LQDH - LQDH Will Likely Underperform In A Decreasing Rate Environment

2023-03-28 04:57:00 ET

Summary

- The iShares Interest Rate Hedged Corporate Bond ETF is a fixed-income exchange-traded fund.

- The vehicle seeks to track the investment results of an index designed to mitigate the interest rate risk of a portfolio composed of U.S. dollar-denominated, investment-grade corporate bonds.

- We are closing in on peak rates, with the Fed Funds curve implying cuts later this year and in 2024.

- LQDH will underperform its sister fund LQD in a decreasing rate environment due to its interest rate swaps.

- The vehicle did very well in 2022 when rates were rising but is now set to be dragged back by its structure.

Thesis

The iShares Interest Rate Hedged Corporate Bond ETF ( LQDH ) is a fixed income exchange traded fund. The vehicle is a hedged version of the very popular investment grade bond fund iShares iBoxx $ Investment Grade Corporate Bond ETF ( LQD ). The name is also reflective of this composition, representing a LQD-' H edged'.

The fund has done very well in the past year, being down only -2.4%, versus -8.9% for LQD. The performance is achieved via the layering in of interest rate swaps, which gain in value as rates move higher. The opposite effect happens when rates decrease - LQDH will lose value versus a pure LQD position as rates move down.

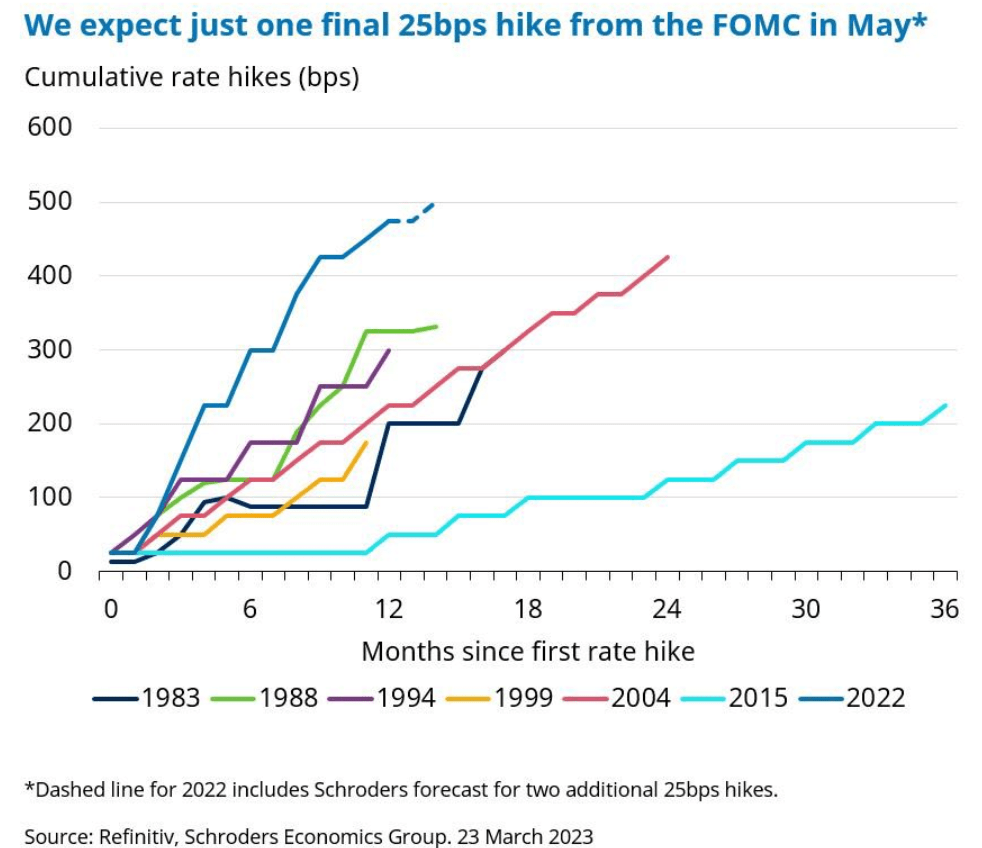

We have had a very violent rise in rates, an almost unique one in recent history:

{kind=link}

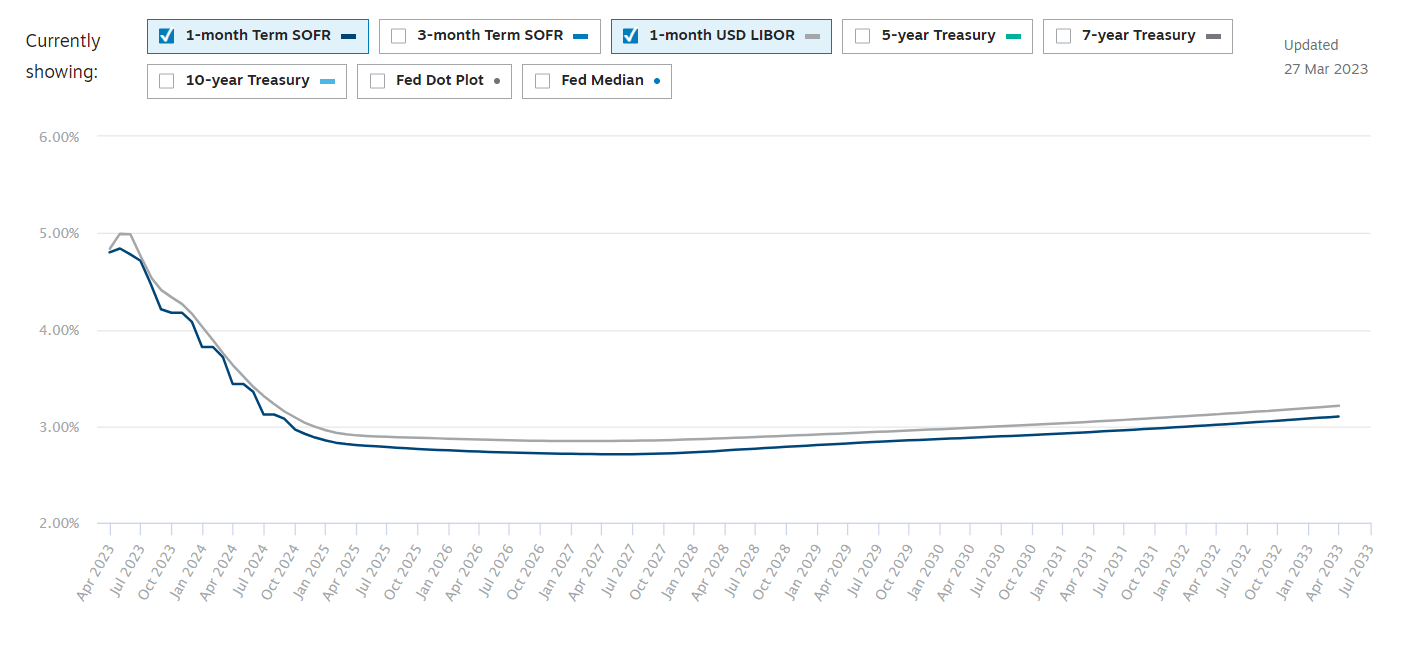

While nobody knows for sure how many rate hikes are left, it is safe to assume we are nearing the end of the rate cycle. While many pundits are predicting a higher for longer rates environment, the SOFR / Libor markets are predicting cuts as early as this year:

{kind=link}

We can see how the SOFR curve has priced in a massive reduction in rates this year - the current futures show a 4% SOFR rate at year end! That is a massive change from two weeks ago, when the year end rate was much closer to 5% than 4%. The regional banks crisis has taken its toll on the monetary tightening cycle, with market participants pricing in fundamental direct credit tightening given the issues experienced by banks' balance sheets and their need for liquidity.

What happens when rates move down?

Given the inverse relationship between bond prices and interest rates, we expect LQD to go up in value later this year if rates do move down, while the interest rate swaps present in LQDH will lose value, thus dragging performance.

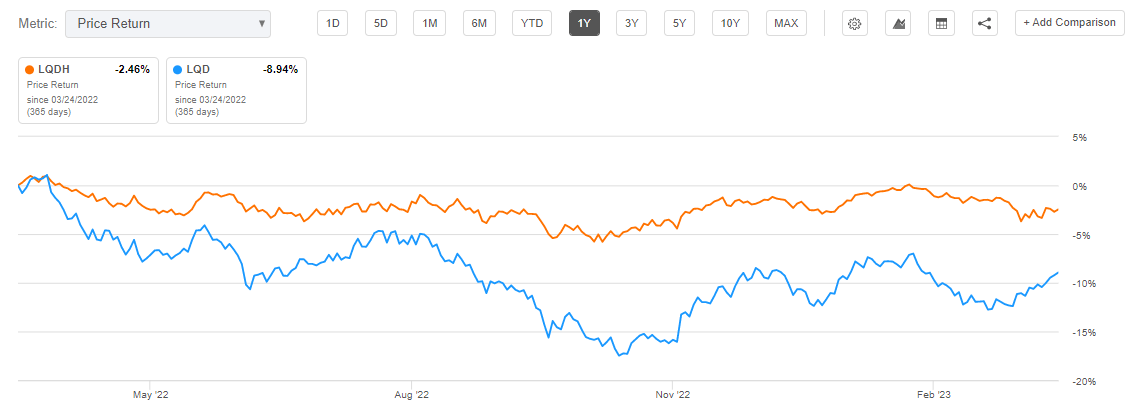

In the same fashion LQDH outperformed during 2022, it will underperform once rates start moving down:

{kind=link}

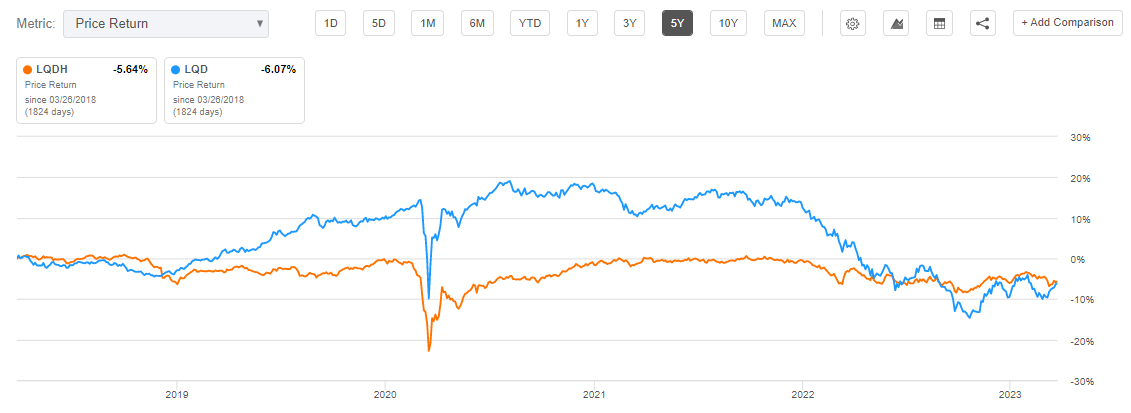

We can clearly see from the performance graph above how LQDH kept a steady NAV while LQD was losing value due to rising rates in 2022. Long term though, LQD exposes a better total return, particularly during lower rates:

{kind=link}

LQD runs a high duration profile, and we can see from the above table how it gained value as rates moved to zero post the Covid crisis. Conversely, LQDH is almost flat duration, thus its performance was very muted during 2021.

