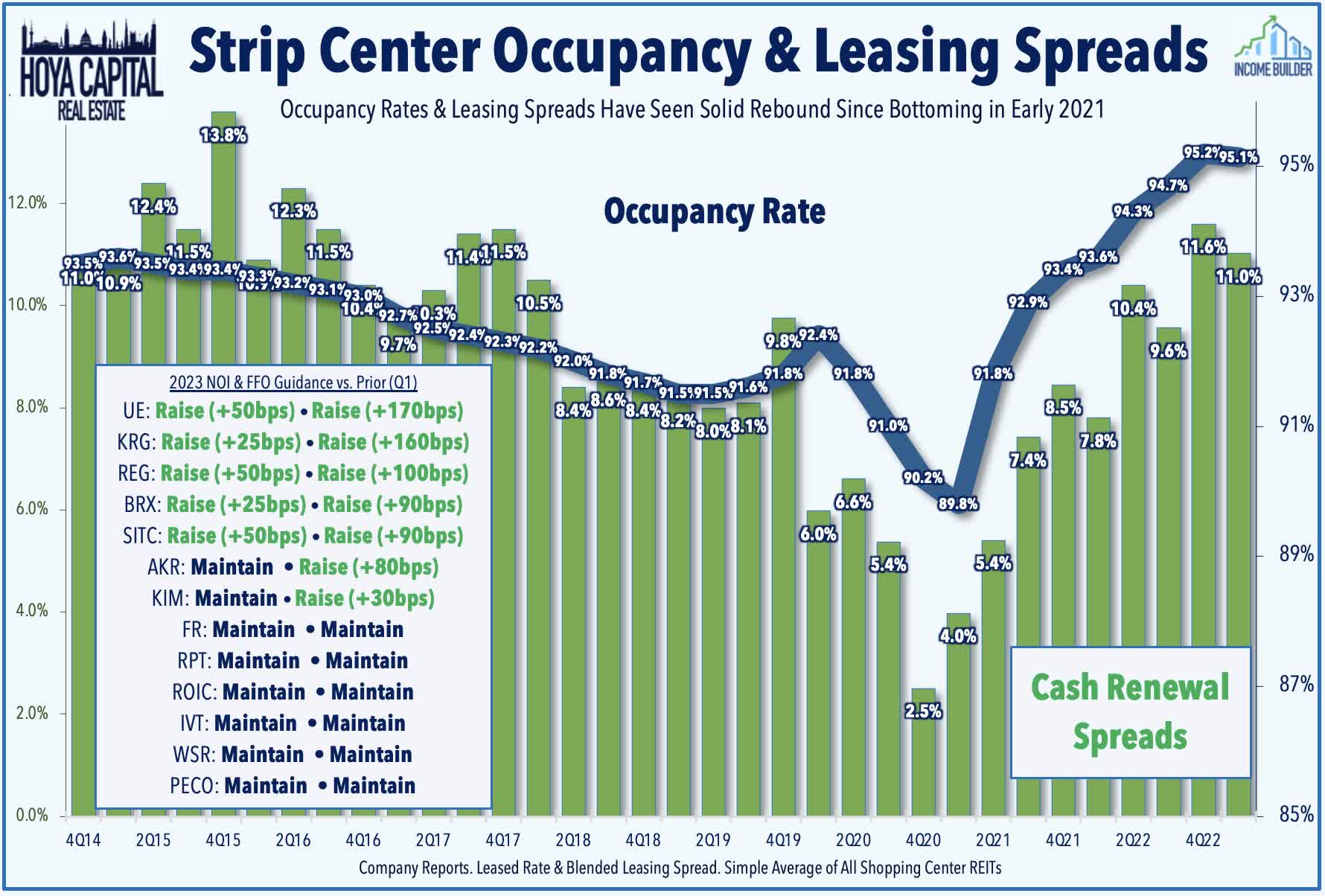

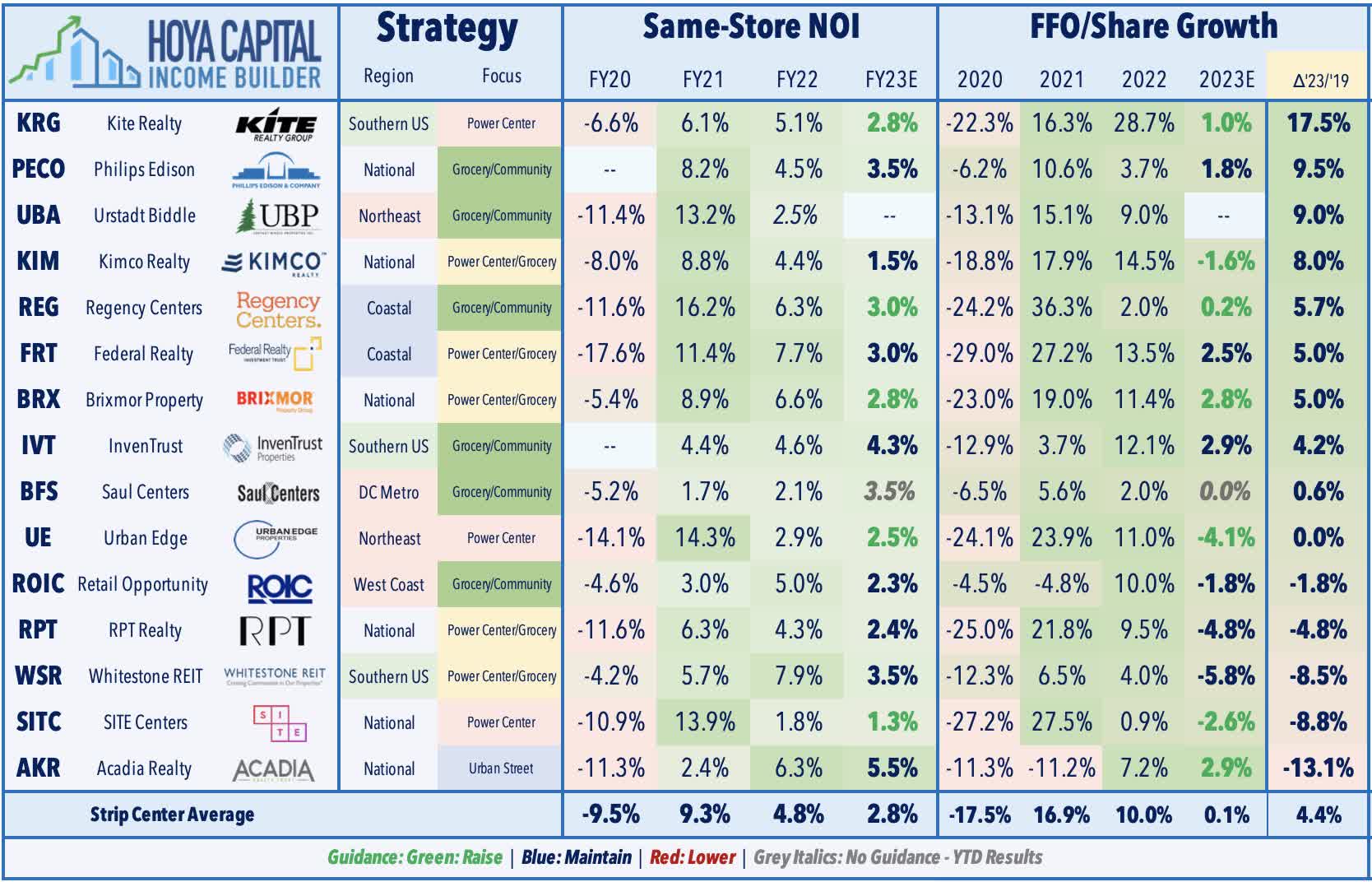

Strip Center : (Final Grade: B+) For retail REITs, the high-profile bankruptcy of Bed Bath & Beyond overshadowed an otherwise solid slate of reports showing buoyant rent growth. For strip center REITs, the solid slate of Q1 results continued the trend of better-than-expected reports stretching back to late 2021 as demand for "big box" space has significantly exceeded the available supply. Roughly half the strip center REIT sector raised their full-year outlook. Kite Realty ( KRG ) was the upside standout this earnings season, raising both its full-year FFO and NOI growth outlook. Leasing activity was impressive, with cash leasing spreads of 38.0% on 17 new leases, 10.0% on 77 renewals for a 13.0% blended increase. Brixmor ( BRX ) has also been an upside performers after it reported similarly strong "beat and raise" results, with rent spreads accelerating to 19.2% - its strongest in a half-decade. BRX raised its NOI growth target to 2.75% at the midpoint - up 25 basis points from last quarter - and now sees FFO growth of 2.8% - up 90 basis points from last quarter. Regency Centers ( REG ) and Kimco ( KIM ) also raised their full-year FFO outlooks. Recent retail bankruptcies haven't fazed these REITs, who generally expressed confidence in quickly filling any vacated space. SITE Centers ( SITC ) - which has the highest exposure to Bed Bath & Beyond ( BBBY ) among these REITs - commented, "we are confident that there are single-user backfill options given the amount of inbound activity we’ve seen.

