LKNCY - Luckin Coffee: Poised For Redemption

2023-06-26 03:44:29 ET

Summary

- Luckin Coffee has recovered from its accounting scandal and bankruptcy, achieving profitability in 2022 under new CEO Jinyi Guo.

- The company is well-positioned to capitalize on China's growing coffee consumption, with over 9,000 stores and a focus on affordability and convenience.

- Strong Q1 2023 financial performance and aggressive expansion plans make Luckin Coffee an attractive investment opportunity and I rate it as a "Buy".

Editor's note: Seeking Alpha is proud to welcome AN Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

After major restructuring efforts & a complete overhaul of its C-Suite executives, Luckin Coffee (LKNCY) is way past its "dark days" of investor fraud and corporate oversight.

Secular tailwinds, coupled with a unique customer value proposition, Luckin Coffee holds immense growth potential, which is further propelled by the company's aggressive expansion plans and efficiently managed lean team.

Furthermore, consumer expenditure on food & beverage items in China remains resilient despite macroeconomic conditions, with the market for coffee expected to grow annually by 6.58% from 2023 to 2025.

I believe that the company's strong Q1 2023 financial performance and solid balance sheet present an attractive investment opportunity for long-term growth investors.

I rate Luckin Coffee as a "Buy"

Company Overview

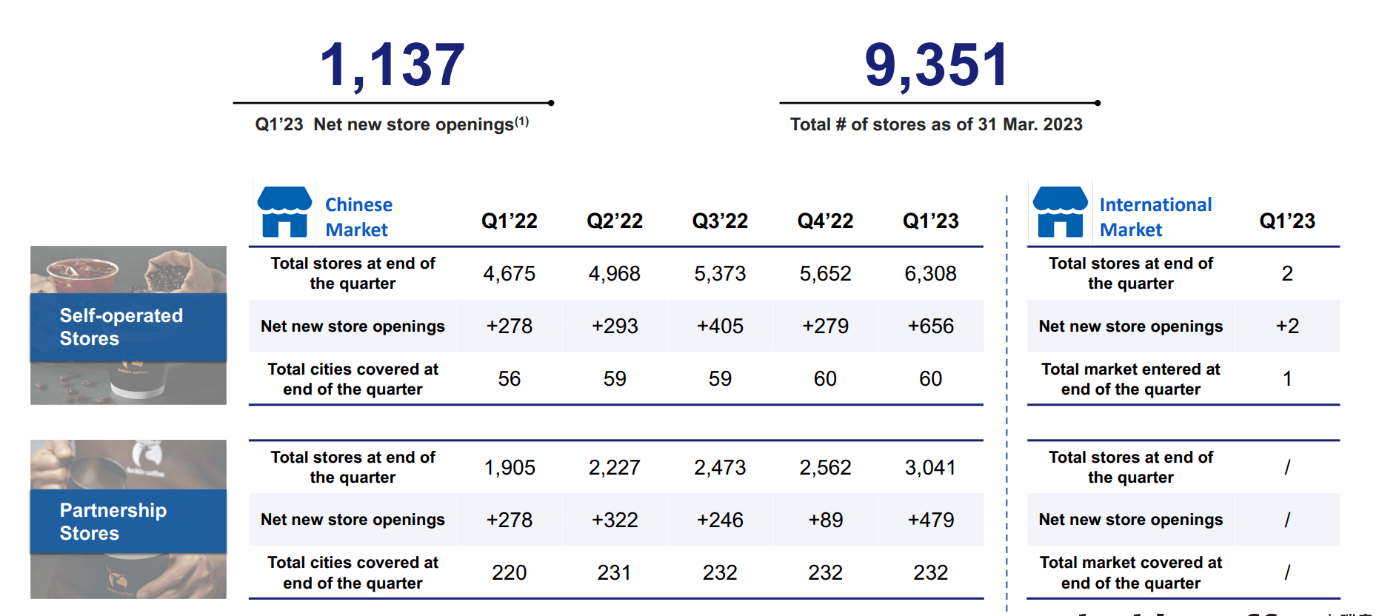

Luckin Coffee is a Chinese coffee company and coffeehouse chain. The company is headquartered in Beijing and operates a total of 9,351 (as of 2023 Q1) physical stores across China and Singapore.

Dubbed the "Starbucks of China", the company offers a variety of novel drinks such as the "Minty Coconut Latte", targeted at the younger, less-wealthy demographic. The average price for a cup of coffee from Luckin Coffee is around ~15 RMB , which roughly translates to $2, compared to the average price for a cup of coffee from Starbucks, which sells for around ~30 RMB.

