LOVE - Lovesac: Time To Divest

Summary

- Shares of Lovesac have soared 30% this year after sharp declines in 2022.

- The outlook for the company doesn't look much brighter, with sales growth decelerating and inventory piling.

- In addition, gross margins are being pressured by higher freight costs and more aggressive discounting.

- Though cheap at ~12x forward P/E, I find it difficult to believe Lovesac can hit consensus estimates with both top and bottom line pressures weighing.

Yes, the market is rebounding in 2023, but now is not the time to be complacent. I've been aggressively reviewing my portfolio of small and mid-cap growth stocks to determine which companies are poised for a further rally while also cutting out those that I think have reached the end of their rope.

Lovesac ( LOVE ) is a position that I have decided to trim. This furniture vendor, popular for its "Sactionals" products that offer a modular mix-and-match design, has already seen its share price climb by ~30% this year. And though the stock continues to be cheap on paper, I think Lovesac has run out of fuel for a further rebound, especially as fundamental results are tipping toward worsening in 2023.

With revenue deceleration, margin compression, and inventory buildup, Lovesac has become a value trap

Though previously bullish on Lovesac last summer , I am sharply cutting my outlook on this company to sell. I see too many red flags here to ignore.

No doubt that Lovesac was a powerful investment during the heyday of the pandemic. Back then, the company enjoyed a bevy of fundamental tailwinds. The stock market was riding high, and well-to-do upper-middle class consumers were spending more and more on home comfort. At the same time, the rising popularity of remote work and out-migration from cities and into suburbs drove a big one-time boost for furniture and home-goods companies.

But as we know now, big hard-goods purchases like furniture have a very long replacement cycle. The pandemic pulled-forward a lot of this demand, and Lovesac's growth has slowed to the mid-teens. Amid this backdrop, however, potentially forecasting that outsized growth would continue at a much faster pace, Lovesac has aggressively expanded its showroom fleet across the U.S. while piling on more sales and marketing expenses. It's taking on the typical tech playbook of "grow now, hit profitability later" - but the biggest draw to Lovesac, in my opinion, was its relatively rich profitability profile and reasonable valuation against those earnings.

Yes, Lovesac is still technically a value stock. At current share prices near $29, the company trades at just a 12x forward P/E against Wall Street's consensus FY23 pro forma EPS of $2.45 (data from Yahoo Finance ). This is an assumption of 24% y/y earnings growth (versus consensus estimates of $2.05 in FY22 EPS) on 11% y/y revenue growth.

Both assumptions, in my view, are at risk. Revenue growth has already decelerated to 15% y/y as of Lovesac's October quarter, and in my view macro pressures have only sharpened since then. We also can't ignore the state of the housing/real estate market in relation to Lovesac's sales. With interest rates high and real estate activity low, the number of people moving is also declining - which is a big driver behind furniture sales.

The assumption of EPS growth faster than revenue growth (implying margin gains) is also one to challenge. Gross margins have been in sharp decline, driven by rising freight costs. With Lovesac's most recent quarter showing a rise in inventory, the company may also see an increase in holding costs as well as more promotional activity to move product.

The bottom line here: I think most signs point to downward estimate revisions for Lovesac, and the current stock price reflects the company's new macroeconomic reality. I would cut any losses at this point and wait for Lovesac to either show an upward growth trajectory or see a sharp compression in share prices before diving back into this stock.

Q3 indicators point to further pain ahead

There are several red flags in Lovesac's fiscal Q3 (October quarter), released in early December, to watch out for - as I think these conditions will only worsen heading into 2023.

