ADDDF - Lululemon: Solid Growth Appears Here To Stay

2023-03-29 11:17:27 ET

Summary

- Lululemon Athletica Inc. is my top pick in the apparel clothing sector as it shows very impressive margins, brand strength, and has a long runway of growth ahead of it.

- Q4 2022 results were above the Wall Street consensus as growth remained strong, despite somewhat lower margins.

- Even more impressive was the outlook given off by management, which guided for strong double-digit growth for FY23, blowing away the consensus.

- Management remained confident that it can keep executing on its growth strategy and deliver $12.5 billion in revenue by FY26. I believe it can do even better.

- Despite my sheer enthusiasm about Lululemon, I rate the company a hold right now as the big jump in share price at the opening of the market leaves very little upside based on my EPS estimates.

Introduction

I covered Lululemon Athletica Inc. (LULU) back in December, when I called it my favorite apparel stock based on a strong growth strategy and management team. Lululemon is very well positioned to show strong growth over the next several years, driven by its focus on growing its international presence, focus on man's apparel, and growth of its digital platform. Yet, despite my enthusiasm, I rated the company a hold , as the company was priced for perfection back in December. I concluded the following back then:

The company has incredible plans for continued growth and is very well positioned to become a threat to industry giants such as Nike and Adidas. I like Lululemon for its products, incredible management, strong growth prospects, and international potential. At the same time, the valuation is a difficult one as I feel like the company was way better value at around 30x P/E which it was not so long ago. The recent significant increase in share price has made the stock expensive and therefore has more downside risk than it has upside potential.

Yesterday, March 28, Lululemon released its 4Q22 results and managed to outperform both the top and bottom-line Wall Street consensus. EPS beat by $0.14 and revenue by just $100 million. Lululemon managed to report this strong beat even though back in January the company warned of lower margins due to some markdowns in the quarter as a result of slightly falling demand. This resulted in some worries among investors on whether the company would be able to maintain its strong growth rate, bringing down the share price. This is what I said about this share price decline in an article I wrote in December :

In my eyes, the 10% drop of Lululemon Athletica Inc. on the 9th of January was simply an overreaction by the market, and this has created a nice buying opportunity for long-term investors. The company continues to be a dominant force in the athletic apparel industry, driven by a strong brand.

And Lululemon showed that this, indeed, was an overreaction. Despite decreasing margins, Lululemon showed an impressive result once more during its latest quarter as growth remained resilient. In addition to this, the outlook for FY23 from management came in above the consensus, contributing to the bullish sentiment on the shares after the earnings release. At the time of writing this article, shares are up over 13%, bringing the share price back to the highs from December last year and up over 16% since my January buy call. Following this earnings release and jump in share price, in this article, I will revisit my outlook, rating, and thesis on the company by diving into its latest financial results and outlook for FY23.

Quarterly Review

Lululemon reported revenue of $2.8 billion for its 4Q22 , up by a very impressive 30% YoY and above its 3-year CAGR of 26%. Transactions among existing customers grew 30% YoY and, even more impressive, new customer transactions increased by 30% YoY, showing Lululemon is rapidly expanding its brand among new customers. From personal experience, I can confirm that once you buy Lululemon clothing, it is hard to switch back to the likes of Nike, Inc. ( NKE ) or Adidas AG ( ADDYY ).

Moreover, this top-line growth shows that demand for Lululemon products remains strong and does not seem to be impacted by lower consumer spending and high inflation. Company-operated store revenue was $1.1 billion (40% of revenue) and grew by 15% YoY due to increased traffic of 30% and the opening of 32 new stores with 16 new stores in North America, 14 new stores in Asia Pacific, and 2 in Europe, bringing its total store count to 655. Lululemon keeps increasing its store count at a rapid pace to increase its brand exposure and penetrate new markets in both Europe and Asia as part of its power of three 2x growth strategy. Through this strategy, Lululemon aims to double its revenues by FY26 which would result in revenue of $12.5 billion. With this strategy, Lululemon focuses on market expansion, product innovation, and guest experience. Yet, for a more in-depth analysis of this strategy, I recommend reading my December article, in which I dive into this in particular. With the first year of this new strategy now completed, we can see Lululemon is very well underway to achieve its goal. This is what management said about this :

As you know, we launched our new five-year Power of Three x2 growth plan last spring. At the highest level, this plan assumes 15% CAGR revenue growth and modest operating margin expansion annually. In 2022, our revenue increased by 30% compared to 2021 and 27% on a three-year CAGR basis. Adjusted operating margin increased 10 basis points, while adjusted EPS increased 29% and 27% on a one and three-year CAGR basis, respectively.

