LUNMF - Lundin Mining: 'Hold' Was The Right Choice Revisiting And Updating Thesis

2023-11-02 10:56:03 ET

Summary

- Lundin Mining is a controversial stock due to past human rights breaches, but it has shifted focus and is now a good base metal company.

- The company has seen solid operating results and has taken steps to stabilize its current and future results.

- Lundin Mining is copper-heavy and believes in a positive long-term trend for copper, with a potential copper deficit in the future.

- I believe the company can become a "BUY" at under $6.6 per share.

Author's Note: All dollar amounts in this article are Canadian Dollars unless specifically noted.

Dear readers/followers,

Lundin Mining ( LUNMF ) is a somewhat controversial stock even here in Sweden, where the company is from. However, beyond controversy, we find a qualitative mining company that I have been writing about once before at the beginning of 2023. I actually started researching it over a year ago because a friend and investment colleague of mine invested heavily in the business and asked me for my opinion.

I like mining in general - I just have never found much luck in pure-play gold mining (Lundin isn't that). While the company is originally Swedish, it's actually incorporated in Toronto, Canada. This means that the company has a native NA ticker in the form of Canadian ticker LUN - which is the one I'm going to try and focus on here, aside from the Swedish one for me personally due to the tax-advantaged investment option of the Swedish ticker.

My first Lundin article can be found here - meaning this is an update to that thesis, where I did not see a good enough valuation to warrant or interest me in terms of investing.

Lundin Mining - updating on my thesis

So, the controversies and difficulties with Lundin are pretty well-known at this point, and if you're unclear about why exactly some, especially in Europe, would raise an eyebrow if you're stating that you're investing in a Lundin business, you can read my first article. To summarize very shortly, Lundin has been comprehensively accused of substantial human rights breaches in work in Africa, and the firebrand manager at the time made no secret of his ambition to make money from controversial risks or dictatorships - seeing this as a competitive advantage.

Even someone generally more focused on profit rather than ESG or human rights tends to pause when Lundin is brought up.

On the positive side, Lundin today, including Lundin mining, isn't really involved in those sorts of businesses any longer. I believe what can be said about Adolf Lundin is that he was a "gunslinger", a wildcat sort of investor who had no issues leveraging laws and regulations where he saw it as possible - a very "No guts, no glory" sort of approach, think of it what you will. But that is not Lundin mining, nor its latest results, nor the reason why the company has actually underperformed the index over time, much like I expected it to.

Seeking Alpha Lundin (Seeking Alpha)

Granted, I did not expect it to outperform as it has, and perhaps this current valuation does imply that there's an upside - that's what we'll look at here.

