TIP - LTPZ: More Risk Than Reward Further Out On The TIPS Curve

2023-12-11 15:21:25 ET

Summary

- Both nominal and real rates are down across the curve.

- The catch is that the curve now embeds some very aggressive Fed easing assumptions.

- Buying long-duration TIPS doesn’t offer a particularly attractive risk/reward here.

Treasury bonds may have rallied in recent weeks, but the fundamental and technical support for the move seems shaky - at best. Last month's consumer inflation print did surprise consensus expectations on the downside, but at +3.2% YoY headline and +4% YoY core, it remains a long way off the Fed's target. A lower long-duration issuance schedule (per Q4 refunding ) also helped, driving real and nominal yields to the lower end of their recent trading ranges.

The big repricing echoes what we saw in Q4 last year, when inflation also surprised to the downside and triggered a widespread decline in yields - despite YoY inflation running well above the Fed's target. Since then, we've seen more hikes, not cuts, and big yield spikes at the long end as a result. It also remains unclear if the demand/supply dynamic for duration has changed - recall the last five and ten-year Treasury Inflation-Protected Securities ((TIPS)) auctions saw consecutive tailings (i.e., bonds issued at a discount to face value), as well as significantly higher dealer participation.

{kind=link}

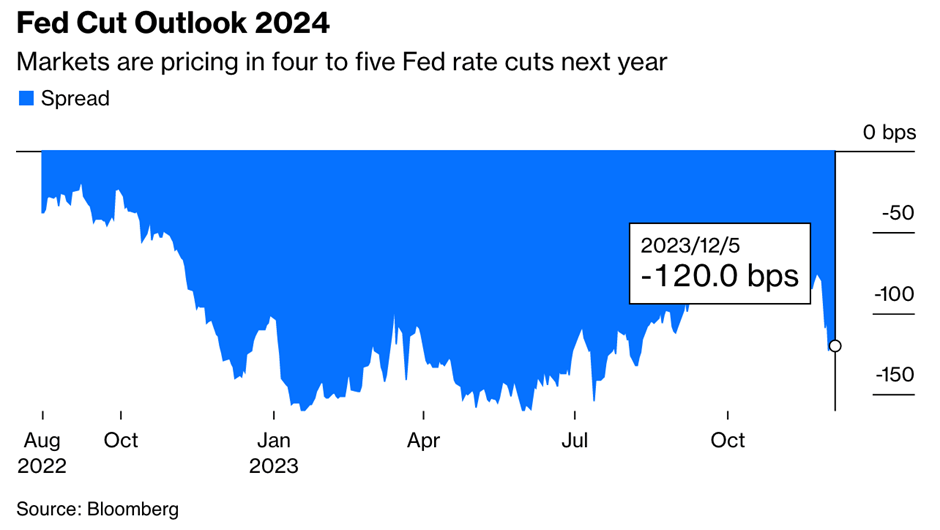

In contrast with the fundamental and technical backdrop, the bond market appears to be pricing in the same dovish bias it did last year. This time around, the Treasury curve is pricing a massive 120bps of rate cuts for 2024 - despite Fed Chair Powell's 'premature' warning . Thus, even if we do see a 'hard landing' scenario that forces the Fed into an accelerated rate cut cycle, any potential upside will likely be modest. Inversely, if we don't see a 'hard landing' or in the likely scenario that we see a 'soft landing' scenario, nominal yields will move higher to realign with Fed guidance for a more gradual rate path.

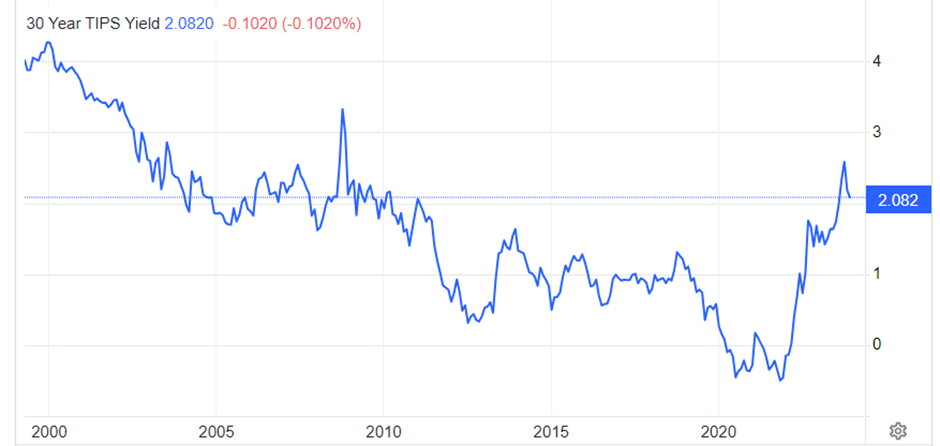

Net, the ~2% real yields (i.e., the difference between nominal Treasury yields and expected inflation) currently on offer across the TIPS curve might seem attractive after years of ultra-low rates, but it doesn't leave a lot of margin for error. The combination of an unfavorable risk/reward further out in the curve and reinvestment risk means long-duration TIPS ETFs like PIMCO 15+ Year U.S. TIPS Index Exchange-Traded Fund ( LTPZ ) don't screen all that favorably here.

