LOVE - Lovesac: Navigating A Difficult Environment

2023-06-22 09:52:08 ET

Summary

- Lovesac, a modular couch and beanbag chair manufacturer, has seen its stock underperform, dropping over 10% since early 2024.

- Despite the challenging environment for home furnishings, Lovesac's product innovation and increased distribution provide potential for growth.

- LOVE stock looks attractively priced and management has been navigating the difficult environment well.

Back in February, I wrote that while its fiscal 2024 could be challenging that Lovesac ( LOVE ) looked poised to benefit from increased distribution touchpoints and product innovation. Since then, the stock has underperformed, down over -10%. Let's take a closer look at the stock.

Company Profile

As a reminder, LOVE makes modular couches and beanbag chairs. While named after its original product, an oversized beanbag chair called the Lovesac, nearly 90% of its sales today come from its line of modular line of couches called Sactionals. The modular couches come with removable covers that can be washed and can be configured in multiple ways and expanded upon in the future as needs change. Customers can add a number of accessories to their couches including a powerhubs, storage, drink holders and even surround sound through its StealthTech Sound+ option.

The company sells its products through showrooms, its e-commence website, and shop-in-shops at other retailers, including Costco ( COST ) and Best Buy ( BBY ). The company operated 211 showrooms at the end of April. The stores are on the smaller side, only about 800-1000 square feet.

A Rollercoaster Ride

LOVE's stock has been on a rollercoaster ride since I first wrote about it. The stock initially struggled mightily in early March as did much of the market, only to see a big rebound after it reported its fiscal Q4 results towards the end of the month.

While its Q4 EPS came in a bit light, sales easily topped the consensus and the company's FY2024 revenue guidance was also above analyst expectations. The stock rallied over 18% the following trading session.

Its FQ1 earnings reported earlier this month were met with less fanfare. The stock initially rose 10% pre-market, but finished the day down over -7%, a pretty big reversal.

