LXFR - Luxfer: Wait For A Better Entry Point

2023-03-10 01:39:51 ET

Summary

- Good financial results in 2022 and promising growth opportunities could reward Luxfer's shareholders.

- Solid financial metrics show the company is managed well and is profitable.

- Those growth factors may not be as exciting as they look on paper.

- Conservative assumptions say the company is slightly overpriced and uncertainty in the economy may bring the share price down.

Investment Thesis

FY2022 results saw a double-digit increase in revenues in Elektron Segment and with a slight increase in the Gas Cylinder revenue segment. Solid financial ratios and metrics at Luxfer Holdings ( LXFR ) prompted me to look into the future growth potential, with conservative assumptions on growth to keep it safe, the company is close to being a good buy but with the global economy still in uncertainty, I believe there will be a better time to buy the company for the long run.

Briefly on the company and FY2022 Results

Luxfer Holdings PLC is a company that makes different kinds of materials and products for various industries, such as defense, healthcare, transportation, and energy. It has two main divisions: one that makes gas cylinders for storing high-pressure gases, and another that makes special metals and chemicals for various purposes.

The Gas Cylinder segment provides high-pressure carbon fiber cylinders for compressed natural gas and hydrogen vehicles, lightweight air cylinders for firefighters, and medical oxygen cylinders for hospitals and home care.

The Elektron segment provides magnesium alloys for lightweight automotive parts, zirconium chemicals for catalytic converters, and flameless heating technology for military rations and emergency relief.

Net sales have increased 13.2% y-o-y with a lot of the increase attributed to the passing through of material cost inflation and an increase in sales of magnesium powders, a pickup in demand for commercial aerospace and medical applications, and higher demand for zirconium products in industrial applications.

The results were good but were not outstanding. The Electron segment, however, did show some potential as the sales in that segment increased over 20% y-o-y, while the Gas Cylinder segment went up only around 4%.

Growth Prospects

What is in store for the future? The management is seeing some softening in revenues in the first half of '23, and then revenues pick back up to normalized levels. This is largely due to price inflation not being under control and the cost of goods will decrease profit margins slightly for the next year or two. To combat this, the management is taking some cost-cutting measures that already are bearing fruit by saving around $1m annually, which helps recover margins as that is one of the priorities they have mentioned. The supply chain issues are continuing to improve in broad terms, so cost issues should subside within a couple of years and with the implementation of cost-cutting techniques right now, the company will become more efficient once inflation subsides and may see higher profit margins than they have historically.

Gas Cylinder Segment

This segment seems a bit lacking compared to the Elektron segment, however, it still accounts for over 45% of the total revenues of the company. The management is going to focus on what they believe will be the most profitable products within this segment, and that is the further development of the hydrogen market. They are looking to increase the adoption rate of hydrogen fuels for public transportation, particularly in Europe. The transportation segment accounted for over 30% of total sales and the company is very focused on sustainability which will bode well with socially responsible investors, mainly the younger generation. I could see this boosting revenues in the future if the management can implement the sustainability measures further and an increase in the adoption of alternative fuels worldwide will benefit the company.

Elektron Segment

This segment has seen the highest y-o-y increase, going up around 22%. The management sees this segment as being the most profitable in the future and will reinvest a good portion of the company's free cash flow into the high-visibility growth projects within the segment. The management did not disclose where they are going to invest, but they did mention that the commercial aerospace, automotive and military sectors were seeing the most demand in the last year, so I would venture a guess that these three sectors would be their focus in the coming years, especially aerospace and automotive within the MEL Technologies as the management is going to invest more than half of their planned capital investment budget in '23.

The management seems to be competent and I like that they will shift their focus toward what is most profitable within the two segments and shows the most promise in the future. The cost-cutting measures could also show up as discontinuing some products that do not offer high-profit margins or are being produced at a loss, but the management does not disclose that. Maybe they will mention something in the near future.

