LUNMF - Lundin Mining: Copper Will Shine Again Too Cheap To Ignore

Summary

- A significant decline in the copper price and some short-term company-specific bad news are creating a low-risk entry point for Lundin Mining.

- The company has very good assets, with the Josemaria project capable of doubling its copper output.

- Lundin Mining is well-managed, is already returning capital to shareholders, is cheap and insiders are buying shares.

- The long-term fundamentals of the copper market remain rock-solid.

Introduction

A good moment to get long a company, or a sector, is when a series of negative short-term news causes a rapid price decline and widespread negativity, while at the same time the underlying long-term fundamentals remain very bullish. I believe Lundin Mining ( OTCPK:LUNMF , LUN:CA ) offers precisely this kind of setup.

In the short term, there has been a remarkable sequence of bad news. The copper price has collapsed in June from the $4.5/lbs region to a low of $3.2/lbs in mid-July. As a result, the company has just reported an unexpected quarterly loss of $0.07/share. In addition, Lundin is also in the eye of the storm, as Chilean politicians are threatening severe consequences after the discovery of a huge sinkhole at the company's Alcaparrosa mine. Finally, inflationary pressures, operational difficulties at the Candelaria mine and political risk in Chile continue to weigh on sentiment.

In the long term, however, we have a company that is well-managed, returning capital to shareholders, too cheap to ignore, with good assets, in a sector with very bullish tailwinds. For all these reasons, the current share price offers a compelling opportunity to start building a position.

Copper: A long-term bullish outlook

The main driver for Lundin Mining is the copper price, since copper contributes around 60% of its revenues.

Revenues by metal (Company's Q2 results presentation)

Even if copper has recently suffered a record-fast decline on global recession fears, its long-term fundamentals remain solid.

