CHIQ - Luckin Coffee: Sturdy Growth But Not A Fan

2023-11-27 14:36:23 ET

Summary

- Luckin Coffee has seen a doubling of its share price over the past year, trouncing the returns of other Chinese consumer discretionary offerings.

- Luckin Coffee is growing at 4x the pace of the market, but we have some concerns with the growth strategy.

- The current risk-reward on the charts does not look too appealing either.

Introduction

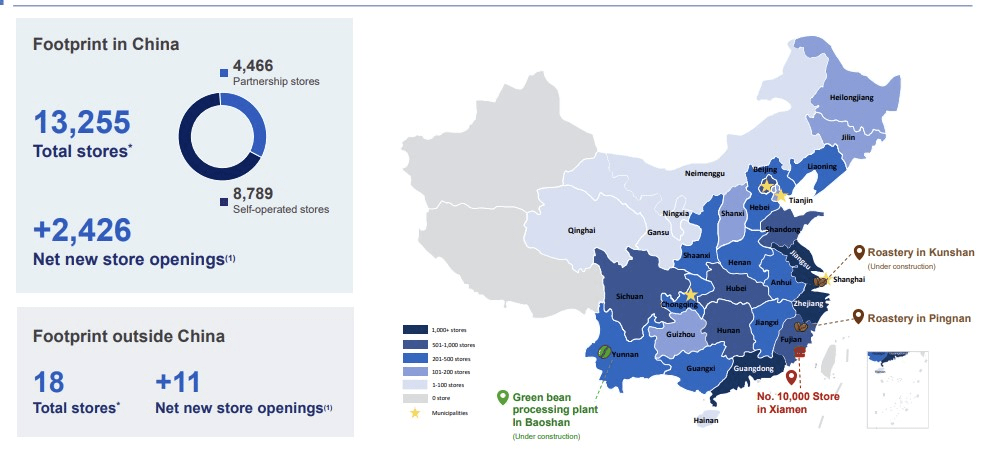

Luckin Coffee (LKNCY) is a Cayman Islands holding company that provides exposure primarily to the fast-growing coffee retail market of China (recently it has taken tentative steps to expand internationally by venturing into the Singapore market. The company has been around since 2017, and since then it has managed to set up over 13,250 stores (the goal is to hit 15,000 stores by the end of this year), with over two-thirds of this consisting of self-operated stores, and the rest accounting for partnerships.

{kind=link}

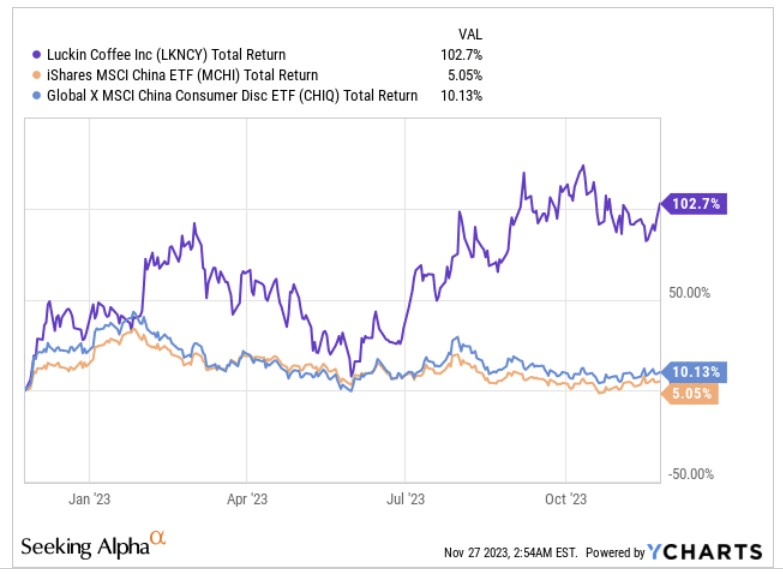

Luckin Coffee's tech-driven retail business model (customer orders are not entertained at the counter, but are placed via an app for either takeaway or delivery) certainly appears to have caught the fancy of investors; this is reiterated in the performance of the ADS which has more than doubled over the past year, at a time when the flagship-MSCI China ETF (MCHI), and the China Consumer Discretionary ETF (CHIQ), have only managed to generate mid-single-digit- to early double-digit returns.

