DLAKY - Lufthansa Stock Is Aligned For Profitable Growth

2023-08-13 08:08:08 ET

Summary

- Lufthansa saw a 14% increase in passenger volume and a 17% increase in revenues in Q2 2023.

- Cargo revenues dropped by 43% while MRO revenues increased by 26%.

- Lufthansa expects further recovery in Q3 and predicts capacity to recover up to 85% in 2023.

Lufthansa (DLAKY) has been one of the European airlines that stood out for me, because of the way the company manages its liquidity and debt. I’ve been flying with Lufthansa Group airlines several times since the pandemic and all I can say is that the price-quality profile is underwhelming. So, as a passenger I am certainly not thrilled by what the Lufthansa Group offers paying customers, but the company knows what it can offer to customers to make them stick and at the same time somewhat compete with low-cost carriers on the European mainland. Overall, I do believe that management has been executing well, and as it deleverages and refocuses the company, a simplified Lufthansa Group should be able to compete more efficiently. In this report, I will analyze the second quarter results.

Lufthansa Turnaround In Full Swing

{kind=link}

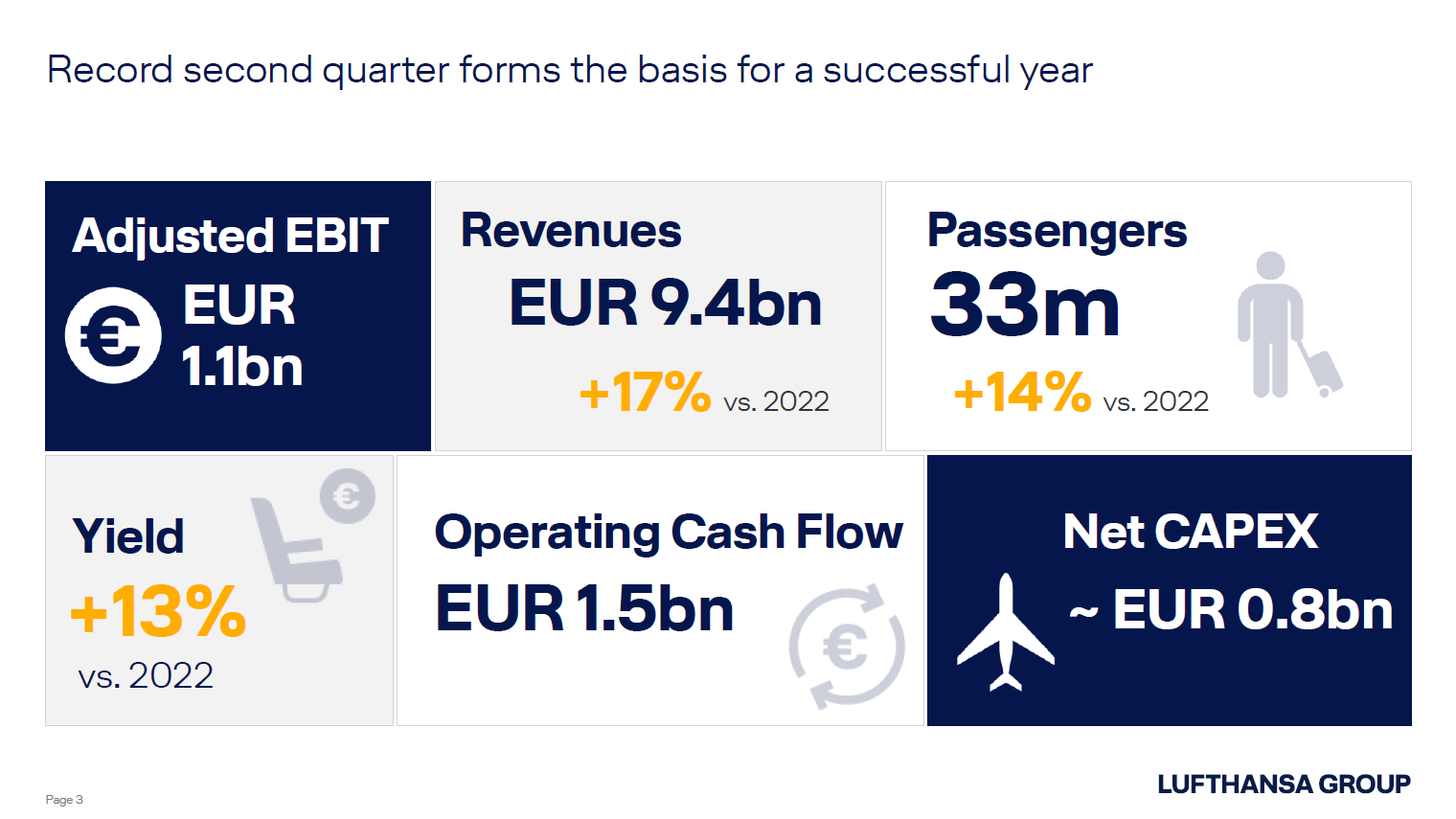

