LXU - LSB Industries: Demand Is Slowing But Cash Is Growing

2023-05-19 10:46:32 ET

Summary

- LXU has underperformed over the past 6 months due to dropping fertilizer prices, but it may have found a bottom as demand begins to pick up.

- The company has invested in improvements to its existing facilities with capital improvements, including the application of AI and machine learning for optimization.

- I rate the stock a Buy after reading the first quarter earnings report that indicates that fertilizer prices may have bottomed out while cash flow is increasing.

With renewed bullish sentiment driving the stock market higher so far in 2023 while climbing a "wall of worry", this may be a good time to identify prospects for growth companies that are undervalued and that may benefit from a bullish turnaround. This is the third in my series of growth stocks that may benefit from a 2023 second half recovery. The first in the series discussed the prospects for Kimball Electronics (KE). I wrote about KE here , and that stock is currently up about 12% since I rated them a Strong Buy on May 5. Next on the list was Atkore, Inc. (ATKR), a global manufacturer of electrical, safety, and industrial products. The ATKR article was published on May 7, just before they reported Q1 earnings and despite a good earnings report and upwardly revised net income and EBITDA outlook for 2023, that stock is down slightly since my article was published with a Buy rating.

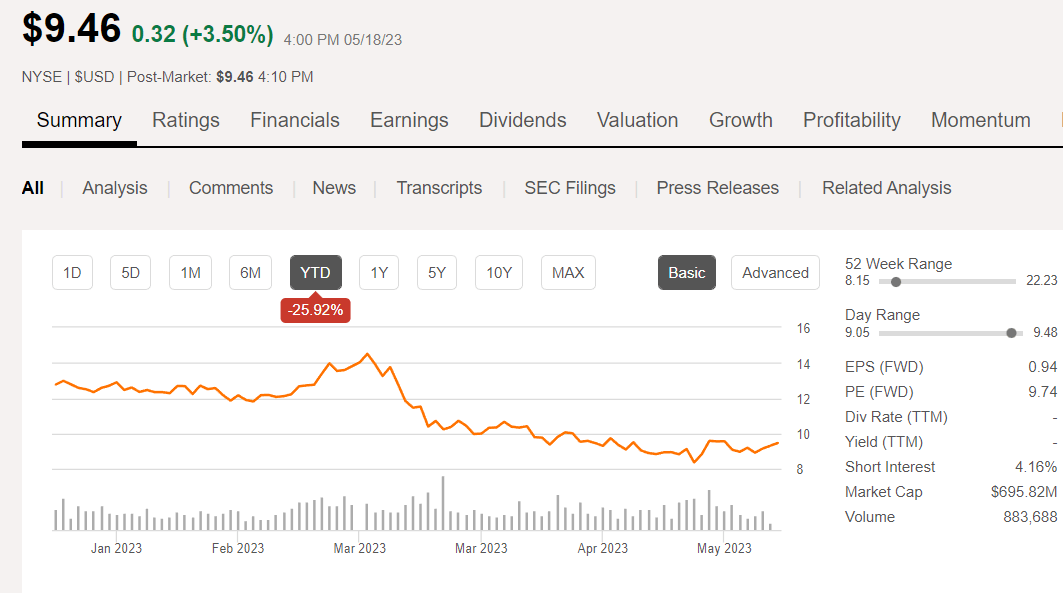

Just about six months ago now, I wrote about a small cap, under followed company that specializes in diversified chemicals including nitrogen fertilizer for agricultural applications, among other products specializing in ammonia, ammonium nitrate, sulfuric acid, and nitrogen-based fertilizers for both farming and mining. That company is LSB Industries, Inc. (LXU) and it is down more than -36% since I wrote my latest article on them in December 2022 when I assigned the stock a Buy rating.

