NSNHF - Luminar: Approaching Inflection Point

2023-08-09 13:57:06 ET

Summary

- Luminar Technologies had a strong Q2 with 63% year-over-year growth, but the market is still waiting for a major inflection point.

- The company's Q3 2023 revenue guidance fell short of expectations, but it is still on track for 100% growth this year.

- Luminar's future order book is valued at $3.4 billion, and hitting revenue targets could lead to a significant increase in stock valuation.

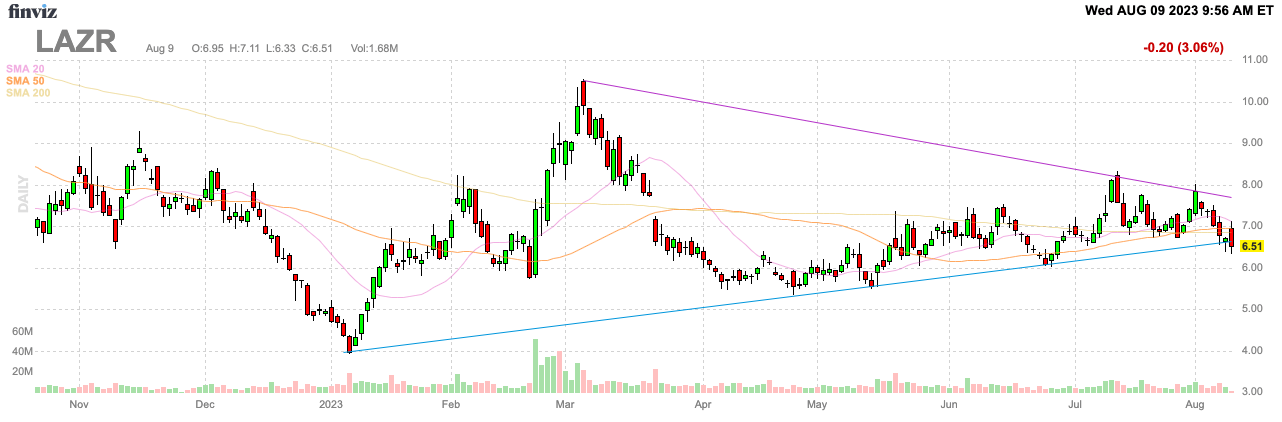

By all regards, Luminar Technologies, Inc. ( LAZR ) had a blockbuster quarter with massive growth. Still, the market is waiting for the Lidar sensor company to report a massive inflection point where production deals ramp toward millions of automotive Lidar units. My investment thesis remains ultra Bullish on the stock, which is still trading near the year lows with the business making tons of progress.

{kind=link}

Breakout Approaching

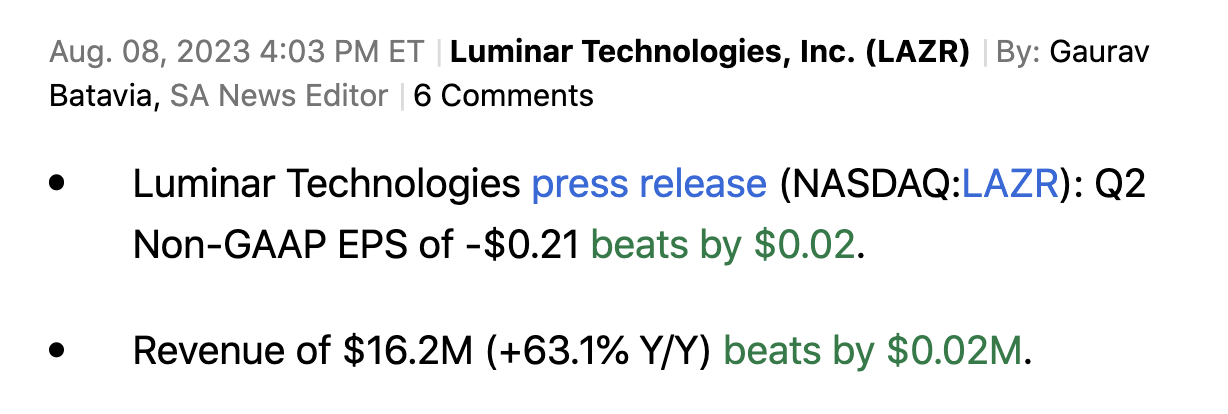

Luminar reported record quarterly revenues and grew those numbers 63% YoY in what would normally be considered a great quarter as follows:

{kind=link}

Unfortunately, the market still wants the promised inflection point where revenues are doubling and tripling annually, reaching $1+ billion levels. This quarter didn't deliver this number, and guidance for Q3'23 revenues were only $18 to $21 million with consensus estimates up at $22 million.

Luminar didn't change the guidance for revenue growth topping 100% this year, leaving a lot of revenues during Q4 with the production ramp of the Volvo EX90 vehicle in China and the Polestar 3 underway. In addition, the company has the Mexico production facility ramping up towards production volumes by year-end to meet these targets.

By all accounts, Luminar will cross the major breakthrough point in the next few months. The company generated $40 million in sales last year and needs to hit $80 million this year to reach the corporate target for 100% growth. Sales are generally targeted at the $50 million range for the first 3 quarter of the year, leaving at least $30 million in Q4.

Luminar would be approaching 200% growth in Q4 and analysts were already forecasting the quarter actually reaches $34 million. Just hitting $20 million in quarterly sales in Q3 should open up investor interest and of course hitting the $80+ million target for 2023 and guiding to 100%+ growth for 2024 should further garner investor interest with the Lidar company becoming a full revenue story.

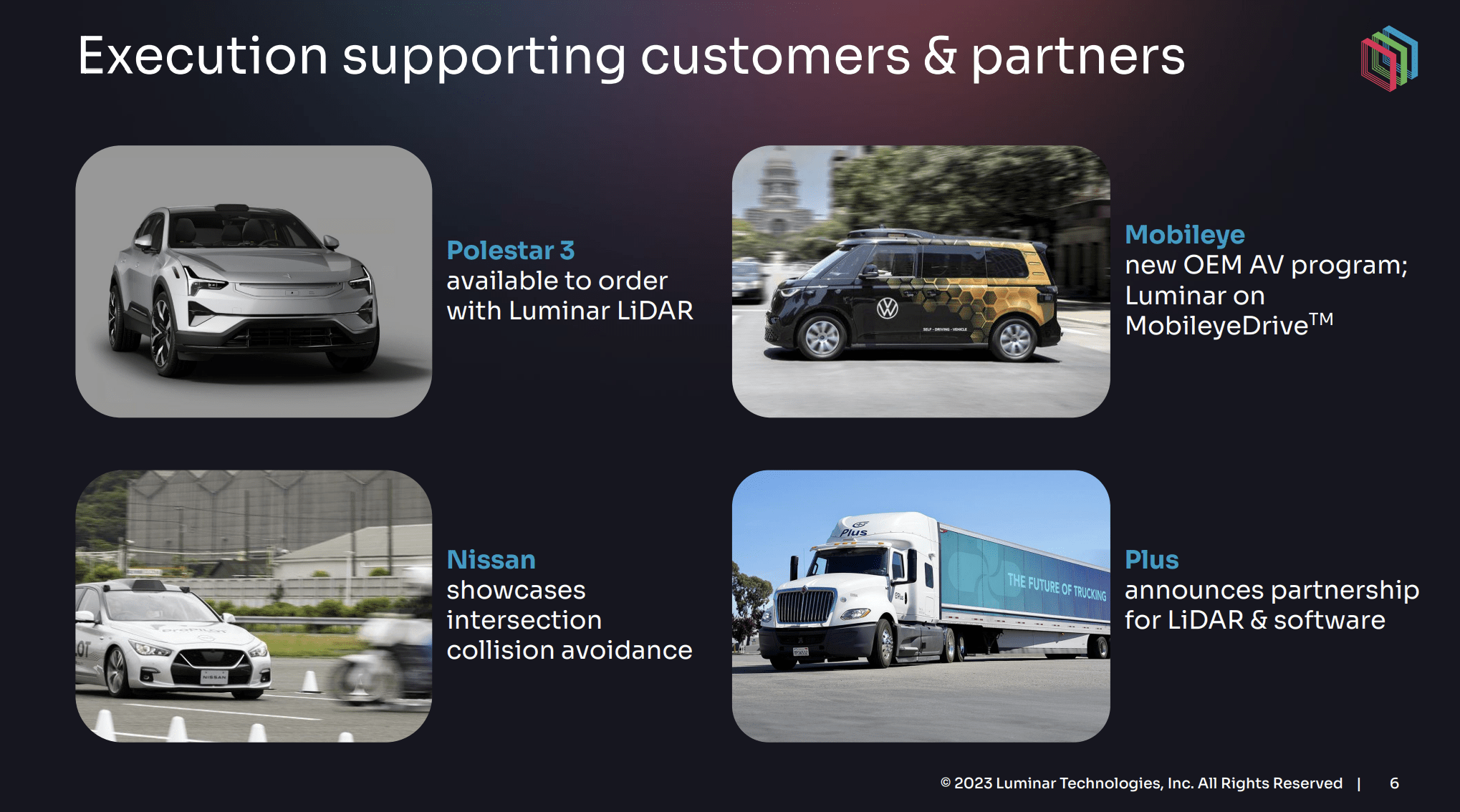

The prime benefit of hitting revenue targets and gaining investor confidence as the company moves into production mode is that the massive opportunity story already exists. Luminar has already outlined a $3.4 billion future order book, and the company outlined new deals with a Mobileye ( MBLY ) OEM, Nissan Motor Co., Ltd. ( NSANY ) and Plus .

{kind=link}

All of these deals are likely part of the puzzle for Luminar adding another $1.0 billion in order backlog this year bringing the year-end total to at least $4.4 billion. The stock valuation would likely soar, if the market had confidence in the reality of this order book size.