{kind=link}

What's The Big Draw?

So why is the market lapping up this story?

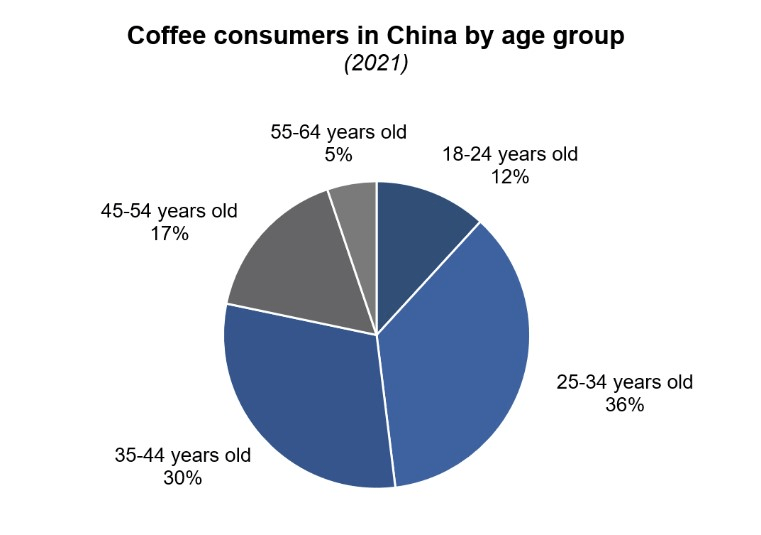

Well, for starters, the coffee market there has been growing at a rapid pace. China may previously have been noted for its ferocious appetite for tea, which reportedly accounts for 40% of global consumption, but don't dismiss the growing predilection of the Chinese youth for accessible luxury experiences such as coffee drinking over luxury goods. What's also key is that close to two-thirds of coffee consumption there takes place amongst impressionable, young Chinese earners with high disposable income (the 25-44 age bracket).

{kind=link}

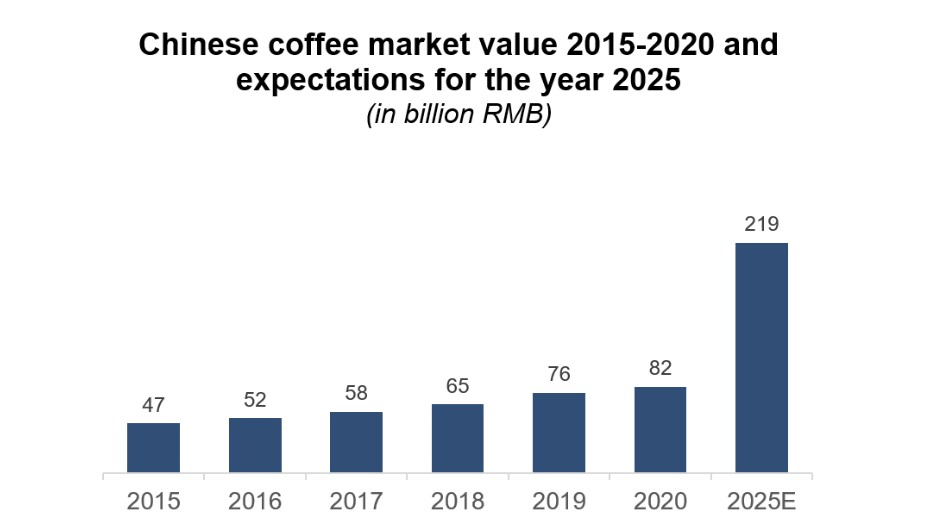

In effect, the Chinese coffee market which was valued at RMB 47bn in FY15 had almost doubled by FY20, and the expectation now is that by 2025, this market could well grow at 22% CAGR and hit RMB 219bn.

