LOVE - Lovesac: My #1 Pick For 2023

Summary

- Lovesac is my top pick for 2023.

- I see the stock as pricing in all but the worst and harshest recession scenarios.

- I believe the stock has massive upside potential in 2023 and beyond.

While 2022 has seen trillions of dollars wiped out from investors’ account balances globally, periods such as this create enormous opportunities if one knows where to look. Not all bear markets are created equal, and this one has hammered growth and tech names that were previously reliant upon low interest rates for their valuations.

It is my belief the market has priced in higher rates, and that the focus now is on a potential recession in 2023. That’s key because if I’m right about that, it can guide what stocks are most likely on sale today. With that in mind, allow me to present my pick for the top stock of 2023: The Lovesac Company ( LOVE ).

The last time I covered Lovesac, I said a recession was already priced in and that it was a buy. Of course, we’ve seen further selling since then, and I’ll own that. However, that hasn’t changed my belief that Lovesac is attractively priced; it is simply more attractively priced now than it was.

My pick hinges on several things that I think will converge to create the opportunity for enormous returns for buyers of the stock in 2023. Higher interest rates are priced in, a mild to moderate recession is priced in, demand remains strong, valuations are extremely low, money is rotating into the sector already, Lovesac has strong competitive advantages, and analysts have already built in weakness into 2023+ estimates, leaving room for upside surprises.

Let’s dig in.

Signs of a bottom

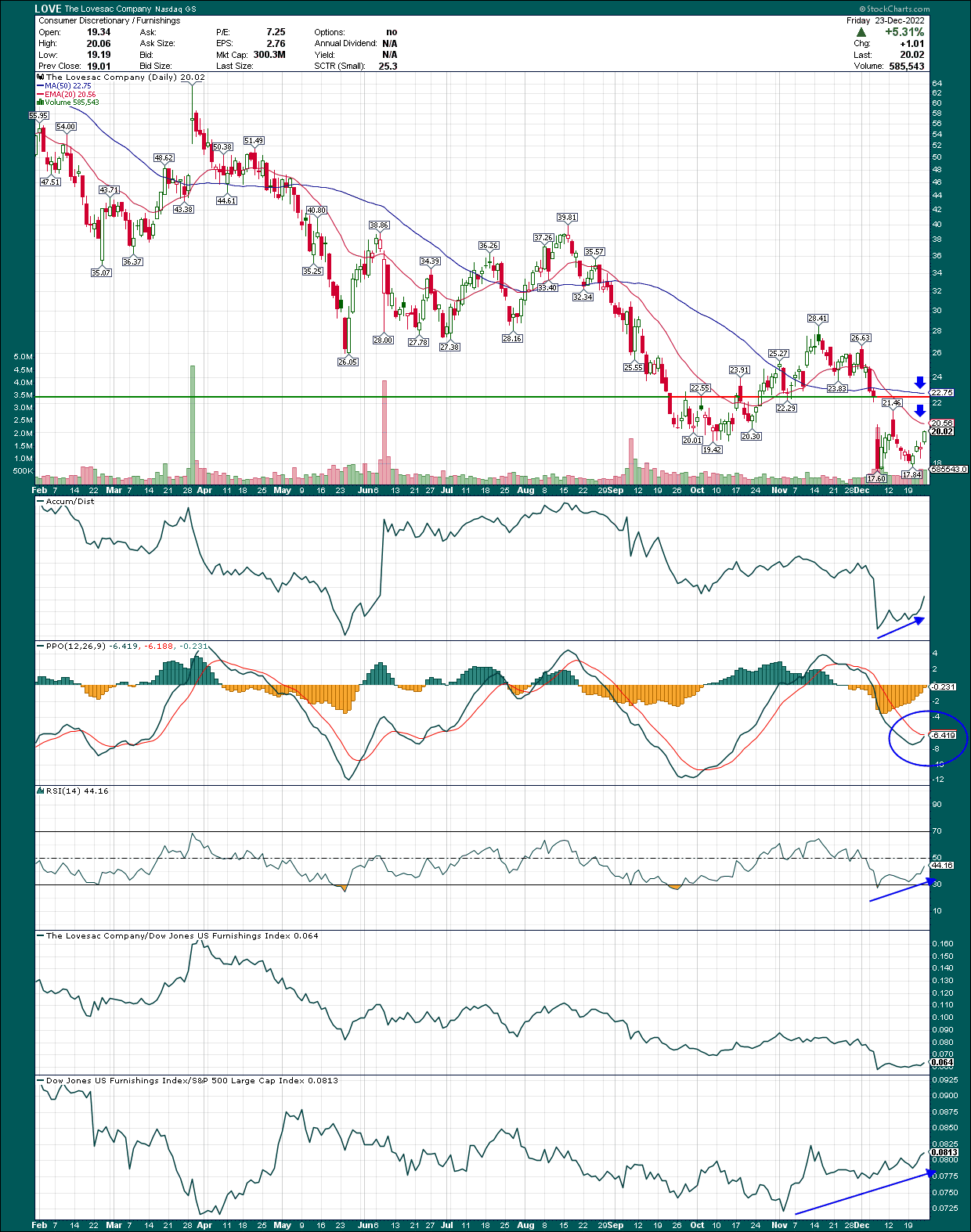

As anyone that is familiar with my work will know, I always rely upon technical analysis as a primary tool for investing/trading, and this situation is no different. I find Lovesac’s fundamental setup extremely compelling, but even more so given I very much like what I see in the charts. We’ll start with a daily chart to get a short/medium-term view of the stock.

{kind=link}

This stock has been in a nasty downtrend for the whole of 2022, with some bounces that were all short-lived. However, to my eye, there’s cause for optimism.