{kind=link}

{kind=link}

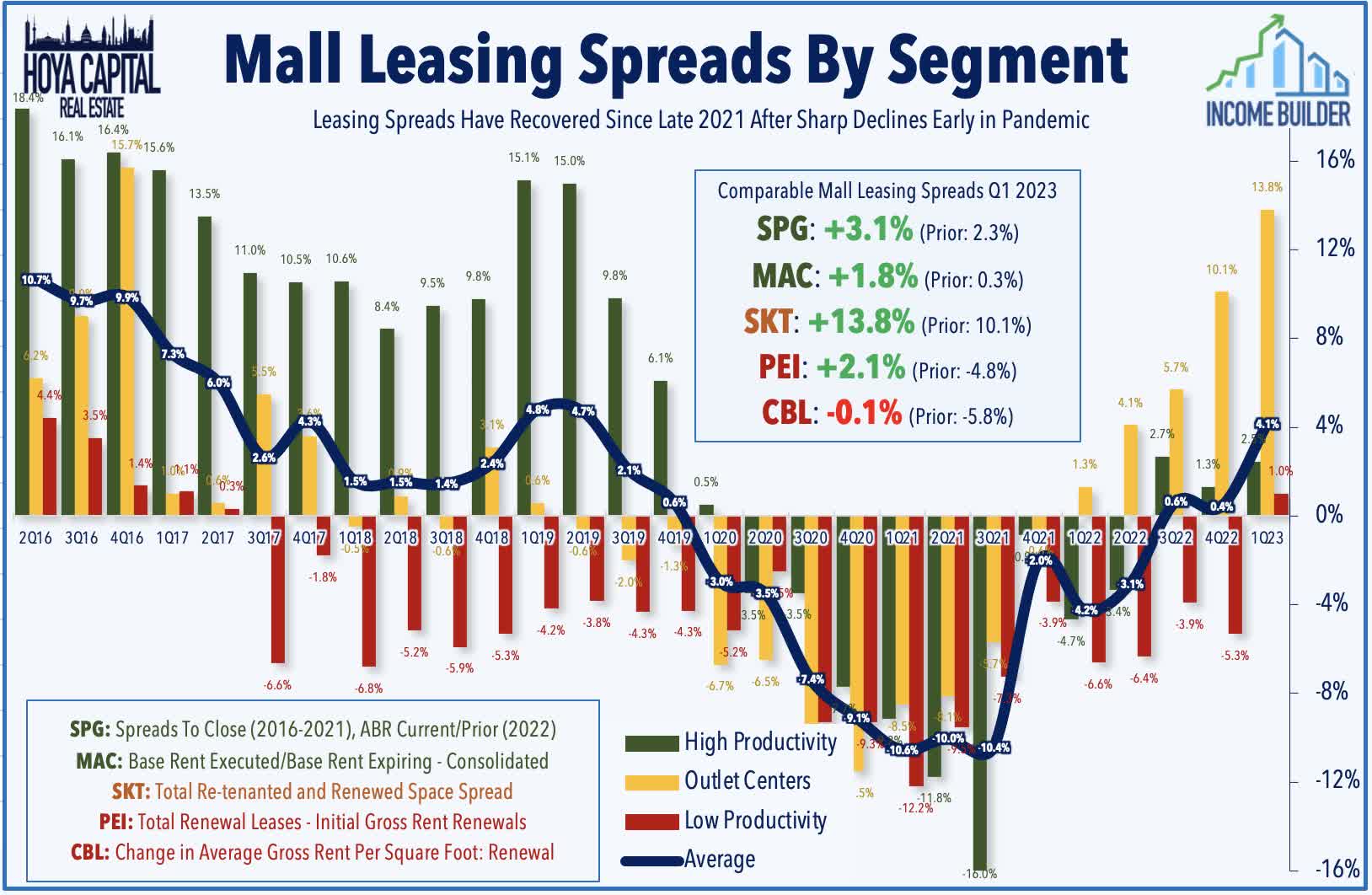

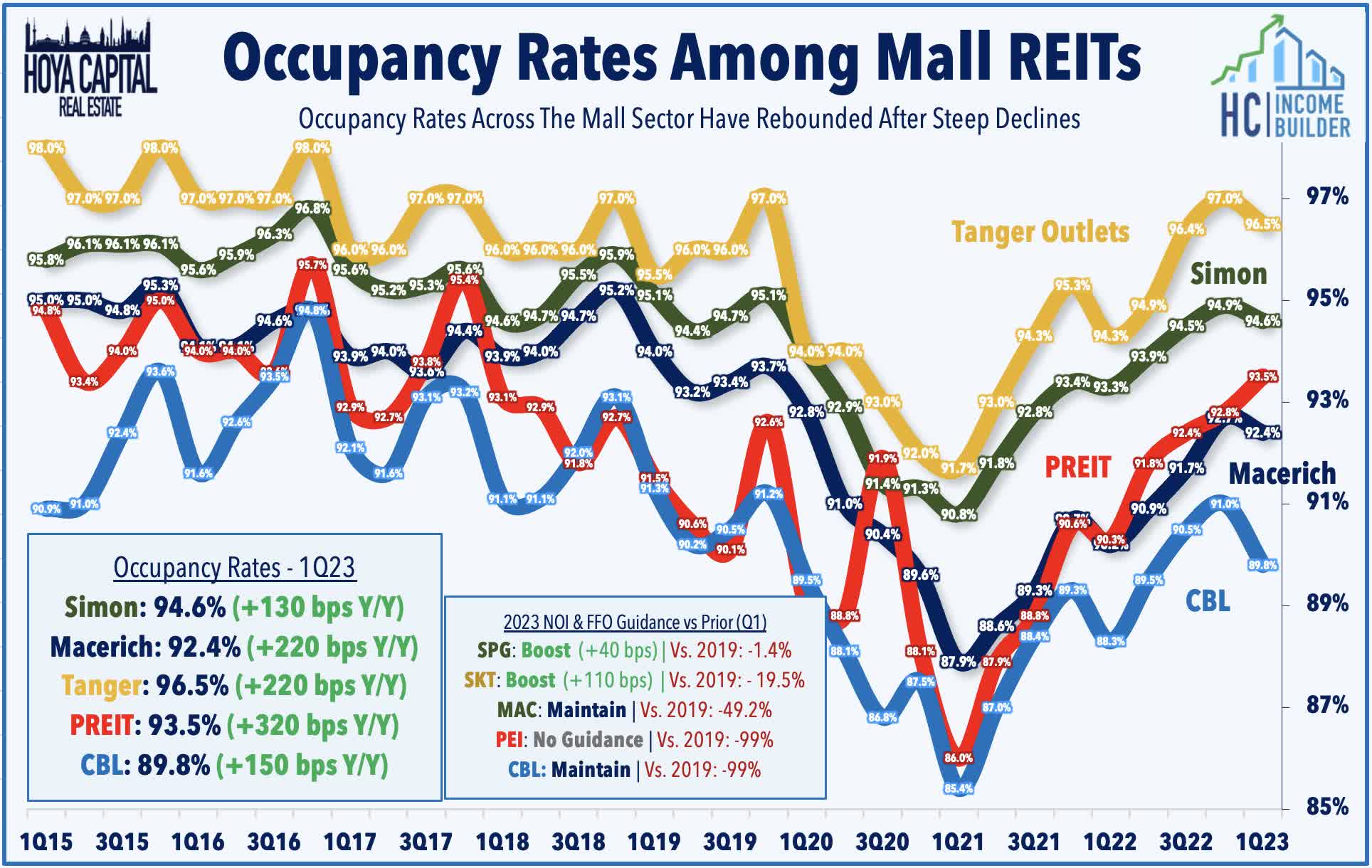

Malls : (Final Grade: B+) While not displaying the outright strength seen in the strip center format, mall fundamentals have stabilized in recent quarters for properties in the upper-end of the quality tiers. Simon Property ( SPG ) raised its dividend while also boosting its full-year outlook. Questions over SPG's plans to spend $1.5B on mixed-use redevelopment and expense headwinds offset strong leasing results. SPG now expects its FFO to be flat with last year - an upward revision of about 40 basis points from last quarter - which would bring its FFO to within 2% of full-year 2019. Tanger Factory Outlet ( SKT ) also raised its full-year guidance. Encouragingly, SKT reported that blended rent spreads rose 13.8% on a trailing-twelve-month basis in Q1, which was the eighth-straight quarter of positive spreads following a period of eight-straight negative quarters, consistent with the recent buoyance in rental rates observed across the retail real estate space. SKT commented, "we are seeing robust leasing activity with accelerating double-digit rent spreads as our retailers demonstrate their commitment to the outlet channel and Tanger's open-air portfolio." Macerich ( MAC ) maintained its full-year outlook - which calls for an 8.2% decline in FFO due to higher interest expense - but reported a continued stabilization in rental rates and occupancy rates.

{kind=link}

{kind=link}

Loser #5: Non-Traded REITs

