LQDH - LQDH: What Explains The ETF's Outperformance?

2023-10-21 00:29:33 ET

Summary

- The iShares Interest Rate Hedged Corporate Bond ETF tracks a diversified portfolio of U.S. dollar-denominated investment grade corporate bonds.

- The fund hedges out interest rate risk by owning the iShares iBoxx $ Investment Grade Corporate Bond ETF and a portfolio of interest rate swaps.

- The LQDH ETF has delivered strong returns in the past year, but investors should not expect the same level of returns going forward.

Recently, I wrote an article on the Invesco Variable Rate Investment Grade ETF ( VRIG ), arguing the risk/reward in floating rate investment grade credit is not attractive at the moment. While looking at comparable funds for the VRIG ETF, I came across the iShares Interest Rate Hedged Corporate Bond ETF ( LQDH ).

On paper, the two funds are very similar, as they both provide floating rate exposure to investment grade corporate bonds. However, LQDH has a 1-year total return of 11.6% vs. 6.9% for the VRIG ETF. Does LQDH have a 'secret sauce' that can explain the large performance gap between the two funds?

I believe the short-term performance gap between LQDH and VRIG can be attributed to LQDH's fund structure. LQDH hedges interest rate risk via interest rate swaps. As short-term interest rates rise, these swaps accrue mark-to-market ("MTM") gains, which have boosted LQDH's total returns. However, over a cycle, MTM gains and losses should net out and LQDH's long-term returns are similar to VRIG's.

Looking forward, I caution LQDH investors against expecting double digit total returns, as the same magnitude of MTM gains are unlikely to repeat. In fact, if short-term interest rates stay unchanged, the value of LQDH's swaps should amortize and act as a headwind.

With credit spreads near 1-year lows, I find the risk/reward in LQDH unappealing at the moment and rate the fund a hold .

Fund Overview

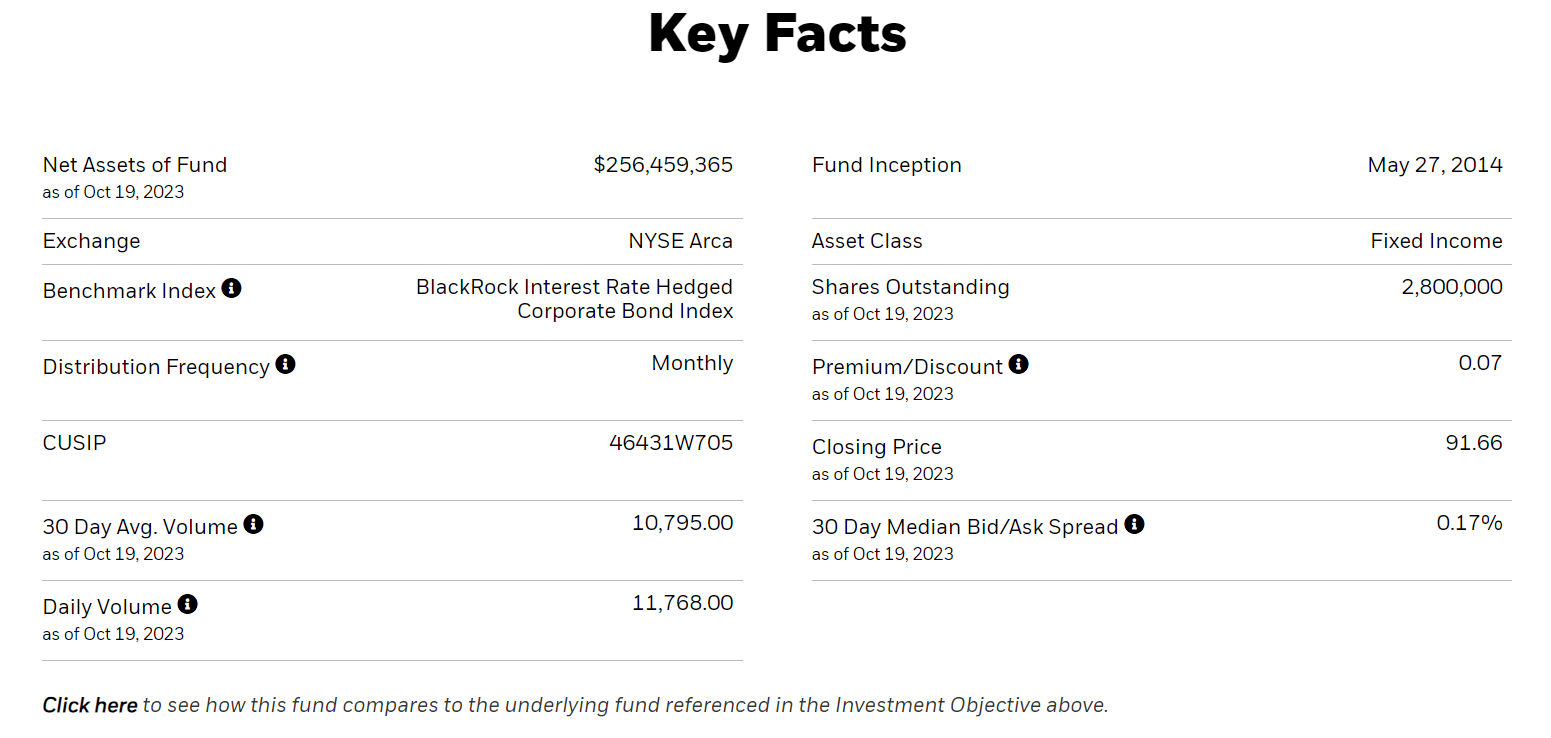

The iShares Interest Rate Hedged Corporate Bond ETF tracks the returns of a diversified portfolio of U.S. dollar-denominated investment grade corporate bonds. The LQDH ETF charges a net expense ratio of 0.24%, contractually fixed until February 2027 after fee waivers of 0.20% and has $256 million in assets (Figure 1).