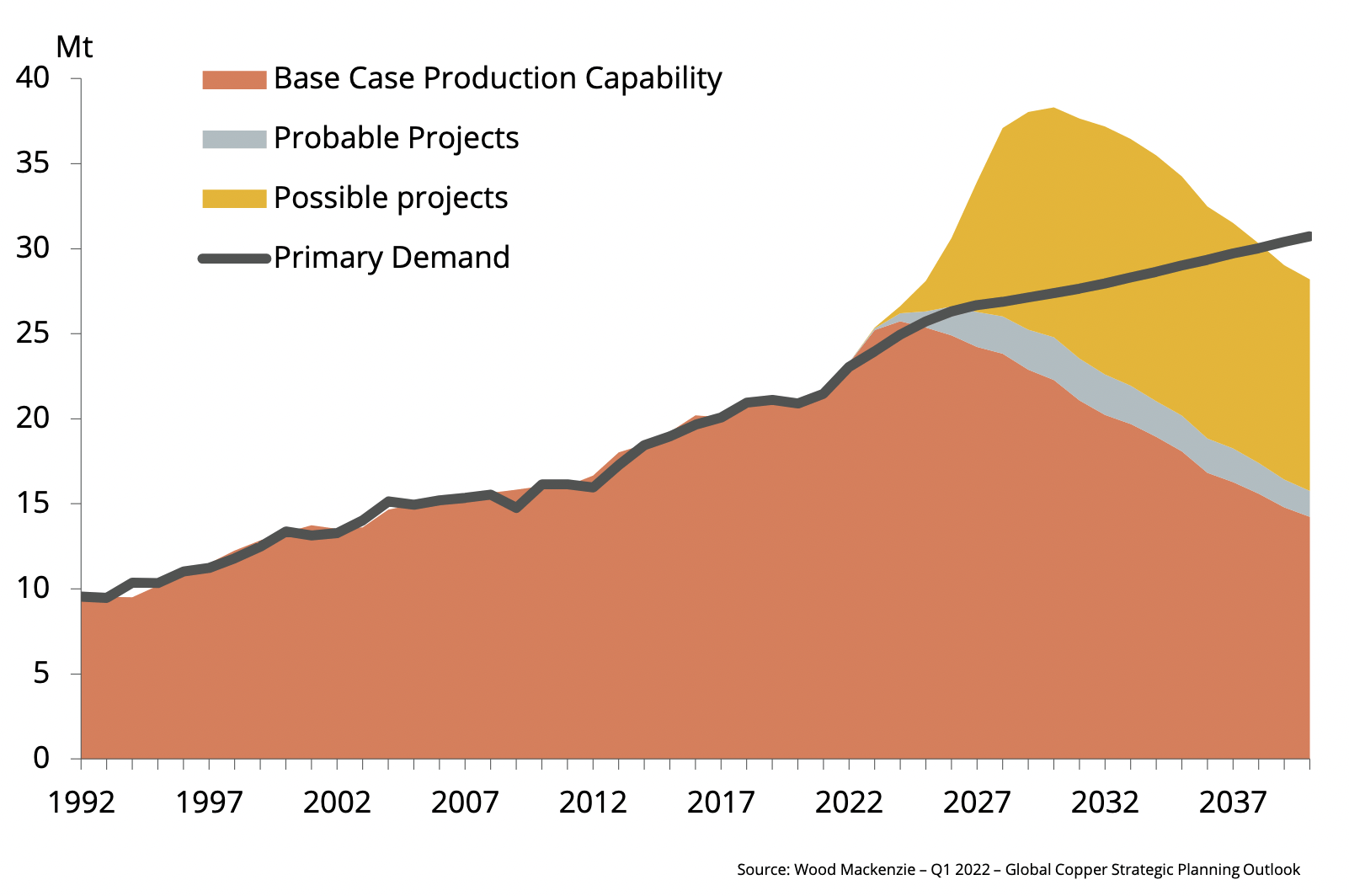

Demand is projected to increase over the next 20 years, because of the energy transition of developed countries and the electrification of developing countries.

On the other hand, supply is relatively inelastic. Developing a copper mine has always been an incredibly complex technical job, with multi-decade timelines. Nowadays, worldwide inflation, supply chain disruptions, stricter environmental regulations and political tensions are further extending such timelines. For an example, one has to look no further than at Oyu Tolgoi , the massive copper-gold deposit in Mongolia that Rio Tinto wants to develop into the fourth biggest copper mine in the world, which has been suffering from continuous delays and cost increases.

Copper projected demand vs supply (Wood Mackenzie - Q1 2022 - Global Copper Strategic Planning Outlook)

