LULU - Lululemon: Strong Brand Fierce Competition

2023-10-16 10:31:19 ET

Summary

- Lululemon is a sportswear company with impressive financial metrics and a strong brand recognition.

- The company is expanding into new categories, including men's apparel, footwear, and accessories.

- Lululemon aims to double its men's segment, increase its digital direct-to-consumer business, and quadruple its international business by 2026.

- To achieve its objectives, Lulu has established a three-pillar program: Product Innovation, Guest Experience, and Market Expansion. This strategy is geared toward driving growth and enhancing the brand's presence.

- Last week, I compared Lululemon to Nike in an article. The research for that piece piqued my interest, prompting me to dig even deeper into Lululemon's business.

Same Thesis, More Answers

Today, we will delve into what I consider one of the most intriguing opportunities on Wall Street. Last week, I compared Lululemon ( LULU ) to Nike ( NKE ) in an article . The research for that piece piqued my interest, prompting me to dig even deeper into Lululemon's business. I aimed to answer whether it has a moat that justifies its price. You will find those answers in the following article. Last week, I rated Lululemon as a BUY. As I delved deeper into the business, I felt the need to provide you with more answers. Rest assured, my opinion remains the same, and I continue to recommend it as a BUY.

Lululemon is a sportswear company that primarily targets women but is extending its reach into other categories, as we will soon explore. Lululemon boasts impressive financial metrics, including remarkable growth, pricing power, high returns on capital, and a robust balance sheet. Its strength is primarily derived from the exceptional quality of its products and its strong brand recognition, appealing to both adults and teenagers. Beyond these notable attributes, we must address crucial questions: What is Lululemon's competitive advantage? What constitutes its moat? Can brand recognition alone sustain its pricing power? Is this pricing power sustainable over the long term? Does the future hold a trajectory resembling Under Armour's ( UA ), or is it more aligned with the path of the next Nike?

Lulu's Business

Lululemon has been a remarkable compounder over the years, achieving this status through several key factors that we will explore. Lululemon primarily operates in the sportswear industry, offering high-quality, innovative apparel tailored to its most loyal customer base: women. The company is also in the process of expanding into the men's category and diversifying its product offerings, which now include footwear and accessories.

Founded in Vancouver, Canada, in 1998 by the controversial figure, Chip Wilson, Lululemon's core mission was to provide workout apparel that not only enhanced performance but also made the wearer look good. The brand is renowned for its use of high-quality fabrics, innovative yoga pants, and notably, a premium price point exceeding $100 . This pricing power is a rare achievement, placing Lululemon's products at the intersection of luxury and regular apparel. They have become a status symbol for adults and a popular choice among teenagers, as we will further delve into.

Lululemon's appeal revolves around the concept of looking fashionable during workouts and having the versatility to wear yoga pants or a sweatshirt hoodie in various settings beyond the gym or yoga class.

Lululemon's brand power, which I consider its primary strength, is built upon community-based marketing and the practice of treating customers as honored guests. Furthermore, the management is highly committed to preserving and nurturing this brand power, as underscored in the 2022 10-K statement:

Our brand continues to resonate across geographies and cultures, and we remain focused on building global brand awareness while ensuring local relevance

Lululemon has successfully evolved from a brand that started 25 years ago to becoming a multigenerational company. Both adults and teenagers, who typically have different tastes, now appreciate its products and the brand. Notably, teenagers, who represent the future adult customer base, have a strong affinity for the brand. In fact, they rank Lululemon as their third most preferred brand, following only Nike and American Eagle (AEO), even though American Eagle is not a direct competitor of Lululemon. This brand power plays a pivotal role, as it directly contributes to Lululemon's pricing power. This is reflected in the company's resilience during challenging economic periods, as its top-line performance remains relatively unaffected, even though apparel is often one of the first product categories consumers cut back on in tough economic times.

Growth Plans and Objectives

Lulu's growth goals include doubling its men's segment, doubling its digital direct-to-consumer business, which accounted for 40% of the rev as of Q2, and quadrupling its international business, which is growing rapidly but currently represents a small fraction of the North American business. In terms of numbers, Lulu has set a goal to increase its revenue from $6.25 billion in 2021 to $12.5 billion by 2026, representing an achievable 14% CAGR.