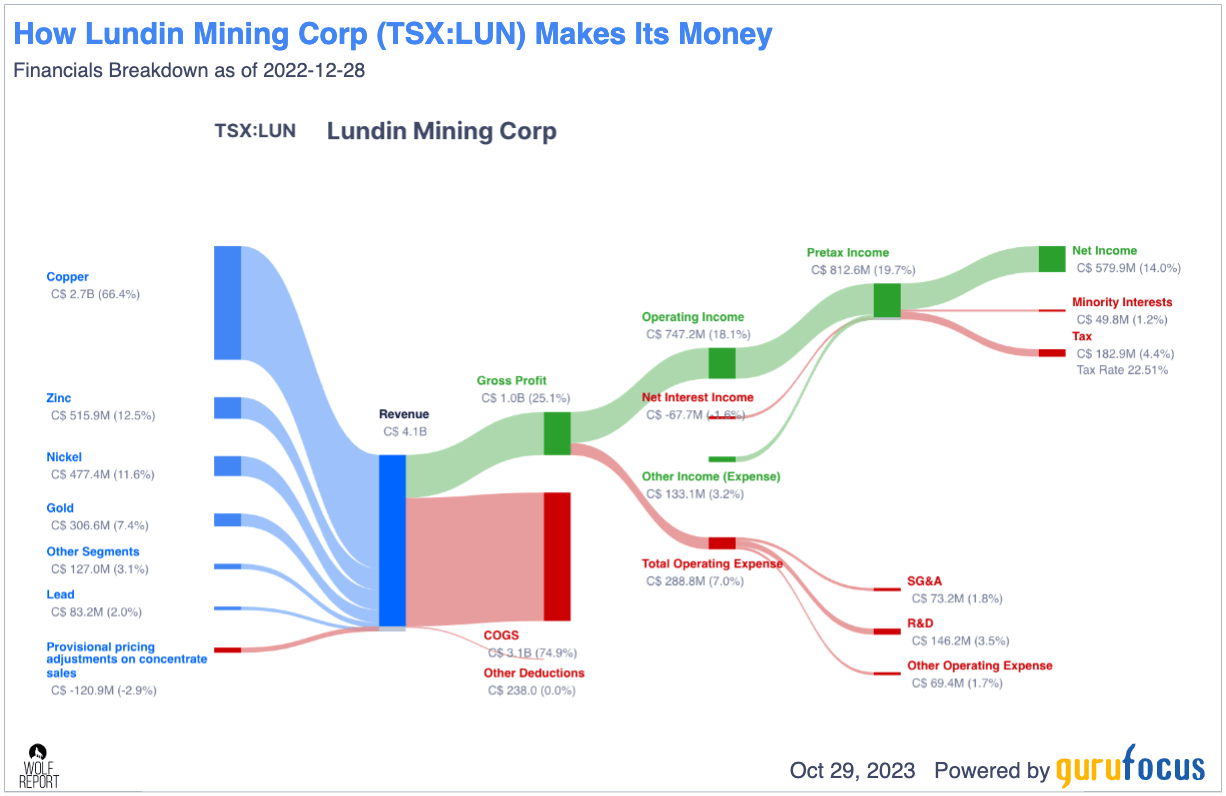

Remember, despite the focus on gold, the reason why I can consider investing is that the company isn't just focused on Gold - it's actually mostly a copper company, with only 7% gold.

Lundin IR (Lundin IR)

The company has effectively turned from a controversial business into a good base metal company. The company has seen fairly acceptable trends for 2Q23, and we're obviously moving closer to 3Q23 as well. 2Q23 saw solid operating results, with completion of the Caserones M&A during early 3Q, reported during the 2Q report. The company was able to generate about $60M net and over $160M of adjusted EBITDA.

Just as with the prices of other commodities, base metals and overall metal prices have been declining and lower realized sales prices mean that profits are going to go down.

However, the company is not in any sort of fundamental danger. With $1.6B of liquidity, good foreign FX hedging (important given the company's operation), as fuel hedging for diesel, the company has taken steps to stabilize not only current but future results.

Another positive is that the company decided to maintain a ~4% yield - this may not sound like much, but in context and given what the company does, and how other companies in the same sector fare, it's actually quite good. In fact, Lundin when you look at the company, is one of the more profitable mining operators in the entire peer group, in terms of margins, RoE, RoA, and ROIC. It also has average or above-average debt and interest coverage profiles, and that yield and dividend growth rate is well above the average for the sector (Source: GuruFocus)

This operation, seeing it from a high level, is working very well - and the company is very experienced at "making it work".

Lundin Mining Business (GuruFocus)

{kind=link}

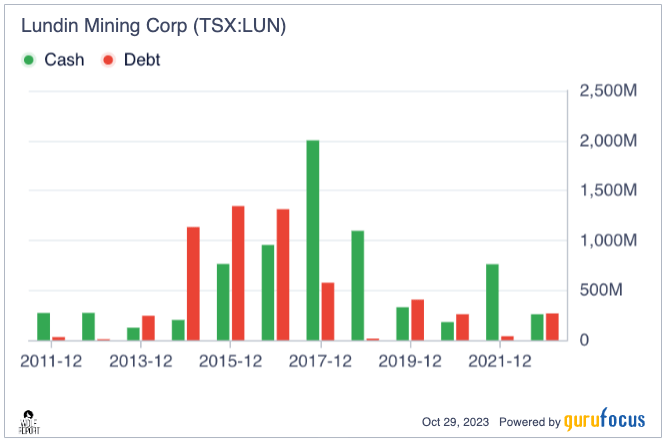

The only few negatives I can really find in fundamentals are a somewhat unfavorable dilution some years back - the stockholder equity portion of the assets has been shifting since that time, with a significantly lower % of SE/TA, but that's one of the few drawbacks. The company has otherwise seen significant profitability improvements, only sliding back down somewhat this year, and any significant or worrying debt burden is actually gone.

Lundin Mining cash/debt (GuruFocus)

{kind=link}

As I mentioned in my earlier articles, Lundin is copper-correlated.

In a positive copper environment, Lundin goes up - in a negative, it's likely to go down. The company believes Copper to be one of the driving forces going forward, with a high-level positive copper outlook based on its importance in the energy transition. This coupled with a very inelastic supply of profitable copper mines means that the company has a very bullish outlook on the demand. I've mentioned in other articles on automotive and ESG stocks overall, that the energy transition seems to have hit some small snags here, with less demand for EVs and not the same profitability for many ESG and Energy projects. This will of course impact the demand for copper as well.

However, while I do believe in the short- to medium-term the demand to decline, I believe the long-term positive trend for copper is a clear one.

In the copper mining industry, I believe there are two reasons why Lundin will continue to outperform - one is what I mentioned above - even if the short-term perspective goes down, the long-term one will continue to go up, due to the potential copper deficit I describe below.

Secondly, and more importantly, supply. There are fewer copper mines globally coming "online" than assets declining. Mine production is expected by Lundin and other players, to go down - and there are few advanced-stage projects for new mines available (Source: Lundin IR). That means we're in a real possibility of an eventual copper deficit.

This will prevent companies like Lundin, which are copper-heavy, to really decline massively.