Fund Overview - A Concentrated and Pricey Vehicle for TIPS Duration

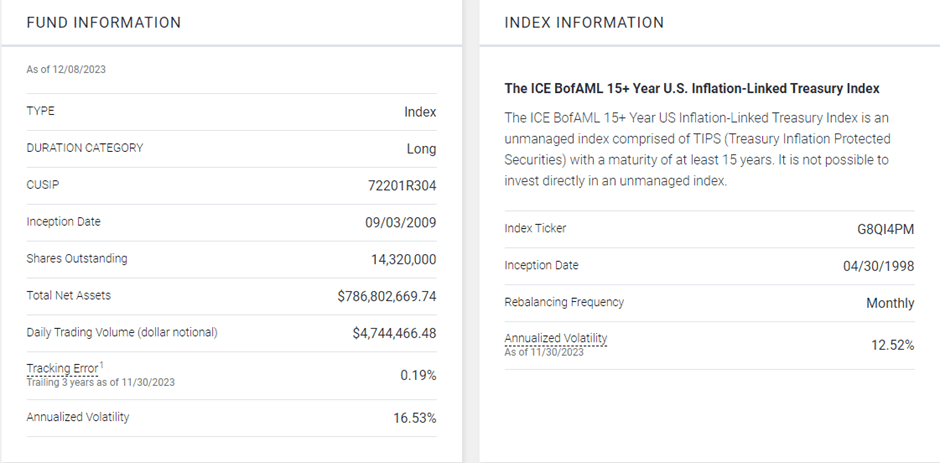

The PIMCO 15+ Year U.S. TIPS Index Exchange-Traded Fund tracks (pre-expenses) the total return performance of the BofA Merrill Lynch 15+ Year US Inflation-Linked Treasury Index, a basket of US dollar-denominated TIPS with an +15-year remaining term to final maturity. The ETF is one of the smaller TIPS index trackers by assets (~$787bn) and the only major fund that specifically targets the +15-year segment of the curve. LTPZ is also one of the pricier options out there, charging a 0.2% expense ratio. By comparison, larger TIPS ETFs that invest across the maturity spectrum, like iShares TIPS Bond ETF ( TIP ) and the Schwab U.S. TIPS ETF ( SCHP ), charge 0.19% and 0.03%, respectively.

{kind=link}

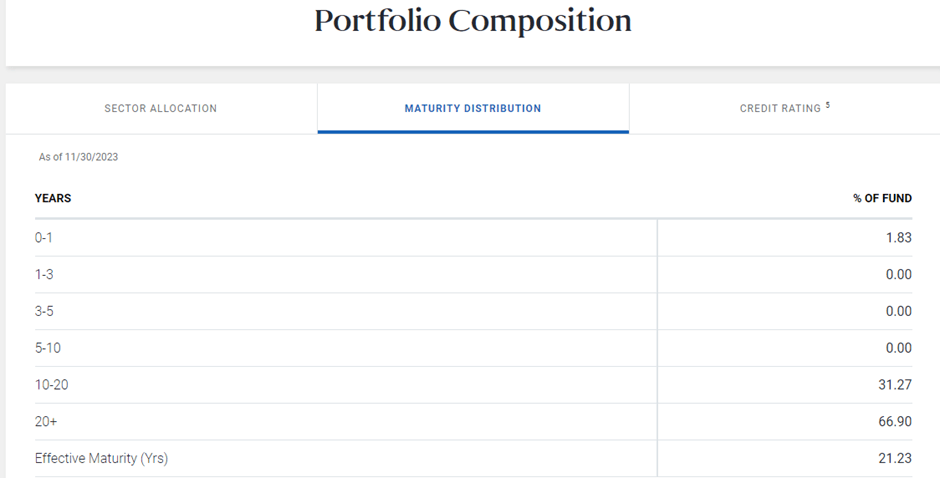

The fund is spread across a fairly concentrated 16-holding portfolio, with the largest allocation going to the +20-year maturity at 66.9%. The 10-20-year bucket has a 31.3% allocation. In line with its allocation, LTPZ has an effective duration profile of 19.24 and an effective maturity of 21.2 years, making this one of the most rate-sensitive TIPS vehicles out there. In contrast, broad-based TIPS alternatives like SCHP and TIP have effective durations of 6.4 and 6.6 years, respectively. Despite its expense ratio and monthly rebalancing frequency, the fund maintains a fairly narrow 0.19% tracking error relative to its benchmark index.