{kind=link}

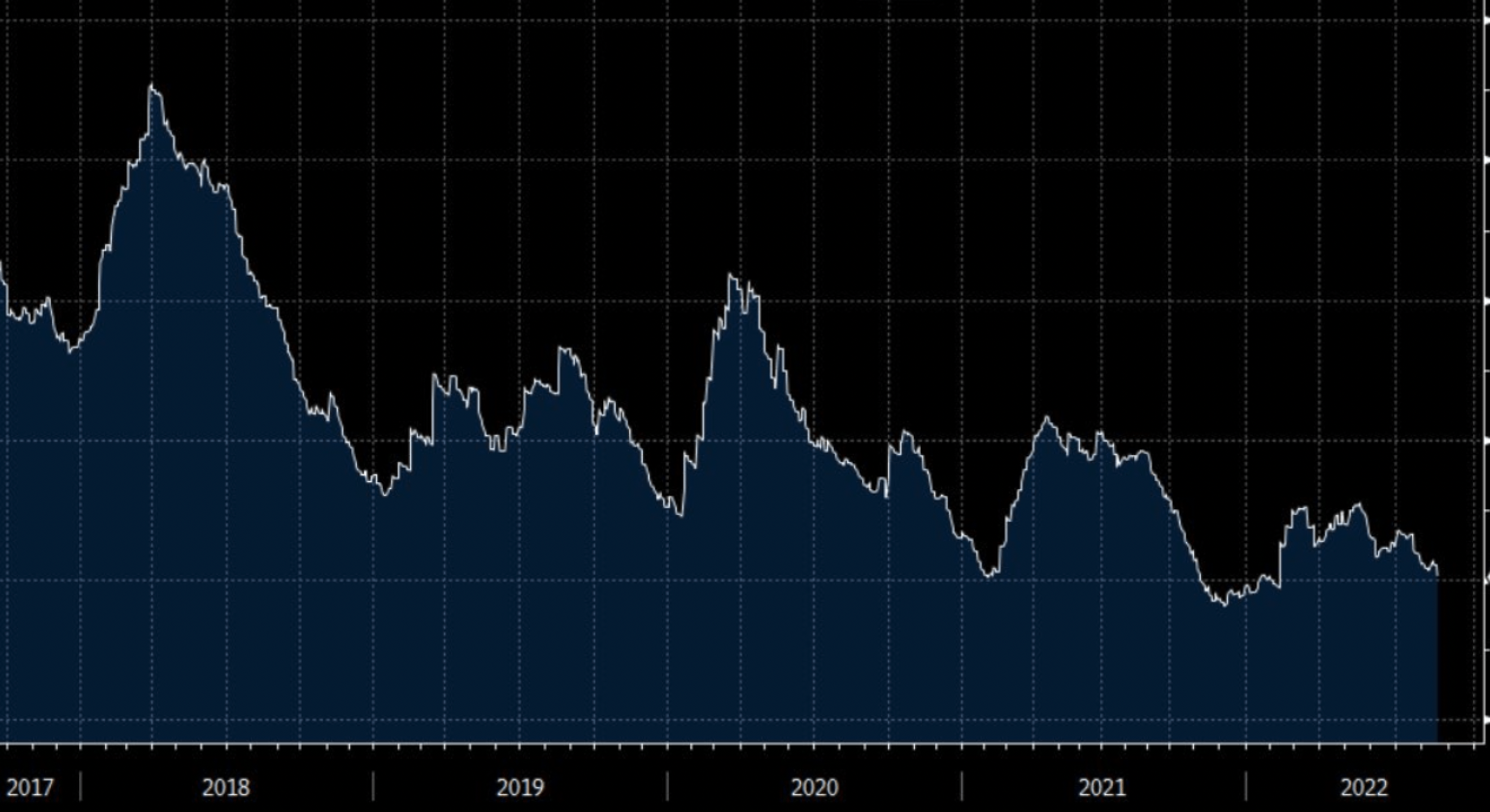

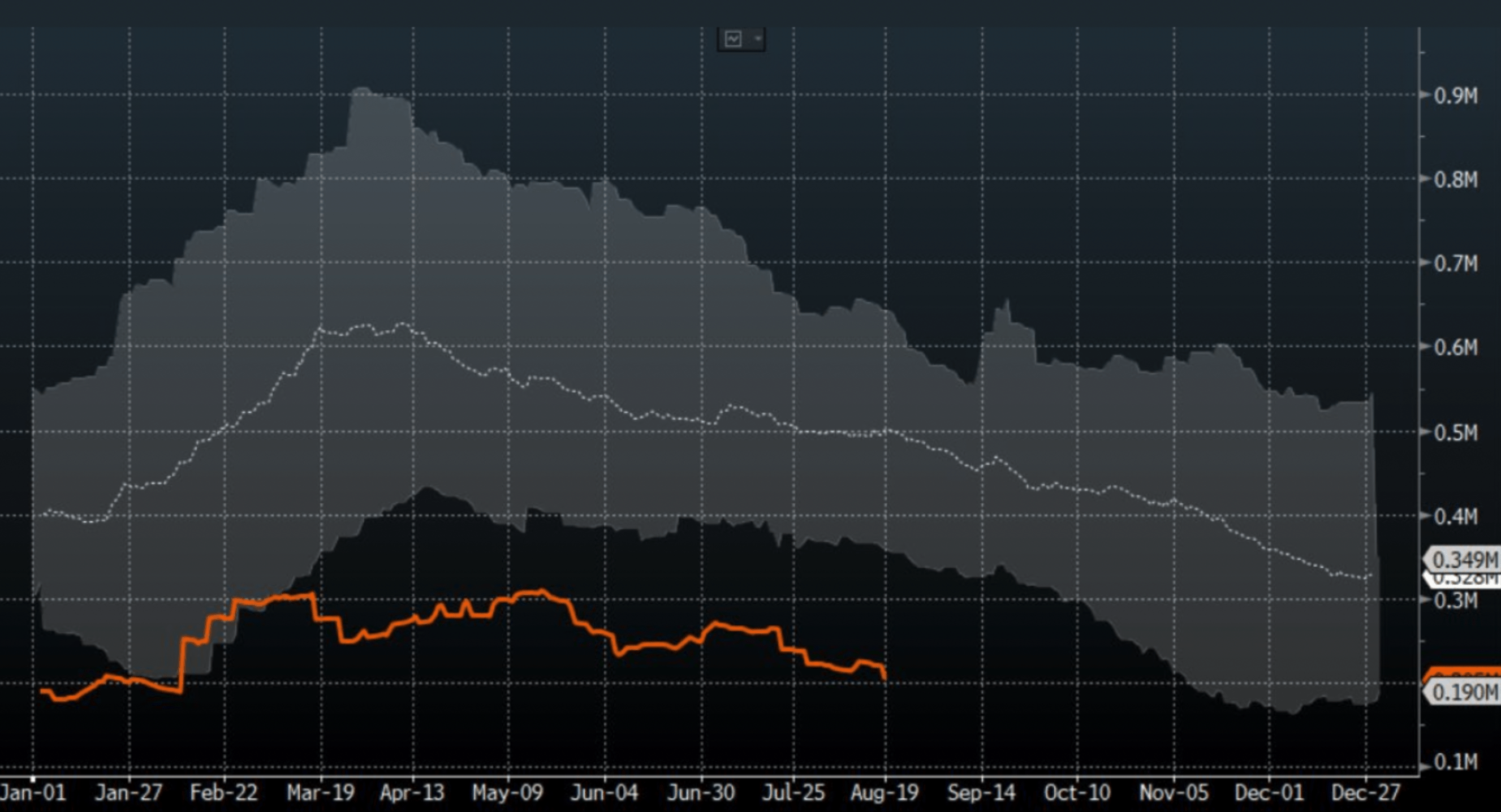

Spot prices have decreased by 25% from their highs touched in the aftermath of the Russian invasion. However, the physical market remains tight. Physical inventories are at historical lows and the futures curve is in backwardation.

Physical copper inventories across all exchanges, last 5 years (Bloomberg) Physical copper inventories across all exchanges. Orange line is 2022, gray is last 5 years (Bloomberg)

{kind=link}

{kind=link}

Of course, the copper price might further decline from here. The short-term future is difficult to predict. However, the noise decreases over longer timespans. Fundamentals then become inevitabilities. The world is going to need more copper. The pipeline of projects currently in development is insufficient to cover future demand . Therefore, the price of copper has to rise to new historic highs over the next decade.

This is the conclusion of BHP's market outlook for copper, released together with its full-year results. After some short-term weakness, related to new projects coming online and softness in demand, the copper price is expected to take off from the middle of the decade, if not earlier.

Once this phase of the decade is transited, a durable inducement pricing regime is expected to emerge from the mid-to-late 2020s. A "take-off" of demand from copper-intensive easier-to-abate sectors (renewable power generation, the electrification of light duty transport, and the infrastructure that supports them both) is expected to be a key feature of industry dynamics from the second half of the 2020s forward: if not earlier.

At the same time that demand is growing, supply is not keeping up.

[...] it is notable that while there has been some activity in the project space, the response has been timid when you consider both the very strong prices we have observed and copper's future-facing halo effect.

The result will be higher long-term prices.

Our view is that the price setting marginal tonne a decade hence will come from either a lower grade brownfield expansion in a lower risk jurisdiction, or a higher grade greenfield in a higher risk jurisdiction. Neither source of metal is likely to come cheaply.