{kind=link}

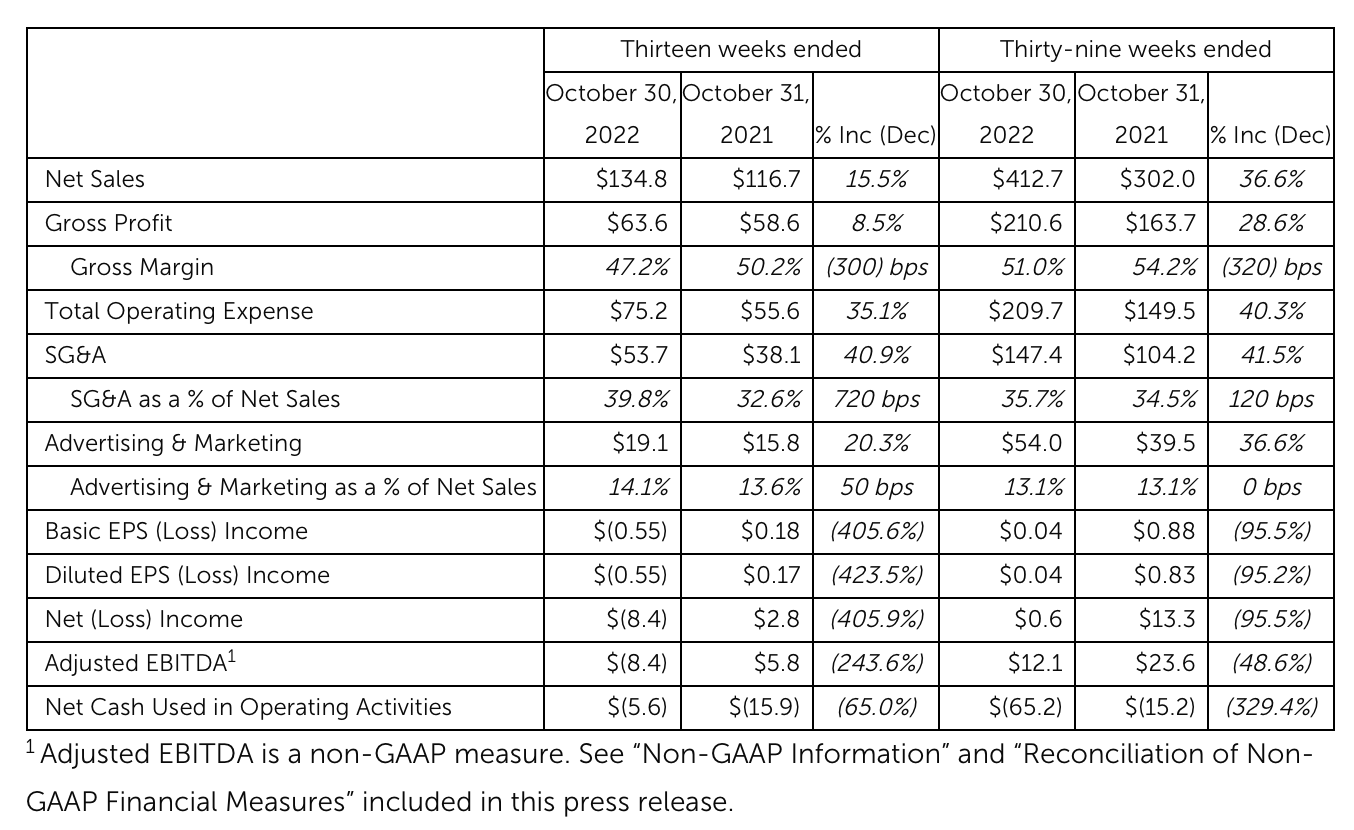

First, we've started to see a sharp deceleration in revenue. As shown in the chart above, revenue growth decelerated to 15% y/y in Q3, down sharply from 45% y/y growth in Q2.