Seeking Alpha

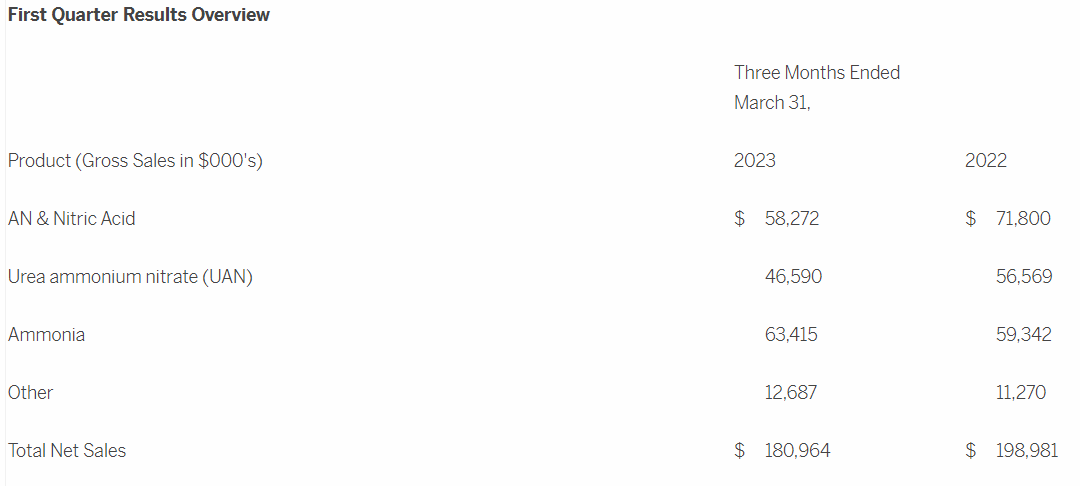

At the time, the stock was up more than 57% in 2022 while the rest of the stock market (as measured by the SPY) was down by -16%. Since then, prices for ammonium nitrate and other products that LSB manufactures have rapidly declined resulting in a decline in Q1'23 net sales, net income, and adjusted EBITDA compared to Q1'22. EPS of $0.21 missed estimates by $0.06 when the company reported Q1 earnings results on May 2. Looking at Ammonium Nitrate prices in Q1'23, the demand was bearish through March and prices were continuing to decline in part due to lower natural gas prices, especially in Europe.

The company President and CEO, Mark Behrman, summed up the difficult quarter that resulted in relatively poor performance despite the capital improvements made in 2022:

"We generated a healthy increase in sales volumes relative to the first quarter of last year. This improvement reflects the benefits of the reliability investments we made in our facilities in 2022 along with our successful commercial initiatives. However, the stronger volumes were more than offset by lower product selling prices resulting largely from a decline in natural gas prices in Europe, which reached all-time highs during 2022 and drove ammonia prices to record levels. After declining steadily for the past six months, we believe that prices for ammonia and related products are at or near a bottom, bolstered by the significant increase in fertilizer demand we've seen recently. We expect the pricing stabilization coupled with continued strong operating performance by our facilities to benefit our second quarter 2023 financial results."

As a result of the poor performance during the quarter and with prices dropping, investors have essentially sold off the stock to the point where I believe it may have bottomed out, perhaps along with ammonia prices. Also, cash flow from operations was $59M during the quarter with CapEx of $18M. The company ended the quarter with $426M in cash and short-term investments as of March 31, 2023. Furthermore, the company is buying back shares of the stock at lower prices with a recently authorized program to repurchase up to $150M of outstanding common stock.

As a result, I continue to rate LXU a Buy at the current price below $10 per share and a forward P/E of less than 10.

{kind=link}

What Does the Future Hold for LSB Industries?