Sustainability Could Drive Further Growth

With the focus on alternative fuels and lightweight products, I believe the company can attract some of the younger generations of investors who are focused more on sustainability and ESG factors when it comes to their investment decisions. Socially responsible investors can see that the company is starting to perform quite well within these factors as they have reduced their absolute emissions by 30% compared to '21. According to these statistics here , the company is right now at medium risk in terms of ESG, however, they have been improving quite a bit and are perceived as a much more sustainable company than its peers in the industry. With how they are reducing their global emissions y-o-y, I could see their rating improving further which will attract more socially conscious investors, particularly the younger generation.

Financials

The company doubled its cash position from last year and believes that it will have an even stronger position in '23. This cash flow generation helped them reduce their outstanding long-term debt by $7m. I'm not a big fan of debt but if the debt reduction is being prioritized and mentioned as the management has done here, I do not see an issue in that regard and so the debt figure is not a red flag.

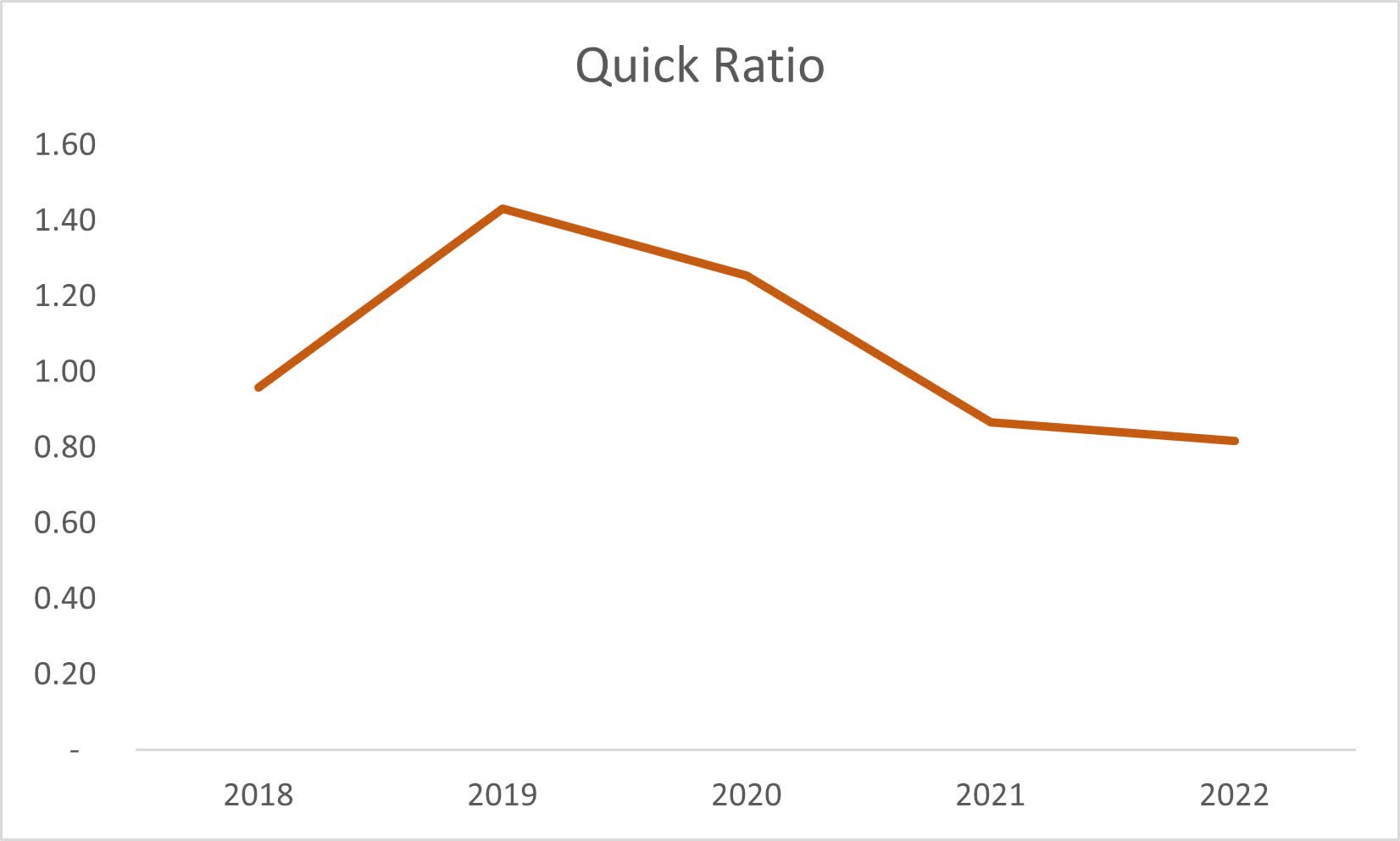

In terms of liquidity, the quick ratio, which measures a company's ability to pay off its short-term obligations with the most liquid assets on the books has left me with a tiny red flag, but it is not a deal breaker. It is currently sitting at .82 which means they are not able to pay off their short-term obligations efficiently.

Quick Ratio (Own Calculations)

