LOVE - Lovesac: Sell-Off Provides A Good Entry Point

2023-11-29 01:53:17 ET

Summary

- Lovesac has been seeing its sales grow despite a very difficult home furnishings market.

- Gross margins have held up well, although increased expenses have eaten into profitability.

- The stock's valuation looks inexpensive given its growth prospects.

Back in February, I placed a “Buy” rating on Lovesac ( LOVE ), saying that while FY24 could be challenging that the long term should be solid as the company continues to innovate and increase its distribution touchpoints. I followed that up in June , saying the stock looked attractively priced as management has navigated a difficult environment well.

Company Profile

As a quick refresher, LOVE is best known for its modular line of couches called Sactionals, which make up nearly 90% of its sales. The couches can be arranged in a variety of configurations, while a number of accessories including powerhubs, storage, drink holders, and even surround sound, can be added. Its name comes from its original offering, which was an oversized beanbag chair called the Lovesac, which it still sells.

LOVE sells its furniture through its own showrooms and e-commence platform, as well as through shop-in-shops at other retailers, including Costco ( COST ) and Best Buy ( BBY ). The company operated 223 showrooms at the end of July.

Delayed Q2 Results

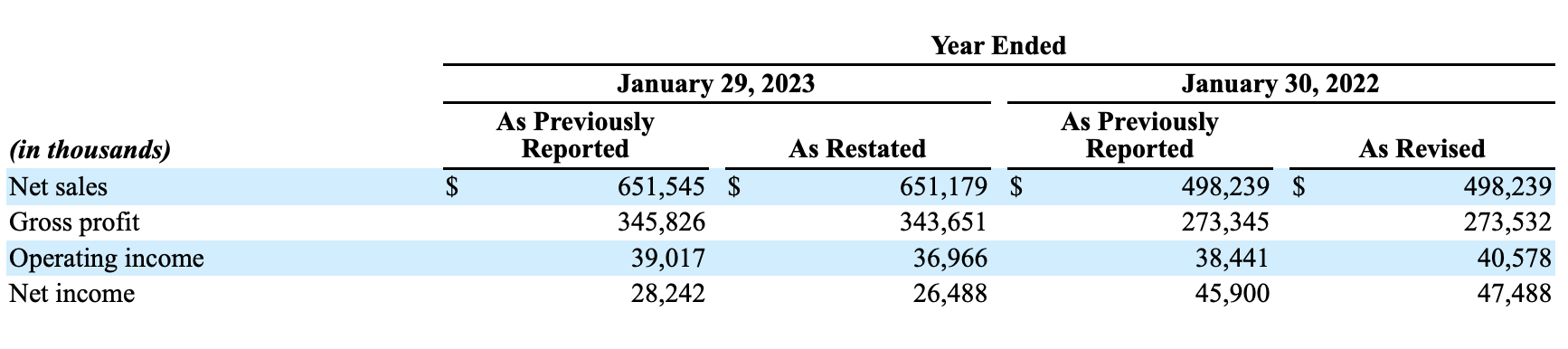

LOVE didn’t report its Q2 results ending in July until earlier this month due to the need to restate previously issued 2023 and Q1 FY24 results related to how it calculated the accrual of its last mile freight expenses.

For Q2, the company reported a 4.0% increase in sales to $154.5 million. That topped the analyst consensus for sales of $154.0 million.

Total comparable store sales climbed 7.2%, while comparable showroom sales rose 2.7%. Internet sales climbed 16.6%, while total e-commerce sales, which include Costco.com and bestbuy.com, were up 12.8%. The company ended the quarter with 223 showrooms, compared to 174 a year ago.

The company added 18 showrooms in the quarter and 3 BBY shop-in-shops.

Sales from COST were up 15% in the quarter, as the warehouse retailer increased its number of pop-up-sop days.

Sactional sales increased 3%, while Sac sales jumped 18%. Other sales, which includes decorative pillows, blankets and accessories, rose 12%.

Gross margins improved 650 basis points to 59.8% from 53.3%. However, SG&A expenses soared 30.8% to $63.8 million and advertising & marketing expense climbed 39.0% to $26.5 million. Advertising & Marketing was 17.2% of sales, an increase of 430 basis points. The company noted that it increased advertising for its 25 th anniversary celebration and for its introduction of angled sides.

Adjusted EBITDA fell -57.1% to $5.3 million. EPS was a loss of -4 cents versus 37 cents a year ago, but topped the -13 cent consensus.

The company ended the quarter with $54.7 million in cash and equivalents and no debt. Through the first half of the year, it has generated free cash flow of nearly $15 million.