{kind=link}

Strategy

The LQDH ETF tracks the BlackRock Interest Rate Hedge High Yield Bond Index ("Index"), an index designed to minimize the interest rate risk of a portfolio of U.S.-dollar denominated investment grade ("IG") corporate bonds.

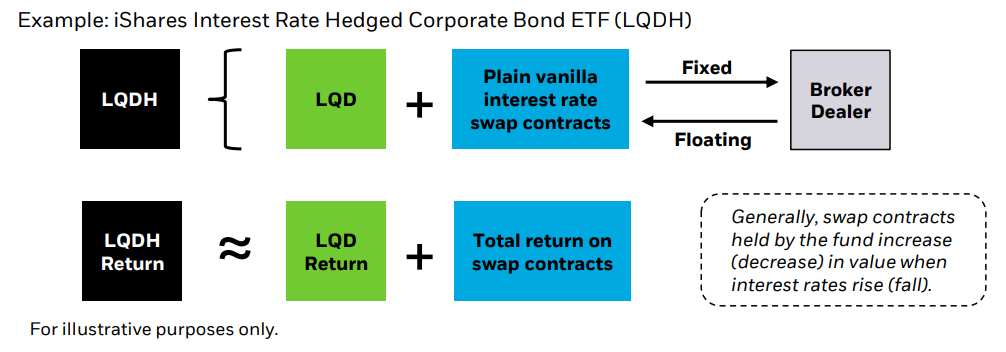

The fund achieves its objective by basically owning the iShares iBoxx $ Investment Grade Corporate Bond ETF ( LQD ) and a portfolio of interest rate swaps to hedge out interest rate exposure (Figure 2). In effect, investors in the LQDH ETF has exposure to the returns of the LQD ETF plus the total returns on the swap contracts. In general, these interest rate swaps increase in value when interest rates rise.

{kind=link}

The main purpose of the LQDH ETF is to mitigate interest rate risk of owning the LQD ETF, allowing investors to express their views on the credit risk of IG corporate bonds.