We’ll start with the very bottom panel, which shows the home furnishings category against the S&P 500. This measures if money is flowing into the category on a relative basis (bullish), or out of it (bearish). It’s quite clear that money is flowing into home furnishings since the beginning of November, with the category strongly and consistently outperforming the S&P 500. We want to buy great stocks in great categories, so that’s the first box checked.

If we turn our attention to the momentum indicators, the 14-day RSI and the PPO are showing signs of a bottom while price action is turning higher. Generally, when a stock is bottoming, you’ll see the momentum indicators make higher lows and turn up before price action does. This indicates selling momentum is waning, and that’s often a key sign the stock is in its last bearish throes. When the sellers dry up, that’s the best time to buy.

If we look at the price lows from May and November, we can see the PPO actually made its low at the same spot. That’s a positive divergence, meaning selling momentum was already waning. We see it again with the December low, as the PPO’s low was actually much higher despite a much lower low on the price chart. This is a sign of severely waning selling momentum, which is quite bullish and greatly increases the odds “the” bottom is in.

On the price chart, to balance this discussion out a bit, I’ve annotated a few levels of key resistance those of us that are bullish will need to contend with. There is gap resistance from the December earnings decline at just over $22, the 20-day exponential moving average at $20.56, and the 50-day simple moving average at $22.75. I fully expect all three of these levels to fall and for the stock to turn the moving averages higher in the weeks to come. However, it is unrealistic to expect the stock to simply blast through all of these levels, so expect pullbacks along the way.

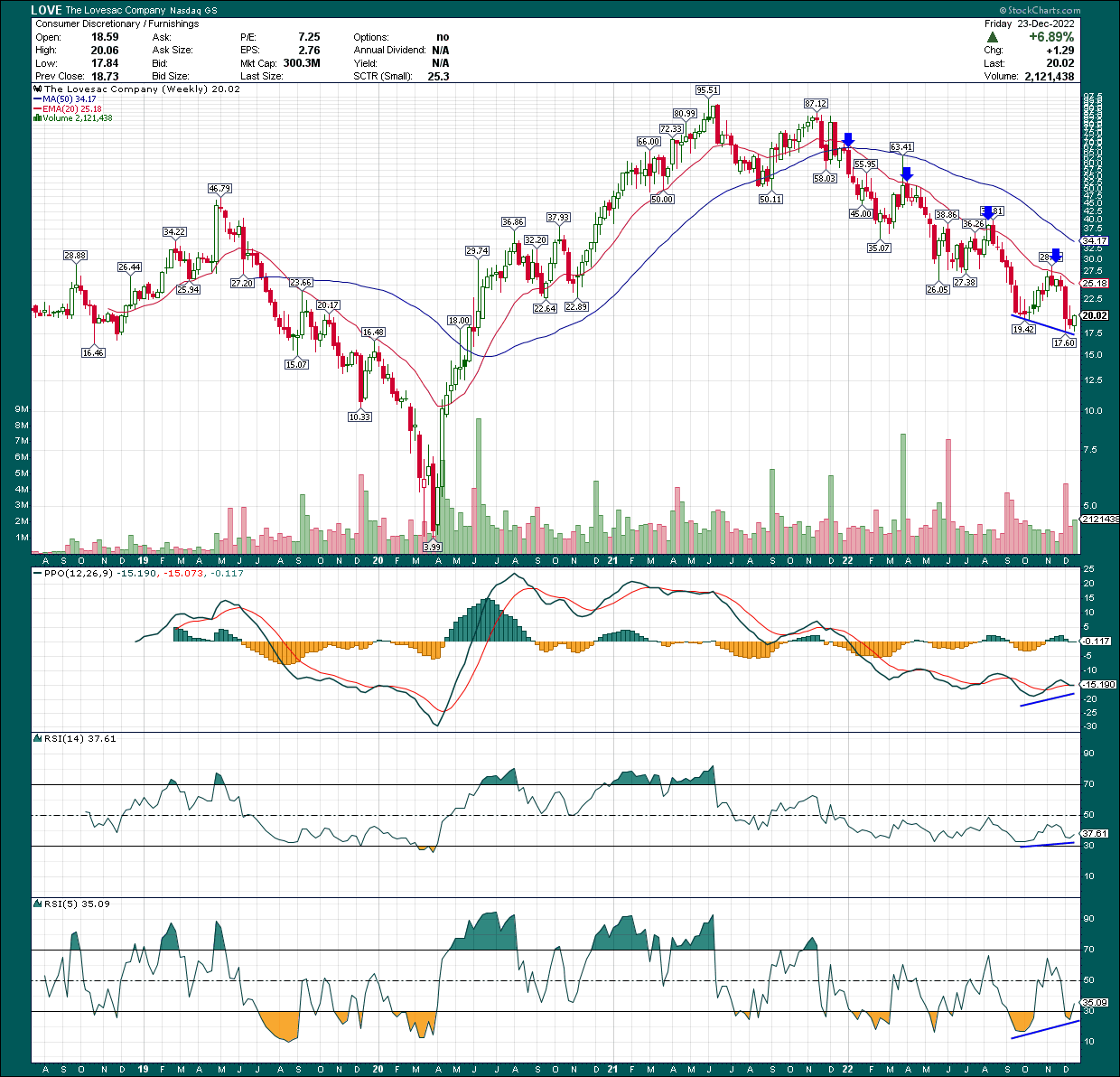

Let’s look at the weekly chart now to get a longer-term view.

{kind=link}

The momentum indicators show the same kinds of positive divergences, which I’ve annotated with the blue lines above. Apart from that, I’ve noted the 20-week exponential moving average has been a brick wall for the bulls since 2022 began, so that’s a further level to watch on the upside for signs of rejection. It current sits at just over $25, so that’s something to keep in mind.