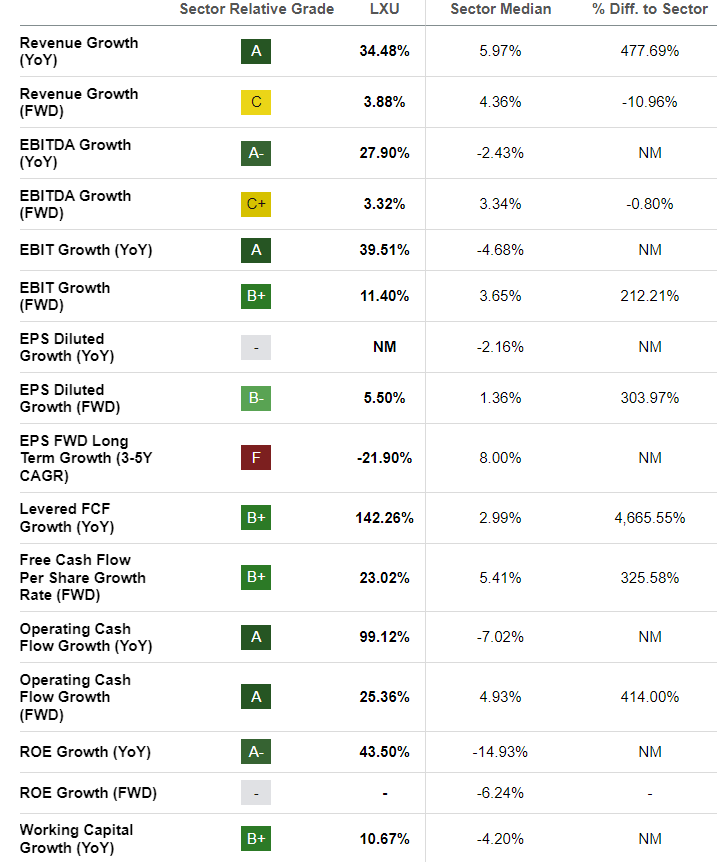

At first glance and reviewing the SA Quant ratings for LXU it might appear that growth has slowed and there are mostly downward revenue revisions going forward. When I wrote about LXU in December the SA Quant factor grades were all very good with an A+ for Growth. Now those ratings have changed, and Growth actually dropped all the way to F.

SA Quant Rating

That is quite a significant change in only 6 months, so I decided to dig a little bit deeper, and I found that only one growth factor was assigned an F rating and that is the long-term (3-5yr) FWD EPS growth rate.

{kind=link}

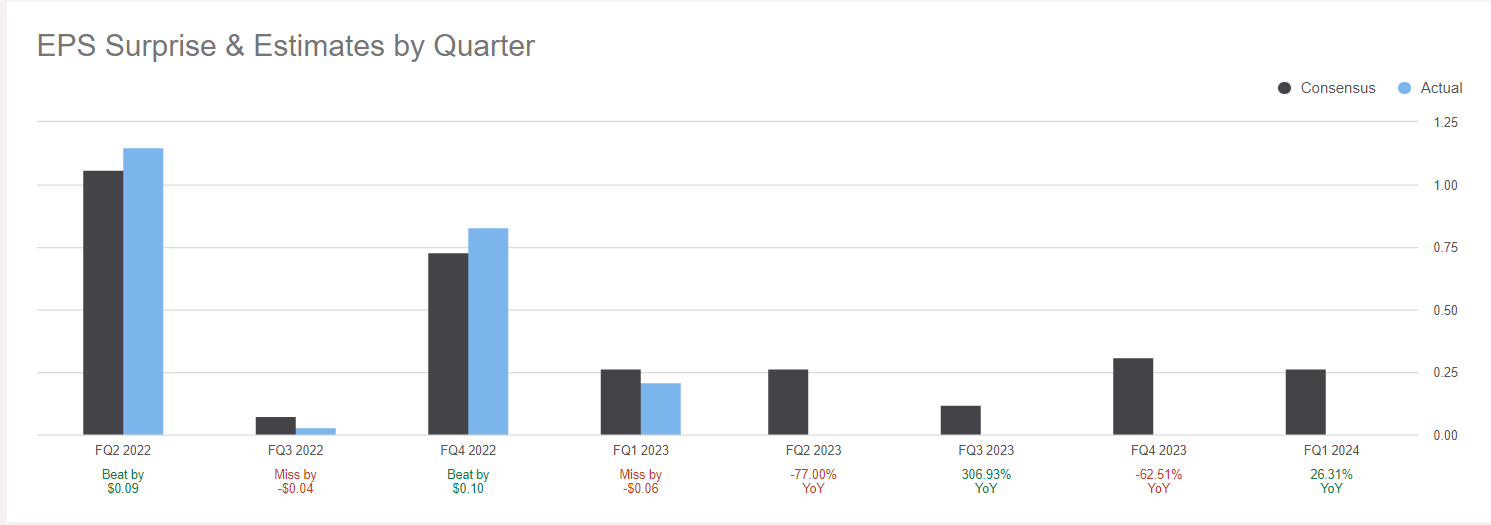

Looking at it another way, I viewed the EPS Estimates and Surprises page for LXU. It does not appear that the phenomenal growth experienced in 2022 is expected to be repeated any time in the next year or so, based on the estimates of a handful of analysts who follow the stock.