The slide above captures the key figures for Lufthansa in the second quarter of 2023. The company saw passenger volume increase by 14% to 33 million resulting in 17% higher revenues driven by a 13% expansion in yield and even 25% compared to pre-pandemic levels.

Lufthansa’s Cargo revenues dropped 43% to €712 million while adjusted EBIT dropped by 92% to €37 million as the cargo unit revenues are normalizing and consumers have grown more cautious towards spending while remaining spending is often used for travel. MRO revenues increased by 26% to €1.591 billion while adjusted EBIT grew 39% to €156 million. The catering business, for which the sale will be completed in the third quarter of this year, saw a 21% increase in revenues to €584 million while adjusted EBIT increased from €1 million to €15 million. The disposal of this business will significantly simplify Lufthansa’s structure as the catering unit includes 160 businesses and has not been a high margin business.

{kind=link}

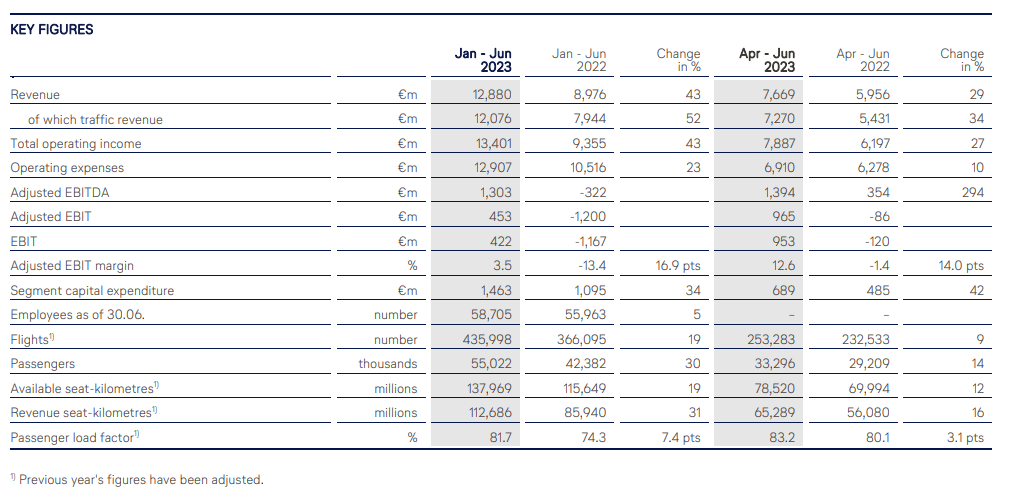

For the second quarter, the Lufthansa Group airlines saw capacity increase by 12% and load factors expand by 3.1 points, which together with 13.1% higher yield resulted in a 34% increase in traffic revenues. Adjusted EBITDA increased by 294% with EBIT margins improving 14 points to 12.6%.