Accounting Scandal

In 2020, Luckin Coffee overstated its 2019 revenue , resulting in the company's delisting from the NASDAQ. While it could take years for the company to fully shed the stigma from this controversy, the new management has done a remarkable job of turning the once-failing business around.

Under the leadership and guidance of its new CEO Jinyi Guo, the company emerged from bankruptcy and achieved profitability in 2022 .

This remarkable feat could be attributed to repositioning the company's business model, a lean management team, and adopting a franchising model. However, investor sentiment seems to remain bearish toward the stock.

Luckin Coffee currently trades at a price-to-sales ratio of 3.16 , a significant discount compared to its closest competitor, Starbucks (SBUX) which trades at a ratio of 3.43 . While it would be wise to take the company with a pinch of salt, I believe that it would be a great investment for investors willing to tolerate some uncertainty for long-term growth.

Secular Growth And Consumer Resilience To Macroeconomic Conditions

According to the China Coffee Association, coffee consumption in China is expected to grow by 15% annually. This strong growth in demand for coffee can be attributed to the switch in consumer preferences of millennials and Gen-Z from tea to coffee.

With over 9,000+ stores and 200+ cities served as of Q1 2023, Luckin Coffee is well positioned to serve this strong increase in demand and capture a larger share of the domestic coffee market.