{kind=link}

A +20% growth rate is no doubt respectable enough, but that pales in comparison when you consider that our focus stock-Luckin Coffee has been taking share and growing at over 4x the pace of the overall market in recent periods.

Q3 earnings presentation

So, what explains LKNCY's popularity in particular? Well, we believe there are two key trends here that fit well with LKNCY's underlying ethos. The first is that the majority of Chinese coffee consumers have an affinity towards domestic brands (45%, as opposed to just 25% who like foreign brands). Interestingly enough, you'd be interested to know that LKNCY recently also overtook Starbucks ( SBUX ) and became the market leader despite coming to the market 18 years after the latter.

Secondly, you also have the growing trend of tech-driven coffee deliveries (as opposed to visits to the stores), not just in tier-1 Chinese cities, but in tier-2 , and tier-3 cities as well. The convenience that is offered via the delivery app- option of customization, and time-specific delivery (30-minute guarantee at least as far as Luckin is concerned) with no inconvenience of queuing has led to a spike.

Some Concerns

On the face of it, LKNCY looks well-poised to flourish, but we are not overly convinced with the growth strategy that is being pursued. Currently, it looks like LKNCY is pursuing a "growth-at-all-costs" model where the emphasis is not so much on engendering quality or protecting its margins, but just taking share by offering relentless deals.

LKNCY prides itself on the convenience it offers via its mobile app, but a few days back, Business Insider conducted a review, and on the Google Play Store, the app was rated at only 2.5 out of 5 . There also appears to be regular spamming of the app experience by way of frequent pop-ups promoting deals of different sorts. Customers who resort to Luckin have also stated that they've predominantly pursued the brand for the deals that were offered, rather than the quality of the product.

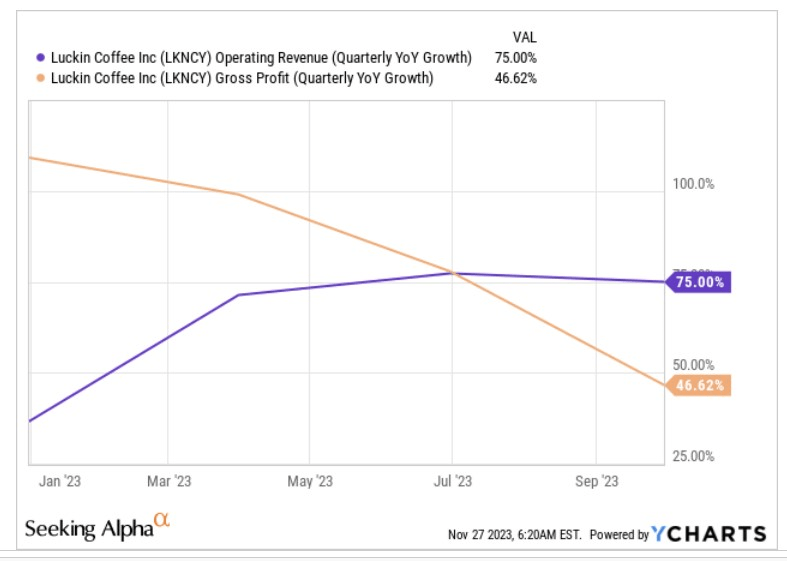

Granted these reviews are based on the Singaporean experience, but yet still, the broad takeaway is that LKNCY has been able to gain traction largely on account of the heavy discounting it indulges in, which will end up dampening gross profit progress. We're seeing the effects of that play out in recent periods (as seen in the image below).

{kind=link}

This strategy could work for brief periods when the market is going through a lull, but this is not something that can be sustained, and eventually, it's the quality and pricing that will help you generate sustainable earnings. Note that on the Q3 call , management confirmed that they will continue to press the pedal with promotion and deals, with margin pressure also likely to be seen on account of seasonality and higher raw material prices.