{kind=link}

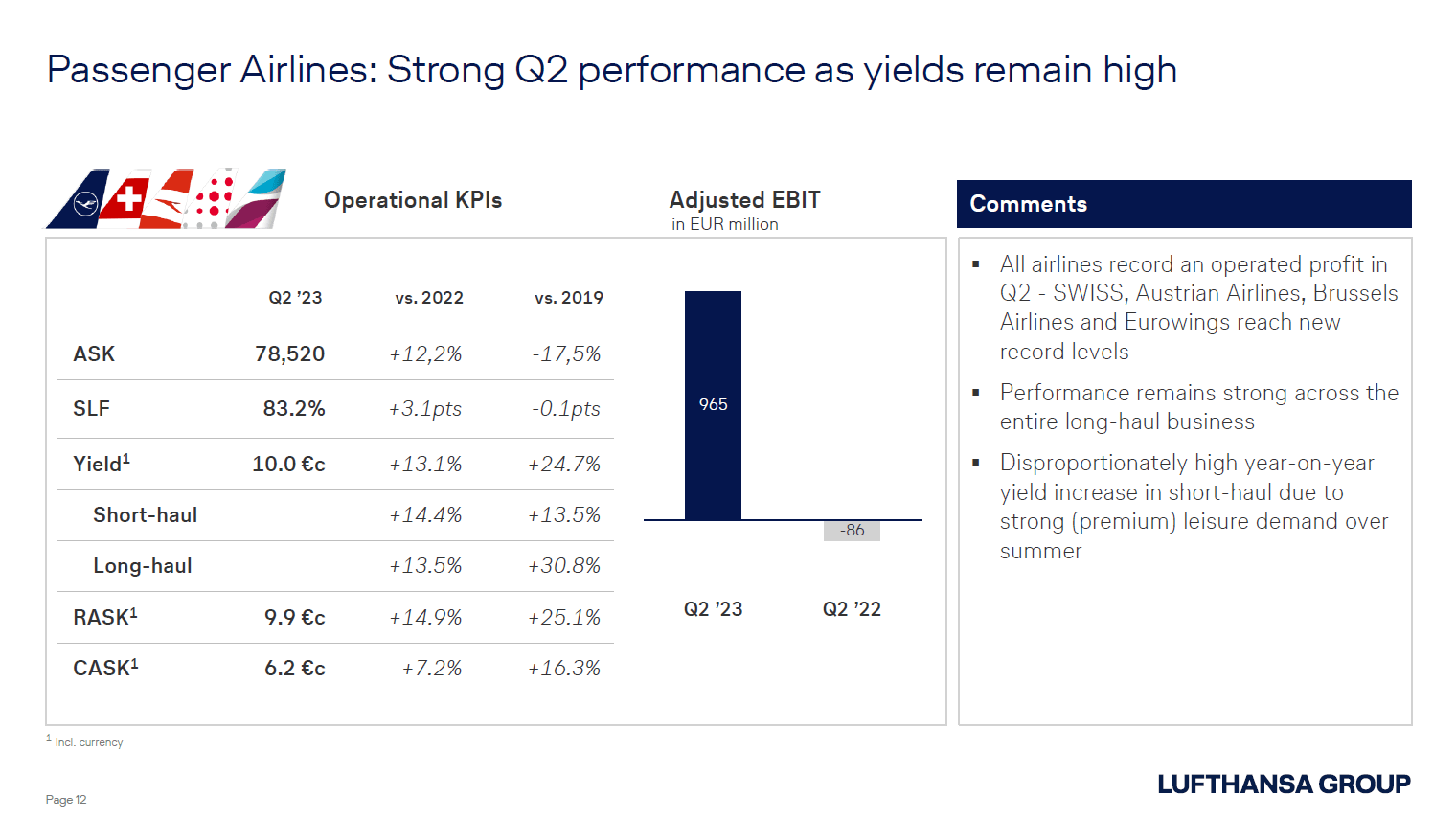

Lufthansa carried 14% more passengers and that translated into 34% higher revenues supported by a better unit revenue which was nearly 15% higher and the yields were 13.1% higher year-over-year with strength shown in the short-haul and long-haul operations. While capacity expanded 12.2%, the unit costs excluding fuel increased by around 7% and decline is only expected next year and on quarterly basis we should be seeing some decline by Q4.

Interestingly, there still remains significant recovery ahead as Q2 2023 passengers flown was only 86% recovered while premium and non-premium leisure are almost fully recovered but corporate, both in the premium and non-premium segment, remain only 60% recovered. So in business travel and long-haul travel to Asia we do see some additional levers to further improve results.