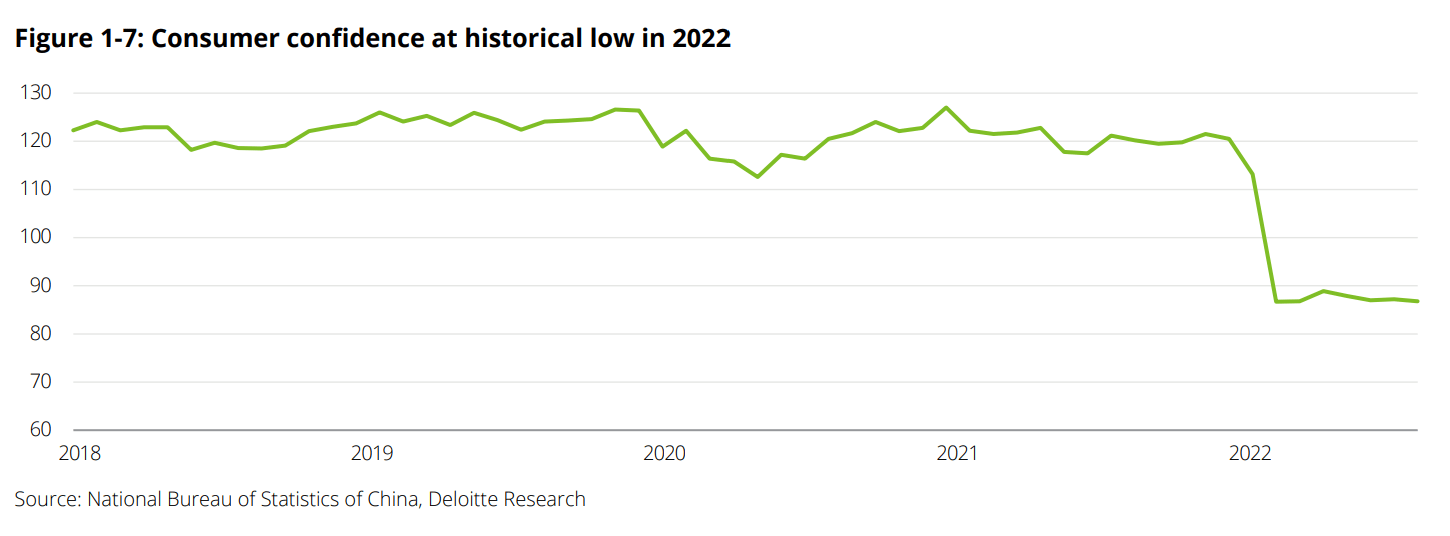

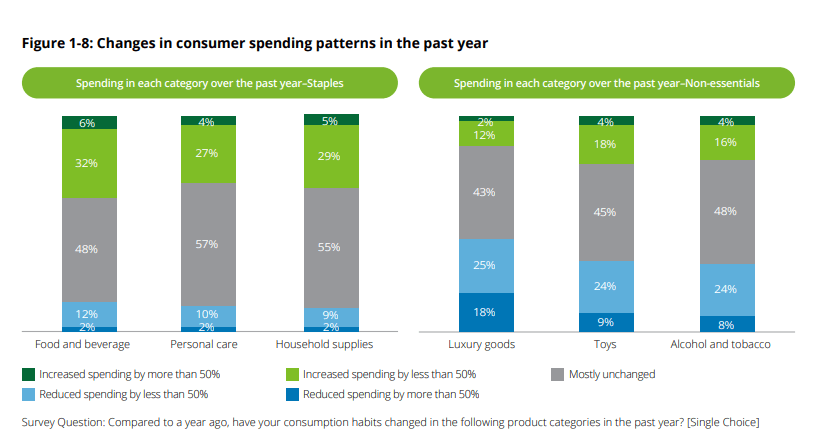

Additionally, consumer expenditure on food & beverages in China seems to be largely unaffected by macroeconomic conditions. Even though consumer confidence fell to its lowest in 2022, only 12% of consumers reduced spending by less than 50% on food & beverage items, and only 2% reduced spending by more than 50%

2023 China Consumer Insight and Market Outlook 2023 China Consumer Insight and Market Outlook

{kind=link}

{kind=link}

Luckin Coffee brands itself a "7-11" for coffee with an emphasis on affordability and convenience, catering to the low-end market. The affordability of the company's products proved to be a differentiating factor compared to its competitors.

During COVID restrictions and economic uncertainty, business was not badly affected as consumers were still willing to spend on coffee. From 2020 to 2021, Luckin Coffee enjoyed a 97% YoY revenue growth while competitors such as Starbucks suffered a contraction of 11% YoY revenue.

The company's unique branding as an affordable yet high-quality coffee maker, coupled with its operational capabilities to capitalize on secular tailwinds could allow them to enjoy greater economies of scale and drive stronger top-line growth despite recession fears.

Unique Value Proposition From A Technology-Driven Business Model

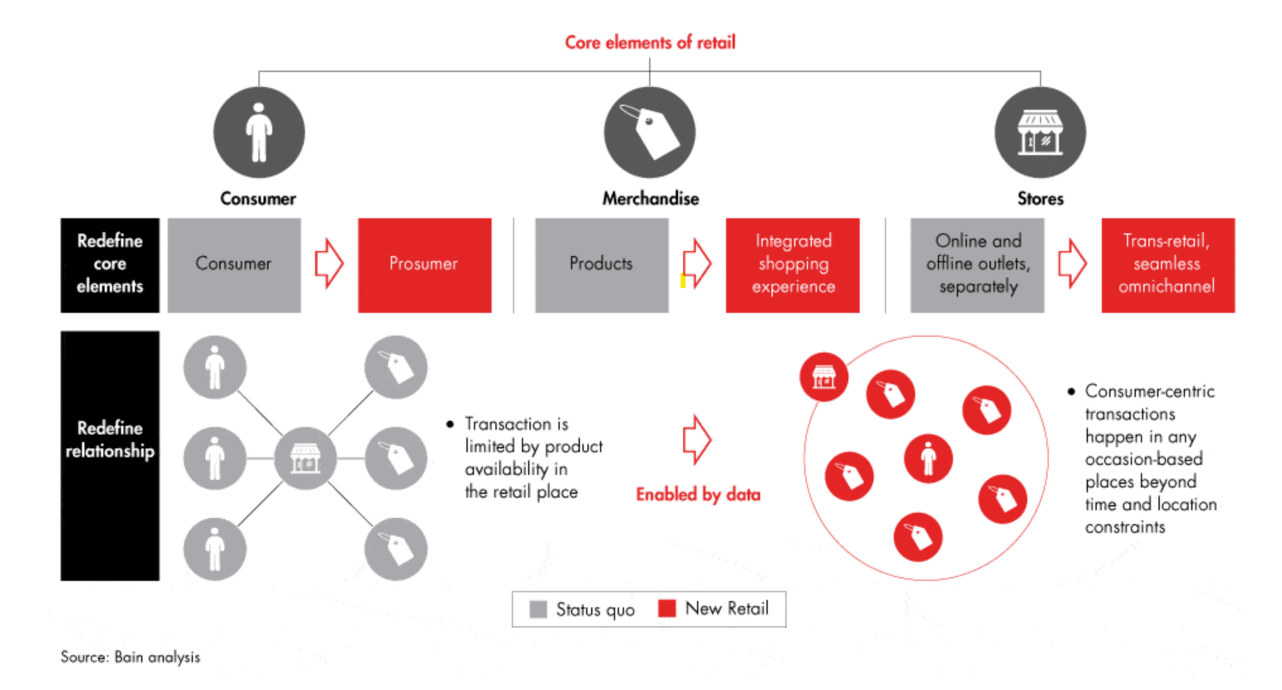

Luckin Coffee's innovative business model is based on the idea of "new retail", which reconciles the convenience of online shopping and the physical presence of brick-and-mortar retail stores to offer a seamless and integrated experience.