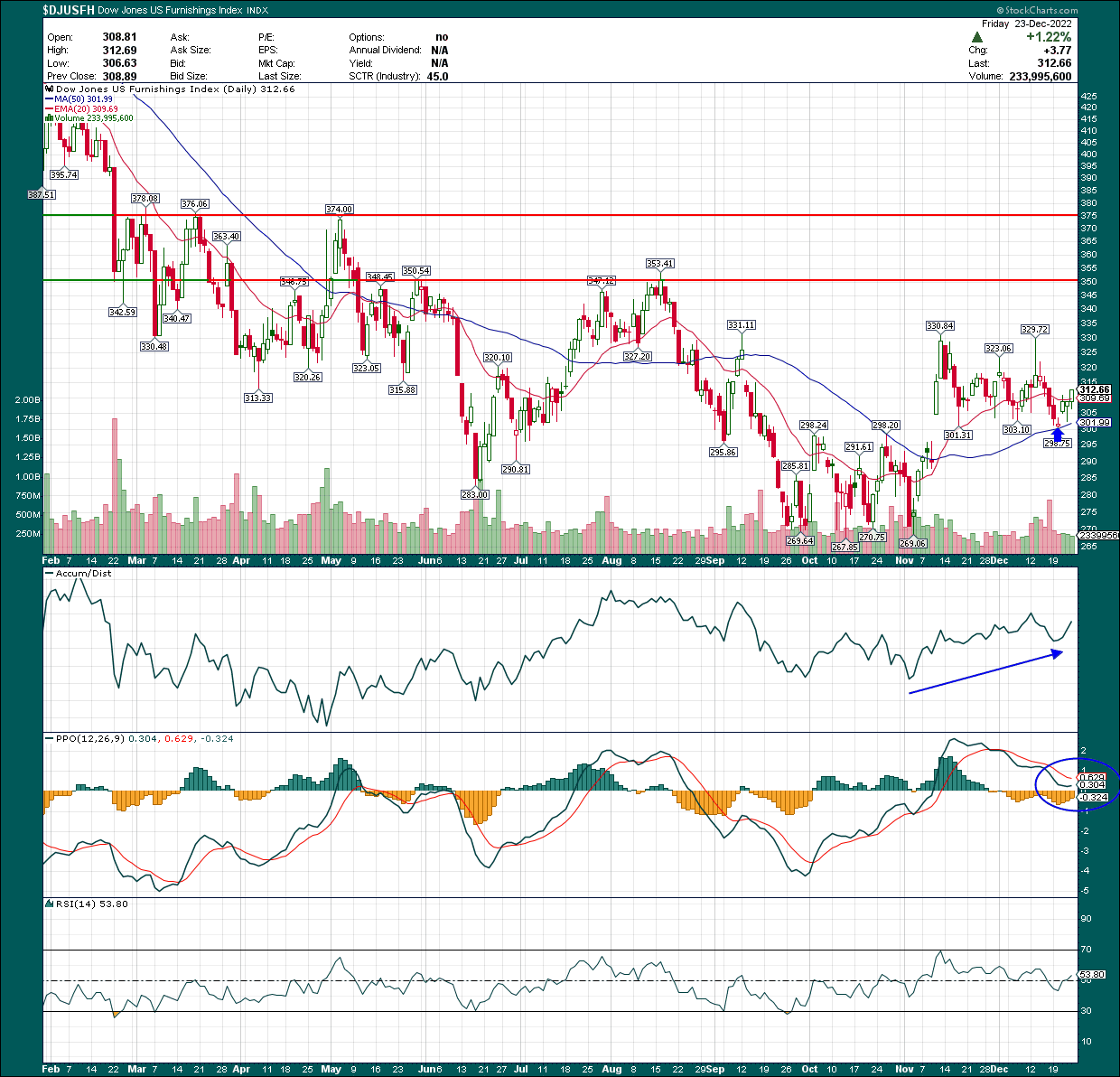

Finally, I mentioned that money is rotating into the category, which bodes well for stocks like Lovesac. Below is a chart of the home furnishings index on a daily time frame.

{kind=link}

This chart looks great in terms of bottoming, as we’ve got a clear bottoming formation in place from September to November, followed by a strong rally. The really good news is that the rally has held, and we can see the group bounced off the 50-day simple moving average in mid-December, annotated by the blue arrow.

Not only that, which is bullish in and of itself, but the accumulation/distribution line continues to rise. This indicates that on average, there are more buyers of the stock throughout the day than sellers. Essentially, that means investors are buying dips rather than selling rips.

Finally, the PPO moved well into overbought/bullish territory on the move from the November lows, and is now testing the centerline right after a 50-day simple moving average test. That’s a textbook pullback after a big rally, so I see no signs at the moment that this group is slowing down.

Now, if we’re heading into a recession, why is Wall Street buying home furnishings stocks? Aren’t they likely to see declining demand and pricing power in a recession? The answer to that question is obvious, but we have to remember that stocks are forward-looking mechanisms. Wall Street isn’t going to wait for the recession to end to buy stocks that will benefit from the recession ending. Institutions position themselves well ahead of whatever they think is going to happen, and it is my belief that Wall Street sees any potential recession as mild. Thus, it is buying more cyclical names because those are the ones with the most upside coming out of a downturn. There's literally no other reason why these stocks would be performing the way they are right now.

Following the money tells us that companies like Lovesac could have a huge 2023 as the recession either doesn’t happen, or comes in as short and mild. On this evidence, it certainly looks to me like Wall Street is positioned as such, and as a result, I want to be positioned that way as well.

Now, let’s take a look at why I chose Lovesac as my top pick and not one of its competitors.

Why is Lovesac different?

