PPRUF - LVMH: A 'Must Own' Company At The Right Price

2023-07-17 11:00:53 ET

Summary

- LVMH is well-positioned to benefit from the growth of the luxury goods industry, particularly in China, due to its strong market position and renowned brands.

- The company consistently surpasses analyst estimates and maintains an impressive margin profile, with a net debt position of €9.2 billion providing financial stability for further investments and shareholder returns.

- LVMH is poised for solid growth over the remainder of the decade, driven by several factors, with revenue growth in the high-single digits through 2026.

- Despite a promising outlook, the current share price of €890 is slightly above fair value, leading to a hold rating on the shares and a recommendation to wait for prices below €815.

Investment thesis

I initiate my coverage of LVMH Moët Hennessy - Louis Vuitton, Société Européenne ( LVMUY ) with a hold rating following my in-depth analysis of the company and the underlying industry.

The luxury goods industry presents a promising outlook for investors. The industry has demonstrated steady growth over the past two decades, showing resilience during economic downturns and quickly recovering thereafter, resulting in a long-term CAGR of around 6%. Today, there are several trends and developments, like the increasing number of high-income individuals and the shift towards digital, with the potential to further boost the luxury goods industry for many years.

LVMH's strong market position, renowned brands, and ability to recognize industry trends make it well-positioned to benefit from the industry's growth drivers, particularly in China. And as the most prominent luxury company globally, LVMH boasts an impressive market share of 15%, surpassing its closest competitor by a wide margin, meaningfully increasing its competitive advantage.

Financially, LVMH keeps on delivering outstanding performances, consistently surpassing analyst estimates and maintaining an impressive margin profile. Meanwhile, LVMH's solid balance sheet, with a net debt position of €9.2 billion, provides financial stability and flexibility for further investments and shareholder returns. These qualities make it stand out as the ideal investment choice to capitalize on the growth of luxury spending.

Looking ahead, LVMH is expected to maintain its growth trajectory, albeit at a slightly moderated pace. While the macroeconomic environment and consumer spending may slow down in FY23, a recovery in China and continued market share gains should support a solid revenue growth rate of 12% for the year. LVMH's focus on optimizing marketing expenses and improving margins is projected to drive slightly faster EPS growth at 17%.

In this article, I will take you through the company fundamentals, latest developments and financial results, and underlying industry trends to end up with a revenue and EPS forecast through 2026 to determine whether this company is an attractive buy today.

The outlook for the luxury goods industry is promising

Some companies are simply a must-own in any portfolio due to their impressive resiliency, strong competitive advantage, strong brand, and ability to compound money impressively. The same can be said about a number of industries and sectors that consistently experience long-lasting tailwinds, driving impressive growth for industry leaders. The luxury goods industry is one of those.

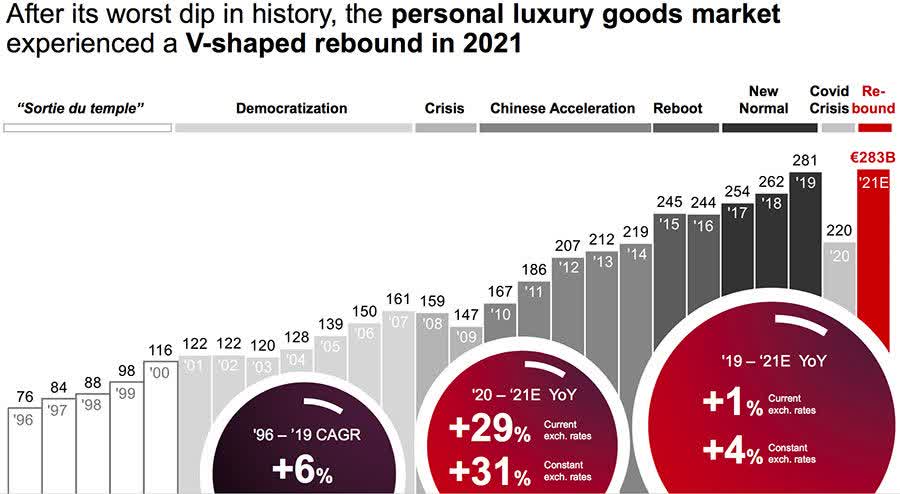

That the luxury goods industry is a very interesting one for investors is perfectly highlighted by the graph shown below. This shows that the industry has experienced steady growth over the last two decades as it grew through recessions, pandemics, and different phases. And while the industry is not entirely resilient against economic slowdowns or recessions, the graph shows that growth quickly returns once the economy and consumer spending recover, overall averaging a growth CAGR of slightly above 6% .