{kind=link}

Fund Performance - Lackluster Returns; ~5% Yield Not as Attractive in Context

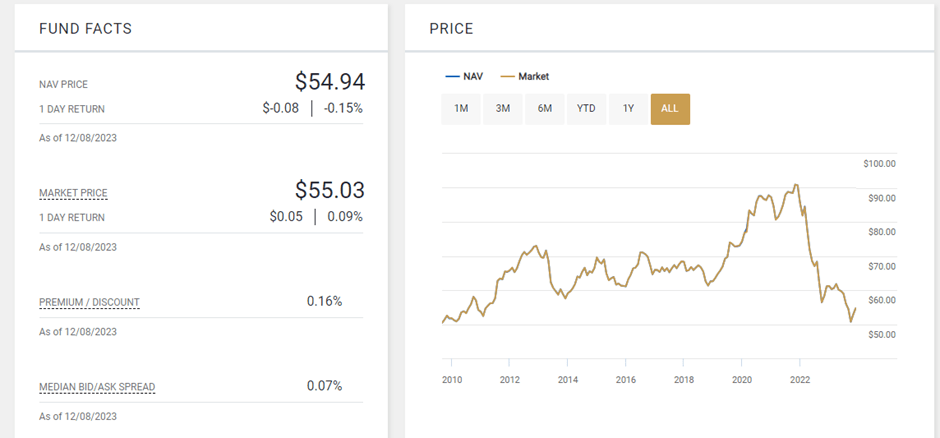

On a year-to-date basis, LTPZ's long-duration approach has seen the fund suffer an overall decline of -2.3% in NAV terms (-2.0% in market price terms), underperforming its TIPS ETF peers. This year's drawdown follows steeper moves over the last one and three years, which saw the fund post -7.8% and -11.2% returns on an annualized basis. Even over longer five and ten-year timelines, LTPZ has returned a rather lackluster +0.7% and +1.9%, respectively, not helped by an ultra-low interest rate environment. By comparison, ultra-low-cost SCHP has outperformed LTPZ across virtually all time horizons over the last decade, though TIP's relative outperformance stops after the five-year mark.

{kind=link}

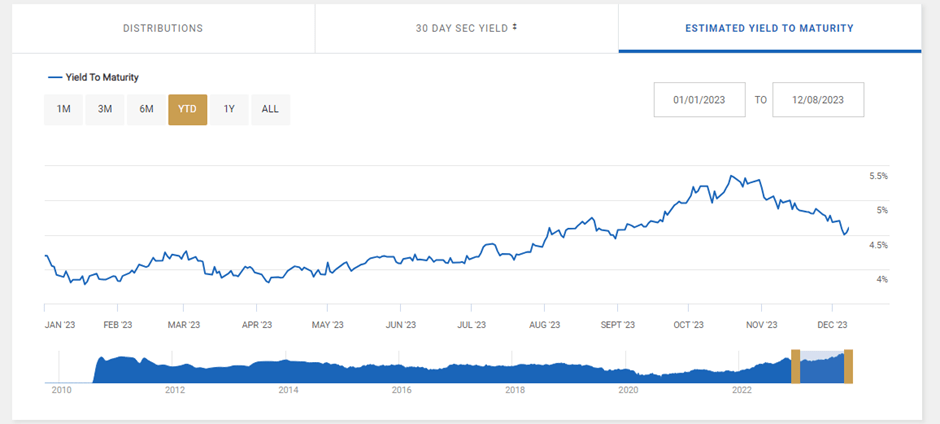

The abrupt shift from ultra-low rates to a 'higher for longer' rate regime may have punished LTPZ particularly hard, but its distribution yield has benefited - the LTPZ 30-day SEC yield currently stands at 5.0% (4.6% market-weighted yield to maturity). On a relative basis, however, lower-duration TIPS funds like SCHP and TIP offer comparable 30-day yields at 4.9% and 4.8%, respectively. Given the TIPS curve also remains mostly inverted (with the exception of the 20-year segment), investors aren't getting sufficiently paid for duration risk here, in my view.

{kind=link}

More Risk than Reward Further Out on the TIPS Curve

It wasn't that long ago when the ten-year Treasury breached the all-important 5% threshold following a one-two-three punch of weak auction demand, resilient economic data, and 'higher for longer' Fed messaging. Since then, the yield curve has rallied, particularly at the long end, despite a lack of fundamental support from the data. Growth is strong, core inflation is still running well above the Fed's target, and jobs data is trending positively. From a technical standpoint, recent Treasury auctions have also done little to reinforce confidence in the marginal buyer further out on an inverted curve - crucial ahead of more Treasury/TIPS coupon issuances in 2024.

{kind=link}

At current levels, pricing is even more aggressive than it was in Q4 last year, when a benign October 2022 inflation print triggered expectations of a pivot. Similarly, 120bps of 2024 rate cuts are currently priced into the Treasury curve today - an outcome that leaves little room for anything other than a 'hard landing.' And zooming out, history says ~2% real yields are hardly a floor number; in fact, it may even be below-par during times of normal monetary policy, much less one where investor appetite has changed for the worse (note the consecutive 'tailed' TIPS auctions in recent months). All things considered, pricing seems a bit overdone in the context of a rather benign economic backdrop, and I would remain sidelined on LTPZ.

For further details see:

LTPZ: More Risk Than Reward Further Out On The TIPS Curve