LOVE - Lovesac: Long-Term Execution Is Key

Summary

- Distribution increases and product innovation should power results.

- Lovesac stock doesn't look expensive given its growth profile.

- FY24 could be a challenge, but long term looks solid.

While FY24 could be challenging against a difficult macro backdrop, Lovesac ( LOVE ) looks poised to benefit from continued increases in distribution touchpoints as well as product innovation. Given its growth potential, the stock looks attractively priced for long-term holders.

Company Profile

LOVE is a maker of modular couches and beanbag chairs. Its original product was an oversized beanbag chair it called the Lovesac. The Sac, as the company refers to it now, has removable covers that are machine washable and come in several sizes.

The company’s main product today, however, is its modular line of couches called Sactionals. The main selling point of the Sactional is that it comes with only two standardized pieces – seats and sides – that can be configured in a multitude of ways. Meanwhile, each piece comes with a removable cover that can be washed. The pitch is that because the couch can be configured in many different ways that it can grow with you as your needs, living space, and family situation evolve. The removable covers also mean that you can eventually change them out to get a brand new look.

Sactionals also come with a variety of accessories such as storage seats, ottomans, drink holders, and even a power hub to charge your smartphones wirelessly. Its StealthTech Sound+ add on, meanwhile, allows customers to have surround sound built right into their Sactionals.

Nearly 90% of LOVE’s sales come from Sactionals.

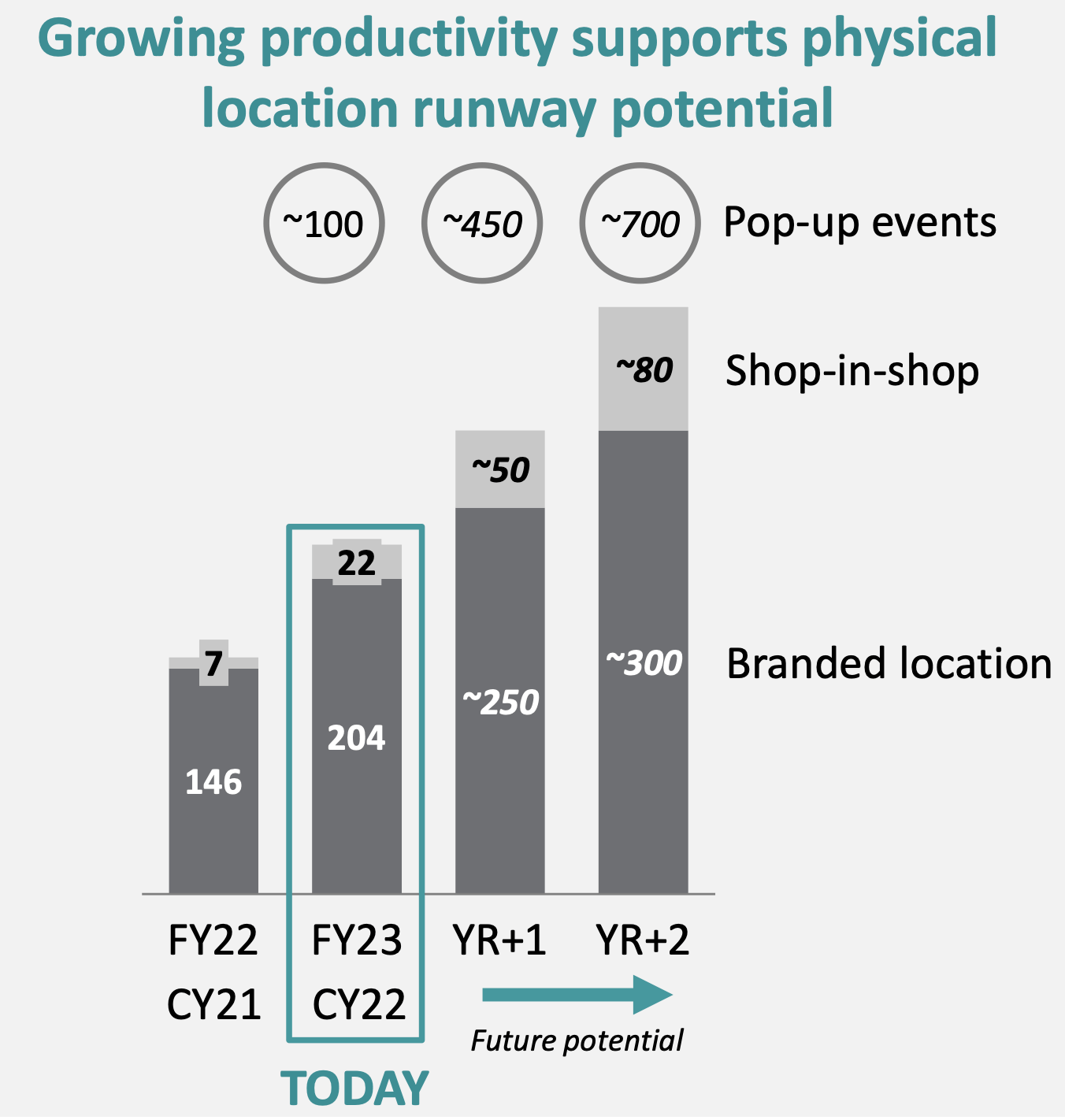

The company sells its products through its e-commerce website, small showrooms, and shop-in-shops at other retailers. The company has nearly 150 showrooms. Showrooms are small, typically between 800-1,000 square feet. Meanwhile, it has shop-in-shops in Best Buy ( BBY ) and pop-up stores at Costco ( COST ).