Also, the industry is protected by the fact that the most obvious consumers of luxury goods don’t balk at price tags. As a result, the luxury industry is not impacted by economic headwinds quite as much as other industries are in my view. While the luxury industry tends to dip slightly, as seen in 2008/09 (a dip of about 9%), the dip is far from severe and the industry usually quickly recovers, reaching new highs in the year after.

{kind=link}

The US is currently the largest luxury market, accounting for around 30% of all luxury spending. Yet, while demand will remain solid, the US luxury market is already very mature and will probably not be a growth driver for the luxury industry. A region that is much more interesting from a growth perspective is China, which currently accounts for slightly above 20% of global luxury spending but will grow to account for 25-27% by 2025 as the growing middle class and increasing wealth in the country are a solid driver of luxury spending. Crucially, LVMH is also a leading force in these regions as brands like Dior, Louis Vuitton, and Bulgari are among the most popular ones .

That China will indeed be a growth driver in the luxury goods industry is once more highlighted by Research and Markets, which believes China’s luxury goods industry will grow at a CAGR of 7.3% through 2030. This is somewhat faster than the 5.4% CAGR projected for the global luxury goods industry. This growth will be driven by a rising number of high-income population groups, especially among Gen Z and millennials, and the growing focus on sustainable products in the luxury industry. Highlighting this, The Gen Z and Millennial generations are predicted to account for 70% of global luxury spending by 2025 due to the rapidly growing spending power of these generations.

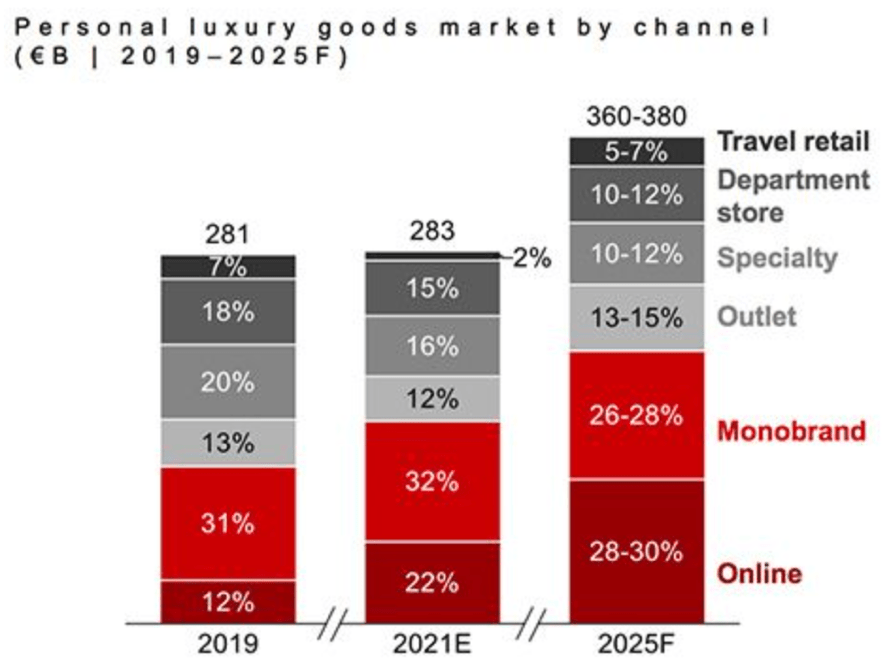

Driving growth in luxury spending among the younger generations is also the shift towards digital with large fashion conglomerates like LVMH and Kering increasingly focusing on online shopping, buy now, pay later programs, and the lure of crypto and NFTs. This is highlighted by the fact that 41% of Gen Z state that they have purchased a luxury item in a virtual world, according to Ypulse . Also, over the last year, traffic to luxury brands’ websites grew, on average, by 31%, showing a clear shift towards digital, also highlighted by the graph below.