Lufthansa: Superior Debt Management

{kind=link}

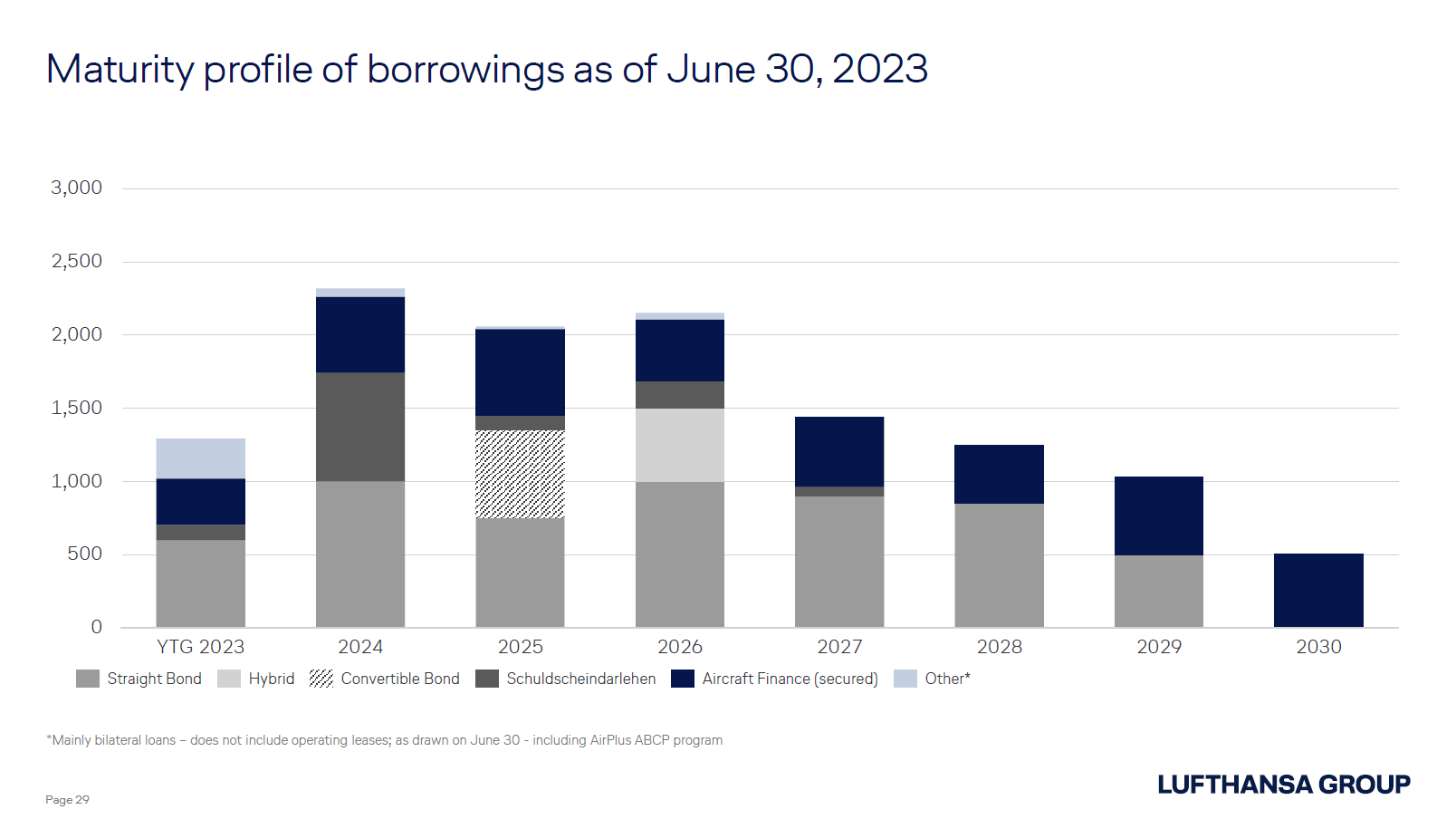

Looking at the profile of the maturities, including aircraft financing, we do see that Lufthansa doesn't have a clear runway, but with the current liquidity, Lufthansa can cover its debt maturities up to and including 2027. In one of my previous reports on Lufthansa, I noted that the years 2025-2026 would be more challenging as its debt maturities were concentrated in those years. What we are seeing is that instead of significantly reducing the near-term maturities early, the company has elected to reduce the debt in 2025-2026 by roughly €1 billion. As the 2023 debt matures, Lufthansa will reduce the debt there obviously, but I also see possibilities for the airline to reduce the 2024-2026 debt to €1.5 billion annually which can be seen as a de-risk and a smoother maturity profile for the business. With €10.8 billion in available liquidity, the business can obviously turn to cash to reduce the debt but it may also be willing to refinance debt with maturity around 2030.

