LQD - LQDW Has Been Underperforming But It May Be Salvageable

2023-11-13 04:17:38 ET

Summary

- iShares Investment Grade Corporate Bond BuyWrite Strategy ETF aims to generate high yields by writing covered calls on investment grade corporate bonds.

- The fund has underperformed its underlying assets even when it theoretically should have outperformed, highlighting the limitations of covered call strategies in volatile markets.

- Investors can potentially improve returns by converting the fund to a covered call spread fund or by buying a mix of LQD-LQDW for high yield and upside participation.

iShares Investment Grade Corporate Bond BuyWrite Strategy ETF ( LQDW ) is a covered call fund that tries to generate outsized yields by writing covered calls on investment grade corporate bonds. Currently corporate bonds yield about 6-7% and this fund hopes to add another 10% to it by writing covered calls and it offers a dividend yield of 16-17% range.

This fund is relatively new and it was created last year with two ongoing trends in mind. First, covered call funds have been getting hugely popular with investors who don't mind trading some upside in return of receiving premiums which can create double-digit dividend distribution yields. The second trend is the implosion of the bond market we've seen in the last 2 years where bonds are still in a bear market, driven by both rising inflation itself as well as the Fed's actions to curtail this inflation. As a result of this, bonds are now down about -21% in the last 3 years.

You'd think that selling covered calls on bonds would generate good returns and beat the bond market averages but it hasn't been happening either. The idea is that when you sell covered calls on an asset that's either flat or in a downslide, you should outperform it because you are collecting premiums to cushion the fall. For example if you have a stock that sells for $100, and you write covered calls on this stock for a whole year and collect $10 in premiums throughout the year, in theory you should come ahead if the stock is down, flat or rose less than $10 because of the premiums you've collected but in real world things work a bit differently. Market's don't go straight up, straight down or just stay flat.

Let me give you one concrete example of this before getting back to LQDW. The S&P 500 index ( SPY ) virtually stayed flat for 2.5 years between April of 2021 and October of 2023. This should be a period where (at least in theory) writing covered calls on SPY should vastly outperform the index. We have Global X S&P 500 Covered Call ETF ( XYLD ) which is a fund that sold monthly covered calls during this period and it certainly didn't outperform even after adding the 10-12% dividend yield that fund distributed during this time. During this 2.5 year period SPY was virtually flat and the fund's total return was just as flat. What causes this? When you write covered calls you limit your upside but you participate in most downside movements and markets rarely go up or down in a straight line. There are a lot of W shaped movements in the market and these can cause quite a bit of NAV decay in covered call funds.

Now we are seeing something similar with LQDW as well. Since this fund's inception a year ago, investment grade corporate bonds had a total return of -3.15% while this fund had a total return of -4.67% which means it slightly underperformed a fund that was sliding down even after writing covered calls against it. This is something many people wouldn't expect to see. When you look at the below chart, look at how bonds performed so well from October 2022 and February 2023 whereas this fund failed to capture most of it because its upside was capped. Another example is the far right side of the chart showing the last 2 weeks where bonds had a strong rally but this fund didn't capture any of it because that's how covered call funds are.

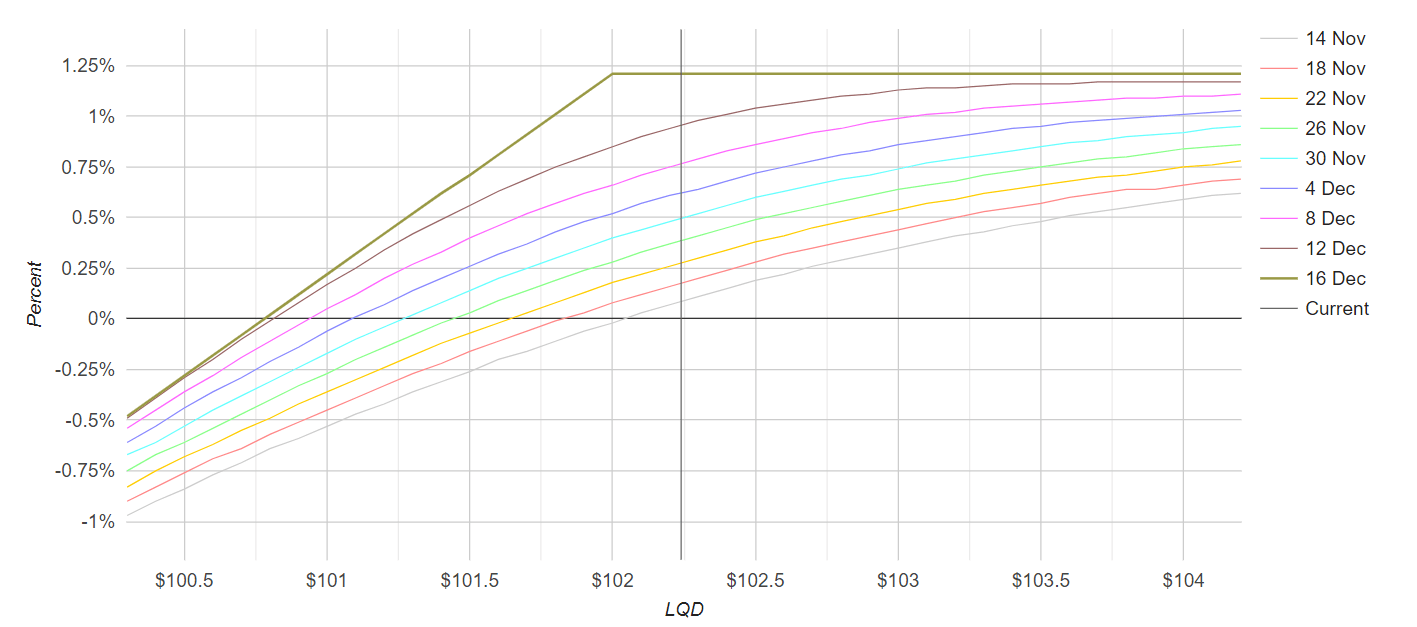

Perhaps the fund would be better off if it sold covered call spreads instead of covered calls. That way it would capture some of the upside that comes suddenly when no one was expecting. Below is how writing a monthly covered call on LQD would go in terms of profits and losses which is exactly what the fund currently does. Notice that any upside above 1.25% is capped which means if bonds were to suddenly jump 3-4% like they often do, the fund would miss out on that.