Lululemon store count (Statista)

Back to the financial results and we can see that Lululemon managed to report solid e-commerce revenue of $1.4 billion (51.8% of revenue), up 37% YoY, driven by increased online traffic of 45%. This is down from a three-year CAGR of 46% with covid-19 tailwinds disappearing for the online business. Still, e-commerce outpaced in-store sales, which illustrates the focus on digital of Lululemon. Lululemon aims to double international revenue by FY26 as part of its growth strategy, and it sure looks well underway.

Growth for Lululemon was also strong across the board. Lululemon reported 26% growth for the men's segment, in addition to 24% growth for the much larger women's segment, and 44% growth in accessories. Lululemon has always been more focused on women's apparel, which is why it aims to increase its share in men's apparel as well, and these growth rates show that it can take market share here. Both product segments managed to report growth in line with the 3-year growth CAGR, showing very consistent growth as well.

A similar thing can be said about its growth by region as well, as growth in the U.S. remained strong at 24%, but international growth is increasing in importance with this growing by 39% YoY, also both in line with the 3-year CAGR. This shows that Lululemon is showing steady growth in a tough operating environment as it keeps increasing its international presence. Still, the company is also increasing its position in the U.S. apparel market, as the company gained 2.3 percentage points of market share in the U.S. in 2022 according to NPD Group's Consumer Tracking service, driven by new product releases and improved brand awareness. The U.S. continues to be a key market for Lululemon to drive growth as it expands its brand to other regions in the world where it is increasing its brand awareness.

For example, in Australia brand awareness grew by 5 percentage points to 24%, in the UK Lululemon is now a familiar brand among 6% of the population, and in China, this grew to 9%. And whereas these increases are great, it also highlights just how much potential is still there for Lululemon. China in particular could turn out as a great growth driver for Lululemon as the Chinese sports apparel industry is expected to grow at an 11% CAGR , compared to just a 2.5% CAGR for the U.S. Overall, Lululemon aims to quadruple its international revenues by FY26 as it continues to increase its presence in both China and Europe.

Moving on to the bottom line, Lululemon reported a gross profit of $1.59 billion which represents a gross margin of 57.4%, down from 58.1% last year. Net income was $563 million or $4.40 per share ((EPS)), up a very solid 31% despite some margin headwinds. As mentioned in the introduction, Lululemon already warned about some weakness in its margins back in January, and margins indeed came in somewhat lower than anticipated, but remained strong overall.

The decline was primarily driven by higher markdowns which were up 40 basis points YoY and flat over the full year. Still, considering the number of markdowns we saw for Nike, this is not bad at all. Yet, inventories increased by 50% YoY to $1.4 billion which is not as positive and in line with what we see at other retailers. Still, management is happy with these inventory levels and expects the inventory growth rate to moderate over 2023 while maintaining the full price selling model as management sees no need for additional markdowns. As for the rest of the balance sheet , Lululemon holds $1.2 billion in cash and cash equivalents and still has $744 million remaining under the $1 billion share repurchase program, which will boost EPS growth over 2023.

Outlook & Valuation

While Lululemon management remains mindful in light of the ongoing macro uncertainties, they are excited about the Q1 sales trend which results in upbeat guidance for FY23. Management guides for revenue to be between $9.3 billion to $9.41 billion which represents growth of 15-16% YoY. Considering the strong performance in 2022 and ongoing headwinds, this is a very strong outlook from management, illustrating strong continued growth. FY23 guidance is also above the $9.14B consensus, requiring Wall Street analysts to upgrade their projections and price targets. Also, these growth rates are still in line to slightly better than the Power of Three x2 growth plan, keeping Lululemon ahead of its targets. Moving on to the bottom line, Lululemon expects to increase margins between 140 basis points to 160 basis points YoY which is predominantly driven by lower air freight expenses and markdowns in line with 2019, and down slightly YoY. This means EPS is expected to be in the range of $11.50 to $11.72, excluding the future impact of share repurchases, against a consensus of $11.30.