Portfolio Holdings

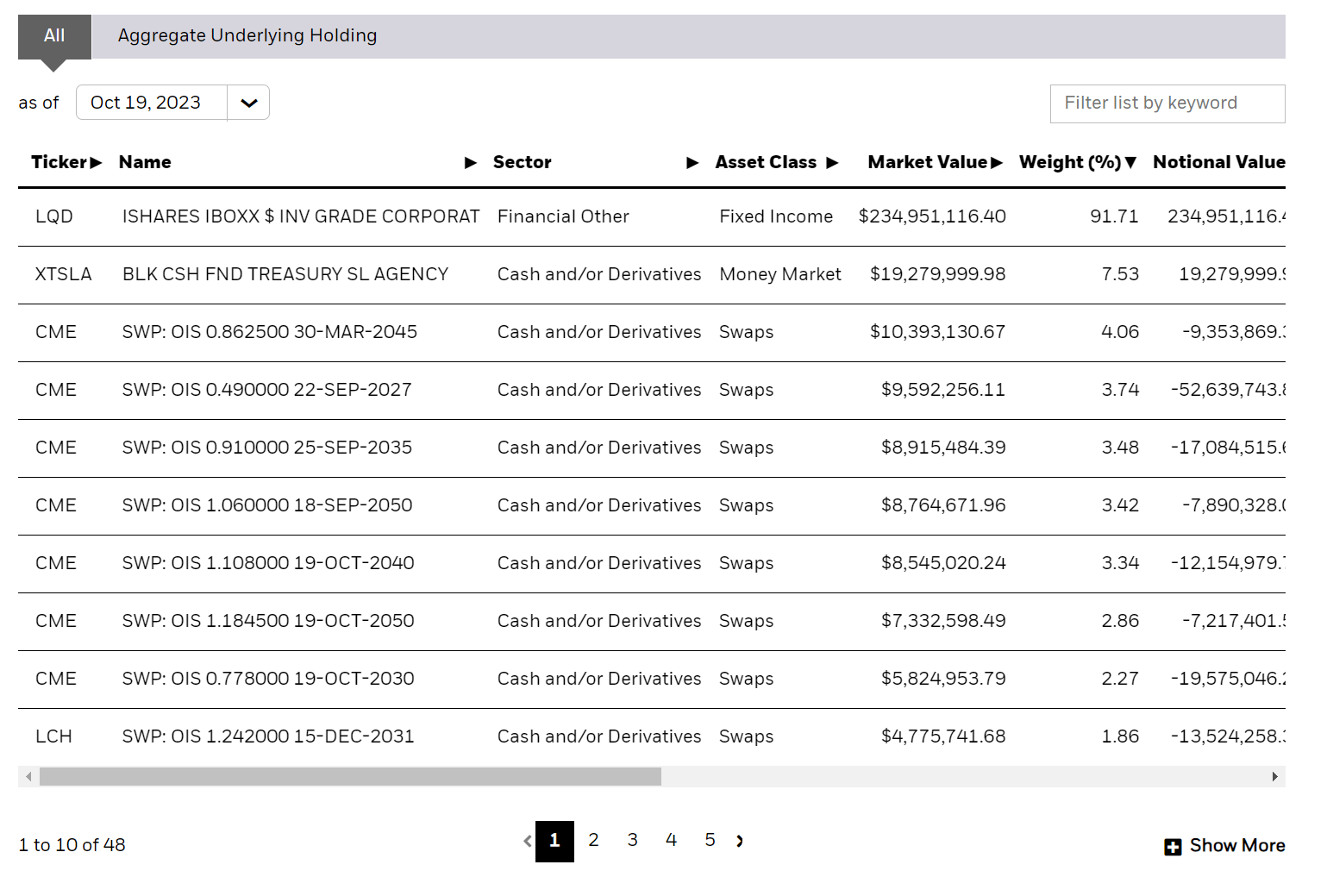

As mentioned above, the LQDH ETF holds the LQD ETF and a portfolio of interest rate swaps to hedge interest rate risk (Figure 3).