{kind=link}

An example of this shift to digital platforms is the metaverse which creates a massive opportunity for luxury companies from several perspectives. This is how Deloitte described this opportunity in a recent report:

The metaverse gives luxury companies an unprecedented opportunity to re-invent the luxury experience, build credibility, brand engagement, and brand loyalty in the metaverse communities. The digital reality offers new ways for consumers (their traditional audience and a new target audience of tech-savvy young consumers) to interact with their products while being consistent with the true nature and essence of the brand.

Meanwhile, the growing adoption of second-hand luxury is expected to be a drag on growth for luxury goods companies. Still, the positives clearly outweigh the negatives here and it is safe to assume that luxury goods will always remain in high demand, even as the industry dips in line with the economy, which is highlighted by the rapid recovery seen in 2021/22. This shows that the industry remains in great health, and looking at current trends, it is also far from boring as there are plenty of opportunities to move (further) ahead of the competition by recognizing trends and operational excellence. And while the changing sense of luxury might require luxury brands to transform and adapt, the luxury market itself will continue to grow for many decades, driven by multiple important trends.

LVMH is the perfect play to benefit from growth in luxury spending

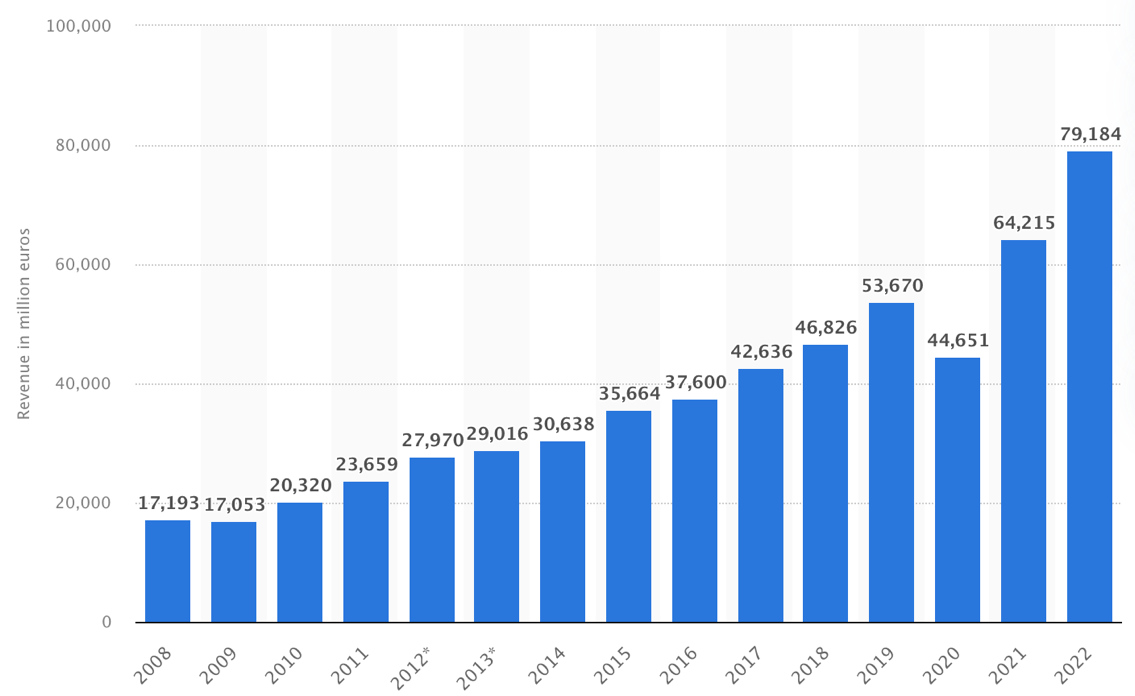

The largest luxury company in the world is LVMH, also known as Moët Hennessy Louis Vuitton. Established in 1987 LVMH has grown into one of the world's largest and most prestigious luxury goods companies. Its sheer size and exposure to multiple luxury markets have allowed it to generate a similar growth graph as we have just seen for the general market, except LVMH has grown at almost twice the pace of the luxury industry as revenue has grown at a CAGR of over 11% in the last 14 years. This has resulted in the company holding an impressive 15% market share in the global luxury goods industry, far ahead of second place Kering ( PPRUF ) with just a 5% market share. This impressive market share lead in this highly fragmented industry gives LVMH a lot of control over the market and makes it the perfect play to benefit from growth in luxury spending.