{kind=link}

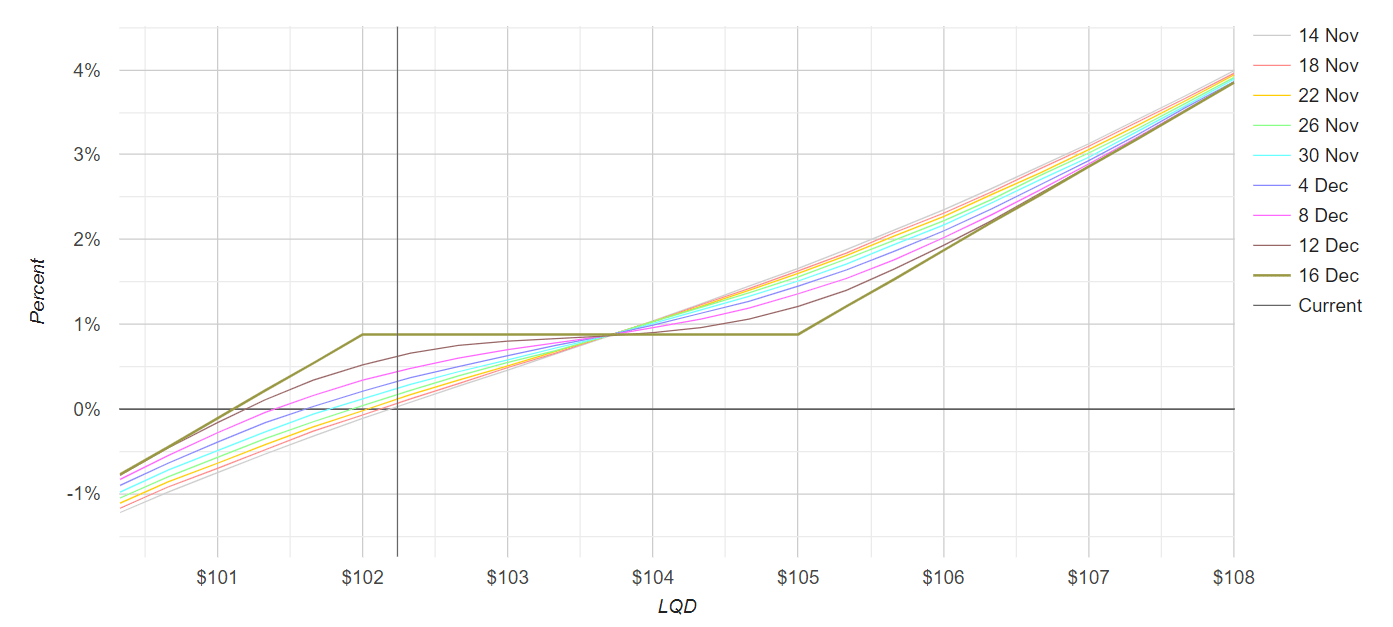

Now compare it to writing covered call spreads. It looks like the fund collects less premiums but it gets to participate in outsized returns. Now the fund is collecting a net premium of 1% instead of 1.25% so it's making a 0.25% sacrifice but it gets to participate in potential upside movements which would limit NAV decay greatly.

Covered Call Spread Profit Profile (optionsprofitcalculator.com)

{kind=link}

I am not saying that the fund itself should necessarily do this. Investors can easily do this themselves. You can buy and hold LQDW as usual but just add some LQD call options to the mix to protect yourself from a possible NAV decay. You'll be sacrificing some of your dividend yield but you will likely be better off in the long term especially if bonds suddenly decide to have a rally in response to slowing inflation. Luckily LQD options are very cheap because it's implied volatility is very low so you can buy those options to protect yourself against NAV decay. Some investors also buy put options to protect their portfolio but I am not too worried about bond prices dropping much more from here so I wouldn't go that far.

Investors shouldn't expect too much from this fund because it didn't even outperform its underlying ( LQD ) under conditions where it theoretically should have outperformed. Still, investors don't need to short it or sell it either. You can possibly salvage this fund and improve its returns by simply converting it from a covered call fund to a covered call spread fund by simply adding out-of-money LQD call options to the mix. You'll be sacrificing some of those rich 16-17% yields but possibly be better for it in the long run if and when bond prices start recovering.

Markets never go straight up and down which makes it very difficult for covered call funds to outperform their underlying even when conditions might seem favorable for them (a market that's down, flat or range-bound). This is especially true if the fund sells options right at the money or very close to the money. Since LQD's volatility is very low, LQDW has no choice but to write calls very close to the money which will limit any upside the fund has. Another thing investors can do to mitigate this is to buy a mix of LQD-LQDW so that they enjoy both a high yield and get to participate in upside as well.

For further details see:

LQDW Has Been Underperforming But It May Be Salvageable