{kind=link}

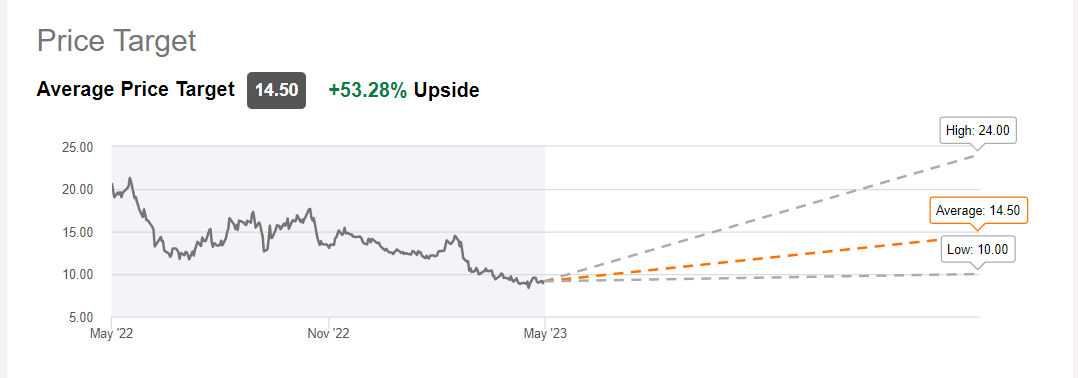

There are now a total of 8 Wall Street analysts following the stock with 4 giving it a Strong Buy, 1 Buy, and 3 Hold ratings. The average target price is $14.50 which represents more than 50% upside from the current price.

{kind=link}

Benefitting from the Energy Transition and AI

The management team at LSB Industries are not sitting on their thumbs waiting for prices to go up again. Although prices for AN and Nitric Acid and Urea Ammonium Nitrate, or UAN, declined over the past 6 months resulting in reduced net sales, Ammonia products increased during the quarter, compared to the previous year. In the market outlook section of the earnings report for Q1, the reasons why that occurred and what is expected going forward were explained:

In addition to the lower production costs for European producers as compared to a year ago, the decline in fertilizer prices reflects the impact of a delay in this season's spring fertilizer application in many corn growing regions of the U.S. due to cold and wet weather. Nitrogen prices have also been pressured by lower demand for ammonia from Asian industrial markets as well as from phosphate producers. Despite these factors, nitrogen pricing remains at attractive levels and appears to have stabilized with potential for improvement as 2023 progresses, given an increasingly favorable demand outlook.