{kind=link}

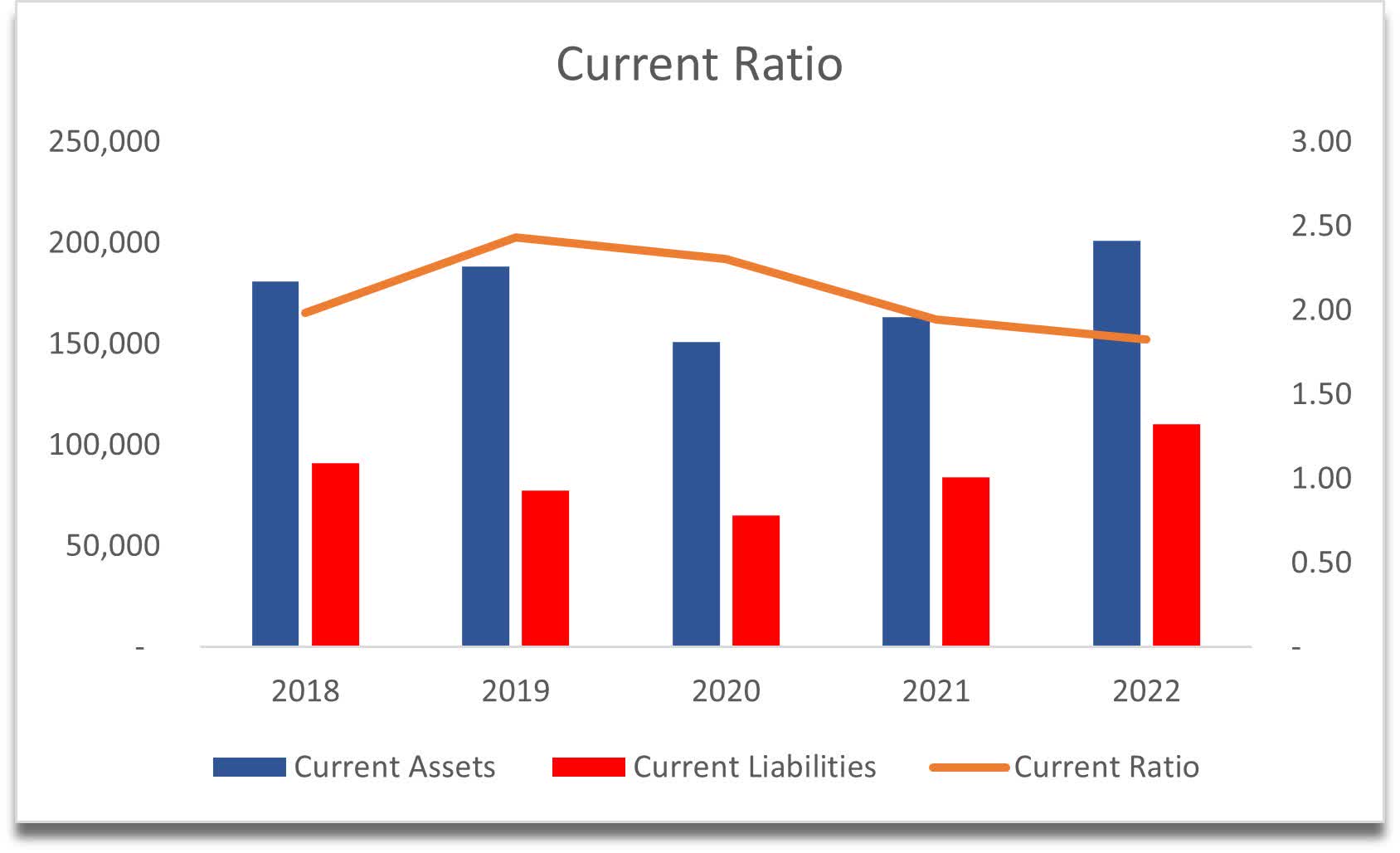

This does not concern me because just a few years back they were above 1 and they would be able to reach that figure again with proper management. If we look at the less strict measure of liquidity, the current ratio is quite healthy and if the company manages to achieve a ratio of over 2, then it would be even more attractive as an investment.

Current Ratio (Own Calculations)