{kind=link}

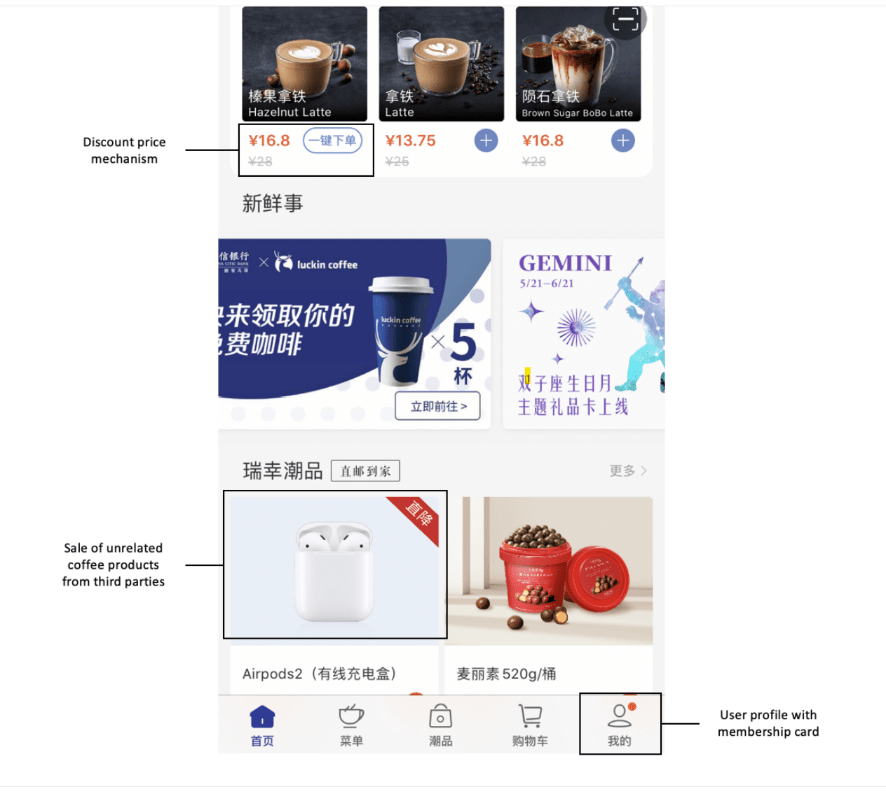

The company has an application that allows customers to pre-order & pay for drinks, enjoy discounts, and even watch a live stream of how their drink is prepared among other features. The app also functions as an e-commerce platform, with the company partnering with other retailers to offer other food products and lifestyle gadgets such as AirPods.

{kind=link}

This seamless and fully integrated experience allows the company to onboard customers easily, which can be seen from their ~20% QoQ growth in average monthly transacting customers, from Q4 2022 to Q1 2023.

Additionally, the company leveraged its technological capabilities to streamline operations & processes, which allowed it to improve operating margins from ~8% to ~15% QoQ.

Luckin Coffee's customer-centric approach and its ability to enhance and optimize customer experience have proven to be pivotal in helping the company to capture market share aggressively from the likes of competitors such as Starbucks despite the former entering the market later.

Aggressive expansion presents endless possibilities

The number of total stores operated by Luckin Coffee has increased steadily from 6,580 to 9,351 as of Q1 2023, representing a ~42% YoY growth. The company currently boasts the most stores in its domestic market and by the end of Q4 2022, Luckin Coffee had more than 7000+ stores in China, while Starbucks celebrated its 6000th store in September the same year.

The company also plans to expand further in Southeast Asia.

According to Dr. Guo, CEO, the expansion into Singapore is the company's first step in its expansion into the international markets and is the starting point of its internationalization strategy. The company aims to build its proof of concept overseas by leveraging the brand's professional, youthful, and fashionable image as well as its fresh retail coffee business model.

{kind=link}

By aggressively expanding, the company has managed to capture returning consumer demand and improve brand recognition and visibility. Since its inception, the company boasts 150+ million cumulative transacting consumers, a testament to its strong retention rates.