If headwinds are stiff for some of the more highly-levered public REITs - most of which have Debt Ratios in the 40%-range, it's certainly not a stretch to assume that conditions are quite a bit bleaker for the less-transparent private real estate platforms, including Blackstone's ( BX ) Real Estate Income Trust ("BREIT"), which boasts a "target leverage ratio in the range of 60%." Last week, Blackstone announced that its fund again hit its monthly redemption limit, fulfilling just a third of the funds that were requested by investors. April marked the sixth straight month that the firm's flagship fund limited redemptions. BREIT noted that if an investor requested their money back beginning in November - and did so in every month since then - they have received 84% of their money back - which BREIT claims as evidence that "the semi-liquid structure is working as intended." As noted in our Casino REIT report last week, analysts have questioned BREIT's self-reported NAV, and investors have seized on the opportunity to redeem shares at these premium NAV valuations and redeploy into cheaper publicly-traded REITs.

{kind=link}

Peakstone Realty Trust ( PKST ) - formerly known as the non-traded REIT Griffin Realty Trust - has been a laggard in its first earnings season a public company following its direct listing last month, a process that was marred by uncertainty over its share count resulting from a reverse stock split and preferred share redemption concurrent with its listing. PKST traded below $20 in its first week after the listing, but climbed to as high as $43/share in mid-April before retreating back below $20 this week. Peakstone is a net lease office and industrial REIT that owns 78 properties across 24 states. Roughly 