To attain these objectives, Lulu has established a three-pillar program to fuel its growth: Product Innovation, Guest Experience, and Market Expansion.

1. Product Innovation: Lulu must prioritize innovation across various segments, including technical advancements, fabric development, and new categories such as golf, tennis, and hiking. A particular area of interest is the exploration of footwear.

2. Guest Experience: Enhancing the guest experience will involve collaborations with influencers, coaches, athletes, and various activities. Additionally, Lulu offers a membership program, second-hand replacements, studio experiences, and digital applications to enrich the overall customer experience.

3. Market Expansion: Lulu's growth strategy includes geographical and global expansion, with a specific focus on the vast Asian markets and the affluent European market. Collaborations with athletes and an understanding of diverse consumer behaviors around the world will be essential for success.

Moat Presence Amidst Intense Competition

The primary question that concerns me is whether Lulu will be able to outmaneuver its competition in the future. While it's a significant player, it doesn't have the same level of robustness and extensive reach as Nike. Competitors abound in all the segments Lulu operates in, each striving to differentiate itself in various ways. Brands like Athleta ( GPS ), Alo, Gymshark, Fabletics, Beyond Yoga, and many others are in the mix. Furthermore, intense competition also stems from industry giants, notably Nike, adidas ( ADDYY ), Puma ( PMMAF ), and Under Armour.

Lulu's management emphasizes innovation, product quality, brand prestige, and a loyal customer base as competitive advantages. So far, these strategies have been effective in maintaining healthy profit margins. However, the question remains: can Lulu sustain this advantage as other brands grow? Will Lulu continue to stay relevant?

Lulu is not a new company, and consumer preferences are evolving. Therefore, I believe it's crucial for Lulu to expand into new markets and diversify its product portfolio, although such moves may risk diverting attention from what has brought them success thus far. While Lulu enjoys a strong brand reputation and a first-mover advantage, it doesn't have the same dominance as Nike, and this is a source of concern for me. I prefer to invest in companies with a wider moat than Lulu's, but its financial performance is impressive. I am cautious about facing a situation similar to Under Armour's and want to avoid that outcome.

It can be challenging to pinpoint a clear competitor among smaller brands, particularly since most of them are not publicly traded. I find the Instagram indicator to be quite useful. By checking the number of followers for each brand on Instagram, you can gauge their global popularity. To provide a benchmark, consider that Nike, as the most prominent brand, boasts 305 million followers. Lululemon, with 4.7 million followers, is no slouch, but it's worth noting that smaller brands in terms of revenue, like Gymshark, have more followers, which raises concerns.

Brands such as Alo are also steadily gaining followers, and it's important to observe the growth rate of their followers to gauge who is gaining popularity and potentially market share. While Lululemon has a strong presence in North America, there's room for expansion on the global stage, especially as other companies focus on markets beyond the United States.

To provide an anecdotal example in the style of Peter Lynch, in the country where I reside, Israel, Alo Yoga is a robust brand, and many women I know prefer it over Lululemon. This reflects the brand's strength and local popularity in various regions.

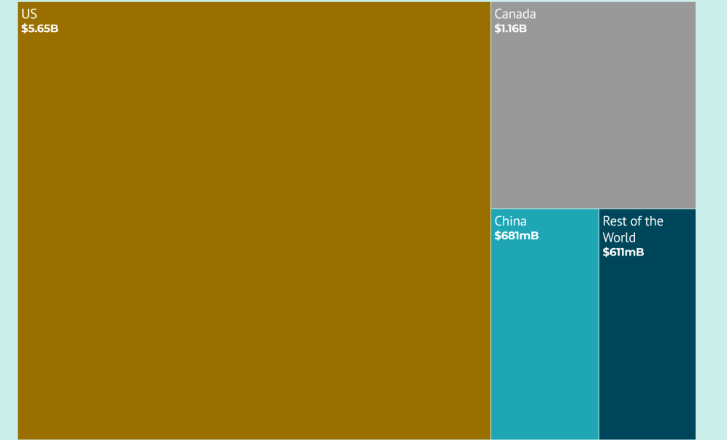

In Q2 of this year, we observed significant global growth for the company, with sales outside of North America experiencing a remarkable 52% surge, and China's sales registering a substantial 61% increase. However, it's crucial to acknowledge that sales outside of North America still constitute a relatively small percentage of the overall revenue pie.

