LQD - LQD: After A Strong Gain Time To Limit Expectations (Rating Downgrade)

2023-12-13 23:46:48 ET

Summary

- The article evaluates the iShares iBoxx Investment Grade Corporate Bond ETF as an investment option at its current market price.

- LQD has seen a really strong move in the short-term and, while welcomed, makes me think caution going forward is appropriate.

- Spreads have narrowed, and other debt sectors offer a stronger relative value. This is important since some of these areas offer similar credit quality as well.

Main Thesis & Background

The purpose of this article is to evaluate the iShares iBoxx Investment Grade Corporate Bond ETF ( LQD ) as an investment option at its current market price. This fund has a stated objective "to track the investment results of an index composed of U.S. dollar-denominated, investment grade corporate bonds".

This is a fund I utilize to give my thoughts on the broader IG-rated corporate bond landscape. It was also an area that I was keen to avoid for most of 2023, but that changed in late summer when it became clear that inflation was (finally) peaking and the Fed could be due for a "pause". Looking back, the timing was pretty good on this call and LQD has indeed offered a strong return since that article was published :

Fund Performance (iShares)

This was certainly a welcome move and pretty strong performance for a defensive asset class in just over four months. The tide seems to have turned and the momentum is back on the side of quality bonds - which is especially notable considering how poorly LQD performed in 2022.

But the challenge here is the outlook going forward. I think it is unrealistic to think LQD is going to keep pumping out such impressive gains and I would advocate not chasing performance here. I think further gains will be much more limited, which is why I believe a downgrade to "hold" makes sense. I will explain the supporting reasons why in detail below.

Spreads Suggest IG Corporates No Longer "Cheap"

To expand on my initial remarks, I want to be clear I am not a bear on bonds right now. This includes IG-rated and junk rated, as I believe fixed-income securities have been long overdue for a rally on the Fed's pause. While I see a path forward that suggests gains will not be as robust as they have been in the short-term, that does not suggest that performance is going to suddenly reverse sharply. This is why "hold" makes sense to me - I see a less favorable backdrop, but not one where big losses should be anticipated.

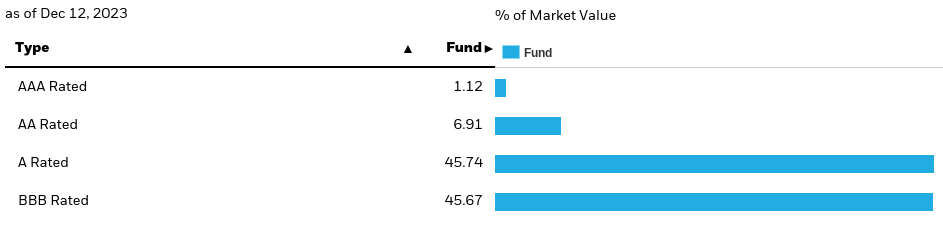

With this in mind, I am evaluating LQD at this point in time. As mentioned, this is a fund that is heavily exposed to IG-rated corporate debt. Over time, this has meant a pretty healthy rating towards corporate issues that are rated BBB, although in fairness just over half the fund is rated above that:

LQD's Credit Quality (iShares)

{kind=link}

Given the quality make-up of this ETF, why wouldn't I remain bullish? The reasoning has less to do with LQD in isolation and more to do with how other debt sectors are looking at the moment.

For instance, IG-rated corporates had yields that were trading above their historical norm a few months back. This made the sector attractive in my view. While yields and spreads are not over-priced, the run-up has altered the dynamic a bit. At present, IG corporates are trading well within their average range now, limiting the return potential going forward. By contrast, other sectors have spreads well above their long-term average. This suggests there may be better value elsewhere:

Current and Historical Spreads (By Sector) (FactSet)

The takeaway for me is that relative value opportunities exist, but LQD is not the option to play it. Rather, investors will find discounted sectors in mortgage debt and other asset backed security sectors. While this one metric alone is not enough to confidently say an investor will get "alpha" through any one particular strategy, it does show that corporate debt issues are not trading at "bargain" levels anymore.

Market Expects (Or Just Wants) Rate Cuts Soon

The next topic to discuss is relevant for LQD, but also for a host of other fixed-income options out there. Of note, many of the same forces that impact IG-rated corporate bonds also impact treasuries, agency MBS, and asset backed securities of similar quality. These sectors tend to have a reasonable correlation with each other, so I want to start off by saying my outlook for the Fed's benchmark rate is relevant for LQD - but other ideas as well.

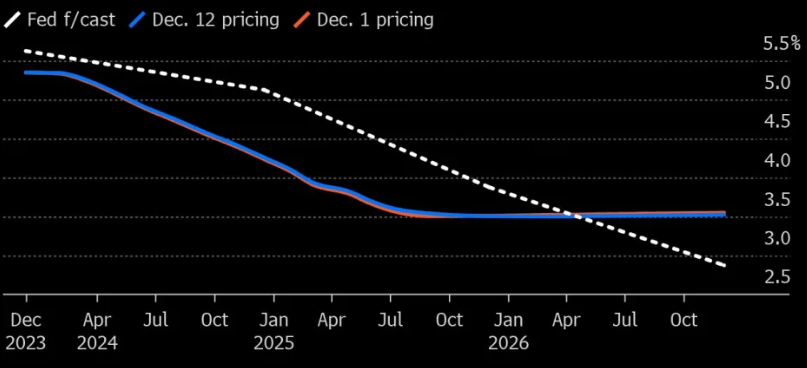

That said, I have growing concerns that market expectations are not going to match reality in 2024. Part of the reason for the surge in bond prices in the last few months is that inflation appears to have peaked and the Fed has resisted any further rate hikes. Beyond those two points, the market is now anticipating rate cuts in mid-2024. This could happen, but I'm of a mind to suggest it won't. That is where myself and the market differ. Furthermore, the Fed has not yet hinted at a timetable for rate cuts, so I am leaning more towards listening to them than to market forecasters who have been wrong for a long time:

