LOVE - Lovesac: Priced For Value But With Growth

2023-10-17 01:31:43 ET

Summary

- Lovesac Company produces modular couches that have positioned the company for good growth with high gross margins.

- The stock is priced very low with a forward P/E of 8.1, and my DCF model estimates a good upside for the stock.

- Lovesac has risks as the furnishing industry has performed very poorly in recent quarters and as the company's cash flows haven't matured yet.

- In total, the risk-to-reward ratio seems worthy - I think the stock is worthy of looking into.

The Lovesac Company ( LOVE ) produces modular couches. The company has achieved very high organic growth in the past years and has managed to grow its operating margin simultaneously. At the current forward P/E of 8.1, the stock seems to be priced incredibly low – although Lovesac operates in a very cyclical industry, and still has an uncertain future in terms of margins and growth, the stock seems intriguing. As my DCF model estimates a significant upside for the stock, I have a buy rating for the stock.

The Company & Stock

Lovesac produces couches among other similar furnishing items. The company has been able to craft a unique offering, as the company markets its couches as changeable, moveable, and rearrangeable. The company sells its products through retail stores and e-commerce – Lovesac has partnered with large companies such as Costco and Best Buy to sell its offering.

The company’s operating model varies in some aspects from traditional operators in the industry – the company focuses on direct-to-consumer sales and a light-inventory showroom model. Also, the company has increased e-commerce as a sales channel from 23.9% in FY2020 to 27.1% in FY2023, providing a lighter business model in terms of inventory.

The stock has seen a massive decrease in price in the past six months due to softer demand and issues in reporting financials – Lovesac’s stock has fallen by around 40% in the period:

{kind=link}

Six-Month Stock Chart (Seeking Alpha)

Financials

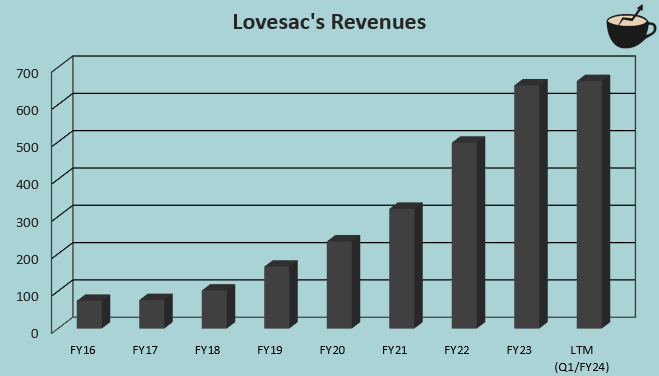

Lovesac has had a very impressive growth in its history, albeit from a low revenue level in the beginning – the company has achieved a compounded annual growth rate of 36.4% from FY2016 to FY2023:

{kind=link}

Author's Calculation Using Seeking Alpha Data

The growth has been achieved through organic efforts as Lovesac continues to open up new showrooms and launch new products. The company anticipates FY2024 to have a growth of 10.5% with the middle point of its guidance, signifying a significant slowdown in the company’s growth. I believe that the lower growth is both a result of already larger operations, and a soft demand as well. In the company’s Q1/FY2024 earnings call, Lovesac’s CEO Shawn Nelson communicated the following:

“We are pleased with our first quarter results that beat expectations even amidst a challenging macro backdrop and against our toughest comparison of the year in the first quarter. Elevated inflation and higher interest rates continued to drive a more cautious consumer, pressuring the home category overall. We are not immune from these headwinds. But as evidenced by our consistent and reliable results, we have significant advantages versus the broader category…”

In my opinion, the growth could still potentially be well above the current year’s growth in the medium-term – in Q1, Lovesac achieved a growth of 9.1%, but competitors have had a significantly harder time in keeping up revenues. For example, Hooker Furnishing Corporation had a revenue decline of -17.3% in the same period, Ethan Allen had a decline of -5.7% in Q1 (although from January to March), and La-Z-Boy Incorporated had a decline of -18.0% in the period – the industry is struggling as a whole, and Lovesac could experience significant growth as the industry recovers.

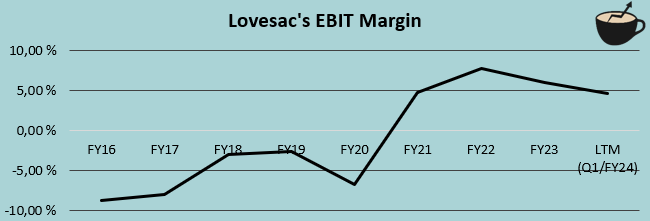

Lovesac’s EBIT margin stayed negative for a long period as the company had massive growth plans and extensive investments. The company has since been able to achieve profitability, as in FY2023 the EBIT margin stood at 6.0%, but has since decreased due to the softer demand:

{kind=link}

Author's Calculation Using Seeking Alpha Data

I believe that Lovesac still has a good amount of operating leverage yet to be unlocked – the company has a strong trailing gross margin of 52.8%, and as the operations scale up, the fixed costs should come down as a percentage of gross profit.

