LXFR - Luxfer Holdings: Price Decline Justified Risks May Keep Prices Low For Longer

2023-11-23 00:18:23 ET

Summary

- Luxfer Holdings' stock price has declined by 46% since March due to poor performance and macroeconomic conditions.

- The Gas Cylinder segment performed better than expected, but the Elektron segment faced obstacles such as supply chain issues and higher magnesium prices.

- Macroeconomic conditions, including high-interest rates and geopolitical tensions, have negatively impacted the company's sales and margins.

Investment Thesis

Luxfer Holdings' ( LXFR ) stock price performed quite badly since my last coverage of the company, going down around 46% since March of this year. I wanted to take a look at the company once again to see if the company would be a good buy for the long run. The macroeconomic conditions are proven to be very tough for LXFR, which brings a lot more uncertainty in the company's profitability in the short run, therefore I maintain my hold rating from the previous article and bring down my PT further.

Comments on Performance

So, I didn't expect the company to perform this badly over the next 3 quarters. There was a lot of dislike for how the company has been performing recently, with missing expectations by large margins, which is reflected in the stock price performance so far. So let's dig in a little deeper to see what happened.

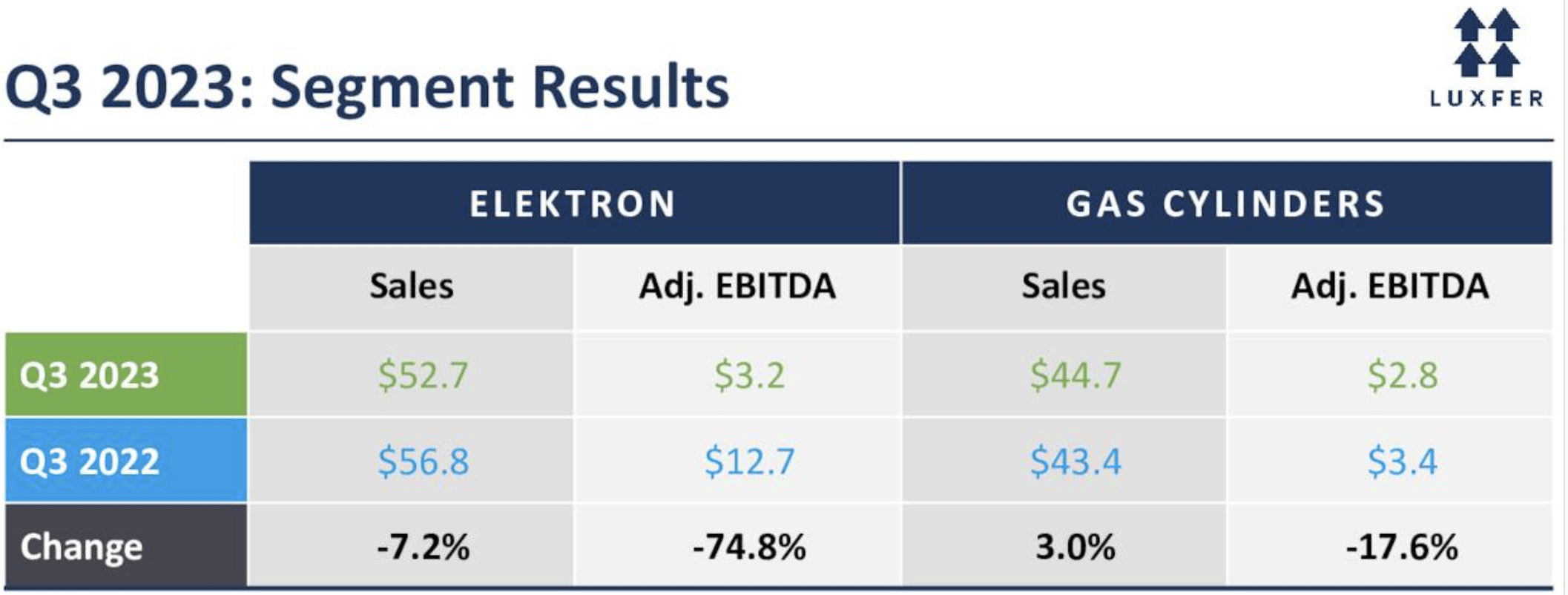

Gas Cylinder

I won't go into the detail of what this segment is as I have that covered in my initial coverage of the company. I will look at how this segment performed over the last while instead. Previously, I mentioned that this segment was a laggard compared to the other one, which is the Elektron segment. If we look at how this performed over the last three quarters, we can see a different image completely. I was hoping that Elektron would continue to perform well going forward, however, this is not the case as Gas Cylinder saw a slight increase y/y while Elektron saw a substantial dip in sales, which brought down the company's total sales. The primary reason the segment performed better (but still not that great) is the automotive industry saving the day, which saw an increase of 6% y/y. Transportation accounts for approximately a third of the total revenues of the company. So, the segment is doing better than I anticipated in my previous article, which is a good sign, but it is not enough to pull the company forward, especially when we factor in the other business segment.