{kind=link}

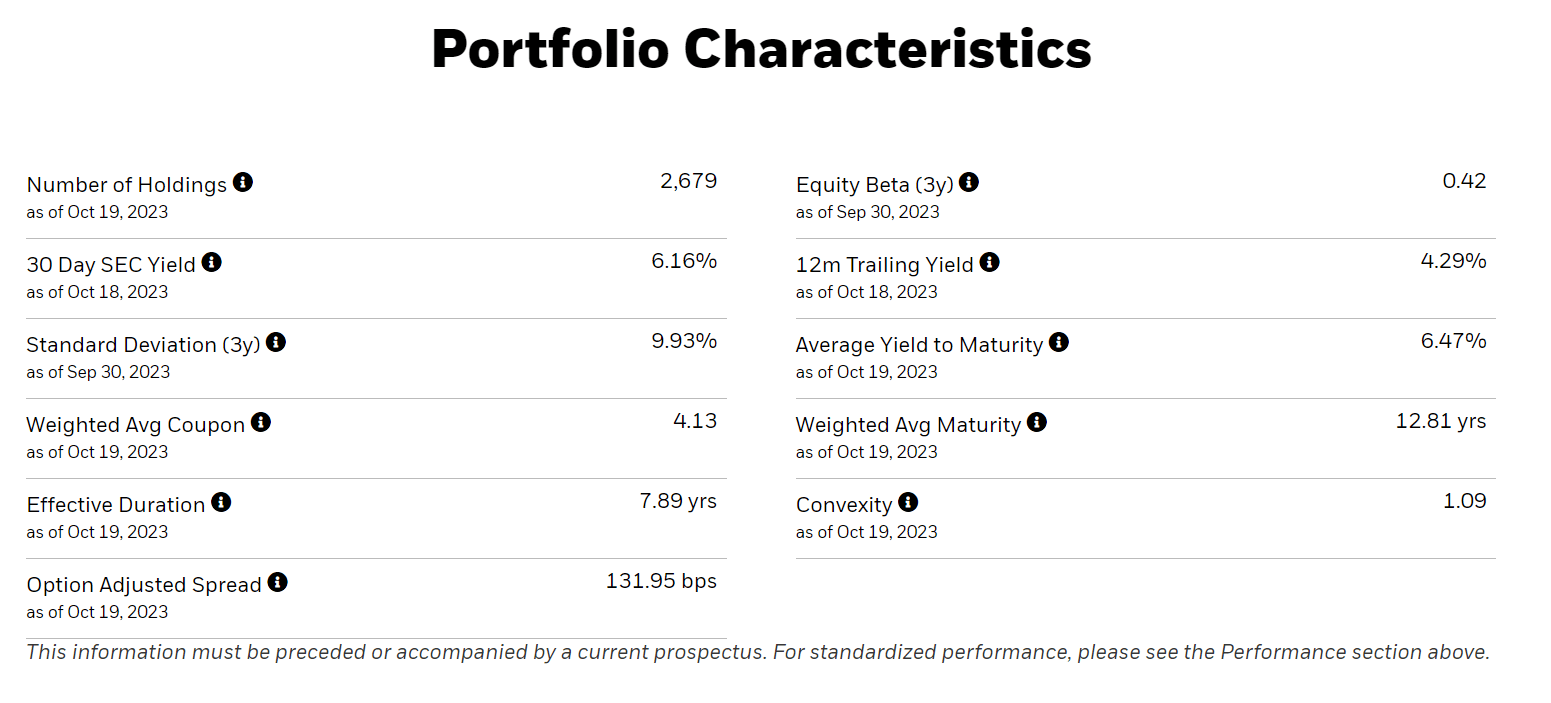

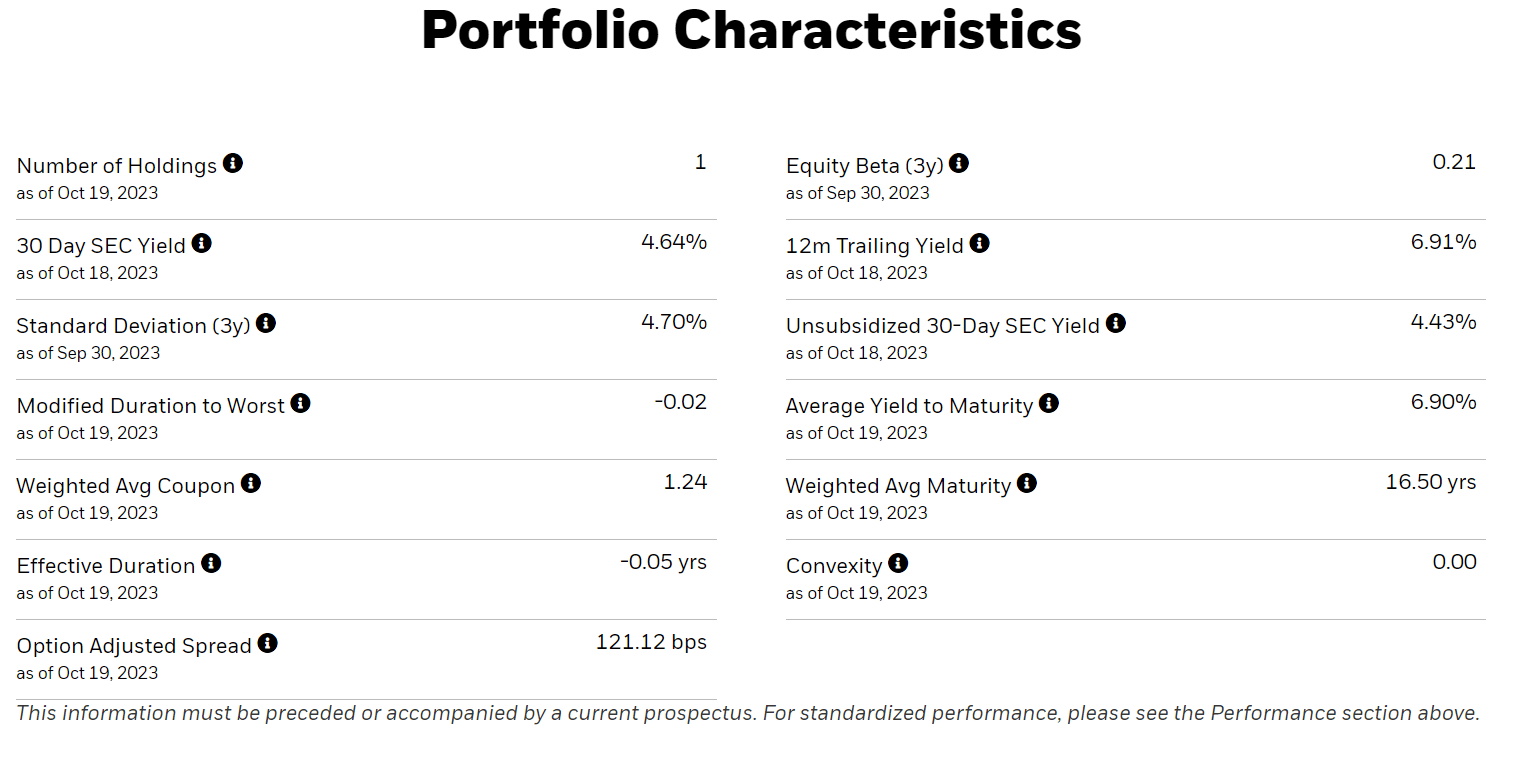

The LQD ETF is a broadly diversified passive ETF of investment grade corporate bonds with over 2,600 securities and a portfolio effective duration of 7.9 years (Figure 4). LQD has a 30-Day SEC yield of 6.2%.

{kind=link}

By hedging away interest rate risk via interest rate swaps, the LQDH ETF transforms the portfolio into zero effective duration and a 30-Day SEC yield of 4.6% (Figure 5).