revenue by geography (fourweekmba)

{kind=link}

Superb Financials

In my view, there are a few critical points in the company's financial performance that are essential for stock outperformance:

1. Revenue growth2. Free cash flow growth3. High returns on capital4. Margin expansion5. Returns to shareholders

To assess growth, we will examine several factors. First, we will consider same-store sales, which showed a robust growth rate of 9% . In my view, it is essential to strengthen same-store sales rather than relying solely on new store openings. In Q2, the company achieved a remarkable 20% growth on a constant dollar basis, which is particularly impressive given the current economic conditions. Lululemon's growth over the last five years has been outstanding, with a 24% CAGR. Considering the management's goal to reach $12.5 billion in revenue by 2026, which represents a 14% CAGR, this target appears quite reasonable.

The company has succeeded in growing its cash flow at a rate that closely matches its revenue growth. This alignment suggests limited margin expansion, a point of concern for me. However, it's important to note that Lululemon's pricing power has already delivered strong margins. Additionally, we should take into account the growth of free cash flow per share, which can be enhanced through share repurchases and potentially achieve up to a 20% FCF CAGR.

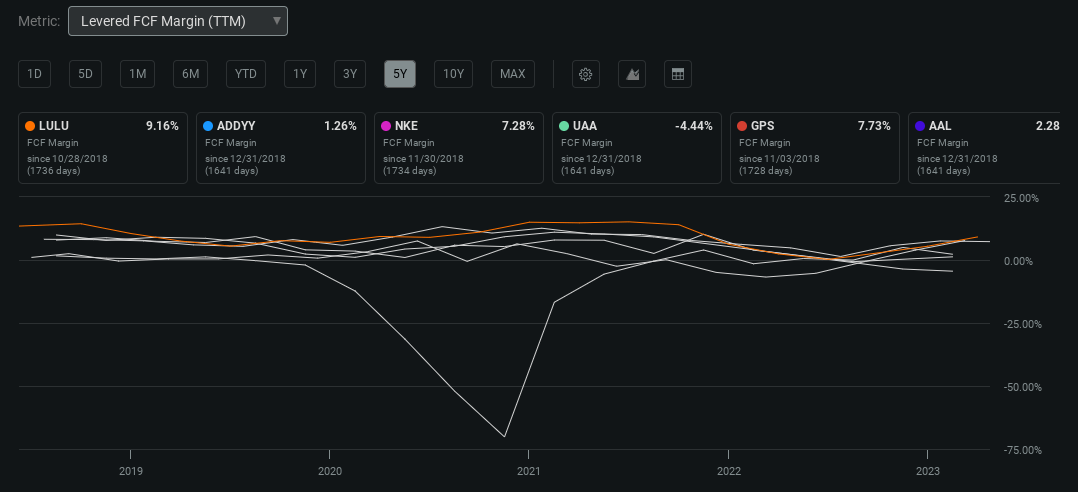

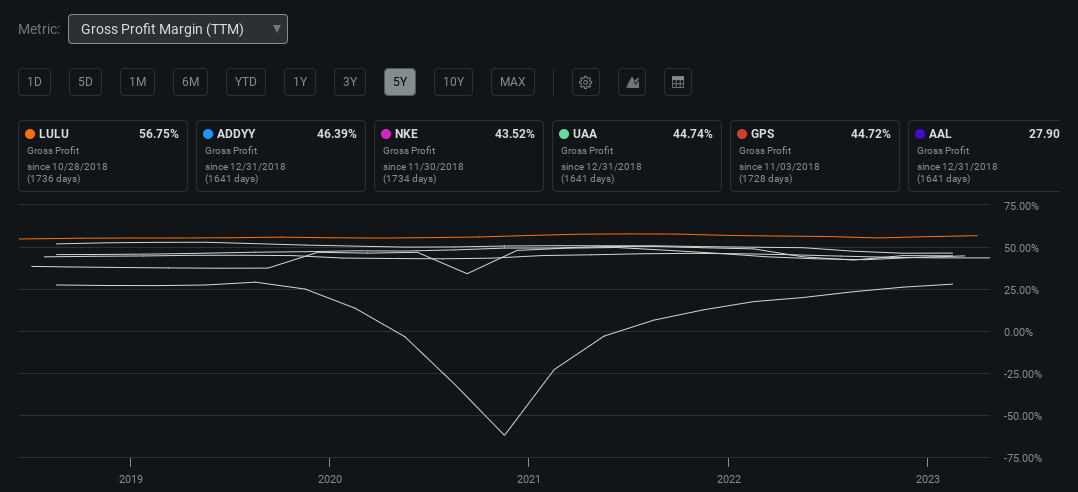

As mentioned earlier, Lululemon boasts excellent margins for an apparel company. For comparison, let's examine the following charts:

FCF Margins (Seeking Alpha) Gross margins (Seeking Alpha)

{kind=link}

{kind=link}

However, there has been no margin expansion for an extended period of time, which is a matter of concern for me. I would like to see the management address this issue.

The high margins are a result of Lululemon not operating its manufacturing facility; instead, most of its production occurs at vendors in East Asia. Furthermore, the primary reason for these high margins is the premium pricing of its high-quality products, with many items priced above $100.

In the last quarter, Lululemon opened 10 new stores, bringing the total number of stores to 672 by the end of the quarter. This is an essential point to highlight—we not only want to see growth in the number of stores but also an increase in same-store sales.

ROC

In addition to its robust revenue growth, I believe that the key reason for Lululemon outperforming the benchmark, particularly after its recent inclusion in the S&P, is its superb returns on capital. These returns significantly exceed the cost of capital and also surpass those of its competitors.

Let's take a closer look at both the ROIC (Return on Invested Capital) and the ROCE (Return on Capital Employed). These are critical indicators, highly regarded by many renowned investors, including Charlie Munger and Terry Smith.