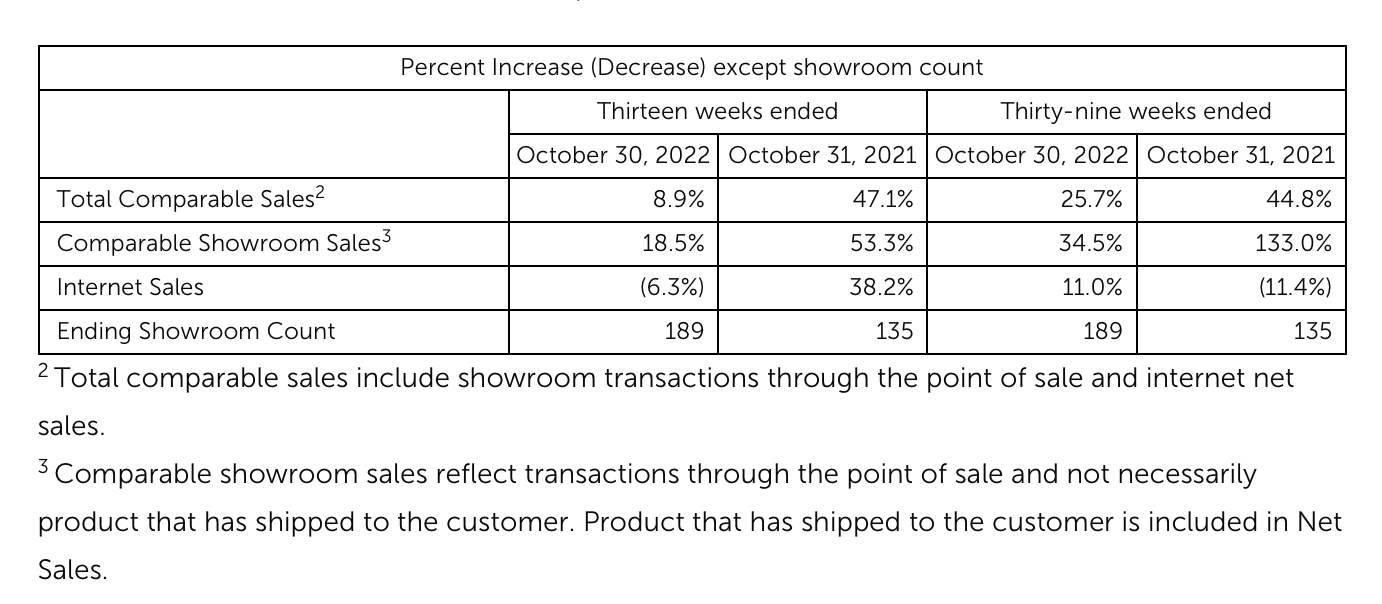

And this result is in spite of Lovesac's broad expansion in showrooms. At the end of the October quarter, Lovesac had 189 showrooms in its fleet, up 40% from 135 in the prior-year Q3.

{kind=link}

What I think is a better indicator of underlying sales growth, which normalizes for the expansion of Lovesac's geographic coverage and store footprint, is internet sales - down -6% y/y. While it's true that there has been "channel mix shift" into physical retail outlets since last year due to the re-opening of malls and brick-and-mortar stores, I think Lovesac's underlying business growth performance is better reflected in its total comparable sales growth of 9% y/y, which excludes the impact of new stores added since the prior year. Against this backdrop, I find it difficult to believe that Lovesac can truly hit consensus expectations of 11% y/y revenue growth in 2023 without significantly expanding its store fleet again (which would come at a cost to profitability).

Gross margins, too, are down 300bps to 47.2% (though we note that for a consumer products company, Lovesac still carries quite a high margin profile, reflecting a decent buildup of brand equity). Per CFO Donna Dellomo's remarks on the Q3 earnings call , gross margin declines were primarily driven by freight increases:

The decrease in gross margin rate of 300 basis points over the prior year period was driven by an increase of approximately 160 basis points in total freight costs, which includes in-bound and outbound freight, tariff expenses, and warehousing costs, and 140 basis point decrease in product margin driven by higher planned promotional activity.

Our gross margin rate exceeded our guidance, driven primarily by lower in-bound freight costs and realization of the lower freight benefits through the P&L earlier than we have projected, partially offset by a slightly lower product margin rate. We do anticipate in-bound freight rates to stabilize at this level for the remainder of fiscal 2023, but because of the amount of inventory we maintain on-hand to support customer satisfaction of the brand, we will not see the full benefit to the P&L of the drop in these rates as compared to prior year until the associated inventory is sold during late Q4 and continuing through the first half of fiscal 2024."

Driven both by gross margin declines and opex increases related to the company's store fleet expansion, adjusted EBITDA swung to negative -$8.4 million, while pro forma EPS of -$0.55 also showed a sharp contraction versus a profit of $0.18 in the year-ago Q3.

