LXU - LSB Industries: Downgrading To Hold Due To Lower Prices And Reduced Demand

2023-09-07 05:01:13 ET

Summary

- LSB Industries has experienced a significant decline in stock price after initial growth expectations did not materialize.

- The company is betting on other projects and initiatives, such as clean ammonia and clean hydrogen, to boost future revenues.

- The outlook for Q3 and the remainder of 2023 remains bleak, with downward earnings revisions and slowing growth.

While my emphasis on investing has shifted recently from under covered growth stocks to more income-oriented securities, I still enjoy keeping an eye on potential growth prospects that could lead to outsized returns over time. I enjoy researching current market trends and I try to identify companies that are poised to take advantage of growth opportunities in the market.

One such small cap growth stock that I have covered multiple times over the past two years is LSB Industries (LXU). When I first covered LXU back in March 2022, fertilizer stocks were in the news in part due to the Russian invasion of Ukraine that sent natural gas prices soaring in Europe and led to global concerns regarding the availability of fertilizer for agricultural and other uses, leading to record high fertilizer prices. At the time, I wrote:

With sanctions against Russia increasing the pressure on some commodities that in normal years are supplied by Russia to the rest of Europe and other parts of the world, the supply is likely to become even more constrained leading to yet higher prices. The impact on oil prices has recently been demonstrated and now prices of other commodities including fertilizer for agricultural, industrial, mining and other uses are also starting to be impacted. There are record high prices for fertilizer already, and the sanctions have only just begun. This offers a potential opportunity for companies that can fill the void and increase supply at higher prices, increasing their profit margins.

{kind=link}

Unfortunately for investors in LXU, that growth story did not play out as I had expected and the stock price rose to a 5-year high shortly after I published that article and then plummeted afterward by nearly -50% as of today, September 6, 2023. In December 2022, I wrote another article updating my coverage of LXU with yet another Buy rating. You can read that article here . At that time, the stock was trading for about $14 per share and had outperformed the broader market throughout 2022 and I had expected the outperformance to continue.

Seeking Alpha

And although I was correct in the short term, the stock price peaked just a few weeks later at a price of $26.74 on April 19 and has come back down to a closing price of $14.34 as of 12/9/22. Now at a forward P/E of 5.19 according to SA, the growth prospects for 2023 and beyond look even better as revenues and gross margins continue to grow.

A year after my initial coverage, in May of this year I wrote another update and recommended again that investors Buy the stock. In that article, I summarized my buy recommendation with this paragraph:

I like the prospects for LXU going forward, with a strong balance sheet, cash available for capital improvements or even a potential acquisition, stock buybacks, the use of AI and optimization of existing facilities and equipment, along with improving acceptance of green and environmentally friendly products that support the energy transition. As an undervalued growth stock that could take off in the second half of 2023, I rate LXU a Buy at a price under $10 with potential 50% upside by the end of 2023.

And in fact, the stock has beaten the S&P 500 in the time since I published that latest Buy recommendation. However, in the most recent earnings report for Q2 the revenues were down -41% YOY and the outlook for the rest of the year did not look too encouraging. President and CEO Mark Behrman attempted to put a positive spin on the report by stating that production facilities are ramping up in anticipation of increasing future demand. From the earnings press release , he made this statement:

"The teams at our manufacturing facilities operated our plants well and our commercial organization effectively moved product in the face of a challenging demand and pricing environment. For the second consecutive quarter we experienced a significant year-over-year decline in selling prices reflecting the impact of lower natural gas prices in Europe and weaker industrial activity in Asia. Additionally, UAN demand was below expectations as farmers opted to apply more urea due to what had been comparatively attractive pricing early this year versus UAN. More recently, however, prices for nitrogen products have begun to increase, a trend we expect to continue at a measured pace through the second half of this year, with further improvement likely building into the 2024 Spring planting season."