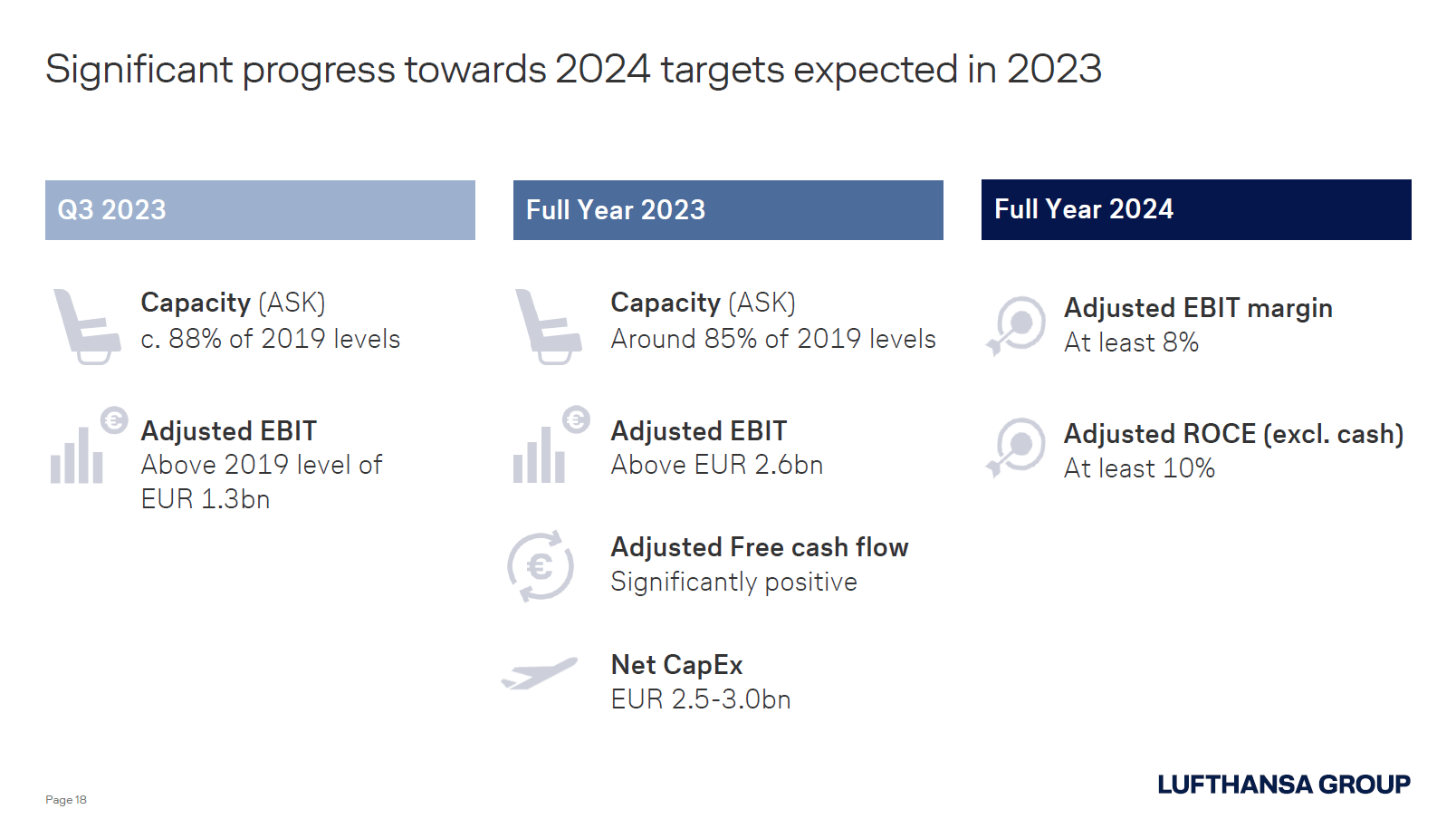

Lufthansa Guides For Further Recovery

{kind=link}

In the third quarter, Lufthansa expects capacity to be 88% recovered with adjusted EBIT soundly above the 2019 levels. For 2023, Lufthansa now expects capacity to recover to up to 85% from 85% to 90% earlier with adjusted EBIT significantly above €2.6 billion and positive free cash flow. Growth drivers for Lufthansa will be the recovery in the Asia-Pacific region as well as improvement in corporate travel volumes while unit costs will start to moderate and decline by year-end.

Is Lufthansa Stock A Buy?