Lululemon does not pay dividends, which is typical for a growth-oriented company. While it has bought back some of its shares, it cannot be classified as a share cannibal. This is not a negative point, especially considering that Lululemon's shares have often been relatively expensive. In my view, the current period presents an opportune time for share repurchases.

Solvency

Lululemon maintains a robust balance sheet with no long-term debt and over a billion dollars in cash. Its only long-term obligations pertain to leases for its stores and distribution centers. Furthermore, the company's short-term balance is solid, boasting a current ratio exceeding 2 and a quick ratio close to 1.

Moreover

Lululemon demonstrates linear revenue growth, which, in my opinion, suggests a robust secular brand. Consumers continue to purchase expensive yoga pants even during challenging economic times.

The company is led by Calvin MacDonald, who has been effectively managing capital allocation since 2018 and has provided a clear direction for the company's goals. He has received high scores on Comparably. It's noteworthy that MacDonald holds a substantial 43,409 shares of Lululemon, as indicated by Gurufocus. While his stake doesn't compare to the massive founder stakes held by CEOs I admire, such as Brian Chesky, Airbnb ( ABNB ) or Pieter van der Does, Adyen ( ADYEY ), it does demonstrate his commitment to the company.

Notably, there have been no significant insider purchases by the executive team.

The Tricky Part - Valuation

After conducting a more comprehensive analysis, I've decided to make slight adjustments to my valuation, particularly in the DCF section. My previous valuation was quite optimistic, and the new one leans a bit more toward the conservative side, which I consider safer. However, this adjustment doesn't alter my "Buy" rating; it doesn't shift the perspective toward the downside or the upside.

Valuation is a critical and intricate aspect of the analysis. Its complexity arises from the multitude of assumptions it entails. Numerous historical examples exist where companies were deemed overvalued by various metrics, yet still managed to outperform their benchmarks by a significant margin. Conversely, there are instances where the opposite holds true.

In my approach to valuing companies, I employ a three-step valuation process: historical multiples, Discounted Cash Flow analysis, and technical analysis to determine the optimal timing for making an investment.

It's important to note that historical multiples are derived from the Zero Interest Rate Policy (ZIRP) era. Now, with the Quantitative Tightening (QT) environment, we can anticipate multiple contractions. The equity risk premium has increased, leading investors to demand lower prices.