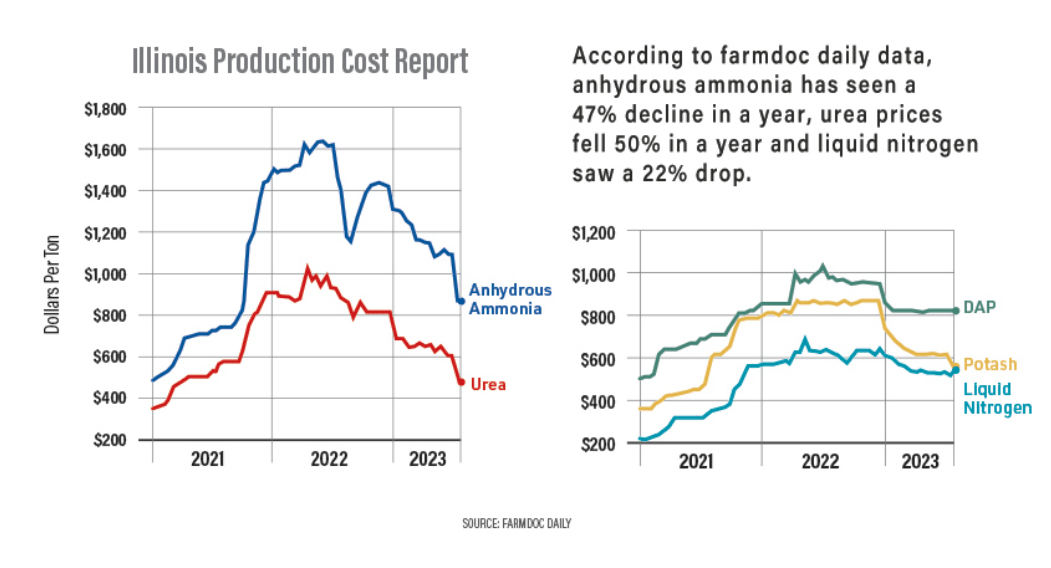

Unfortunately, at least as of August 17, 2023, fertilizer prices have continued to drop and have been in “free fall” for most of the year according to this article from AgWeb.

{kind=link}

Meanwhile, as demand for fertilizer drops, LXU is betting on other products and initiatives to bolster their future revenues. In another statement from the Q2 earnings report, CEO Behrman had this to say about those other projects and initiatives:

"Industry momentum of the development of clean ammonia and clean hydrogen continues to build. We continue to pursue our previously announced blue and green ammonia projects. Additionally, we recently signed an MOU with Amogy for the development of ammonia as a marine fuel for U.S. inland waterway activities. Through these projects, and the other projects we are exploring, we are well positioned to benefit from attractive government incentives that are currently in place. Additionally, we believe these projects will benefit from anticipated growth in end-market demand, particularly for clean ammonia for power generation and marine locomotion. Our vision is to be at the forefront of this energy transition, reducing our CO2 emissions and contributing to the expected reduction in global CO2 emissions. At the same time, we believe these opportunities will allow us to generate additional meaningful incremental profitability and shareholder value."

In my opinion, those are worthwhile endeavors, however, they are likely to take some time to play out. Meanwhile, the outlook for Q3 and the remainder of 2023 remains bleak. In fact, the SA Quant rating recently downgraded LXU to a Sell due to downward earnings revisions and slowing growth.

Seeking Alpha

In fact, in the past 3 months there have been 7 downward earnings revisions and 6 downward revenue revisions. During the earnings call it was mentioned that a sequential decline in Q3 revenues is expected to occur, similar to what they saw in 2022. In fact the CFO, Cheryl Maguire, clarified that expected decline in response to a question on the LSB Industries, Inc. Q2 2023 Earnings Call Transcript :

Andrew, so what I was referring to is we generally see a pretty heavy sequential decline as you move from Q2 to Q3 because Q3 is the seasonally weakest quarter, as you know. And so if you look at Q2 of last year and you look at Q2 to Q3 and what the decline was there, it was ballpark 65%, 70% decline. I think you're going to see a similar decline this year if you compare the third quarter to the second quarter of this year.