LOVE ships sactionals to customers unassembled, who then must put them together and add the covers. According to the company, its typical customer is 24-45 years old with household income of over $100K. Sactionals are not cheap, and the average first year value of a customer in fiscal 2022 was $2,840.

Opportunities

Increased distribution is one of the biggest opportunities for LOVE. The company has done a nice job moving away from primarily being an e-commerce company to building showrooms across the country and getting into other retailers such as BBY and COST. Adding more showrooms, BBY locations, and COST pop-ups will only help expand brand awareness and increase sales. LOVE could also eventually look to get into other retail touchpoints such as a Target ( TGT ) or Kohl’s ( KSS ).

{kind=link}

Product innovation is another area of opportunity. StealthTech, which was introduced in 2021, is the best example of this. It’s a $3,000 upgrade, and one that past buyers are able to upgrade to later. The company projects that StealthTech could be a $100 million opportunity. Wireless charging stations are another example.

The company is looking to make about 8 new product introduction over the next 2-3 years. LOVE says that about 42% of its transactions come from repeat buyers, so product introductions can not only drive new customers, but also draw people into making upgrades to their existing sactionals.

While the company has been reluctant to add it, and COVID certainly made it less desirable, I think a white-glove delivery and set-up service could be a growth driver. Sactionals are expensive and many people don’t want to spend $10,000 or more on a couch that they then have to assemble themselves. The company claims it sells to the RH ( RH ) crowd who will put a $20,000 Sactional in their finished basement, but I’m sure offering an assembly service would drive sales among higher-income consumers even more.

Risks

As noted before, Sactionals aren’t cheap, in fact the price can balloon pretty quickly when adding more sections and upgrading fabric for the covers, not to mention the cool tech features. Thus, a weaker economy can certainly put a damper on sales.

While LOVE has grown tremendously, there could also be some pull-forward of sales from the pandemic. When everyone was couped up in their homes, spending often went more towards household items, like furniture. Most polls now indicate that people are more apt to spend their discretionary income on things like vacations or other experiences like concerts. As inflation curbs spending power, expensive household furnishings are generally not at the top of the list of where people choose to spend their money.

{kind=link}

At the same time, I think the lack of a white-glove delivery service can keep some people from considering buying the product. I know from personal experience I looked at the couches and liked them, but the idea of assembling it and adding the covers put me off. From what I’ve read in reviews, assembly can be a time-consuming process, especially when trying to get the covers to fit perfectly. I’m not the handiest of people, so at least for me, this kept me from buying one.

In addition, many copycat companies have also popped up, selling similar looking modular couches, generally at cheaper prices. There also has been an uptick in promotions from competing firms, which was a big topic on LOVE's Q3 earnings call.

On the Q3 call, COO Mary Fox said:

“So obviously, as everybody has reported, there has been an uptick in promotions. But obviously, that was up against last year where it was incredibly benign. And even for this year, it is very benign to pre-pandemic levels, so we feel good in terms of what we have seen. And as we have been testing with the teams, [agility], sometimes our customers are responding as much to financing as they are to depths of promotion.”

It's also notable that when the company filed its last 10-K it did identify a material weakness in is internal controls over financial reporting. The company did not find any material misstatements and thinks the issue has been fixed, but it is worth watching.

Insider Buying

One positive that LOVE has seen is that insiders have stopped selling shares and reversed course to buy shares recently. In January Chairman Andrew Heyer picked up $847K worth of shares, according to form-4 filings. He was previously a seller of the stock in 2020-21.

Chief Strategy Officer Albert Krause, meanwhile, bought $192K in shares in December when the stock was trading under $20. Krause was a seller of shares in January 2022 and July 2021.

Valuation

LOVE currently trades around 9x the FY 2024 (ending January) consensus EBITDA of $65.4 million and 5.6x the FY25 consensus of $100.9 million. Add 7x rent expense to EV, and the stock trades at 10x and 6.5x, respectively.

It trades at a forward PE of 11x the FY24 consensus of $2.60.

The company is projected to grow revenue 11% in FY24 to $697.4 million, before accelerating to 15.5% in FY25.

While not a great comparison, as there really aren't any, RH trades at a forward PE of about 18.5x. LOVE doesn't have enough history as a profitable company to look at past valuations.

Conclusion

LOVE can be a volatile stock post-earnings, often making big moves. Meanwhile, the promotional environment intensified compared to last year during its most important quarter – Q4. The company did reiterate its Q4 guidance at ICR, but its FY2024 forecast will be key.

{kind=link}

While FY2024 may not be the easiest year, I think the planned distribution touchpoint increases, combined with an expanding product roadmap, bode well for the company over the long term. I've had my doubt about the company when it IPO'd, but it's done a really nice job of growing and turning profitable. The stock, meanwhile, trades below pre-pandemic levels.

LOVE certainly is a higher-risk stock, but I think if its continues to execute that it could be a $70 stock in a couple of years, which would be about a 15x multiple on its FY25 EPS estimates.

For further details see:

Lovesac: Long-Term Execution Is Key