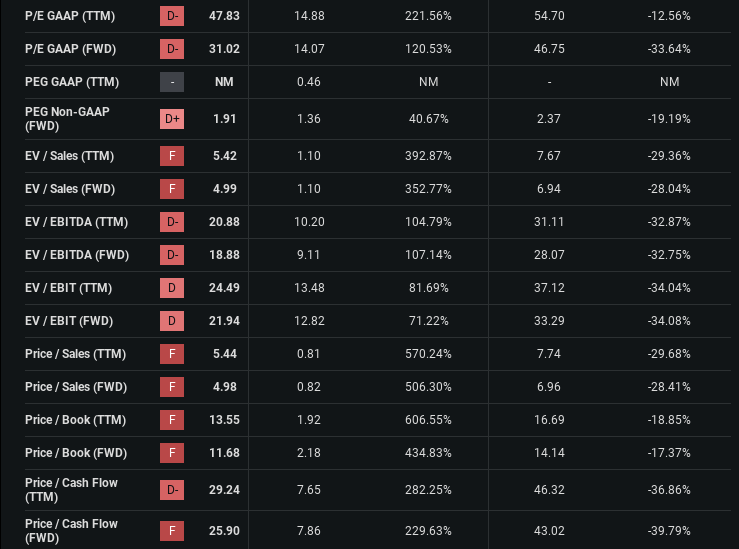

Lululemon is significantly undervalued when compared to its five-year multiples. This undervaluation is evident from both an earnings perspective and a cash perspective. For instance, you can observe that the price-to-free cash flow is undervalued by 36%, and the EV/EBITDA is down by 32%.

{kind=link}

Hence, even with the anticipated average multiple contractions, there is ample room for multiple expansions, driven by business growth. While it might not reach the levels of the past averages, there's potential for it to expand, albeit slightly below those historical averages.

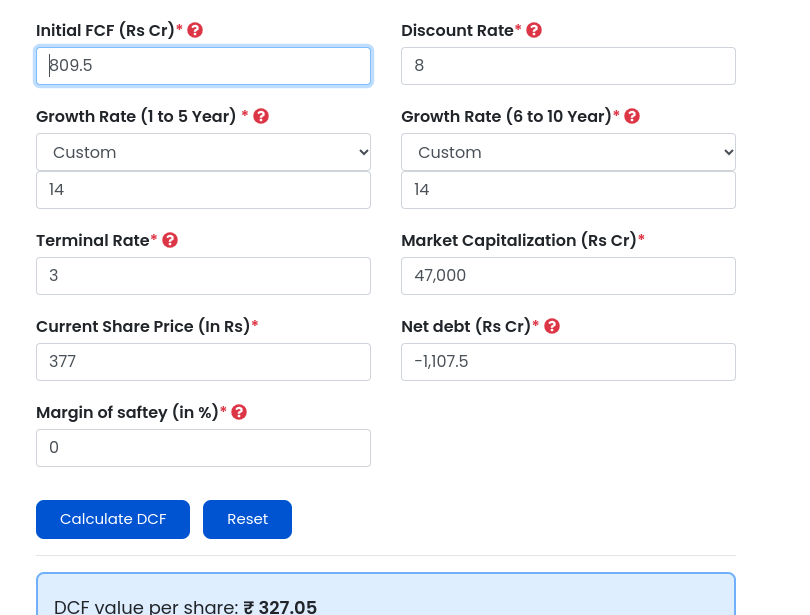

The DCF analysis suggests a different perspective. I utilized an 8% discount rate based on the Alpha Spread WACC calculator, incorporated a 3% terminal rate, and applied a 14% CAGR based on the management's goal. It's important to note that this model does not account for potential margin expansion or stock buybacks, both of which can enhance free cash flow per share.

I've made changes to the growth rate compared to my last article, making it more conservative and aligning it with the management's goals. Additionally, I decided to adjust the terminal rate from 2% to 3% to account for Lululemon's global expansion and the increasing revenue from countries like China, among others. These changes aim for a more balanced valuation.

The outcome of this DCF analysis yields a stock price of 327, indicating a 15% overvaluation. However, I would like to emphasize a crucial point: not all companies align neatly with a DCF calculation, as their unique qualities may not be fully captured by the model. While I'm uncertain if this applies to Lululemon, it's an important consideration.