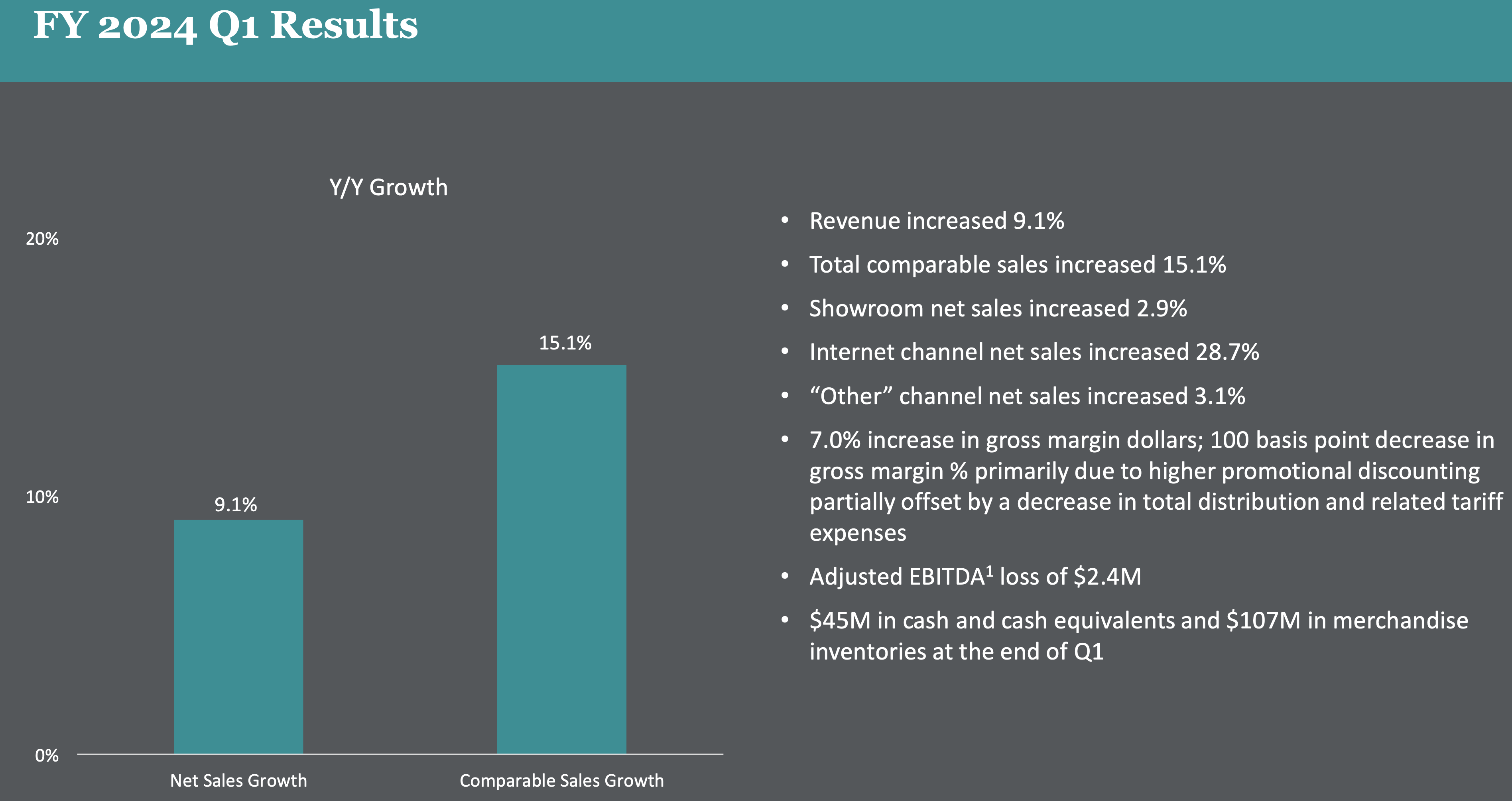

Overall, the quarter was solid given the current environment for home furnishings. Revenue rose 9.1% to $141.2 million, while same-store sales climbed 15.1%. Its sales were $7.5 million above the analyst consensus, while its loss of -28 cents was 13 cents above expectations.

{kind=link}

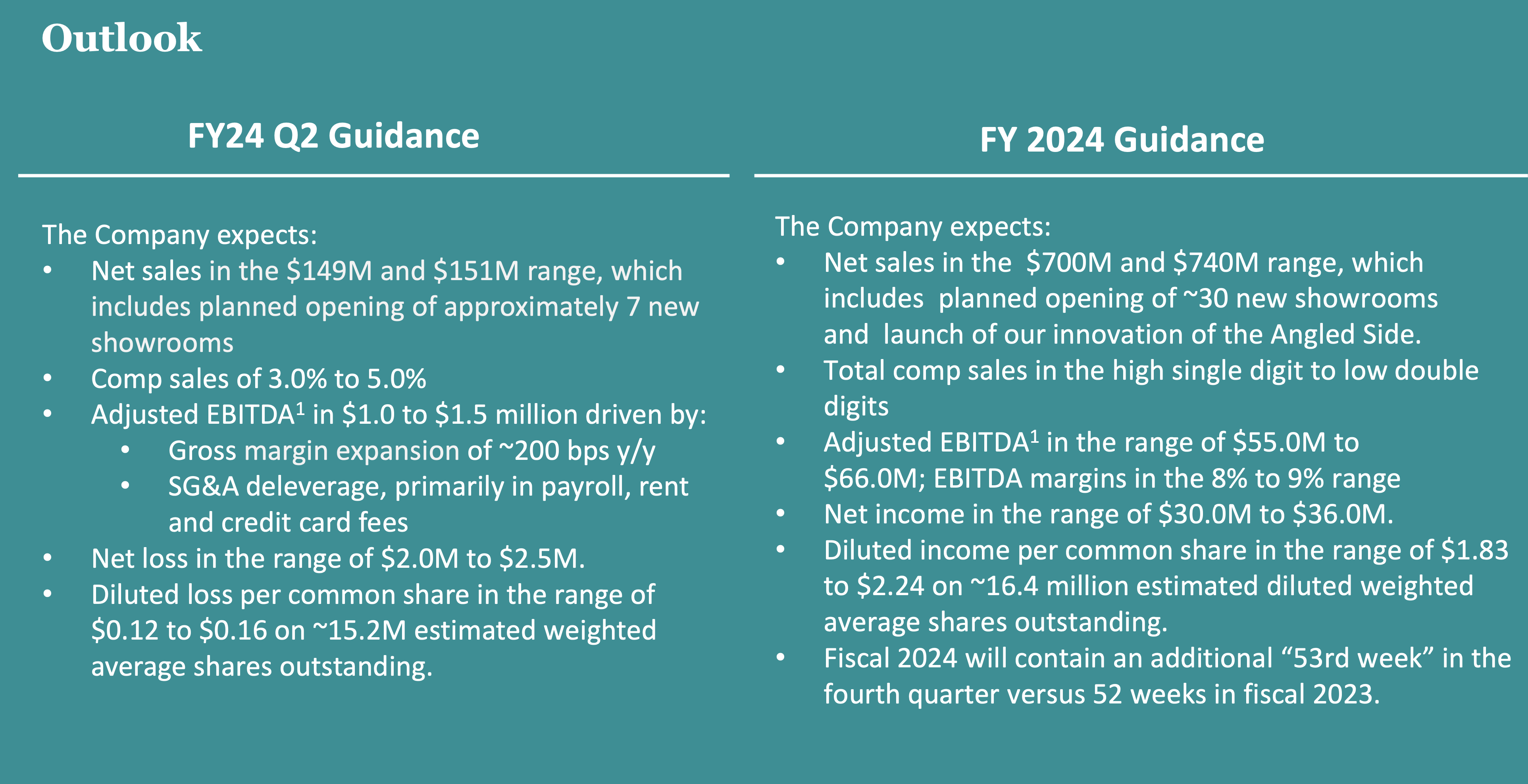

Guidance, meanwhile, was also solid, with the company maintaining its outlook for sales of between $700-740 million and adjusted EBITDA of between $55-66 million. Adjusted EPS is projected to come in between $1.83-2.24.