LVMH revenue development (Statista)

{kind=link}

LVMH operates through a decentralized structure, with numerous prestigious brands (75 fashion houses) under its umbrella, spanning multiple sectors, including wines and spirits, fashion and leather goods, perfumes and cosmetics, watches and jewelry, and selective retailing. Some of the most recognizable and esteemed brands owned by LVMH include Louis Vuitton, Christian Dior, Fendi, Tiffany & Co, Bulgari, and Tag Heuer, among many others. The company has shown over recent decades that it is a true acquisition machine with an exceptional capability to pick out the strongest brands, acquire them, and make them even stronger.

LVMH's strategy is also quite unique. The company encourages each brand to maintain its unique identity and creative freedom while providing them with extensive support in terms of resources, expertise, and distribution networks, making each single one of its established brands purely unique. In a sense, the company tries to avoid synergies between brands which keeps them unique and special – a crucial aspect of brand success in the luxury industry.

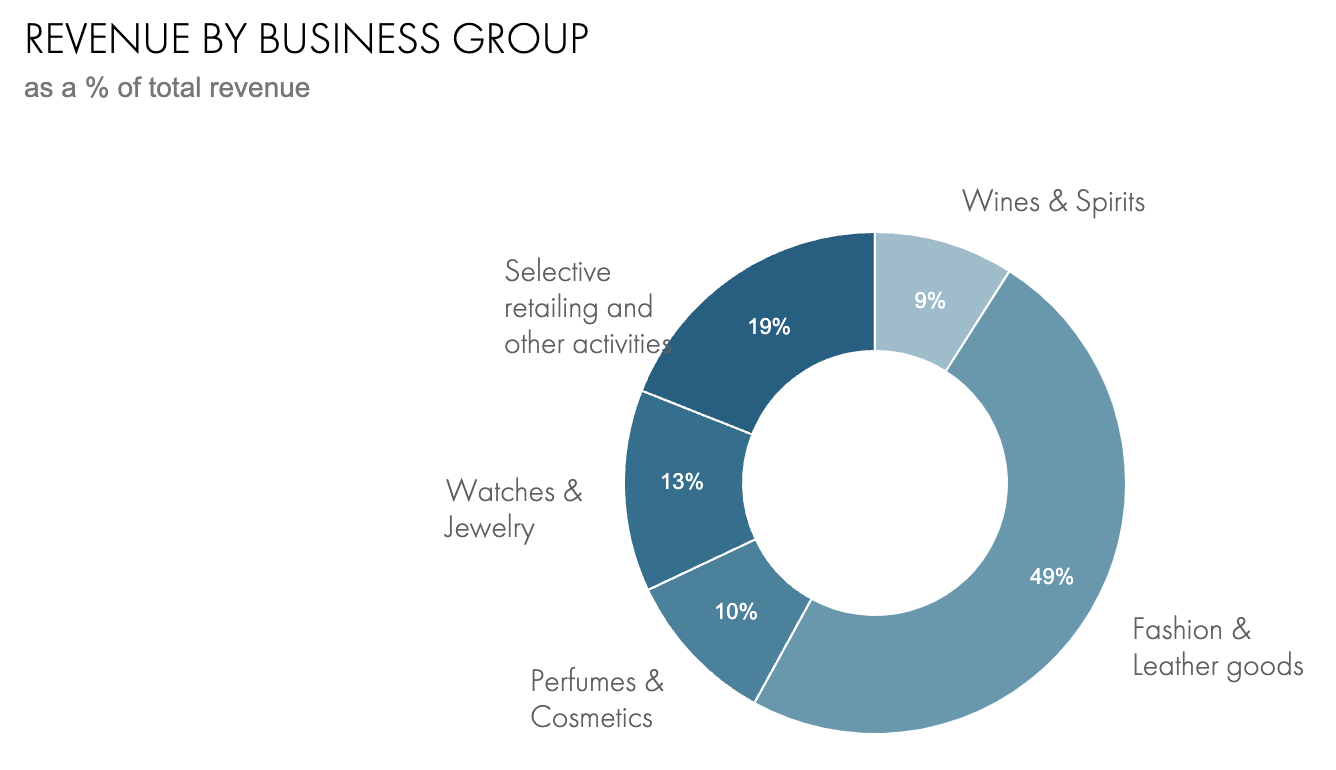

The company reports revenue across five separate business groups, of which Fashion and Leather Goods is by far the largest as it accounted for 49% of FY22 revenue, primarily driven by the Louis Vuitton and Dior brands which, according to several sources, account for 75% of this group’s sales. Louis Vuitton alone is already good for $20 billion in annual revenue, making it by far the most important brand in the LVMH portfolio. And despite Fashion and Leather Goods being the largest segment for LVMH, it was also one of the fastest growing ones with FY22 revenue growing 25% YoY and organic revenue growth coming in at 20% YoY, driven by the sheer popularity of its brands. This should not come as a surprise, though, as both of these brands are among the top 10 most desired luxury brands among the millennial and Gen Z generations, which account for the majority of growth in the industry, as also discussed in the previous section of this article.