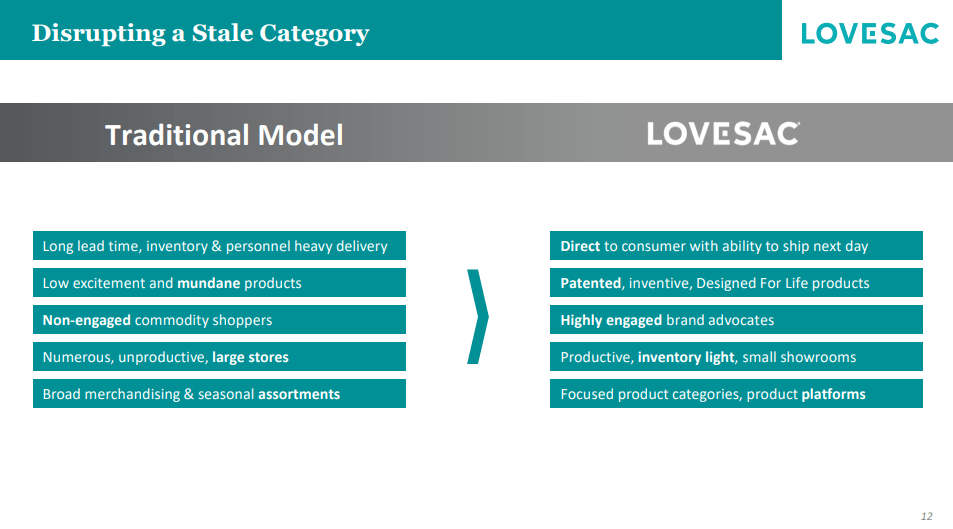

I like Lovesac for a variety of reasons, but its core product is the primary one, and what makes it stand out. The company was founded on the recognition that buying a couch or other furniture is an outdated, somewhat unpleasant, and time consuming process. Traditional furniture retailers have cavernous showrooms filled with dozens of variations of different pieces of furniture, and you select the one that fits best for you, pick a fabric, and then wait weeks or months to get it. Having gone through this process personally a few times, I’ll say I never enjoyed it, and the end result was never perfect. The most recent time, we ordered a sofa in February, and received it in November. Nine-month wait periods are not something customers enjoy.

Lovesac says none of that is necessary, and instead provides components that are essentially endlessly customizable. That means the applications are many and the odds of getting a great fit for your space are much higher. In addition, Lovesac components are interchangeable and reconfigurable, so they can work if you move or simply have different needs over time. These are immense benefits over traditional furniture.

One analogy I use for Lovesac is considering what Chipotle ( CMG ) has done with Mexican food. Chipotle doesn’t have dozens of items on its menu; it has a handful of ingredients and then you tell them exactly how you want it. That model works for everybody because it’s infinitely customizable for the customer. Lovesac is doing for furniture what Chipotle does for Mexican food. Instead of the customer compromising on whatever the traditional furniture store happens to have, the customer can get exactly what they need; there’s no compromise needed.

{kind=link}

The other advantage is that because Lovesac only makes a few components, it can get product to customers in days, rather than months. In my example above, I would have been much happier getting my sofa in nine days rather than nine months, and that speed of service is a huge advantage for Lovesac that other furniture retailers simply have no ability to counter.

Lovesac, because of the way it’s designed, is a platform of products, rather than just a sofa. The platform is highly customizable with attachments like custom covers and pillows, drink holders, and even speakers and charging outlets. Lovesac has found that customers buy a Lovesac product, and then buy additional components later on, including further Sactionals, but also attachments to upgrade what they’ve already got. The company reckons 42% of sales are to previous customers for this reason.

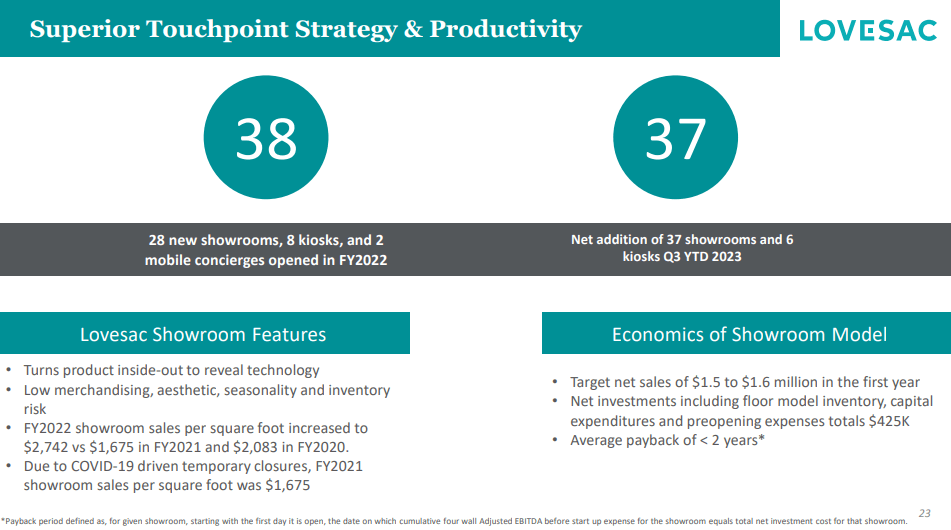

Lovesac’s growth has a very long runway, in my view, because it currently has fewer than 200 showrooms, and it is in the early stages of partnerships with large retailers with its shop-in-shop model. The company has partnerships with Costco ( COST ) and Best Buy ( BBY ) for shop-in-shops, which management has stated have high returns on investment. These allow for capital-efficient sales generation that work for both Lovesac and the partner financially. It’s an innovative sales strategy that the company has said it wants to expand and do more of, in addition to its showrooms.

{kind=link}

Showrooms have a payback of less than two years, which is why Lovesac is expanding so quickly. Sales per square foot are approaching $3k, and that’s with very little inventory on-site. That means that not only do the locations generate a lot of sales for the capital investment, but Lovesac isn’t spending huge amounts of money for inventory to sit and collect dust in stores.

