BFFAF - Lower EU Gas Prices BASF Is Our Top Pick

Summary

- Gas prices are down significantly, but we are more concerned about the medium-term horizon.

- Many chemical players are opting for de-stocking policies, and this should support pricing power.

- BASF is still trading at a lower P/E compared to its historical average.

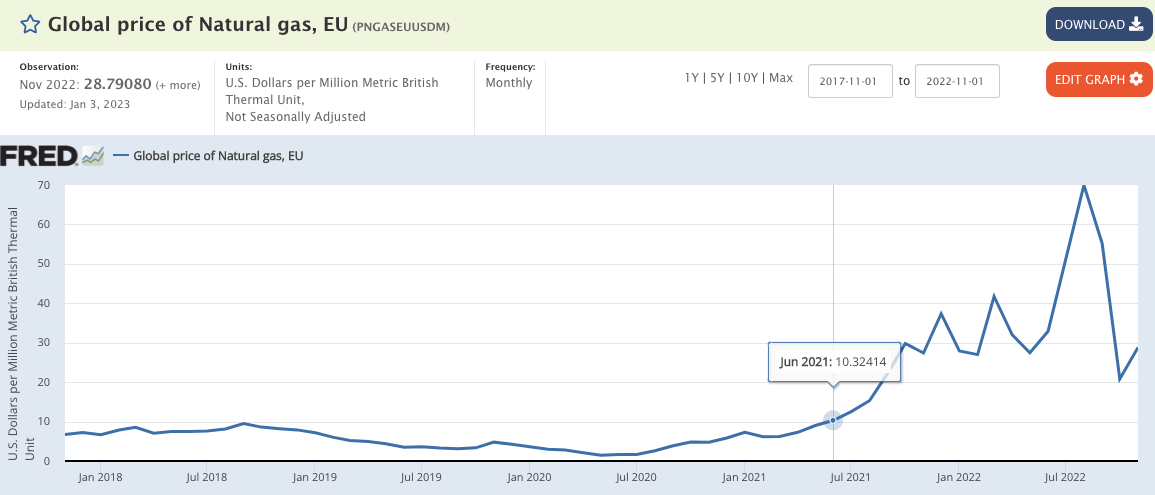

Here at the Lab, today we are back to comment on EU chemical companies with a focus on BASF ( BASFY ) ( BFFAF ). Why? Looking at the worldwide news , we are happy to report that EU gas has finally fallen to the lowest level since Russia's invasion of Ukraine. Consequently, BASF is up by almost 5% today. Although EU gas prices are down considerably from the highs last August (Figure below), we are still considerably higher than the world average costs. Given the fact that the EU still needs LNG and fossil fuels, we are still not too optimistic about the current energy scenario, and we do believe that this situation will continue to be precarious in 2023, just as it was during 2022. For the European chemical industry, gas remains the most significant cost item, bearing in mind that it accounts for about 76% of their bills on average. The positive news is that gas inventories reached a filling level of over 90%, so we believe that the industrial sector shouldn't encounter major problems for the next six months. Here at the Lab, most of the stocks that we are currently covering have shown recovery after hitting lows during 2022 ( Covestro and Evonik ).

{kind=link}

Before moving on with BASF analysis, we should recall that EU chemical companies will continue to produce, buoyed by government grant packages or favorable long-term energy contracts. Indeed, according to our internal estimates, European gas prices will remain high for the next three years due to supply problems. As already mentioned, we are not particularly worried about this winter, but the risks are expected to grow for the two-year period between 2023 and 2024, in which the use of liquefied natural gas will be more strategic.

In the current economic context, the profitability is rather weak for EU chemical companies, and this is especially true in the case of those players involved in the production of ethylene and soda ash. Certainly, this is not the case for all products given the peculiar characteristics of supply and demand, but it is likely that many European companies will record limited profitability in the next 12 months. However, we should also mention that the European chemicals sector's net debt-to-EBITDA ratio will average 0.9x and is well below the 2008/2009 level of 1.4x. Balance sheet and earnings defensiveness are two key topics to be constantly monitored. Looking at the aggregate valuation, the current price/book value average ratio for cyclical stocks is 1.1 times and is greater than 0.8 times recorded during the 2008 financial crisis.

This is due to the fact that chemical companies were able to pass higher costs to their customers with higher selling prices. Here at the Lab, we believe that pricing power is expected to remain strong for next year; however, volume outlook trends look less rosy. We assumed average growth is just 2% for 2023, below 4% compared to the last five years. With consumers grappling with the cost of living increase, we expect a knock-on effect on the volume trend in the final market.

Why BASF?

- BASF recently announced a new €500 million cost-saving plan;

- In October, the company said that its German operations were making a loss. In 2022 first nine months, BASF recorded €2.2 billion higher natural gas costs compared to the same period last year, with this reverse gas trend, the company could revert its depressed EU profitability;

- Still related to point 2) and to support BASF marginality is the fact that many players are opting for de-stocking policies; this could support higher selling prices;

-

Even if BASF admitted that EU demand is decreasing with agriculture and auto exception, we should recall that almost 3/4 of the company's total EBIT is in non-EU countries;

-

Since our last update, the company is up by 8%; however, the German chemical giant is still trading at a discount.

In our Q3 publication, we lowered BASF's Q4 EBIT guidance, and we are below the estimate of Wall Street analysts. However, BASF is still one of our top picks, with a current upside of 21% and a tasty dividend yield of 7%. Valuing the German company with a P/E of 7x, we confirm our €62 per share buy rating target.

The crucial events to closely watch in the coming months are a possible end of the Ukraine conflict, which could lead to an outperformance of cyclical stocks, a convincing response by the EU to the US Inflation Act, and an eventual V-shaped recovery of the Chinese real estate market.

For further details see:

Lower EU Gas Prices, BASF Is Our Top Pick