The other thing to note is that much of the momentum is coming through the rapid pace of new stores (this is not particularly hard to set up as a typical store is just 20-25 square feet, and they run a cashier-less model) whereas existing stores are not quite able to generate the same level of revenue momentum, as saturation takes hold and the quantum of deals and discounts ebb (at established stores). When you seek to establish a high density of stores in a certain area, there's also the risk of cannibalization. Nonetheless, all this is validated in the manner in which the growth rate of average sales per existing store has been trending lower (In Q3 this was down by -6%, worsening from -2.3% in Q2).

KrAsia

Closing Thoughts- Technical Considerations

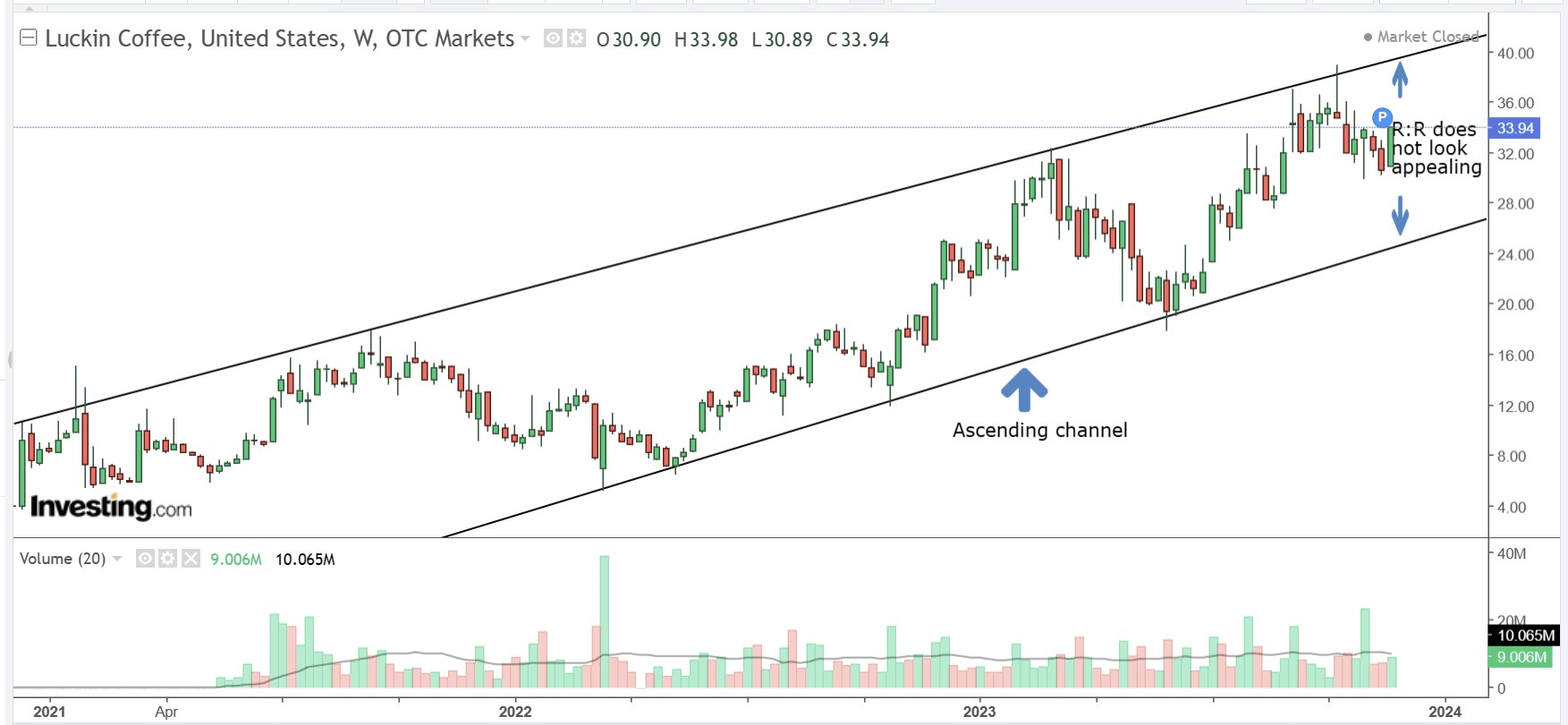

If we switch our attention to LKNCY's charts, we can't say we're too chuffed with the current reward to risk on offer here. The weekly chart of LKNCY shows us that for close to three years, LKNCY has