Why Lundin Mining

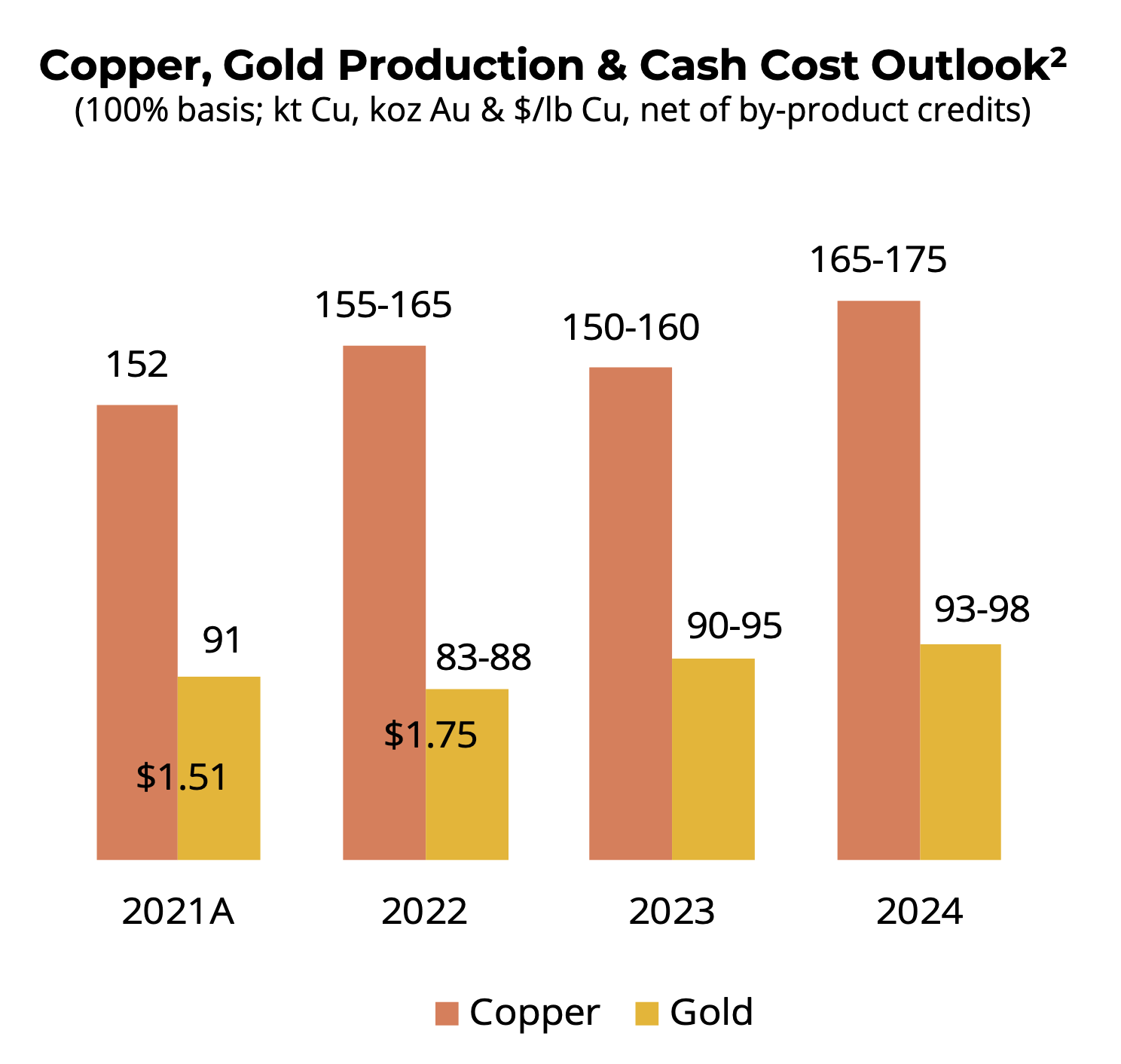

Lundin Mining is in an excellent position to capitalize on a copper bull market. The company has a lot of copper in reserves and resources (besides other base and precious metals, including zinc, nickel, gold, and silver). In addition, the cash costs are typically lower than competitors.

Production and cash cost outlook for 2022 (Company's Q2 Results Presentation)

{kind=link}

This is true even without considering the recent acquisition in April 2022 of the Josemaria project, which is a true game changer.

Josemaria Copper-Gold project camp construction, San Juan, Argentina - April 16, 2022 (Company's Corporate Presentation)

{kind=link}

Josemaria is a porphyry copper-gold system in the San Juan Province of Argentina. It is fully owned by Lundin, and has already access to water, power and transportation infrastructure. It is planned to be developed as an open-pit operation, with a 19-year life of mine, to produce 1 billion tonnes of ore at an average grade of 0.30% copper and 0.22 g/t gold. The strip ratio is a very good 0.98 (for comparison, Candelaria is about 2.4). All numbers are based on conservative estimates of $3.00/lb Cu, $1,500/oz Au and $18.00/oz Ag.

Some back-of-the-envelope calculations imply that Josemaria may produce upwards of 150 thousand tonnes of copper per year. For comparison, the company is guiding for 155-165 thousand tonnes for 2022. Josemaria will double the company's copper production. It is a big deal.

Unfortunately, Josemaria is going to be expensive to develop. Preliminary capex estimates have been revised to above $4 billion, because of recent inflationary pressures. More details will be available in the updated Technical Report, which is targeted for completion by Q4 2022.

Despite the costs, I am reasonably confident that Josemaria will be put into production successfully. The Lundin family has a long-standing tradition of acquiring and developing assets with complex development plans, ultimately creating a lot of value for shareholders. Besides, Josemaria is certainly a primary focus for the company. Lundin is planning to spend $300 million this year alone in preliminary studies. Selling its $1 billion copper-zinc Neves-Corvo mine in Portugal can also be interpreted as a strategic move by the company to focus on Josemaria and raise some of the necessary liquidity to push it forward.