{kind=link}

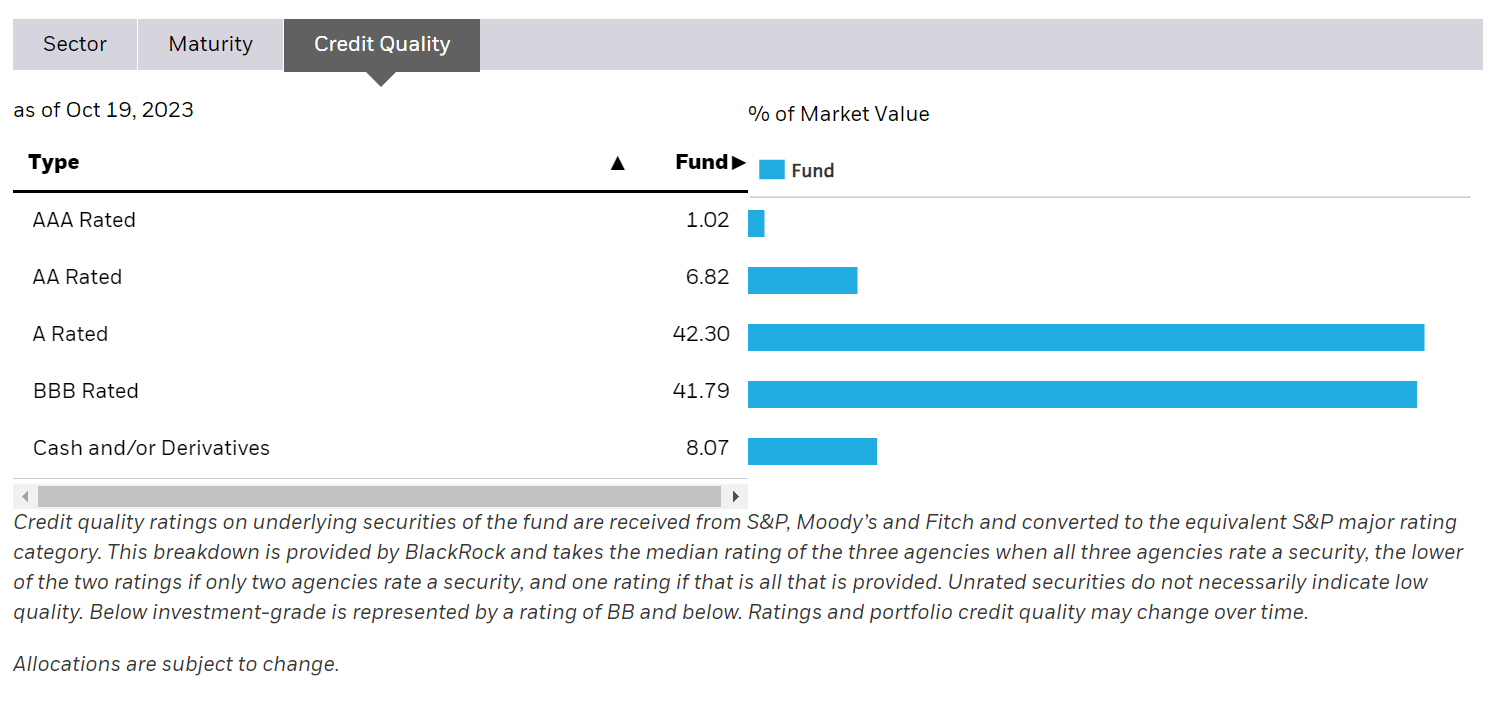

LQDH's credit quality allocation is basically a readthrough of the underlying LQD ETF, with 42.3% allocation to A-rated securities, 41.8% allocation to BBB-rated securities, 6.8% allocation to AA-rated, and 1.0% allocated to AAA-rated (Figure 6).

{kind=link}

Distribution & Yield

The LQDH ETF paid a trailing 12 month distribution of $6.34 or 6.9% yield (Figure 7).