trended up in the shape of a fairly consistent ascending channel. If you'd positioned yourself and exited appropriately at around the channel boundaries, you would have fared rather well. With the stock price around $34, with the channel boundaries at around $39 and $25, the reward to risk looks quite unappealing at less than 1x (0.55x). You ideally want to get in when the R:R is over 1x.

{kind=link}

{kind=link}

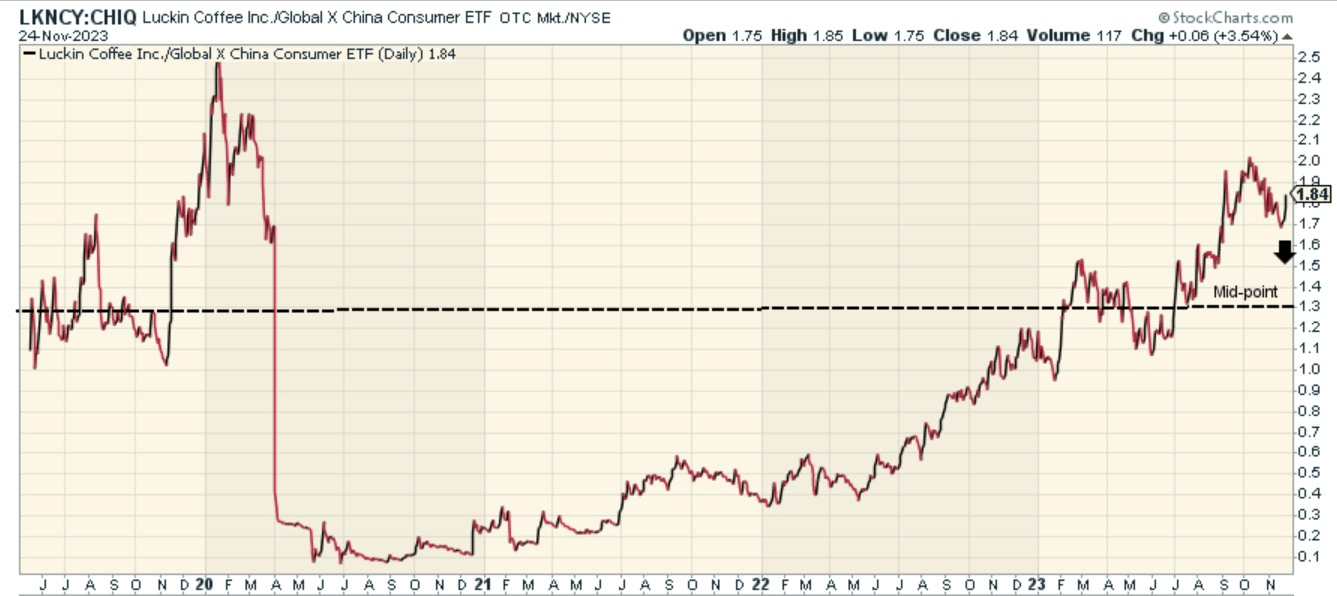

Then, it's also difficult to envisage LKNCY benefitting from further rotational momentum for those interested in the Chinese consumer discretionary landscape. The chart above highlights how the LKNCY's relative strength versus the CHIQ ETF could've benefitted from some mean-reversion momentum in H1 as it was trading around 25% off the mid-point of the long-term range. That narrative is no longer in play, with the ratio now trading towards the upper half of the long-term range.

For further details see:

Luckin Coffee: Sturdy Growth, But Not A Fan