In addition to an already very strong outlook, Lululemon also plans to continue investing in its growth pillars at a strong pace. As a result, management expects to open 45 to 50 new stores in 2023 and grow square footage in the low double digits. Of these new stores, 30 to 35 will be located in international markets, with the majority of these planned for China. I believe this focus on expanding exposure in China is a good one from management and will drive strong continued growth in this region and for Lululemon overall as it increases its share of the revenue.

So, what does this mean for 1Q23? Lululemon expects to report revenue in the range of $1.89 billion to $1.93 billion ($1.85B consensus), representing growth of 17-20% YoY. The gross margin is expected to improve by 290 basis points to 320 basis points YoY which, again, will be driven by lower air freight expenses. As a result, EPS is expected to come in between $1.93 to $2,

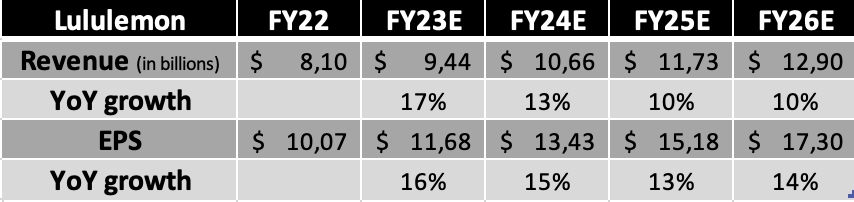

Now, following my deep dive into the company and all the aspects laid out above, I arrive at the following financial expectations for the years until FY26.

{kind=link}

(My 1Q23 estimate: revenue of $1.94 billion and EPS of $1.99 vs consensus of $1.92 billion and $1.98.)

Shortly explaining these estimates, I expect Lululemon to report revenue and EPS at the high end of guidance by management due to a better-than-expected macro climate and margin improvements. For the years after, I expect Lululemon to continue growing at a steady pace, but with a somewhat moderating growth rate as the business grows. I do expect Lululemon to keep focusing on margin improvement driven by higher revenue and faster EPS growth through cost savings and share repurchases.

Based on the current premarket share price of $366 and the current analyst EPS estimate, Lululemon is currently valued at a forward P/E of 32x which is quite rich, even for a strong growth company like Lululemon. Still, with Lululemon executing to perfection and having a long runway of growth ahead, I believe it does deserve a valuation of around 30x forward earnings. Therefore, based on my own EPS estimate for FY24, I calculate a target price of $403 per share. With a current premarket share price of $366, this leaves investors with just a 10% upside potential. As for comparison, 33 Wall Street analysts currently maintain a price target of $377 combined with a buy rating.

Conclusion

Overall, Lululemon Athletica Inc. delivered an excellent 4Q22 with steady top and bottom-line growth and no slowdown visible, despite the tough operating environment. Management continues to execute its growth strategy, and Lululemon looks well underway to achieve its FY26 revenue targets. Growth is strong across all product categories and regions, with increased growth in international markets and its digital channels. As a result, Lululemon easily outperformed Wall Street analyst expectations. While margins are experiencing some near-term weakness as a result of somewhat higher markdowns, I don't believe this is something investors need to worry about as the long-term margin outlook remains strong.

The outlook given off by management for both 1Q23 and FY23 was easily above the Wall Street consensus and shows strong continued growth rates. As a result, I remain confident in the long-term growth of Lululemon as illustrated by my growth expectations until FY26. Yet, the stock is quite expensive when taking into consideration the big jump in the share price. Based on my FY24 EPS estimate, which is slightly above the analyst consensus, I calculate a target price of $403, leaving an upside of only 10% for investors over the next two years.

Considering Lululemon is still very much a growth stock, despite its strong brand, I believe 10% does not offer sufficient upside potential to maintain my buy rating on the company. While I remain very bullish on Lululemon Athletica Inc. in the long term driven by its excellent management team, growth strategy, brand strength, and long runway of growth in international markets, the company is currently priced above perfection. Therefore, I recommend investors stay on the Lululemon Athletica Inc. sidelines for now and wait for a better entry point, possibly in the coming weeks, before adding to an existing position or initiating one.

I rate Lululemon Athletica Inc. a hold and recommend looking for prices below $345 per share.

For further details see:

Lululemon: Solid Growth Appears Here To Stay