{kind=link}

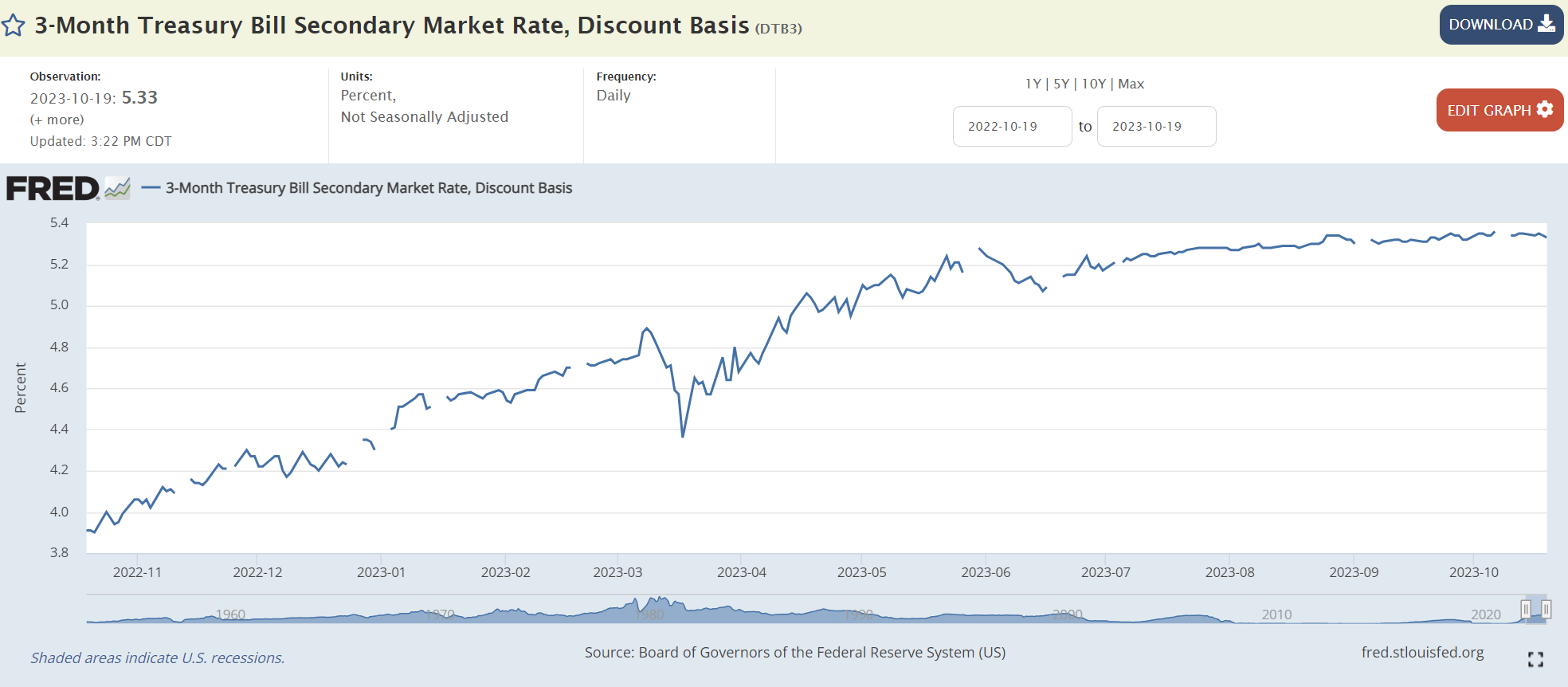

The way to think about LQDH's distribution is to recognize that LQDH's strategy has transformed fixed rate cash flows from the LQD ETF into floating rate cash flows with interest rate swaps. So conceptually, LQDH's yield should be a short-term interest rate, for example, the 3 month treasury bill yield, plus IG credit spreads of ~1.5%. With 3 month treasury bills yielding 5.3%, the LQDH ETF should be paying ~6.5% distribution yields (Figure 8).