Summary and Conclusion

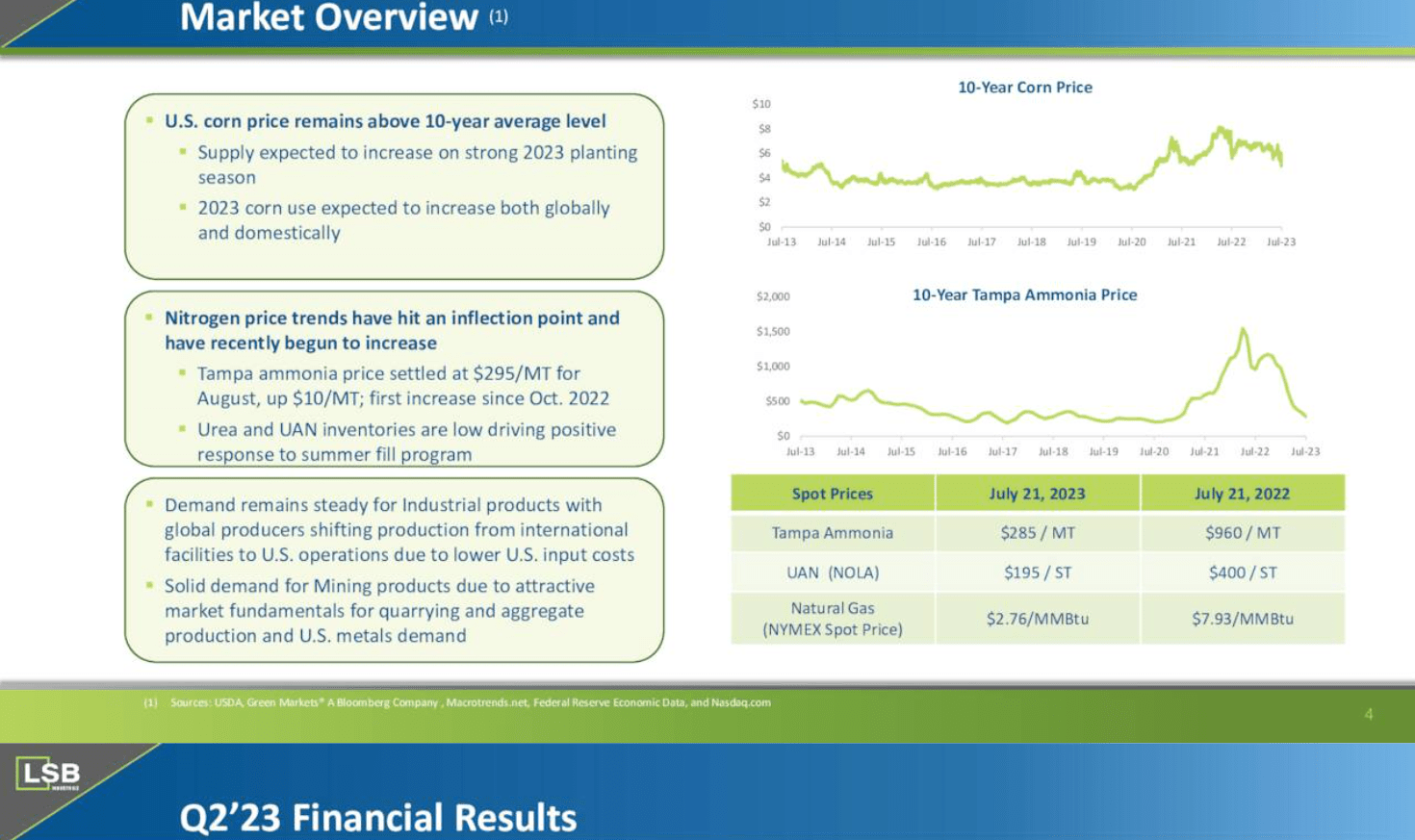

With the continuing decline in fertilizer prices and reduced demand for UAN and Ammonia products from LXU, I do not anticipate that the third quarter will show any improvement. In fact, Ammonia prices have dropped precipitously in 2023 to near a 10-year low as shown in this slide from the Q2 investor presentation.

{kind=link}

Given the recent downward revisions in revenues and earnings and with the expected sequential decline from Q2 to Q3 anticipated by the company as outlined in the earnings call, my recommendation is to hold shares if you already own them and wait for the next earnings report to determine whether it makes sense to add more or sell at that time.

There is a possibility that the company can turn things around in 2024 with the expanded product mix, and if fertilizer prices begin to trend upward again. For the remainder of 2023, I do not anticipate that any substantial changes to the growth trajectory are likely to occur unless there is some news that is not currently known such as an acquisition or takeover bid. I am downgrading my rating on LXU to Hold based on the latest data.

For further details see:

LSB Industries: Downgrading To Hold Due To Lower Prices And Reduced Demand