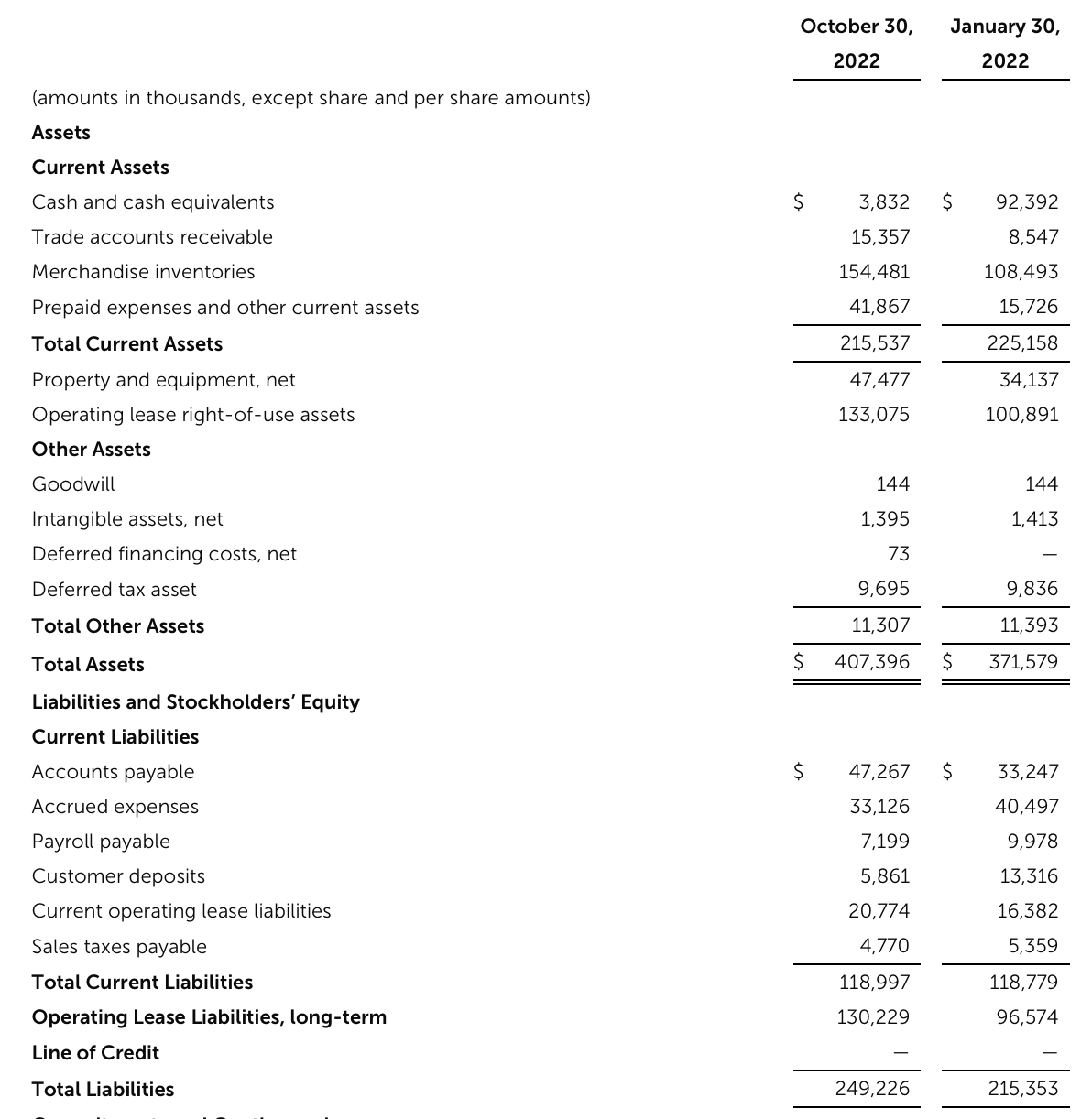

We should also note Lovesac's dramatically weakened balance sheet position. As of Q3, the company has only $3.8 million of balance sheet cash remaining. The good news is that Lovesac does have an unused line of credit from Wells Fargo ( WFC ) (which provides for up to $40 million of borrowings, per the company's latest 10-Q filing ) - but as this line of credit is priced on a variable basis amid rising interest rates, Lovesac's profitability will continue to get crushed by the additional burden of interest costs if it turns to debt to finance its buildup in inventory.

{kind=link}

Key takeaways

Lovesac is in a tough position. It is chasing sales growth by expanding its store fleet, but this is requiring the company to hold more inventory, draining its cash reserves and potentially requiring it to dip into interest-bearing debt. And amid a potential recessionary crunch, the company may need to turn to more aggressive discounting to keep its inventory moving, damaging gross margins and impacting profitability further.

Steer clear here.

For further details see:

Lovesac: Time To Divest