And LVMH has been focusing on servicing these generations for years already. For example, it has introduced more customization possibilities for several brands, including Louis Vuitton, and is increasingly introducing sustainable materials in its luxury products. Also, the company has been acting on the earlier discussed digitalization trend and has favorably positioned its brands to fully benefit. As a result, LVMH holds three positions in the list of the top 15 most popular luxury brands online, with Dior even holding the #1 position. The brand has been gaining significantly over recent years with it gaining 7 positions on the list in the last 6 years, highlighting LVMH’s ability to spot industry trends and act upon it.

In the luxury industry, it is incredibly important to be aware of customer preferences and adapt while maintaining brand profile and exclusivity. This is where LVMH shines, allowing it to grow into the conglomerate it is today and will enable it to keep growing for many years. The underlying strategy and thinking behind the conglomerate are simply sublime and unmatched.

Moving back to the company’s reporting structure, besides the Fashion and Leather Goods segment, there is the Watches and Jewelry which accounts for 13% of total revenue and saw solid organic growth of 12% in FY22. Perfumes and Cosmetics account for around 10% of revenue and reported organic growth of 10% in FY22. Wines and Spirits accounted for 9% of total revenue and grew by 11% organically in FY22. Finally, there is selective retailing and other activities which is the second largest segment for the conglomerate and includes retailer Sephora, travel retail specialist DFS, newspaper Le Parisien, and luxury travel specialist Belmond, among others. This final segment accounts for 19% of revenue and reported solid organic growth of 17%, driven by the recovery in travel. Overall, LVMH has an incredible portfolio of brands spread across several luxury segments, giving the company excellent exposure to the entire luxury industry.