Not to mention, CEO Austin Russell continues to forecast the massive opportunity by decade end by only grabbing as little as 4% of the auto units. He made this comment again on the Q2'23 earnings call (emphasis added):

...our target market penetration, by the end of the decade is only 3% to 4%. Because we think even with that, we'll be able to achieve around 5 billion revenue and two and a half million EBITDA with as much as 60 billion forward looking order book at that point, even with just a relatively small amount of market penetration.

Difficult To Value

Naturally, the market is having a difficult time valuing the stock. Should Luminar be valued based on $80 million revenue estimates, or should the stock be valued based on a forward-looking order book approaching $4.4 billion.

Our view leans more towards the order book size. Luminar is working with far too many auto OEMs to have made up order book values, and the company continues to make substantial progress on achieving goals, whether or not the path is perfect.

A big focus will turn towards liquidity as the calendar flips to 2024. Luminar forecasts ending the year with $300 million in cash with a goal of finally reaching positive gross margins to help reduce the cash burn.

The company spent $79 million on free cash flow during the quarter with up to $37 million due to cost for the high-volume launch of the Mexico facility and working capital investments. The cash balance of $366 million at the end of June implies a quarter cash burn of only $38 million in the 2H and matches the goal of cutting cash burn by 50% while collecting small investments, such as the additional $10 million cash investment from TPK.

The stock has a listed market value of $2.5 billion with sales set to soar next year as production starts on several deals. The only question now is when, not if, these production deals ramp.

Takeaway

The key investor takeaway is that Luminar Technologies, Inc. remains a bargain as sales are set to ramp the rest of the decade. The company has all of the deals lined up and investors should focus on the progress, not perfection.

For further details see:

Luminar: Approaching Inflection Point