{kind=link}

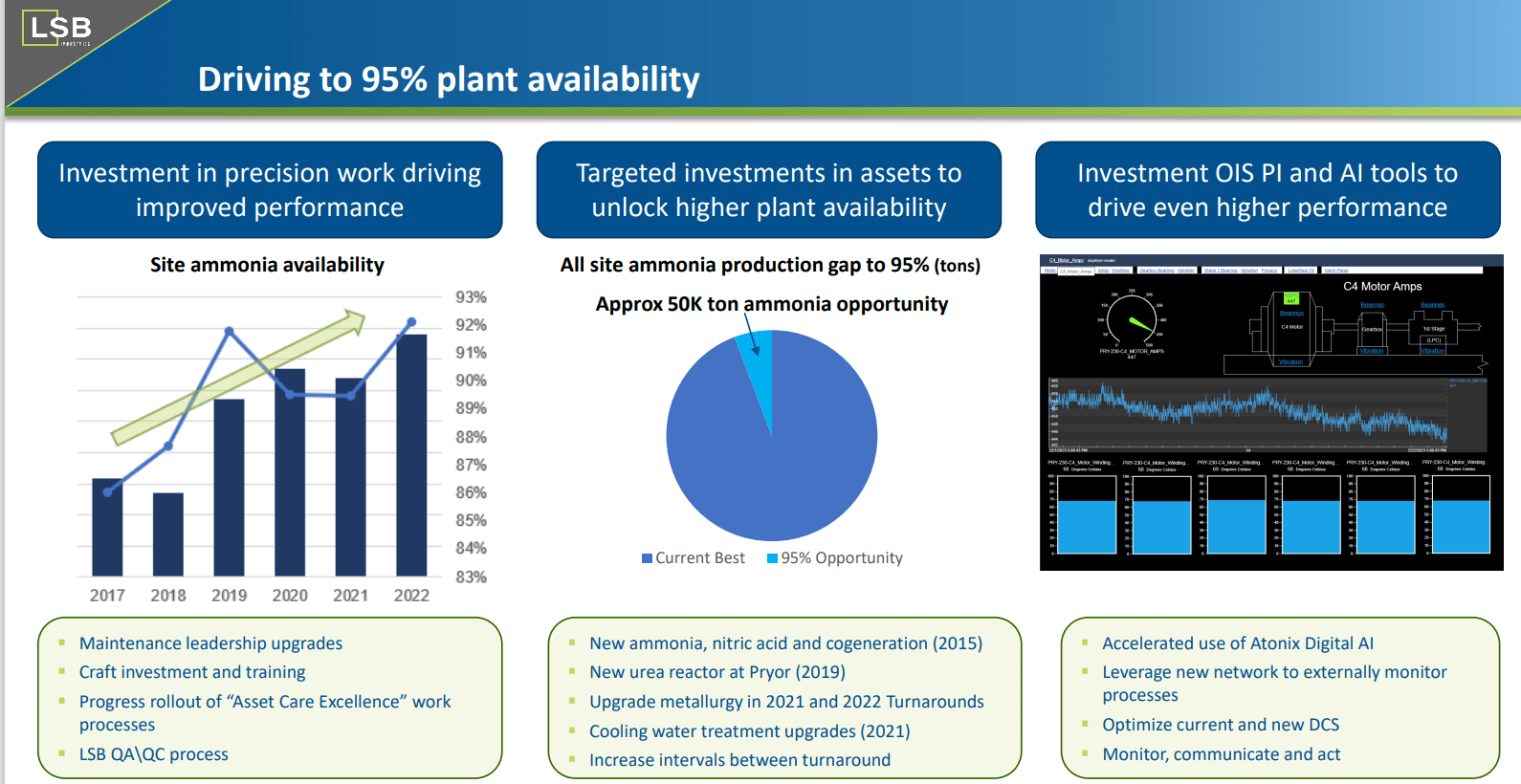

Meanwhile, the company is continuing to improve its existing facilities and production capacity including the use of machine learning and AI applications to optimize performance. This slide from the Investor Day presentation in March of this year illustrates these investments and the results that have occurred.

{kind=link}

In addition, the company's vision is to be at the forefront of the energy transition with their blue and green ammonia projects which are gaining traction, as well the use of ammonia as a clean fuel and as a carrier for hydrogen. In addition, the El Dorado Carbon Capture and Storage project is making headway with a milestone reached by filing a Class VI sequestration well permit. The EPA is currently evaluating the permit.

The El Dorado project is the first carbon capture and storage ("CCS") project in the state of Arkansas, and only the third project of its kind in the United States, putting LSB-El Dorado at the forefront of low carbon or blue ammonia production.