{kind=link}

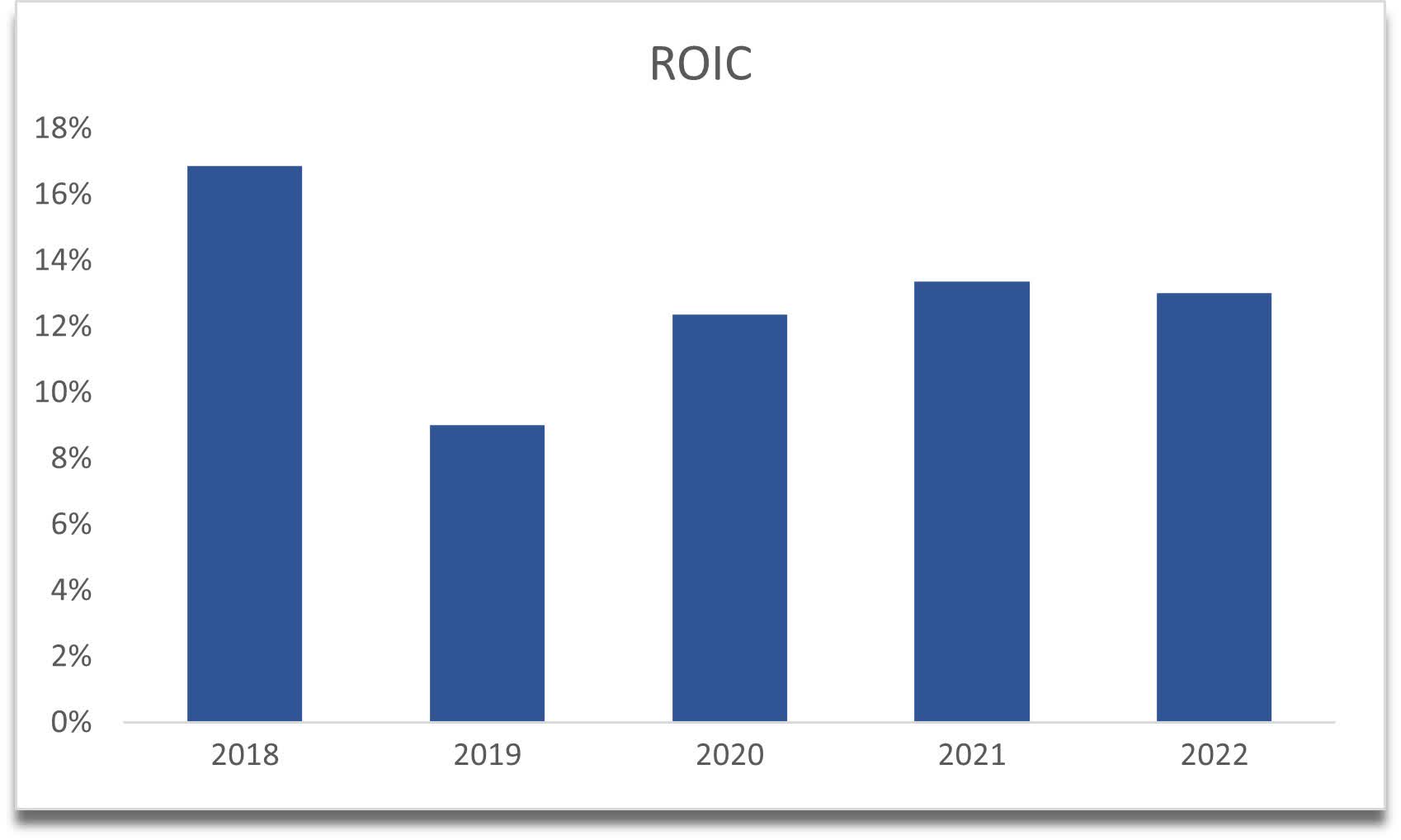

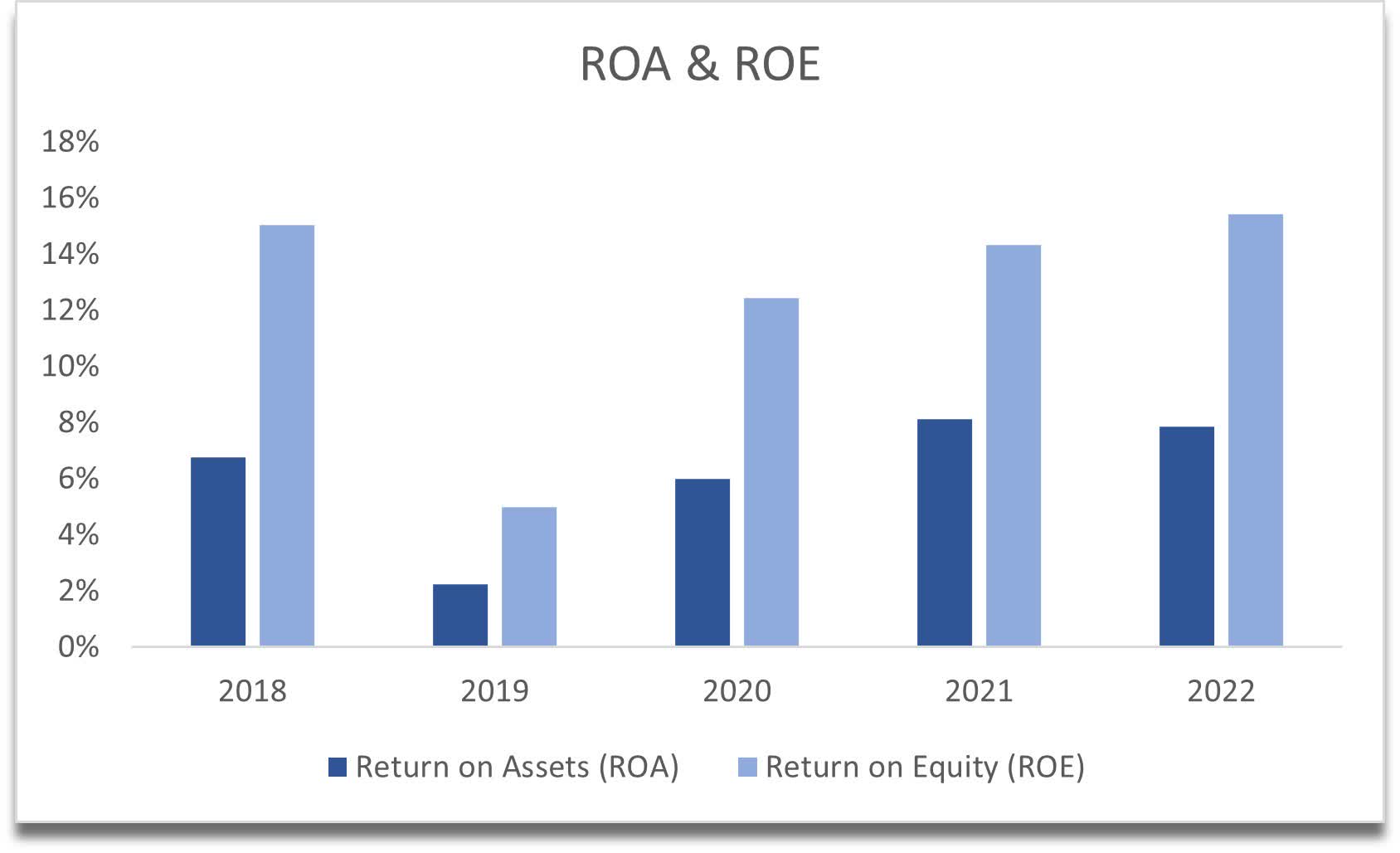

The following metrics that made me look into this company further were ROIC, ROA, and ROE. My stock screener searches for specific numbers here and the company met my requirements of profitability. These metrics are quite good, which shows that the management is effective and value-creating. If ROIC is exceptionally high, I would be willing to pay a premium, however, here, these metrics are acceptable.

Return on Invested Capital (Own Calculations) ROA and ROE (Own Calculations)

{kind=link}

{kind=link}

I do like seeing uptrends in these metrics, which I hope continue in the future.

Overall the management has done a good job in running the company and I did not see any major red flags that would deter me from a potential investment, which depends not only on the balance sheet strength but also on growth prospects in the future.

DCF Valuation

The market cap of the company is around $430m, which is quite small. Over the last 10 years, the company saw a lot of revenue fluctuations but none of the increases or decreases were over 15%. There is not much growth potential that could propel the revenues much more than they have in the past and so in my model, I took a conservative approach to be on the safe side. The company could perform well if it