Dr. Guo remains optimistic about the company's future expansion plans, and the store count in Singapore is expected to reach 10 by the end of April 2023.

Recent Financial Performance

Here, I discuss the company's recent Q1 financial results which can be found here .

In the first quarter of 2023, Luckin Coffee experienced significant growth in its revenue and EBITDA. Specifically, its revenue increased by 20% quarter-over-quarter, rising from 3.6 billion RMB to 4.4 billion RMB.

The company also witnessed an impressive 90% growth in EBITDA, soaring from 416 million RMB to 793 million RMB. Additionally, Luckin Coffee saw a QoQ increase in its EBITDA margins from 11% to 18%, while maintaining a healthy gross margin of 60%.

In comparison, competitor Starbucks achieved lower gross margins of 25% and EBITDA margins of approximately 17%. This discrepancy in margins could prove to be a potential distinguishing factor in the long run as the company continues to expand.

Moreover, Luckin Coffee boasts a strong financial position with a cash balance exceeding 4.4 billion RMB and no significant debt. The company exhibits a current ratio of 2x, indicating its favorable financial health when compared to Starbucks, which has a current ratio of 0.8x.

However, it is worth noting that Luckin Coffee's average cash conversion cycle is 35.4 days, which is higher than Starbucks' more efficient management of working capital, reflected in their average conversion cycle of 20.9 days.

Valuation

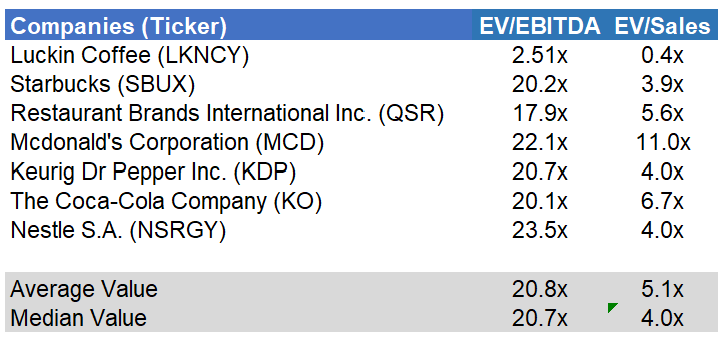

I opted to do a relative valuation analysis of comparable companies, using both the EV/Sales and EV/EBITDA multiples for completeness.

Methodology

Using data from Yahoo Finance, I retrieved the EV/EBITDA and EV/Sales of the below eight companies that cater to the coffee market, or own brands that do.

{kind=link}

I then opted to use the lower of the average and median values, to be as conservative as possible.

EBITDA Multiple

Author's Analysis

Using the median EV/EBITDA multiple of 20.7x, I arrived at a Price/Share of $17.9. This suggests that Luckin Coffee is overvalued at a current price of $21.18.

Understandably, this result is not surprising as Luckin Coffee is still in its growth stages, and has yet to scale its margins relative to its more established competitors.

Sales Multiple

Author's Analysis

For EV/Sales, I used the median value of 4.0x to arrive at a Price/Share of $28.70. This suggests that Luckin Coffee is undervalued as its current Price/Share sits at $21.18.

In my opinion, using the EV/Sales multiple instead of EV/EBITDA for a young company such as Luckin Coffee could provide a more accurate and fair valuation for the company.

Risks

Due to its aggressive expansion plans, Luckin Coffee has a large capital expenditure account which is also forecasted to increase in the near future. This severely affects the liquidity and free cash flow of the company.

If the company cannot scale its topline and remain at healthy margins, its huge investments in expansion and acquisitions could prove to be futile and detrimental to the company.

Lastly, Luckin Coffee has a beta of -0.70 while competitor Starbucks has a beta of 1.04 which suggests that the stock tends to increase in price when the general market price falls and vice versa.

Investor Takeaways

Since 2020, Luckin Coffee has been through multiple "make or break" events such as their accounting scandal, as well the COVID-19 pandemic. While certain investors remain wary and bearish on the stock, the company has shown incredible resilience through their miraculous turnaround and stellar financial results.

Helmed by a lean and experienced management team, I strongly believe that Luckin Coffee is well-positioned for growth and could present immense value for long-term investors willing to tolerate short-term uncertainty.

Hence, I rate Luckin Coffee a "Buy" based on its resilience to macroeconomic conditions, unique value proposition leading to customer stickiness, and strong financial health.

For further details see:

Luckin Coffee: Poised For Redemption