The very short payback period on new stores means Lovesac is creating a flywheel effect that helps it generate more and more capital as more and more stores reach their payback point, and it can then invest in additional stores.

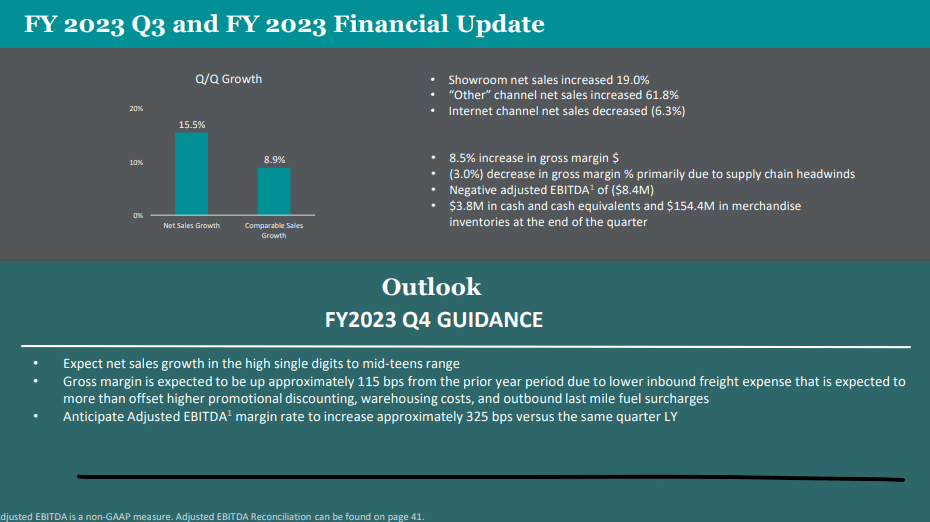

I briefly mentioned the December earnings report above, and the stock crashed off of that report. However, I think there are bright spots here that were ignored with the kneejerk selloff of the stock, the most salient of which can be seen below.

{kind=link}

The company guided for Q4 sales growth of high-single digits to mid-teens, but perhaps more importantly, for margin improvement. Gross margins are expected to be +115bps on lower freight expense, offsetting promotions and discounting. That should help adjusted EBITDA margin rise 325bps, which would be a massive improvement.

Investors have been rightly worried about retailers’ margins for months now, but Lovesac appears to be on its way to pushing margins higher in the coming months, rather than lower. If that comes to fruition, that’s a huge overhang removed from the stock.

Other considerations

I mentioned above that a reasonably large portion of the bull case here is that we may be entering a recession, but that it is already priced in. After all, conventional wisdom would tell you that you do not want to own home furnishings stocks heading into a recession. But what did we see earlier? Wall Street started buying them weeks ago . Why might that be?

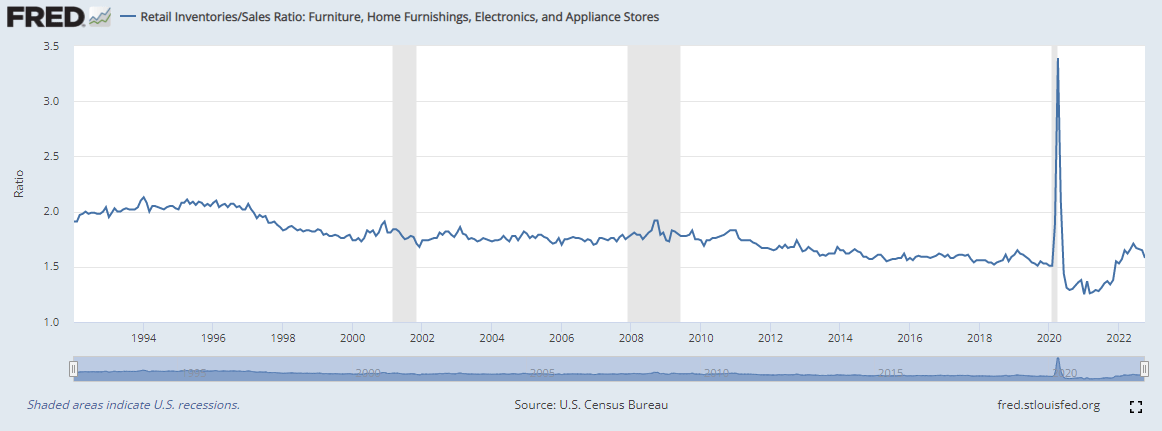

Let’s start with the worry that has been present for most of 2022 with retailers, and that is inventories. Below, we have a look at the ratio between inventories and sales of home furnishings, electronics, and appliance stores for the past 30 years. This gives us some historical context of how inventory levels are faring, and keep in mind that in general, lower is better (up to a point).

{kind=link}

This ratio spiked to historical highs during the initial stages of COVID because the sales portion of the equation fell off a cliff. Sales then spiked while inventory levels fell due to lack of production, leading to historically low values, briefly. If we ignore that noise, we can see that the ratio moved back to historical levels in 2022, but has started to come down.

What does this mean? It means that in general, if inventory levels are back in line with historical norms, the promotional activity that has been present for Lovesac and its competitors should be reduced going forward. Promotional activity moves product, but does so at reduced margins. Lower promotional activity, then, is good for profitability. This data suggests we’ve reached the tipping point, as does Lovesac’s guidance of less promotional activity going forward.

Shifting gears, Lovesac has short interest of about 11% of the float today, and while that’s not among the stocks that are most shorted, it’s significant. It also means that if the stock does take off higher, as I believe it will, there will come a time when those 11% of shares that are shorted would need to be bought back to avoid losses. I’m NOT suggesting a short squeeze is coming, because I don’t think it is. But I am suggesting that as we move into 2023, those shorts will need to be reduced as the stock rises, and that’s additional buying pressure.