manages to reduce costs, which in turn will improve profitability margins. For this model I looked at the potential growth of the Elektron Segment and Gas Cylinders Segment separately, giving different growth assumptions to both.

Since Elektron has performed much better than the Gas Cylinders, and also it accounts for over 55% of total revenues, I gave this segment higher growth rates over the next decade. In my base case scenario, I modeled 15% growth in '23, 10% in '24 and '25, and then around 6% over the next 7 years, which give me 8% average growth per year for the decade. In my conservative case, 10-year average growth goes down to 6% and in my optimistic case, it sits at 10% per year.

For Gas Cylinders, a low revenue increase at the beginning, which then picks up in '25 and '26, and then comes down to low single digits for the remainder of the model. Growth in '23 I modeled at 3%, 5% in '24, 8% in '25 and '26, and then for the remainder of the model it averages out to 4% a year. These assumptions give me a 5% average growth per year for the decade in the base case scenario, 3% in the conservative case, and 7% in the optimistic case.

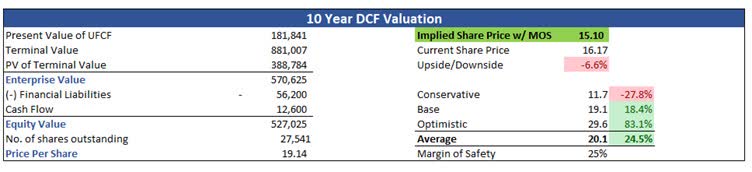

I could not be very optimistic in my assumptions, because the company has not seen any prior huge increases in revenues, and given the above-mentioned growth prospects, which are hard to put a number on, I believe these numbers are conservative enough. Just to make it even safer, I also added a 25% discount on the final share price. With that said the 10-year DCF model shows the intrinsic value of the company to be $15.10 per share, which implies the company is slightly overvalued.

10-year DCF Valuation (Own Calculations)

{kind=link}

Closing Remarks

So what does that mean? Well, if you believe the assumptions are justified and the growth prospects are there but are not that exciting, the company is slightly overvalued and could do with a drop to where in the long run it will be a great company that could award its shareholders. With a lot of uncertainty going on in the world, I will not be surprised if the company does come down further and becomes much more attractive in the long run. If the management's focus on the most profitable products works out, then the company can become more efficient and could see an appreciation in the share price, but also, if they are not able to, the share price could stay flat or even deteriorate, but only time will tell. Nevertheless, my watchlist is updated with price alerts that are lower than the current share price, and I am looking forward to seeing how the economy unravels in the near future.

For further details see:

Luxfer: Wait For A Better Entry Point