What about the loss posted in Q2 2022? The quarterly loss was mainly the result of provisional price adjustments due to the rapid decline in the copper price in June. Revenues were revised downward by a $220 million impairment. However, both free cash flow and cash flow from operations were significantly positive, at $215 million and $366 million, respectively. Lundin Mining remains profitable even at these depressed levels.

There are additional reasons to be optimistic going forward. First, the copper price has already partially recovered since mid-July. In addition, even the current price is probably unsustainable over a long period of time.

In fact, I suspect we may have already experienced the worst part of the decline (or be very close to that moment). Despite a remarkable coincidence of negative circumstances, with the Chinese property sector crisis, COVID lockdowns, and global recession fears all weighting negatively on sentiment, the energy crunch is putting a floor under the copper price. If China further stimulates, lockdowns are lifted, or a recession does not materialize, I would expect the copper price to move powerfully to the upside, given the current physical market's tightness.

Lundin Mining is cheap

The company's balance sheet is very robust. Net cash stands at $470 million as of Q2 2022. The company also has access to an $1.8 billion credit line. Market capitalization is around $4 billion. So, one is paying an EV of about $3.6 billion, for a company that in 2021 generated almost $1 billion in FCF. About more recent results, over the first two quarters of 2022, Lundin has generated FCF of $187 million in Q1 and $215 million in Q2. It definitely looks cheap.

Unfortunately, FCF for the full year will likely be lower than in 2021. First, because the average realized copper price will probably be lower. Second, because cash costs are continuing to creep up, due to inflationary pressures related to fuel, labor and consumables (partially offset by dollar strength). For instance, the cash cost outlook for the full year has already been moved from $1.55/lbs in Q1 to $1.75/lbs in Q2, a 13% increase.

In addition, a significant capital expenditure program is going to weigh on FCF in the coming years. In 2022, the company is planning to spend $1 billion dollars on capex (of which $300 million just to advance the Josemaria project).

However, regarding cash costs and inflationary pressures, this is undoubtedly a global phenomenon that is impacting all miners. Ultimately, it must result in a higher equilibrium price, otherwise new projects will not be brought online.

Second, regarding capital expenditures, Lundin Mining is turning into a growth story after the Josemaria acquisition. Yes, it is going to be expensive, but the payoff in the end will be huge. There are not that many copper projects in the world that look as promising.

As evidence, consider that mining giants Rio Tinto ( RIO ) and BHP ( BHP ) are both trying to increase their copper portfolios with no success. Rio Tinto recently had its take-over offer for Turquoise Hill ( TRQ ) rejected. Similarly, BHP saw its bid for OZ Minerals ( OTCPK:OZMLF ) rejected. This is the results of years of under-investment, grade decline, resource depletion, scarcity of available projects, and increased complexity and costs of available projects.

The final confirmation that the current share price does indeed offer significant value comes from the fact that insiders have been scooping up shares in the last month. Here is a list of recent SEDI insider filings:

| Date |

| Insider |

| Transaction |

| Amount |

| 2022-08-09 |

| Jean-Claude, Lalumiere (Senior Officer of Issuer) |

| Acquisition in the public market |

| 7200 shares @ $6.93 |

| 2022-08-05 |

| Hastings, Andrew (Senior Officer of Issuer) |

| Acquisition in the public market |

| 5000 shares @ $6.60 |

| 2022-08-03 |

| Lorito Holdings (Security Holder of Issuer) |

| Acquisition in the public market |

| 500000 shares @ $6.84 |

| 2022-08-01 |

| Hastings, Andrew (Senior Officer of Issuer) |

| Acquisition in the public market |

| 3300 shares @ $7.00 |

| 2022-07-13 |

| Lorito Holdings (Security Holder of Issuer) |

| Acquisition in the public market |

| 500000 shares @ $7.52 |

It should be noted that Lorito Holdings is Lundin's family trust.

Conclusion

In conclusion, the recent decline in the copper price and some short-term company-specific bad news are creating a low-risk entry point for Lundin Mining.

The long-term fundamentals of both the copper markets and the company remain rock-solid. The Josemaria project is expensive, but can be brought online in a timely fashion to capitalize on the coming copper bull market.

The current share price offers a good margin of safety, as evidenced by insiders buying shares. For all these reasons, I am starting to accumulate a position, I will buy on further weakness and rate Lundin Mining a BUY.

For further details see:

Lundin Mining: Copper Will Shine Again, Too Cheap To Ignore