Another feature I love about this stock is that the company has zero long-term debt . It has managed to expand rapidly without the use of the capital markets whatsoever. That has numerous benefits, including no interest expense, but it also means that if the company does want to borrow, it has tremendous flexibility to do so. At this point, I’d actually be in favor of the company borrowing to buy back stock, but the point is that zero long-term debt is hugely advantageous, and gives Lovesac all the financing flexibility it could need.

In addition, it has not issued any stock to fund expansion. Like just about every company, it does issue some stock for compensation, but it’s quite minimal. Point being, Lovesac is not “hiding” its financing needs through share issuances; it’s been able to do everything it needs to with internal funding.

Let’s now turn our attention to risks to the bull case.

Risks

The first and most obvious risk is that the recession that may or may not be coming ends up worse than expected. This is a real risk, and unfortunately, it isn’t one that we can know ahead of time with any certainty. I made the point above that it is my belief that a mild/short recession is priced into Lovesac and many other stocks. However, I could be wrong about that, and we could get a nasty and/or prolonged recession. I don’t think that will happen based upon current evidence, but I also don’t want to ignore that risk. If we do get a worse recession, the bull case for Lovesac would be significantly impacted, and not in a good way.

If we do get that scenario, it would see the appetite for risk assets decline, earnings estimates would decline, and the valuations investors are willing to pay would decline. All of those things would negatively impact Lovesac’s share price. I’ll say again I don’t think this will happen, but it could. The first clue will be money rotating out of riskier sectors, like home furnishings, so you'll see the charts start to break down.

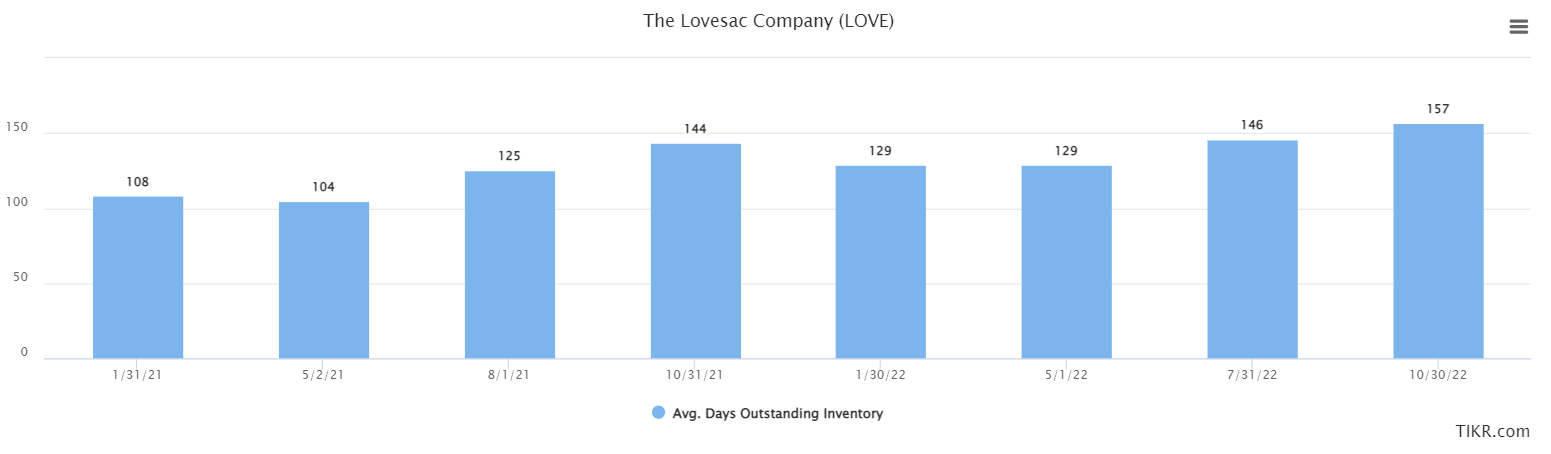

Next, Lovesac has more inventory on hand right now than it ever has before. Part of that is because it is positioning for sales expansion, and part is because it doesn’t want to get caught out by supply chain impediments.

{kind=link}

However, we can see the company had 157 days of sales outstanding in inventory at the end of the most recent quarter. That’s a lot of inventory, and if we do end up in a tough recession, it will prove to be too much. That would mean promotional activity would return in earnest, which would reduce pricing power, and therefore margins and earnings. This level of inventory would exacerbate a recessionary scenario, so that’s something to keep in mind if you think we’re heading into a tough economic period.