{kind=link}

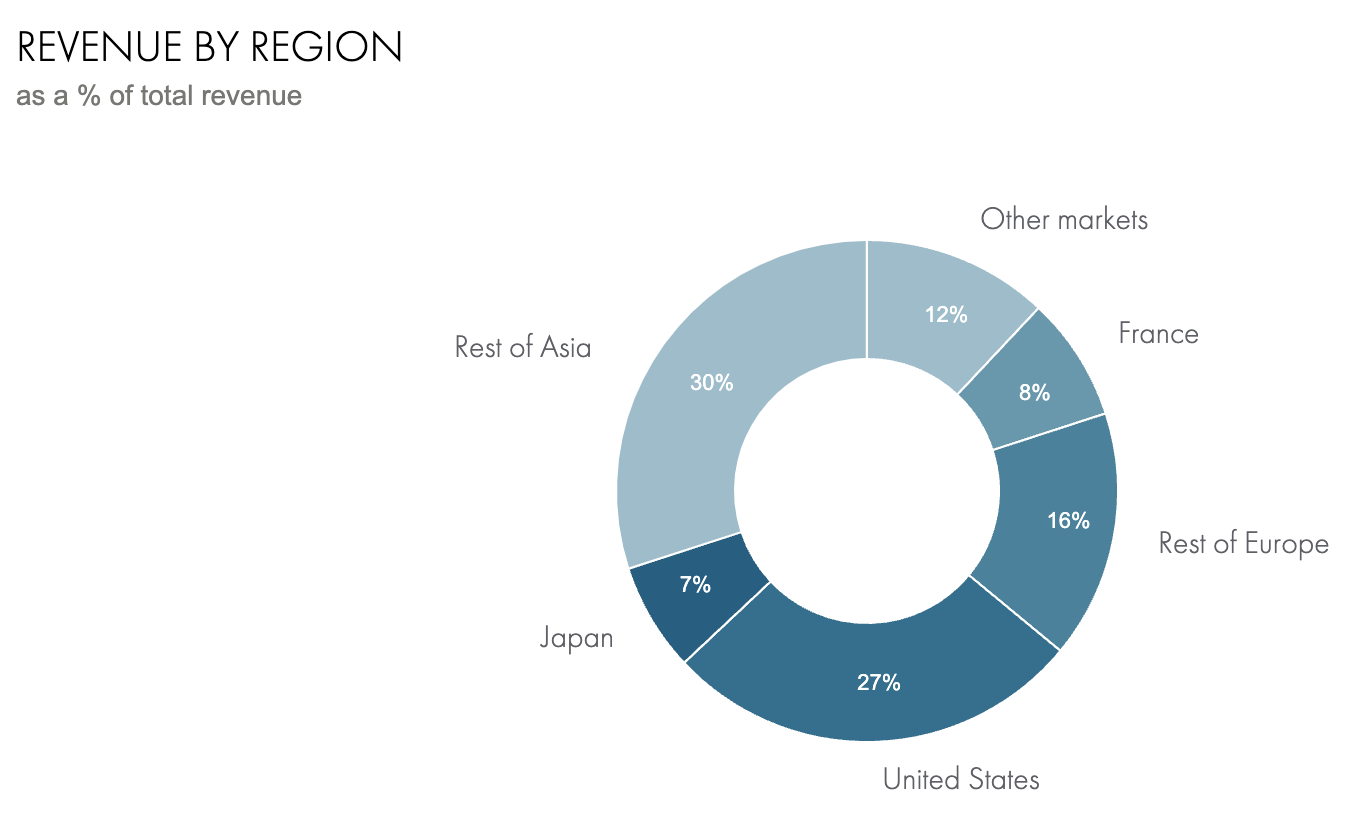

LVMH also has excellent global exposure with no single geographical region accounting for a significant majority of its sales, showing excellent geographical diversification. Moreover, LVMH is well positioned to benefit from the increasing popularity of luxury products in Asia (excluding Japan) as 30% of the company’s revenues already originate from this region, making it its most important region. In 1Q23, this even increased to 36%, driven by a recovery in China. The US closely follows with 27% of FY22 revenue and Europe (including France) accounted for 24% of FY22 revenue.

This means the company does not depend overly much on one single region, although 30% exposure to Asia could still be viewed as risky. Yet, with Asia expected to outgrow Europe and the US, I view this as a meaningful positive for LVMH as the company already has a solid foothold in the region, as explained before. Overall, the company’s brands are massive on a worldwide scale, giving it a strong advantage over competitors.

{kind=link}

FY22 and 1Q23 highlight LVMH’s operating excellence

Moving to the company’s financials, there is also not much to complain about here. 2022 was a record year for LVMH as the company reported revenue of €79.2 billion, up 23%. This was driven by 17% organic growth and a 6% positive effect from FX. The company’s performance remains impressive, consistently outperforming analyst estimates by a fair margin.

To put the company’s size into a bit more perspective, Richemont ( CFRUY ) and Kering reported revenue of around €20 billion, while Hermes ( HESAY ) reported revenue of €12 billion in FY22. Clearly, LVMH is in a class of its own, giving it significant financial benefits. As indicated during the 4Q22 earnings call, LVMH’s size advantage allows it to continue investing rapidly to gain market share, especially as a challenging macro environment might force peers to cut back on investment due to tighter financial constraints.