{kind=link}

It's worth noting that a DCF model is highly sensitive to changes in its inputs, whether upward or downward. As an example, if I input a 17% growth rate based on the five-year average, the resulting price is 410, suggesting a slightly undervalued stock. Conversely, if I speculate that competition will erode Lululemon's margins, resulting in a 12% FCF growth, the stock appears decidedly overvalued. Therefore, the three-step valuation process, coupled with the company's unique qualities, serves as an extra layer of assessment.

I prefer to invest in companies when their stock prices approach or touch their 200-day moving average and exhibit a low RSI. Lululemon is currently near its 200-day average but not quite touching it, and its RSI is in a balanced range. Based on these metrics, if you have decided to invest in Lululemon, I would recommend waiting. However, if your investment horizon is long-term, which it should be, the precise timing becomes less critical.

{kind=link}

Based on the three-step valuation, I would conclude that Lululemon is fairly valued. However, high-quality companies are seldom perceived as fairly valued. In many cases, when they are considered fairly valued, it often indicates that they are undervalued. This assumption is contingent on the breadth of Lululemon's competitive moat, which I'm not entirely certain about.

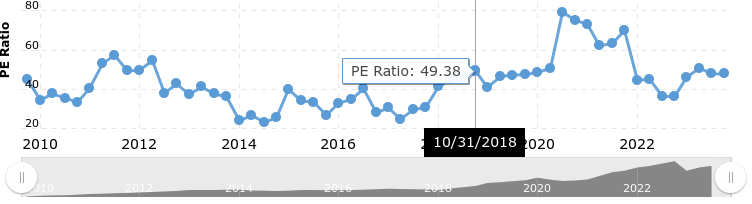

Bonus Aspect: I'm not overly concerned about purchasing Lululemon at a high multiple. Historical data shows that the company's quality, combined with a long-term investment horizon, has led to significant outperformance. For instance, if you had bought Lululemon on October 31, 2018, you would have paid 49 times earnings. However, you still would have achieved an outstanding return, more than tripling the market's return in the same period. It's essential to note that we're not in the same era, as quantitative tightening (QT) might present challenges for stocks. Nevertheless, I encourage you to prioritize the quality of the business.

{kind=link}

Risks

First and foremost, the most formidable risk lies in the realm of competition, which has the potential to seize market share and exert downward pressure on profit margins.

A loss of relevance represents a significant and ever-present risk, given the fluid nature of consumer preferences.

Overreliance on the North American market is a risk, as any shifts in consumer preferences within this market could leave Lululemon with insufficient alternatives.

The pace of innovation presents its own set of risks. Failure to maintain its innovative edge, which it asserts as its core strength, could render Lululemon vulnerable to competitive threats.

And, of course, there's the matter of valuation. The fact that Lululemon appears to be fairly valued suggests that there is little room for error, and the growth trajectory must maintain a CAGR above 15% in free cash flow.

All of these risks are inherently tied to the question of the company's competitive moat. As it stands, my current assessment is that Lululemon does possess a moat, particularly in the form of a brand power moat, which contributes to its pricing power. However, this moat doesn't appear to be as expansive or profound as those of other companies I've analyzed, such as Nike, Hermes, or even Ulta Beauty. This aspect is a central concern for me.

Conclusion

I hope I've provided you with a more comprehensive and in-depth perspective this time, offering more answers. However, after delving into the business, I've surfaced with pretty much the same conclusions as last week and the same rating as well.

In my assessment, the robust brand, pricing power, transparent management, high returns on capital, and sustained secular growth collectively represent characteristics of a high-quality company. As I have emphasized several times throughout this analysis, it all boils down to the pivotal question: does Lululemon possess a substantial competitive advantage? Is the moat sufficiently wide, and is the growth sustainable?

I do believe that Lululemon's growth is sustainable, thanks to a relatively straightforward formula centered on international expansion and maintaining local relevance. However, I harbor doubts about the width of the company's moat. While there is indeed a moat, I'm uncertain whether competitors might leap over it and undermine Lululemon's continued relevance.

Therefore, my recommendation is to consider Lululemon a BUY. If the moat were broader, I would readily advocate for a STRONG BUY. However, in my perspective, that is not the current situation.

I'm keen to hear your insights on Lululemon's competitive advantage and whether you share a similar perspective.

For further details see:

Lululemon: Strong Brand, Fierce Competition