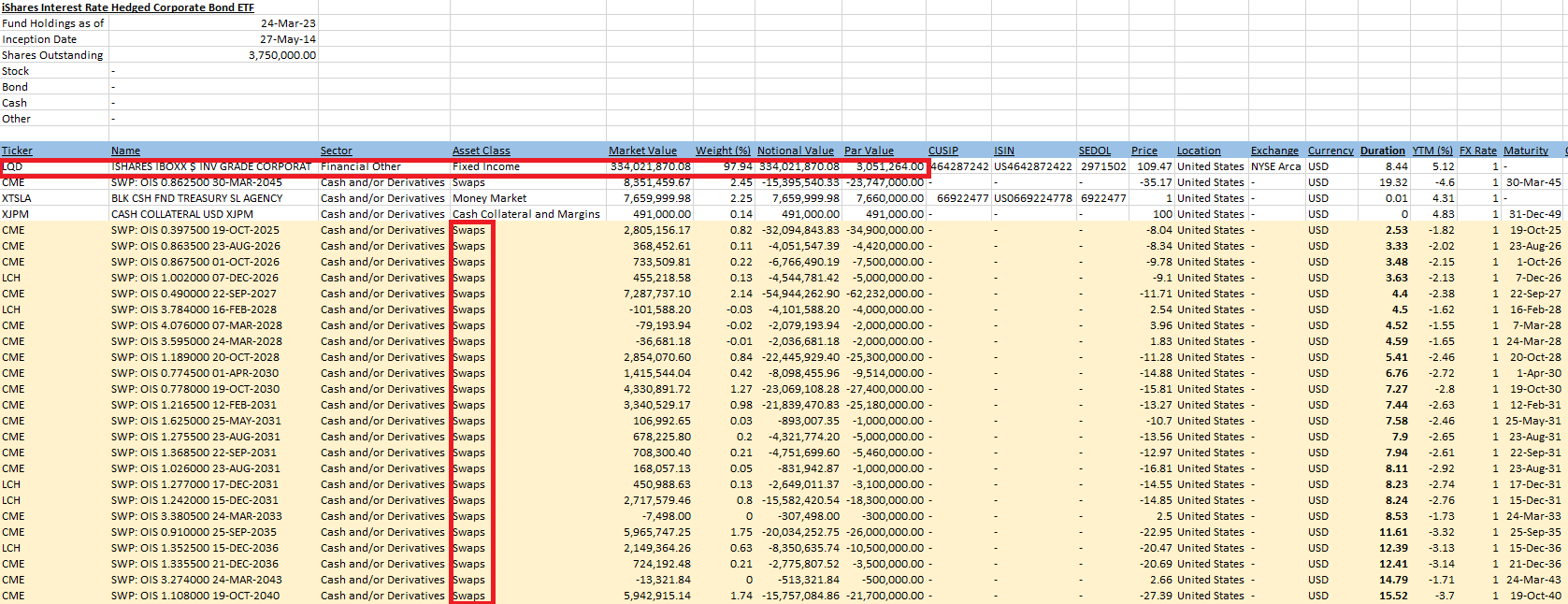

LQDH Holdings

The fund has a large position in LQD, and a laddered interest rate swap portfolio:

{kind=link}

The proper way to hedge an investment grade bond portfolio is via a laddered approach. This means that a manager decomposes the portfolio and creates a PV01 profile:

PV01 of a portfolio of assets is the sensitivity of the total scheme assets to a one basis point (or 0.01 per cent) change in interest rates (spot curve if available; otherwise, par curve)

Once you have a tenor bucketed PV01 profile then you can layer in equivalent interest rate swaps that mitigate the interest rate sensitivity. You can observe from the above table for example that the notional of the swaps with a 2027 maturity is much higher than the ones for 2028. That means there are more bonds maturing around that time frame than in 2028, so the portfolio manager had to hedge accordingly.

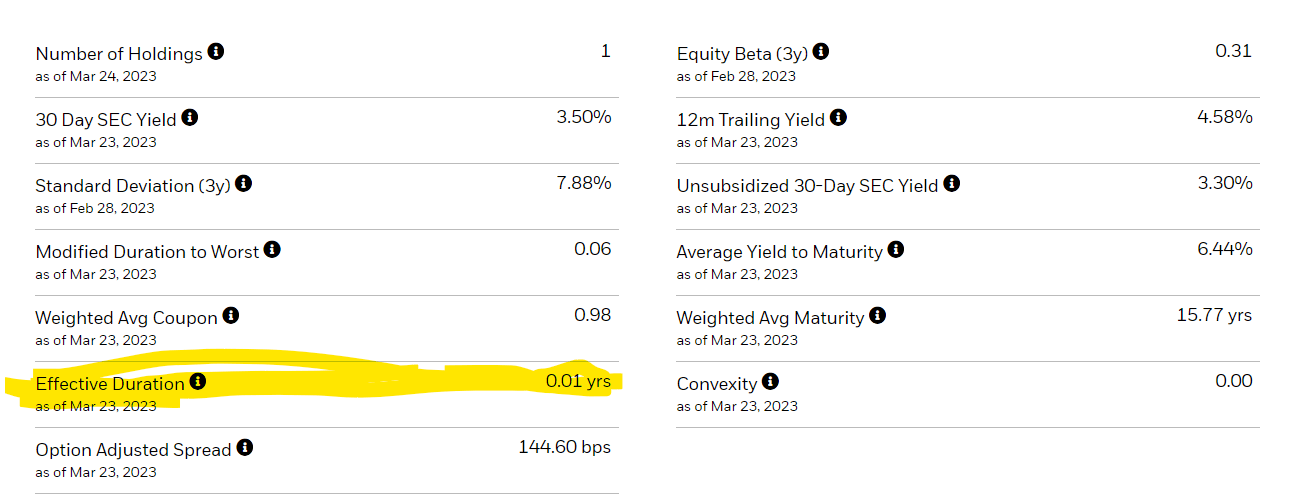

The hedging out of the interest rate component creates a flat duration profile for the fund:

Duration Profile (Fund Website)

{kind=link}

At present, LQDH's performance is driven mostly by the credit spread on the underlying portfolio - if the spreads widen, LQDH loses value. If spreads tighten, LQDH gains.

Conclusion

The iShares Interest Rate Hedged Corporate Bond ETF is a fixed income exchange traded fund. The fund takes a large position in the LQD ETF (i.e. a portfolio of investment grade bonds) and hedges out the interest rate risk via swaps. LQDH has a flat duration profile, and has outperformed in 2022 as rates have risen violently. Currently the fund represents a long position in investment grade bonds credit spreads, and is set to lag LQD significantly in a decreasing rates environment. Lower rates will have a massive positive NAV impact to a long duration fund like LQD. Due to the regional banks crisis, the SOFR curve now prices in several rate cuts for 2023, indicating the market is expecting lower rates soon. If the market expectations are fulfilled LQDH will lag significantly.

For further details see:

LQDH Will Likely Underperform In A Decreasing Rate Environment