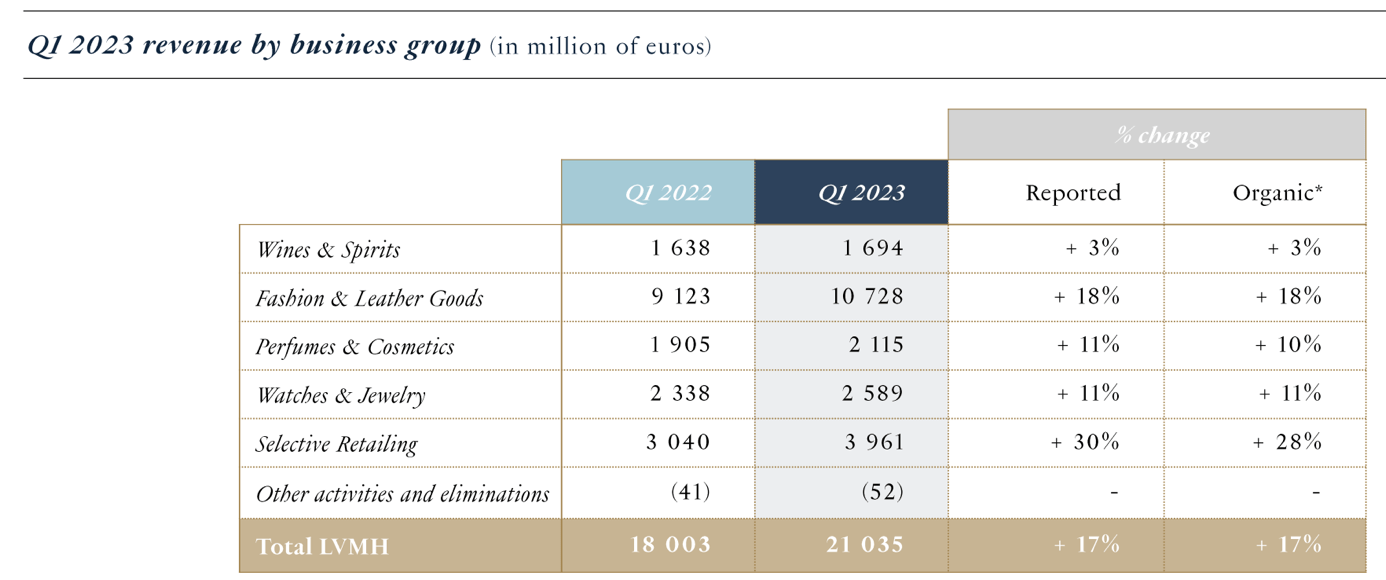

And we could see this happening in FY23 as growth will slow due to a deteriorating macroeconomic environment and slowing consumer spending. Still, the company is in a strong position, as highlighted by its Q1 results in which revenue again increased by 17% YoY, on top of an already strong Q1 last year. This was driven by solid growth in all business segments and regions. Growth in Europe and Japan was especially strong, growing 24% and 34%, respectively.

In the different operating segments, growth in Fashion and Leather Goods stood out once more as this increased by 18% YoY due to a strong continued performance for both the Louis Vuitton and Dior brands. The Selective Retailing segment also recorded strong growth of 28% YoY as Sephora keeps gaining market share and DFS benefitted from a recovery in travel.

{kind=link}

Moving to the bottom line, in FY22 (as LVMH does not report margins in Q1 and Q3), the gross margin was a very impressive 68%, which was relatively flat YoY despite high inflation.

The operating profit totaled €21.1 billion with an operating margin of 26.6%. There were some doubts among analysts about whether the company would be able to maintain this impressive margin in 2022 but the company was very well able to, despite a slowdown in growth in the second half of the year and relatively high marketing expenses as the company remains committed to further market share gains. In luxury, increased marketing is very often the way to go. This resulted in an FY22 free cash flow of €10.1 billion, which fully covers all further obligations like the dividend and share repurchases.

Although it is tough to compare LVMH to its peers as the company has twice the market cap of second-place Hermes, it can give some valuable insight into its margin profile. Comparing LVMH to Hermes, Richemont, and Kering, it looks very competitive overall and margins are very similar. Hermes clearly is in its own league but is a very different company, focused on high-end luxury while being much smaller. Overall, LVMH definitely has an impressive margin profile.