The company does not have a credit rating and currently has a market cap in Canadian dollars of ~$7B. This makes it perhaps one of the smaller players, but it also comes at a yield of 4+% currently, which is above par for the segment. What's more, the company is currently valued at less than 14.1x P/E, which is well below where it usually trades - more on that later.

I remain in my stance that Lundin does, without a doubt, have a very attractive set of assets on a global scale. I would categorize it as significantly riskier than many purer-play EU miners, but with a broader potential appeal exactly due to this diversification.

What about risks? What risks exist?

Well, you really only need to look at the news for the past 4-5 months. Lundin was recently prevented from reopening Alcaparrosa in Chile, which is part of what has been weighing on the company's share price. These sorts of cases are a natural result of operating mines, but in this case, it's unclear when things will be able to start back up again. These sort of cases, especially for comparatively new mines in a politically unstable or uncertain environment, is part of what you need to discount when investing in Lundin.

The metal industry is a cyclical one - I don't view that as the primary risk to Lundin. Instead, these sorts of cases from courts and other players are really where I see the risk to the company, and why my targets for Lundin may be lower than others.

Results for 3Q23, which were published the day that I am submitting this article, were good to mix, but did not change my thesis in a material way, which I did not expect them to. The company saw increased revenues to just south of $1B, beating expectations, with EPS coming in at around breakeven levels, at a loss of $3B, or a net loss to shareholders of $0.00/share, or $0.11 on an adjusted level. The company raised its overall production guidance, and came in at an operating cash flow of $0.41/share, generating just over $70M worth of FCF.

What investors should keep a close look at is the integration of Caserones - and the company has found some synergies worth an impressive $20-$30M a year. On the housekeeping side, the company's corporate move to the city of Vancouver is complete, and I will say that 3Q23 closes the books (quarterly) on a company that is well-prepared for the year 2024.

Worth noting is that there is a CEO shift in Lundin - but none of this news for 3Q23 do anything to change my overall expectations for this company in the long term or my valuation targets.

Let's look at those valuation targets.

Lundin Mining - Updated valuation and upside calls for "HOLD" here.

My last stance for the company was a "HOLD" with a PT of $6.6. There are a few reasons why I am so "negative" when a simply 15x P/E to a decline year like 2023E implies a $10/share PT.

First off, estimates are often way off. We're talking about missing estimates over 65% of the time, negatively. That's worse than the accuracy of a coin toss, and during certain years these forecasts are off more than 100% (Source: FactSet). This means that short- to medium-term safety is not something you can, or should count on Lundin to have.

Secondly, risk-free rates. Lundin would be much more attractive back in 2020. Now, when you can get 5-6% literally throwing your money at any IG-rated bond or pref stock, with some IG-rated debt alternatives going up to 8-9% (I know, I invest in those as well), Lundin at $8.8/share isn't looking as sweet as it once did.

Lundin is currently followed by 20 analysts. Out of those 20 analysts from S&P Global, the company is estimated to have a PT starting at $5.9 and going up to $9.9/share. The average is currently $8.7, which is close to the current PT. However, more than 5 analysts "should" have a "BUY" here given that range and average, but only 4 are currently at "BUY", with a total of 10 at "HOLD" and 3-5 at "Underperform" or even "SELL" (Source: S&P Global).

While there are calculations, such as DCF or Lynch models, where you can easily see the company as being implied valued between $10-$13/share, I would say those estimates are perhaps a bit too positive for me, and you'd do better discounting heavier. My own PT stays at the $6.6/share level, which is just north of the lowest PT for the company from other analysts - but it's a level I justify using a 5%+ risk-free rate, the risks and actual events of closed (even temporarily) mines

I believe Lundin as a business may grow very interesting during any sort of serious downturn or recession. If the company drops below $6/share, I will actually be adding heavily to this business, and in fairly quick order, because I believe at that level, implying almost a 5% yield, this company could be an absolutely stellar outperformed with an annualized, realistic upside of over 20% for a reversal.

However, in this environment, and under the current valuation specifics, I do not view the company as materially attractive - and I direct you to my track record with the company to "prove" it in 2024.

I will keep a closer eye on it in the coming year, and if it does drop to any investable level, i will be purchasing shares.

Questions?

Let me know!

Thesis

- Lundin is a Canadian-based, originally Swedish miner in the Copper, Zinc, and Gold segments. The company doesn't have a credit rating, but does have a set of appealing assets across the globe, and has left behind its problematic operations in Africa to focus on South America, Europe, and NA.

- At the right valuation, the price for the company's assets is appealing enough to where you may garner a triple-digit rate of return for a good investment. However, that time is not now. The company is richly valued, and I see a strong potential for a flat valuation or even a downturn.

- The company is, to my mind, worth 0.5-0.6x NAV and below a 1x BV. That implies a PT of $6.6.

- This makes Lundin Mining a "HOLD" here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company fails the safe and valuation checks. The only way Lundin can become a "BUY" is if it falls to below $6.6, which is my current price target for the company. It's a "HOLD".

For further details see:

Lundin Mining: 'Hold' Was The Right Choice, Revisiting And Updating Thesis