Elektron Segment

The darling of the company, at least back when I only had the results of FY22, where the revenue saw an increase of 20% y/y. Fast forward 3 quarters and the company saw obstacles in the segment. The obstacles have not changed since my first coverage: supply chain issues are still being blamed for the poor performance in the segments coupled with the problem with sourcing magnesium. The company had to find other sources of magnesium because of the disruptions of their supply originating from the US magnesium force majeure declaration. This led to an increase in prices of magnesium as the company was forced to look for other suppliers. This did not bode well for the performance of the segment.

{kind=link}

Macroeconomic Conditions

The macroeconomic conditions have not been favorable for the company either. High-interest rates, tight labor conditions, and geopolitical tensions around the world have impacted some of the demand for its products, especially in the General Industrial end markets, which saw a whopping 30% decrease in sales in the latest quarter, which is on top of 23% decrease in the previous quarter, and 8% in Q1.

It doesn't look like the conditions are going to improve any time soon. The Graphic Arts business sector within the General industrial segment is seen to be performing the worst because of the competition from Europe. These competitors are sourcing their materials from lower-priced Chinese counterparts, and even with magnesium coming back online in the US, I don't think this is going to solve the company's issues at least not in the short term. The management mentioned in the latest transcript that they intend to source lower-priced magnesium sometime in 2024, but that remains to be seen.