{kind=link}

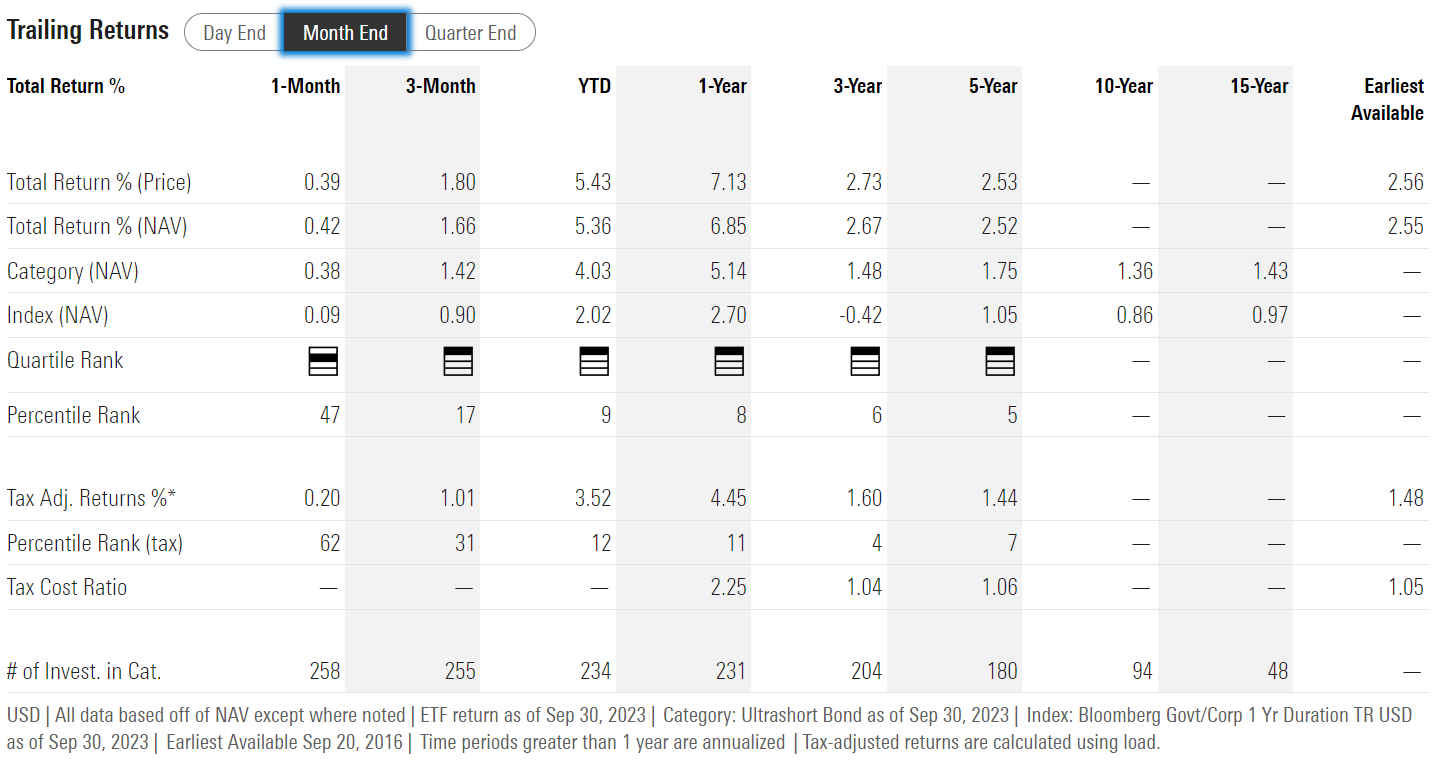

Returns

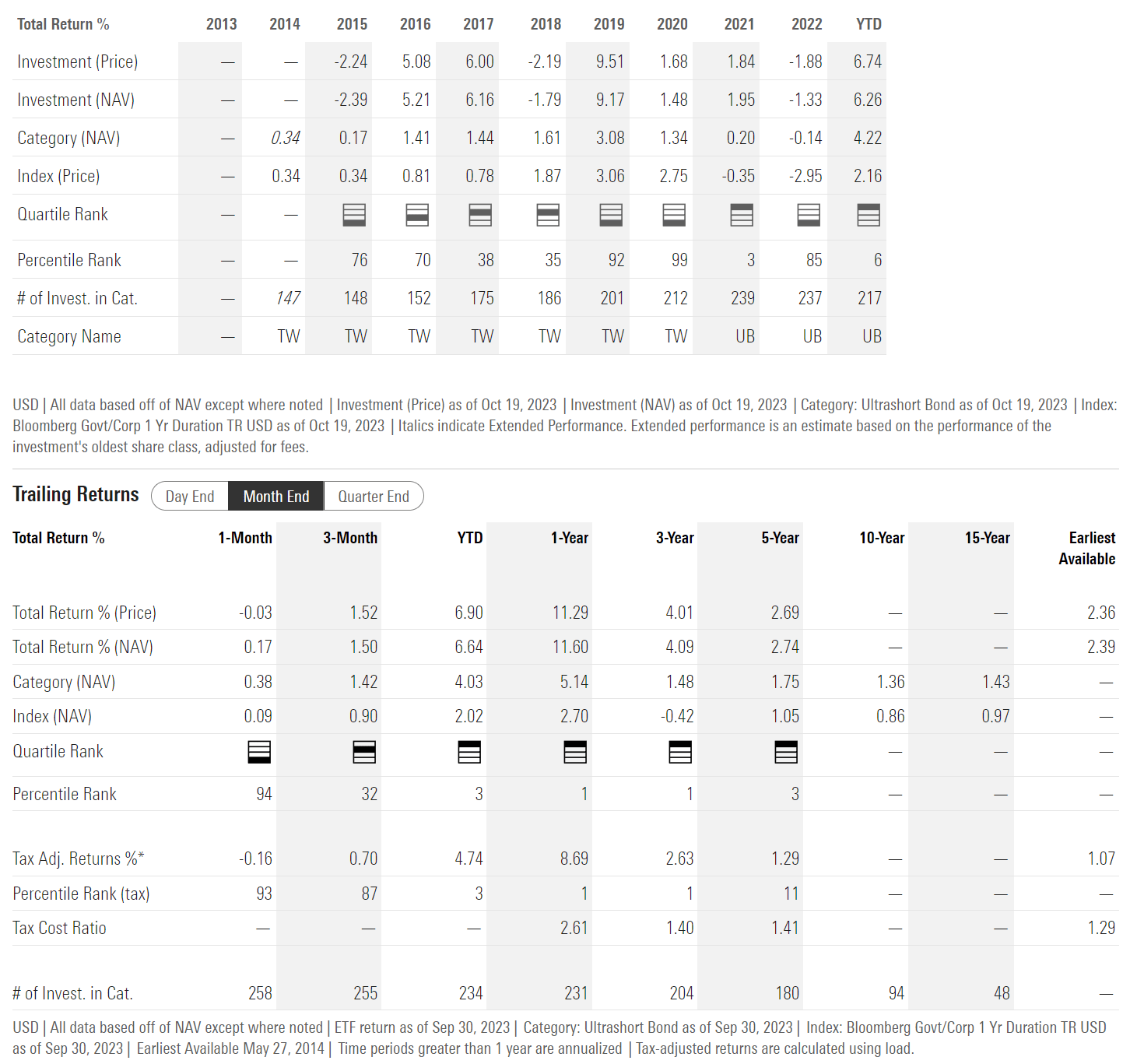

Figure 9 shows the historical returns of the LQDH ETF. As explained above, since the LQDH ETF hedges out interest rate risk, long-term returns of the LQDH ETF can be thought of as short-term interest rates plus IG credit spreads less fund expenses.

{kind=link}

However, surprisingly, the LQDH ETF has delivered strong returns in the past year to September 30, 2023 of 11.6%. This is far above what can be expected from floating rate investment grade credit. For example, the Invesco Variable Rate Investment Grade ETF ("VRIG") invests in floating rate investment grade bonds, but have only returned 6.9% in the past year (Figure 10).

{kind=link}

VRIG's 6.9% 1 year return is similar to LQDH's distribution yield and is the expected return of floating rate investment grade credit, as I explained above. So what explains the difference between LQDH and VRIG's trailing 1 year returns?

Interest Rate Swaps Have Unrealized Gains / Losses

I believe the difference between LQDH and VRIG's return can be attributed to LQDH's strategy/structure. Recall from Figure 2 above, LQDH's strategy is derived from owning the fixed rate LQD ETF plus a portfolio of interest rate swaps to hedge out interest rate risk. Interest rate swaps are derivatives that transform a series of cash flows from fixed to floating rate.

As the payer of fixed rate cash flows / receiver of floating rate cash flow, LQDH records a mark to market ("MTM") gain when short-term interest rates rise. So the difference between LQDH and VRIG's 1 year total return is mostly the MTM gain of its portfolio of interest rate swaps.

Over a cycle, the rise and fall in interest rates should net out. That is why LQDH's 5 year average annual return of 2.7% is similar to VRIG's 5 year average annual return of 2.5%. However, in the short run, increases and declines in interest rates can cause performance to diverge between LQDH and VRIG.

Don't Expect 11% Returns Going Forward

Looking forward, unless short-term interest rates continue to rise at a similar pace as they have in the past year, investors in LQDH should not expect 11% forward returns. In fact, since LQDH has recognized a MTM gain on its interest rate swaps from a rise in short-term interest rates, if interest rates stay unchanged going forward, then the MTM gain should amortize as time passes.

Risks To LQDH

I see two risks with owning the LQDH ETF. First, as the Federal Reserve nears the end of its current rate hiking cycle, many analysts are looking forward and expecting the Fed to begin cutting short-term interest rates sometime in 2024 (Figure 11).