{kind=link}

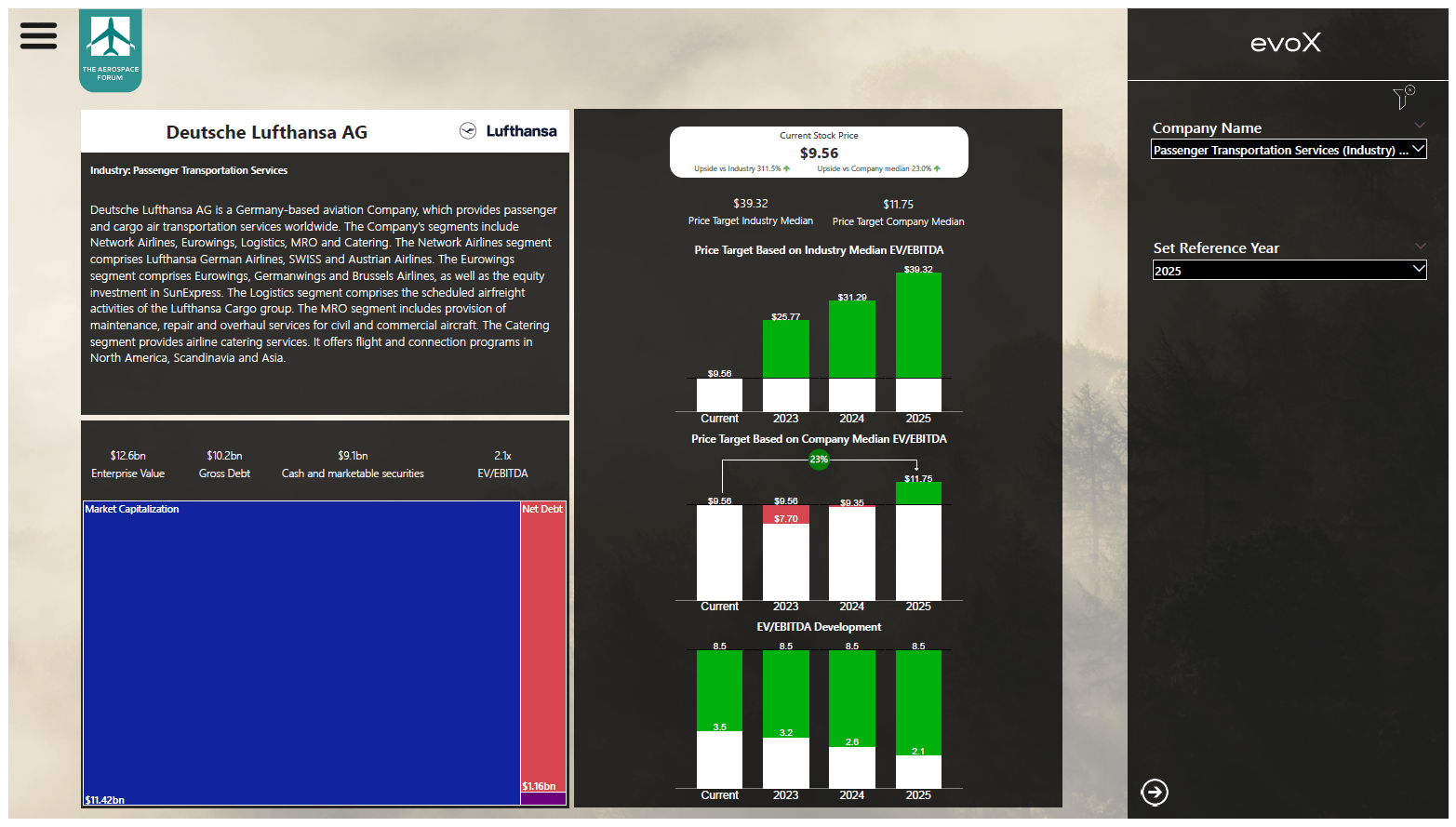

Valuing Lufthansa stock is quite challenging as the company tends to trade against a discount compared to peers and it is currently simplifying its operations by disposing the catering business and later this year it could spin off part of the MRO business, which I believe will positively enhance the value of the business. Perhaps that will unlock some upside by justifying a higher multiple for Lufthansa to trade at. Lufthansa’s 2023 and 2024 expected results are currently fully priced in at a lower multiple that the company tends to trade at. With 2025 earnings in mind, which I think is justifiable to include in today’s stock price given the low EV-EBITDA ratio, around 23% upside remains which is in line with the 27.35% upside that Wall Street analysts see in the name.

Conclusion: Lufthansa Stock Remains A Buy

Lufthansa most definitely is not my favorite airline to fly given the company’s underwhelming product on the European network against its pricing. However, the group is far more than a European network and I believe the company is becoming a more attractive carrier on international routes and is simplifying its structure while prudently retiring debt and maintaining a strong liquidity position. Compared to peers, Lufthansa is significantly undervalued, and even if we accept that and factor in 2025 earnings against Lufthansa’s low EV-EBITDA multiple, significant upside continues to exist for the name.

For further details see:

Lufthansa Stock Is Aligned For Profitable Growth