70% of PKST's NOI is derived from its portfolio of 55 office properties, while 30% of NOI comes from its portfolio of 23 industrial properties. PKST reported that its FFO was $0.37/share - $1.48 annualized - which implies a Price-to-FFO of roughly 13x based on its $20 current share price. Before its direct listing, PKST reported that its Net Asset Value was roughly $65/share after adjusting for its 1-for-9 split, underscoring the huge gulf between public market pricing and self-reported NAV valuations by non-traded REITs.

{kind=link}

Recap: Strong First Quarter, With Exceptions

With the notable exception of office REITs - and specifically, the office REITs focused on primary coastal markets - REITs delivered surprisingly strong first-quarter results. As we've covered extensively in our State of the REIT Nation reports, most REITs have been preparing for this exact kind of dislocated macro environment, perhaps to the frustration of some investors that turned to higher-leveraged and riskier alternatives in recent years across private markets - including the non-traded REIT platforms discussed above. Considering the pain being felt by some of the more highly-levered public REITs, it's not hard to imagine the looming crisis facing many private market players that lack access to cheap, long-term fixed-rate unsecured debt. External growth for public REITs remains challenged for now, but REITs that played it safe during the "boom times" will likely have opportunities as reality sets in for many over-levered private-market property owners.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Losers Of REIT Earnings Season