Margin comparison (Seeking Alpha)

{kind=link}

LVMH also has a solid balance sheet with a net debt position of just €9.2 billion, down from €9.6 billion at the end of FY21 but still meaningfully above a pre-covid level of €6.2 billion. The balance sheet looks healthy and LVMH should have no trouble paying down debt. This then allows the company to pay a solid dividend to investors. Shares currently yield 1.64%, which is not overly impressive, but LVMH has been growing the dividend at a rapid clip and will most likely continue to do so as it has the financial resources. This can be seen in its 5-year dividend growth CAGR which stands at 19%, while still keeping the payout ratio relatively low.

Outlook & LVMH valuation

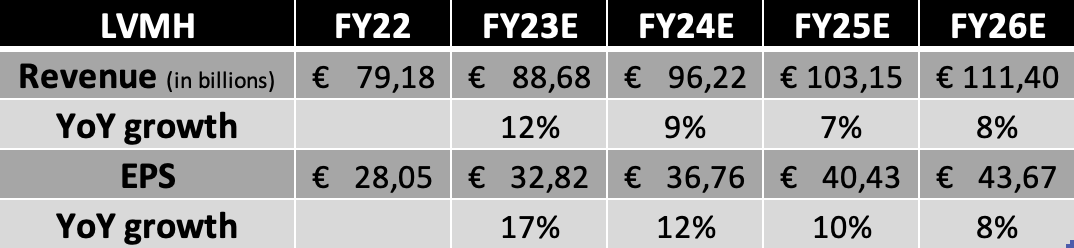

Following my analysis of LVMH, its fundamentals, competitive positioning, recent performance, and the underlying trends in the luxury goods industry, I arrive at the following revenue and EPS estimates for LVMH through 2026.

Revenue and EPS estimates (Daan Rijnberk)

{kind=link}

Shortly explaining these estimates, I expect LVMH to see demand for luxury goods remain resilient in 2023 but growth to ease towards the end of the year as a further slowdown in consumer spending and a very strong performance in 2022 make it hard to maintain current growth rates. Still, a recovery in China will largely offset the expected slowdown in the US and Europe, which will support 12% revenue growth in FY23. At the same time, I project EPS to grow slightly faster at 17% as LVMH will lower its marketing expenses and improve margins.

For the following years, LVMH will most likely see a more normalized growth rate which sits a few percentage points above the growth rate projected for the luxury goods industry as the company will further increase its market share and pricing power, which will also allow for an improved margin profile, in turn driving even faster EPS growth. This results in a solid outlook with high single-digit revenue growth and close to double-digit EPS growth, which the company should be able to maintain for the foreseeable future, driven by its unprecedented moat and brand power.

Moving to the valuation, shares of LVMH are far from cheap after the share price has increased by over 60% over the last year and 30% YTD. As a result, shares trade at a very demanding 27x forward P/E. Yet, if we compare this to its peers , the valuation does not look that high considering that LVMH has a superior growth outlook, moat, and size. The premium over its peers, therefore, is justified. Furthermore, considering everything discussed in this article and the company’s impressive outlook in a very resilient industry, I believe a forward P/E of 25x is fair for this high-quality compounder.

Using this P/E and my FY24 EPS estimate, I calculate a target price of €919, leaving a minimal upside of 3% from a current share price of €890. (Please note, this target price is solely based on its forward P/E and is only for indicative purposes.)

Conclusion

LVMH is a truly stellar company with a management team that knows how to build a successful luxury fashion conglomerate. The company's unparalleled brand power, market positioning, and ability to adapt to evolving consumer preferences make it poised for sustained growth and continued success in the luxury goods industry.

Considering LVMH's impressive track record, strong competitive position, and the industry's positive outlook, its current valuation, although relatively high with a forward P/E of 26x, appears justified. The company's superior growth potential, robust moat, and unmatched size in the industry validate a premium over its peers.

Yet, with shares trading slightly above fair value and current upside limited to just 3%, investors are better off waiting for a dip in the share price and a better entry point. Therefore, at a share price of €890, I put a hold rating on the shares and recommend waiting for prices below €815 to ensure a better margin of safety.

For further details see:

LVMH: A 'Must Own' Company At The Right Price