Looking to Q3, the company sees net sales of approximately $154.0 million. That would be about a 14% increase in revenue. Ahead of its Q2 earnings release, analysts were looking for Q3 revenue of around $150 million.

It projected adjusted EBITDA to be between a loss of -$1.5 million to a gain of $0.5 million. It is projecting EPS to be a loss between -20 cents to -33 cents. A year ago, the company reported -$8.4 million in adjusted EBITDA and EPS of -55 cents.

For the full year, the company forecast revenue to be between $710.0-730.0 million. It is looking for adjusted EBITDA to be between $51.0-63.0 million and EPS of between $1.21-$1.75.

Discussing its outlook of its Q2 earnings call, CEO Shawn Nelson said:

“Looking to the second half of the year, we expect the macro environment to remain challenging, continuing to pressure the home category. We are not planning for any meaningful recovery in category growth this fiscal year. In terms of the promotional environment, we expect it will be more competitive as we head into holiday season and anticipate more frequency and depth of discounting across the industry. We've adapted our own plans accordingly, and we'll remain very agile through the holiday season. Even taking this into account, which doesn't change our confidence that Lovesac will continue to outperform the category and yes, generate stronger growth in the second half than the first half. ... Given the macro backdrop, we're highly cautious operationally. We're focused on efficiency and will control expenses very tightly. This will become more clear as we lap necessary foundational investments that began in the second half of fiscal '23 and which put peak pressure on bottom-line growth in second and third quarters this year.”

Management said it is currently being more selective with marketing, although it has started using prime and linear TV buys to increase brand awareness. It also entered into a partnership with partnered with Architectural Digest.

Overall, LOVE reported solid Q2, and basically Q3 sales since the quarter was essentially over when it reported its Q2 results, given the difficult home furnishings retail environment. Gross margins, meanwhile, also improved, which was nice to see. The company continues to add new showrooms and shop-in-shops, which over the long-term should help drive sales.

On the downside, I would have liked to have seen expenses kept more in check, and the company did spend a fair amount on advertising. The Q2 ad spending increase did co-inside with its angled side launch, which is an innovation that should drive sales, so I wouldn’t fault the company too much for ramping it up a bit. LOVE’s currently trying out some new marketing tactics, so we’ll have to see how they play out and if they are more efficient.

Currently, the home furnishing market looks pretty promotional as the holiday shopping season kicks into full gear. For its part, LOVE is offering 30% off Sactionals and 35% of Sac & Sactional bundles for Black Friday, which is a bigger discount than its more typical 25% of sales. That is likely to have a slight impact on gross margins, but that appears to already be contemplated in guidance. Meanwhile, its full-year guidance is a pretty wide range, indicating the uncertainty the current market environment is causing.

The current macro-environment and continued weak home furnishing market are the biggest risks to the stock, as the industry as whole is facing a very difficult period after seeing a pull-forward of demand with COVID and now lack of movement in the housing market given high interest rates. This also creates a very promotional environment and intense competition for waning overall industry sales.

Valuation

LOVE currently trades around 7.8x the FY 2024 (ending January) consensus EBITDA of $52.8 million and 5.9x the FY25 consensus of $70.1 million.

From an EBITDAR perspective, it trades at 5.5x FY24 estimates and just over 4x FY25 estimates.

It trades at a forward PE of 12x the FY24 consensus of $1.59 and x the FY2025 consensus of $2.34.

The company is projected to grow revenue 9.7% in FY24 to $714.9 million and 8.7% in FY25.

While not a great comparison, as there really aren't any, RH ( RH ) trades at nearly 12x FY25 (ending January) EBITDA with expected FY25 revenue growth of 7.5% and Arhaus (ARHS) trades at 8x EBITDA 2024 EBITDA with expected revenue growth of 3.7%.

Based on that, I’d value LOVE at around $38, which is a 10x EBITDA multiple and 7x EBITDAR multiple.

Conclusion

While the stock performance certainly doesn’t reflect it, I think LOVE has done a good job navigating what has been one of the worst markets for home furnishings in a very long time. Sales and gross margins have held up well, although certainly other expenses could be held in check more.

The restatements were a bit of a distraction, but at the end of the day, they were pretty minor and only had a small impact on past results.

LOVE FY2023 Restatement (10-K/A)

{kind=link}

When I started LOVE with a “Buy,” I knew this year would not be easy, which it hasn’t, but I think the company has done a nice job. The difficult home furnishing market, meanwhile, will likely continue into 2024. That said, I think the stock is attractively priced and that its prospects over the next few years look solid. A such, I continue to rate the stock a “Buy,” and I’m placing a target of $38 on the stock, which is more in line with higher-end furniture peers.

For further details see:

Lovesac: Sell-Off Provides A Good Entry Point