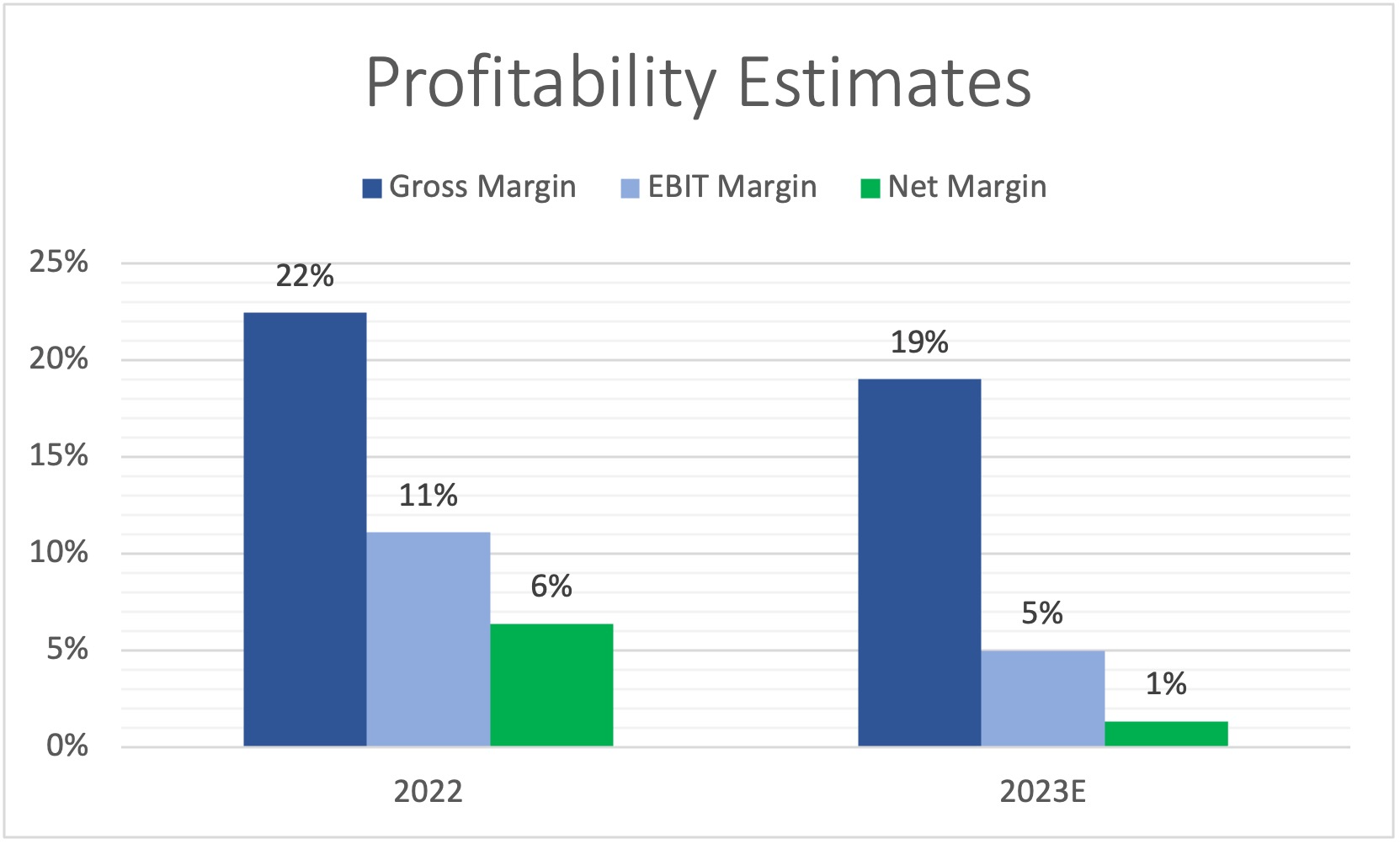

Margins

When looking at margins and how these have performed compared to FY22, there is a night and day difference. All were caused by problems within the industrial sector and macroeconomic conditions that brought on higher production costs throughout the business. This led to the company's margin deteriorating dramatically when compared to FY22, and it doesn't look like it is going to be fixed for at least another year or two, which will weigh on the company's share price performance. Below is the graph of how the margin may look like once the company reports FY23 results in the next few months (Seeking Alpha indicates the next quarter will be announced in February).

{kind=link}

The management has mentioned over the last few quarters just as it did before that they are willing to exit some of the ventures that do not perform well in the future, and if the Graphic Arts segment is not going to turn around, I could see the management taking some initiatives in exiting the segment to improve margins. The management has already cut 20% of the workforce within Graphic Arts and Magtech to improve margins. I am a little skeptical because, in my previous article, I mentioned that the company is looking to improve profitability with what I thought were promising cost-cutting measures, but we can see that it didn't work at all, so I would like to see actual results before praising the management's initiatives.

So, overall, we can see that it has been a very tough year for the company. It has not been particularly good for many companies, but Luxfer seems to be affected rather heavily by what is going on with the macroeconomic conditions. These conditions and how the company has performed so far will play a huge role in the next section where I will try to value the company's future performance.

Valuation

Quite a lot has changed since March. 10-year treasury yields went from 3.9% to around 4.4% right now, which has come down from around 5% just a couple of weeks ago. This will affect my valuation analysis to an extent. What will affect the valuation substantially is the future outlook is not looking as rosy when we looked at the numbers from FY22 and we tried to come up with reasonable assumptions for the next 10 years, which were based very closely on FY22 numbers. Now, we can see that it is not correct to assume that the company will perform well in the short term because of all the obstacles mentioned above that destroyed the company's margins.

For revenue, I decided to be on the conservative end here too and I have the company growing from low-single digits for the conservative case and base case, and mid-single digit growth for the optimistic case. Below are those assumptions.

{kind=link}

In terms of margins and EPS, my assumptions changed dramatically due to the poor performance the company experienced and the lack of improvement in the short run, which made me more cautious for the future. I do believe that eventually, the company's profitability will improve once again, however, it will take a while, and that is exactly what I have modeled below.

{kind=link}

For some extra margin of safety, I went with a 10% discount rate instead of the company's WACC, which was around 7%. I also went with a 2.5% terminal growth rate for the DCF valuation. On top of these assumptions/estimates, I added a further 15% margin of safety just to be extra cautious. With that said, LXFR's intrinsic value and what I would be willing to pay to take on the risks is $5 a share, which is a very different outcome than what I had assumed in March.

{kind=link}

Closing Comments

So, a lot has changed in the last 3 quarters, and the share price has reflected such a bad performance accordingly in my opinion. The company's outlook is not looking too good right now and it is unclear whether the company will recover sooner rather than later, therefore, even after a 46% depreciation in share price, I do not recommend starting a position here as the risk/reward although more favorable, still too risky if the company's cost-cutting initiatives are not going to bear fruit in the end. I am not recommending selling as I am looking at this from a new investor's perspective who has no capital in the company yet. It seems that the company still has some ways to go down and I will be looking for improvements in operations before considering opening a position for the long term.

If the company's performance remained as looked like it was going to go well just like I assumed in March, then 46% depreciation in price would have been unjustified, however, things just got worse and so I think the drop in share price was justified.

For further details see:

Luxfer Holdings: Price Decline Justified, Risks May Keep Prices Low For Longer