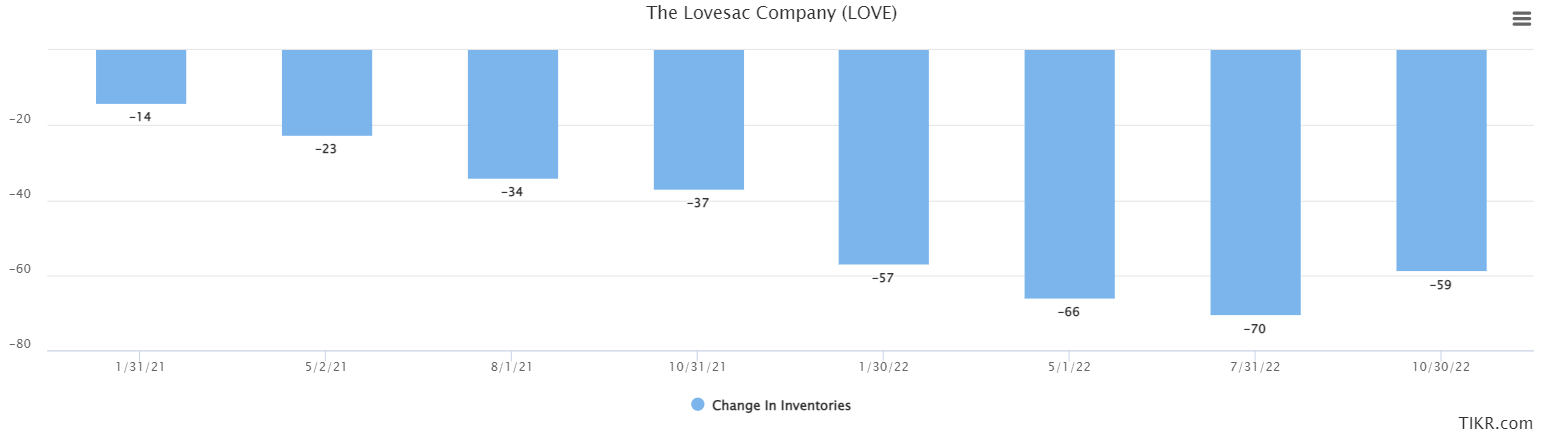

The other thing we know about inventory is that it consumes cash. Basically, buying inventory means the company has to use cash to purchase inventory, and the longer it sits, the longer it consumes cash that could otherwise be used for something else. The company’s rising inventory means its cash is being consumed at higher rates, and I’ve demonstrated that below with trailing-twelve-months cash flow impact from inventory builds.

{kind=link}

Inventory building appears to have peaked in the July quarter, with the October quarter showing an improvement from -$70 million to -$59 million. What we don’t want to see is this number go back down when the company reports in March. It’s okay to build inventory to a point, but this has caused the company’s cash flows to deteriorate significantly in recent quarters.

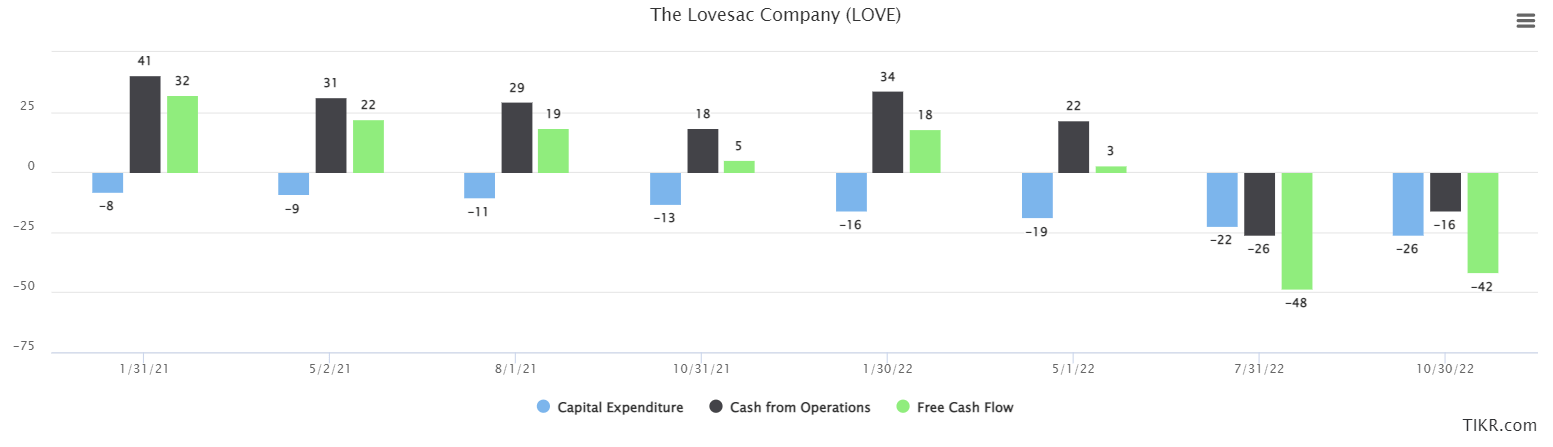

Below we have Lovesac’s capex, operating cash, and resulting free cash flow on a TTM basis for the past several quarters. Keep in mind that inventory builds come out of operating cash flow, and consequently, out of free cash flow.

{kind=link}

Inventory builds are the single largest cause of the company’s FCF declining in recent quarters, and if that continues, could be reason the company would need to go to the capital markets for financing. Its cash position was almost zero as of the end of the last quarter, so I’ll be very closely monitoring these numbers when the company reports in March. The level of FCF we see above is not sustainable, and it’s a risk to keep in mind. However, because it’s due to inventory builds, it should be fairly easy to reverse.

This is why it's important to understand the components of free cash flow, because Lovesac's headline FCF number is awful. Looking closer reveals its just inventory building and not something more persistent.

Growth and valuation

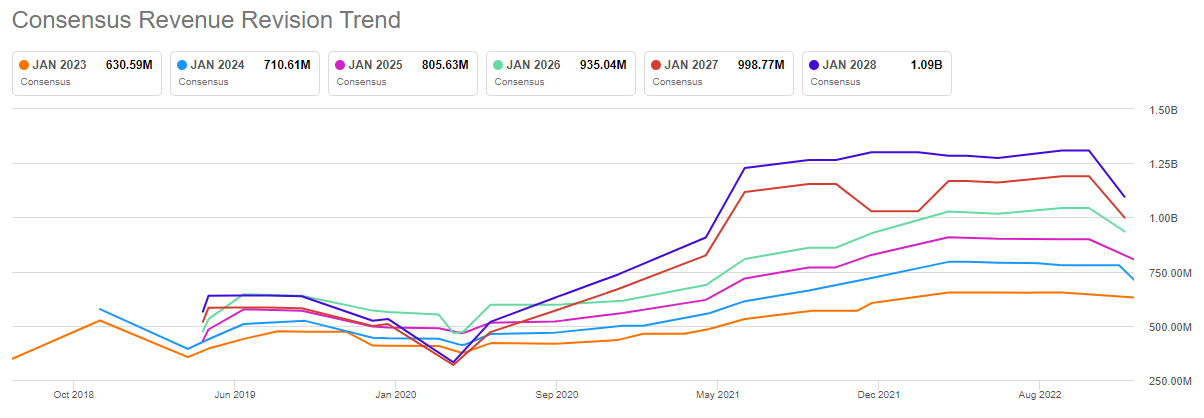

Before we dig into the valuation, let’s take a look at what analysts expect for Lovesac going forward; we’ll start with revenue.