Fed vs The Market (rate forecast) (Bloomberg)

{kind=link}

This is another central reason behind my downgrade. The takeaway for me is there is a heightened risk backdrop in that the market may be getting set up for some disappointment. If the Fed does cut rates in mid-2024, then the market is simply getting what it expects and that isn't a huge catalyst for more upside. By contrast, if the Fed doesn't cut, then the market is likely to overreact to the downside.

The bottom-line is I do not like dynamics like that. I prefer a risk-reward proposition that leans more towards reward, not risk. I don't see that with fixed-income IG corporates at this juncture, and that supports my downgrade for LQD at the recent boost in share price.

Corporate Earnings Suggest Little Credit Risk

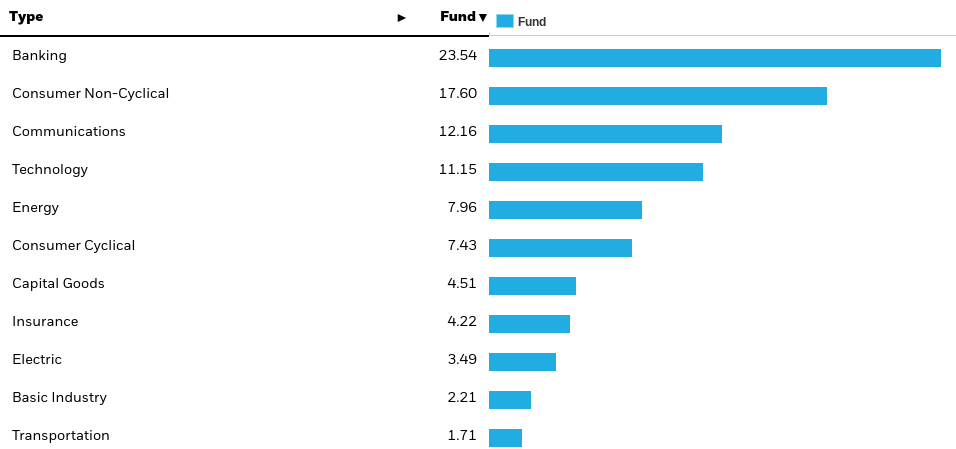

To balance out this review, I want to touch on one of the strongest reasons for staying invested in US corporate debt. As a reminder, LQD owns securities backed by mostly large-cap US companies. In fact, it holds debt from some of more traditional, cash-heavy sectors such as Banking, Consumer Staples, and Communications, but is also very diverse as a whole:

LQD's Sector Breakdown (iShares)

{kind=link}

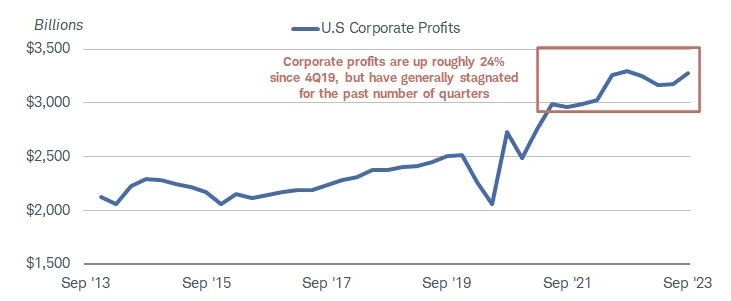

So this type of investment is really a bell-weather ETF for corporate America. If companies are performing well - as they have been - then it stands to reason they are going to make good on their credit obligations. Over time, IG-rated corporate debt tends to have a fairly low default rate. Given how earnings have been strong (on average) over the past few years, this is a trend I expect to continue:

US Corporate Profits (Aggregate) (Charles Schwab)

{kind=link}

The conclusion I draw here is that the stability offered by US corporates in terms of credit quality remains intact going in to the new year. This may be a bit of a stretch argument for junk bonds, but for IG-rated issues "safety" is still a word I would use here. This remains a more defensive, income-oriented play and that is something that is going to draw investor interest in 2024. While the short-term opportunity is limited in my view, there is still a case to be made for holding (or even buying) this sector through a fund such as LQD.

Bottom-line

Bonds have had a nice pop and today's (12/13) comments in the Fed Chairman Powell's speech added fuel to the fire. That could mean more momentum is on the way and further gains are ahead of LQD. It's certainly a possibility that readers need to assess.

But I tend to become much more careful when defensive sectors (such as investment grade bonds) see large swings in a short time period. That usually suggests the go-forward return will be less spectacular and I believe that will be the case here as well. While LQD has some tailwinds, such as the potential for Fed cuts in 2024 and declining inflation, the reality is that other fixed-income sectors are offering a stronger value at the moment. With this backdrop it makes sense to me to change my rating to "hold", and I recommend to my followers that approach any new positions carefully at this time.

For further details see:

LQD: After A Strong Gain, Time To Limit Expectations (Rating Downgrade)