{kind=link}

If there was one area to be critical of it was on the expense line, where SG&A increased 26.6% and rose 560 basis points as a percentage of sales. Marketing costs rose 6.4% and decreased as a percentage of sales, so increased payroll costs and rent were the main culprits. Gross margins also decline by -100 basis points, but overall remained a solid 50.1%.

In my original write-up, increased distribution was one of the areas I talked about as being a driver for LOVE. On that front, the company had 50 more showrooms (and one less kiosk) than it did a year ago, including adding 16 in Q1. It also opened up one BBY shop-in-shop as well. Meanwhile, at COST demand was up 5.6%.

Adding more locations should continue to help with brand awareness, powering sales. The company has done a good job of opening showrooms, and I'd like to see more shop-in-shop locations in the future. There are still plenty of BBY locations it can get space in (it's only in 23 stores), and I'd think the concept could do well at places like Target ( TGT ) and Kohl's ( KSS ).

Innovation was another key driver I discussed, and on that front the company introduced angled sides to its sactionals in May in a soft launch. The company said the lack on angled sides was one of the biggest reasons for people not completing purchases. Since its introduction, it said it has seen strong quotes and conversion with the new style. The style will become available on its e-commerce website by the end of July, with a full media campaign promoting it in August. The company further noted that it should lead to other aesthetic and comfort innovations.

Of course, the current environment for home furnishings and home décor hasn't been strong, as noted in my recent article on RH ( RH ). However, LOVE management believes that its focus on couches gives it an advantage and makes it less vulnerable to recession.

Commenting on the current environment on its Q1 earnings call , CEO Shawn Nelson said:

"It is important for investors to understand one key reason why Lovesac demand remains so strong versus the competition and why management remains confident at least, cautiously optimistic in this environment. We sell value products. This is widely misinterpreted because of our product's high sticker price. Our Sacs, which look like giant bean bags sell for more than $1,000 on average. Sactionals, which are the majority of our sales are priced at the high end for upholstery to be sure. The typical first Sactionals purchase averages around $5,000 and it is not at all in common to see transactions in the $10,000, $15,000 and even $20,000 range on a daily basis, especially since the introduction of StealthTech. But this customer is a value customer. They are choosing to spend quite a bit of money with us because of all the value we designed into the product and platform. …

"Furthermore, we are a couch specialist and the strongest one in the marketplace at that. We have significant scale now. We estimate that our Sactionals business alone to be larger than many of our furniture generalist competitors' entire upholstery businesses across all of their disparate upholstery SKU. Unlike furniture generalists, however, the couch category operates on slightly different dynamics than the home decor market broadly. The #1 driver of couch replacement behavior is old or worn out couches, not new home sales, relocation or even remodels. Even in a recession, couches [wear out.] It doesn't make us recession-proof, but it is still a much better dynamic than being in the furniture business as a generalist at times like these. Not to mention the inventory implications alone, these advantaged Lovesac."

Couches being more of a replacement product than general furniture makes sense, but LOVE is still certainly selling an expensive product. During a tough macro-environment, consumers may certainly look towards cheaper options, even if they don't provide as much "value." LOVE also gets about 40% of its orders from existing customers, who could choose to delay their purchases as well.

Valuation

LOVE currently trades around 8.5x the FY 2024 (ending January) consensus EBITDA of $58.4 million and 5.8x the FY25 consensus of $85.9 million.

It trades at a forward PE of 12x the FY24 consensus of $2.08.

The company is projected to grow revenue 9% in FY24 to $711.1 million, before accelerating to 13.5% in FY25.

While not a great comparison, as there really aren't any, RH trades at a forward PE of about 28.7x. LOVE doesn't have enough history as a profitable company to look at past valuations.

Conclusion

LOVE has been doing a good job managing a very difficult environment for home furnishings and home décor. Meanwhile, it still has plenty of runway for growth through increased distribution and product innovation.

The current environment remains difficult, and the company appears to have gotten more promotional. I've been seeing a lot more discount emails than a year ago. However, it's not discounting a higher percentage than it normally has in the past.

Overall, while I think there near term could remain difficult, I think the stock looks attractively priced and that management has been doing a good job overall navigating this environment. My "Buy" rating remains unchanged.

For further details see:

Lovesac: Navigating A Difficult Environment