{kind=link}

Revenue revisions have been negative recently, which is no surprise. However, we can see the revisions for this year have been very slight, with larger reductions in the out years. Just like we see analysts shoot too far when times are good, I believe revisions to the out years have been to harsh. Once the recession has passed, I believe we’ll see optimism return to the sector, and these lines will turn higher.

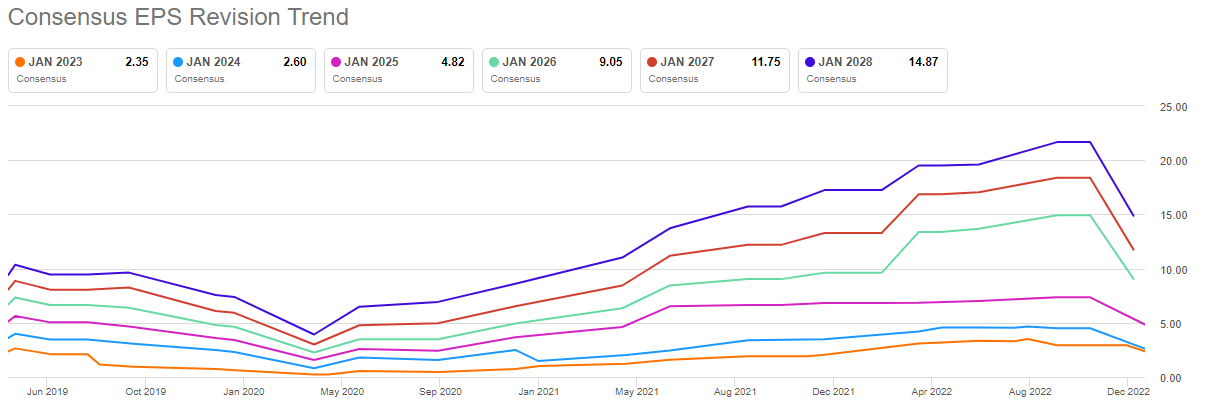

EPS revisions have been worse, as analysts are pricing in not only sales declines, but worse margins as well.

{kind=link}

Now, is it reasonable to expect Lovesac to produce lower margins as it expands? The playbook we’ve seen countless retailers follow would argue that’s counterintuitive. As a retailer expands its footprint and sales, it generally sees leverage on things like back office support, sourcing, rent, logistics, etc. That would mean profit margins would rise over time, and therefore, these revisions would prove to be too harsh. This is another reason I think Lovesac has upside in the coming months.

Lovesac’s growth rating with Seeking Alpha’s Quant system is A-, meaning it is one of the best in its class on that metric. Growth is a big reason why I like the stock, particularly in light of the valuation.

Speaking of that, Lovesac scores an A on valuation . Its PEG ratio is rock bottom at just 0.24, and again, a huge reason why I like the stock.

Lovesac only recently became profitable, so we cannot do a meaningful historical valuation based on a P/E ratio. However, we can use price/sales.

{kind=link}

The COVID low for P/S was 0.24X sales, which was very briefly hit during the initial panic selling. Before that, P/S was between 1X and 3X sales. Lovesac saw a higher range after COVID, but it has fallen to just 0.46X today. The point is that Lovesac is extremely cheap on this metric. But if you also consider that the company is now profitable, and its margins are much, much better than they used to be, I could easily argue its historical tendencies for P/S ratio are too low. After all, sales should be worth more to investors if they’re profitable, rather than not. At any rate, I think there’s huge upside to this ratio in the months to come, at least to 1X sales, but more likely closer to 2X unless we get a really nasty recession.

Finally, let’s look at relative P/E ratios going forward against some of Lovesac’s competitors.

{kind=link}

The stock is 8.5X earnings currently, but if we look out two years, its 4.2 . That’s half its closest competitor, and it speaks to the idea that Lovesac’s growth potential is being completely ignored right now.

Bassett ( BSET ), for instance, traded with a mean valuation of ~17X earnings pre-COVID. Bassett is more entrenched and larger than Lovesac, but has nowhere near the growth potential. Therefore, once the unpleasantness of the recession is past in 2023, I wouldn’t be surprised to see Lovesac trade at 20X+ earnings. With 15%+ growth rates each year, that would be a perfectly reasonable valuation. It’s also almost triple the current valuation, so that gives you an idea of the upside potential. I honestly believe we could see Lovesac at $50+ in 2023, and much more than that in the out years.

Final thoughts

It is my belief that 2023 is going to see a return to risk assets being in favor, and that we either will have no recession, or it will be brief and shallow. I could be wrong about that, and if I am, I’ll adjust my strategy as necessary. However, I see money rotating into home furnishing stocks, and as far as I can tell, the most attractive one of those is Lovesac.

It has a durable competitive advantage, it’s expanding rapidly, its margins are terrific and growing, it has an extremely clean balance sheet, and it’s very cheaply valued. Finally, the chart looks like it has made a sustainable bottom, and there’s really not much else I could ask for. That’s why Lovesac is my top pick for 2023, and here’s to hoping you have a prosperous and healthy New Year.

Editor's Note: This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Lovesac: My #1 Pick For 2023