Valuation

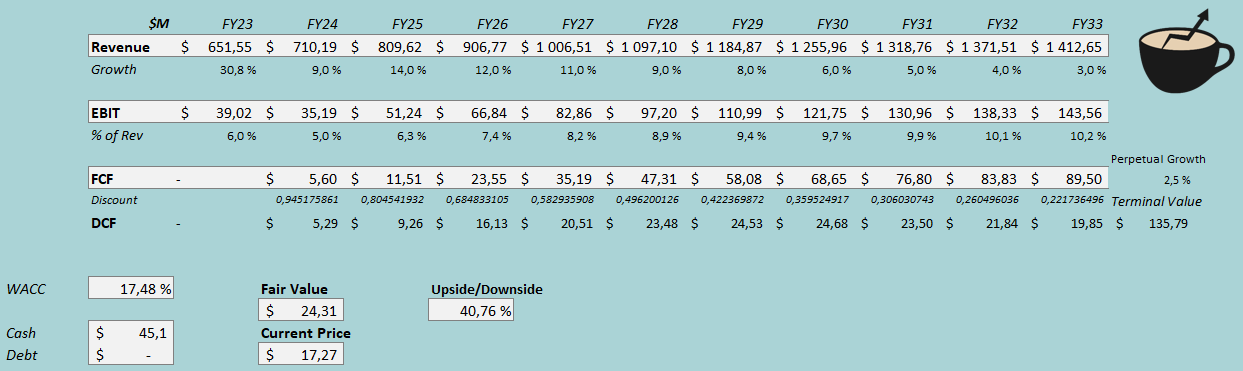

Lovesac currently trades at a forward P/E of 8.1, well below the stock’s average of 10.6 and a high of 14.3 in the past year. I believe the ratio is quite low as Lovesac has demonstrated an ability to grow its revenues and earnings. To further analyze the valuation, I created a discounted cash flow model as usual. In the model, I estimate Lovesac to have a growth of 9%, representing the lower quartile of the company’s guidance of $700 million to $740 million. After FY2024, I estimate slightly higher growth as the furnishing market should recover at some point – for FY2025, I estimate a growth of 14%. After the year, I estimate the growth to slow down in small steps into a perpetual growth rate of 2.5%. The estimated growth represents a CAGR of 8.0% from FY2023 to FY2033.

As for Lovesac’s EBIT margin, I estimate a slight decrease of one percentage point in FY2024 as a result of softer demand. After the year, my DCF model estimates the industry to recover and Lovesac to achieve further operating leverage – in the model, the EBIT margin for FY2033 stands at a figure of 10.2%. As Lovesac continues to invest heavily and eats up working capital, I believe the company should have quite poor cash flow conversion in the medium-term, but a moderately good conversion in the long term.

The mentioned estimates along with a cost of capital of 17.48% craft the following DCF model with an estimated fair value of $24.31, around 41% above the price at the time of writing:

{kind=link}

DCF Model (Author's Calculation)

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

Lovesac doesn’t currently hold interest-bearing bets that are non-operational in nature – in the CAPM, I use figures that I see as reasonable for the debt financing part. I estimate a long-term interest rate of 5.71% for Lovesac – the United States’ 10-year bond yield stands at 4.71% at the time of writing, and I add a margin of one percentage point into the estimate for some safety. The company doesn’t currently hold debt, but I estimate Lovesac to leverage debt as the company matures with a long-term debt-to-equity ratio estimate of 15%.

On the cost of equity side, I use the US’ 10-year bond yield as the risk-free rate. The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate made in July. The very high beta of 2.47 is taken from Yahoo Finance. Finally, I add a small liquidity premium of 0.5% into the cost of equity, crafting the figure at 19.81% and the WACC at 17.48%.

Risks

The company had difficulties in reporting its Q2/FY2024 result on time as Nasdaq has issued a warning for the company – Lovesac expects net sales of around $154 million and a net loss of $0.5 million to $1.5 million in the quarter ranging from May to July of 2023, as per the company’s press release . The quarter does seem to be in line with Lovesac’s earlier expectations, or even slightly above, as the company had the following guidance in their Q1 earnings presentation:

Q2 Guidance as of Q1 (Lovesac Q1 Earnings Presentation)

The delayed but mostly communicated quarter seems to be quite good as earnings should slightly overperform the given guidance. Still, I would be cautious with a business such as Lovesac – the company operates in a highly cyclical industry as Aswath Damodaran estimates a beta of 1.27 for the home furnishings industry. Further, Lovesac’s beta of 2.47 demonstrates the company’s risky position in the industry as the company is still looking for its position in the market and is yet to experience most of its operating leverage with currently quite weak cash flows. Furnishing as an industry has performed very poorly in the most recent quarters, as demonstrated in the financials -segment. The soft demand could last for a prolonged period, creating grounds for very weak cash flows for Lovesac -the company does currently have a cash balance of $45 million, but a long period of soft cash flows could create a need for further financing, possibly being costly for current investors.

Takeaway

I believe that Lovesac is currently a stock worth looking into. The stock seems to be priced very low considering the company’s historical growth – my DCF model demonstrates the same with an upside of 41%. The DCF model also accounts for a very high beta of 2.47 through the CAPM – as Lovesac achieves a more mature position in the industry, I believe that the beta could be significantly lower in the future, creating further upside. For example, with a beta of 2.00, the DCF model would estimate an upside of 72%.

Although the stock seems quite promising, Lovesac doesn’t come without risks – the furnishing industry is performing very poorly in the current economy. Also, the slope of Lovesac’s long-term growth and the company’s margin capacity is quite unknown – in total, the stock is still quite an uncertain investment. At the moment, though, the risk-to-reward ratio seems worthy – I have a buy rating for the stock.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Lovesac: Priced For Value, But With Growth