{kind=link}

Since the LQDH ETF receives floating rate cash flows, if short-term interest rates decline, then the LQDH ETF's returns will scale lower. Moreover, as we discussed above, part of LQDH's total returns include MTM gains and losses from its portfolio of interest rate swaps. If short-term interest rates decline, these swaps will record MTM losses.

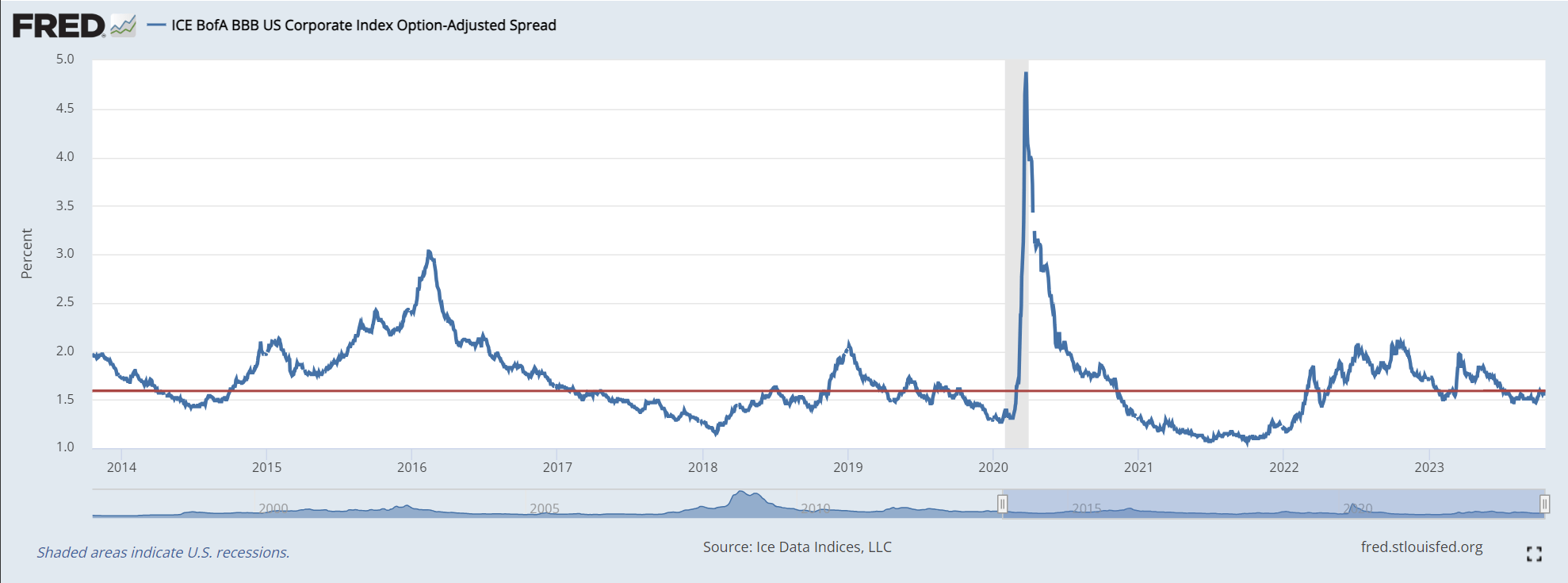

The LQDH ETF is also sensitive to credit risk. If the economy were to weaken and credit spreads widen, then that will have a negative MTM impact on the LQDH ETF. Currently, investment grade credit spreads are near 1-year lows and do not offer attractive risk/rewards (Figure 12).

Figure 12 - Investment grade credit spreads are near 1 year lows (St. Louis Fed)

{kind=link}

Floating Rate Investment Grade Credit May Not Be The Best Place To Be

As I noted in my VRIG article, floating rate investment grade credit may not be the best place to be at the moment. If one is bullish on the economy, then high yield markets should outperform investment grade, and investors should consider high yield investments like the iShares Interest Rate Hedged High Yield Bond ETF ( HYGH ) or the Invesco Senior Loan ETF ( BKLN ).

On the other hand, if investors believe the economy will weaken, then they should consider credit-risk free treasury bill funds like the iShares 0-3 Month Treasury Bond ETF ( SGOV ) or even take on duration risk with the LQD ETF, as a weaking economy may prompt the Federal Reserve to cut interest rates.

With forward returns of ~6% (short-term interest rates plus credit spread), I believe floating rate investment grade credit funds like LQDH simply does not offer a compelling risk/reward at the moment.

Conclusion

The iShares Interest Rate Hedged Corporate Bond ETF offers investors interest-rate hedged exposure to investment grade corporate bonds. Although the fund has delivered strong 11.6% 1 year returns, a large part of the return is derived from MTM gains on interest rate swaps that may not be repeatable.

I find forward returns for floating rate investment grade credit funds like LQDH unappealing at the moment since credit spreads are near 1-year lows. If investors are bullish the economy, they should consider high yield bond funds that can offer higher returns.

Alternatively, if investors are bearish the economy, they may want to invest in credit-risk free treasury bills and potentially take on duration risk if they expect the Federal Reserve will cut interest rates. Personally, I remain sceptical the Federal Reserve will be able to achieve a 'soft-landing' so I have been biding my time in the safety of treasury bills, waiting for better valuations to buy assets for the long-term.

I rate the LQDH ETF a hold .

For further details see:

LQDH: What Explains The ETF's Outperformance?