Peers to Consider

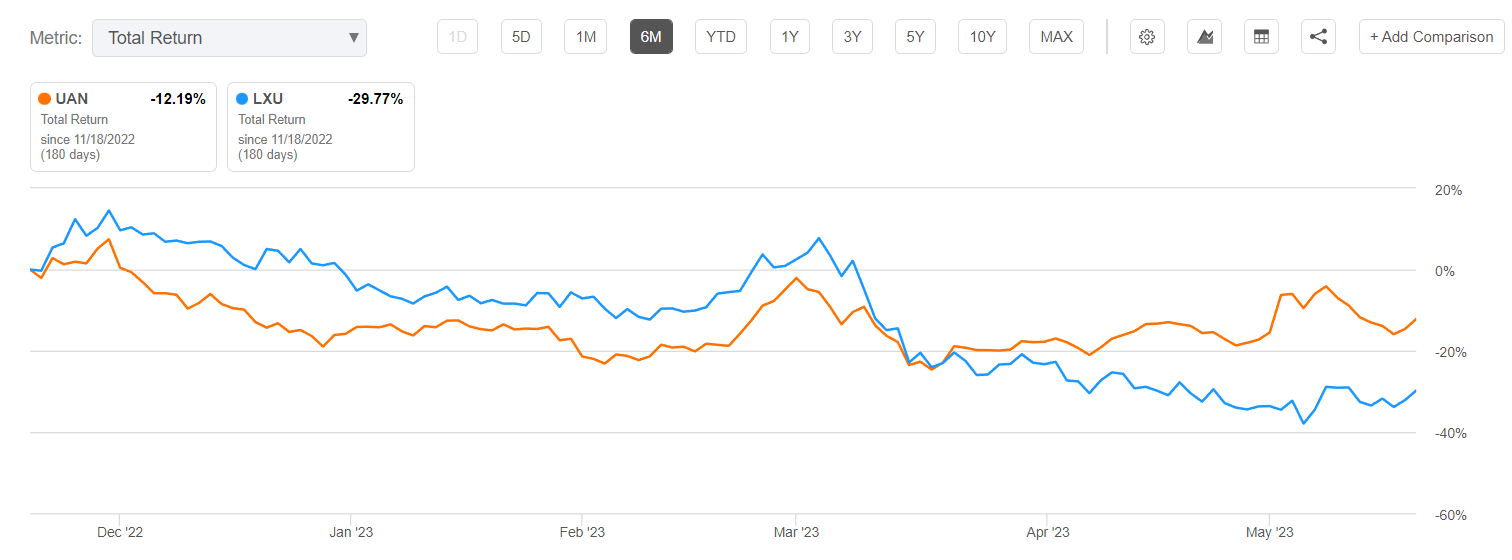

Another popular fertilizer stock that is a peer to and in some cases, a direct competitor to LXU is CVR Partners, LP (UAN). The UAN stock also suffered from a severe price drop over the past 6 months, however, due in part to the large distributions that it pays, the total return in the past 3 months has far exceeded that of LXU as shown in this comparison chart. The UAN stock is registered as an MLP and thus issues a K-1 at tax time, but many investors believe strongly in the stock due to its huge distribution.

{kind=link}

The Q1 report for UAN included more favorable results due to what was called a robust start to the spring pre-planting season, based on comments from CVR Partners CEO Mark Pytosh:

"The spring pre-planting season is off to a robust start and the U.S. Department of Agriculture estimates that planted corn acres will increase approximately 4 percent this spring compared to a year ago, driving strong demand for nitrogen fertilizer."

In addition, UAN, being a variable distribution paying MLP, announced a distribution of $10.43 per common unit, payable on May 22, 2023, to unitholders of record as of May 15. That sizable distribution payout is one of the primary attractions to UAN as an investment.

Summary

The global nitrogen fertilizer market including UAN has grown by about 40% in the past decade with much of that growth occurring in the US, according to S&P Global Commodity Insights :

Key facts about the nitrates fertilizer market

-

Around 35-40% of global UAN production is traded each year with the United States having tripled exports between 2014 and 2019.

-

Russia is by far the largest producer and exporter of fertilizer-grade AN, holding an estimated 45% share in global exports each year.

-

CAN consumption and trade is concentrated in Europe where Germany is by far the largest importer on a global scale, taking around 2 million tonnes per year or about one-fifth of the global import market each year.

-

The global UAN market has grown by more than 6.2 million tonnes, or close to 40%, over the past decade, mainly driven by the United States, which is by far the largest market for UAN around the world.

-

Nitrate prices generally move in step with urea as this is the main competition product, although prices can move in different directions on the back of structural or fundamental changes in one of the markets.

With the war in Ukraine impacting the production of fertilizer out of Russia and due to sanctions on Russian products, the US and Europe have increased production even further to offset the loss in supply. That led to the huge price increases in 2022 which are not likely to be repeated. Prices have been coming down over the past 6 months but are expected to increase again as demand picks up during the growing season, and Q2 results may indicate how much price improvement has actually occurred since the end of March.

From the Q1 earnings call, CEO Behrman had this to say:

"Despite the pricing headwinds in the first quarter, we continued to generate solid free cash flow which further strengthened our balance sheet. Our current financial position gives us the flexibility to create value for shareholders in multiple ways including investments in the growth of the business and potential debt reduction and/or additional share repurchases. Additionally, we are more excited than ever about our blue and green ammonia projects that we have underway, and other potential projects that we are exploring. The groundswell of interest in the use of ammonia as a clean fuel and as a carrier for hydrogen continues to build. Our vision is to be at the forefront of this energy transition, which we expect to result in a meaningful reduction to global CO 2 emissions, including those of our company, while at the same time representing an attractive opportunity for us to generate significant incremental profitability and shareholder value."

I like the prospects for LXU going forward, with a strong balance sheet, cash available for capital improvements or even a potential acquisition, stock buybacks, the use of AI and optimization of existing facilities and equipment, along with improving acceptance of green and environmentally friendly products that support the energy transition. As an undervalued growth stock that could take off in the second half of 2023, I rate LXU a Buy at a price under $10 with potential 50% upside by the end of 2023.

For further details see:

LSB Industries: Demand Is Slowing But Cash Is Growing