LVMHF - LVMH: Domination Continues In H1 2023 (Rating Downgrade)

2023-07-25 19:00:18 ET

Summary

- LVMH just published its H1-23 results, demonstrating domination and differentiation in the luxury market, while its peers are struggling.

- Revenues and EPS crushed expectations, with 15% and 30% growth, respectively. Excluding the U.S., growth was broad-based across all geographies, with China, Japan, and Europe leading the way.

- Wines & Spirits decreased by 4%, Fashion & Leather grew by 17%, Perfumes & Cosmetics grew by 11%, Selective Retailing grew by 26%, and Watches & Jewelry grew by 11%.

- As I expected, LVMH is on pace for another double-digit growth year, easily exceeding consensus estimates. However, its great performance was overshadowed by the U.S. declines.

- I downgrade the stock to a Buy rating and update my price target to €964 per share, or $1,063 per LVMHF ADR.

Louis Vuitton, Société Européenne ( OTCPK:LVMHF ) ( OTCPK:LVMUY ) just announced its H1-23 results. Revenues totaled €42.2B, reflecting 15.0% growth, slightly below my expectations but significantly above consensus estimates. EPS amounted to €16.95, reflecting 30.4% growth, much better than expectations.

The luxury powerhouse continues to provide impressive results despite a weakening consumer, demonstrating its differentiation and domination in the luxury market.

Despite the great results, there are some signs of a slowdown, and the margin expansion story will take longer than expected. Thus, I downgrade the stock to a Buy.

Background

I initiated coverage on LVMH in March, claiming ' 2023 Should Be Another Stellar Year, It's A Buy '. I urge you to read that article, in which I described my investment thesis in detail, as well as the group's amazing operating model as a holding company, its unique leadership strategy, its operating segments, risks, and the major growth prospects I project for 2023 and beyond.

In short, my investment thesis in LVMH is based upon the immense pricing power it possesses with its portfolio of timeless prestige brands, as the never-ending demand for the group's products is resilient and isn't sensitive to the economic environment. In addition, I view the holding structure of LVMH as extremely beneficial for shareholders, with its management's unparalleled capabilities to acquire and significantly improve already-huge brands like Tiffany.

In April, I upgraded my rating to a Strong Buy, after the company dipped due to bad results of its competitors, while it's clearly at a different level. Since my March article, LVMH has performed in line with the market, which in my view is very impressive after a significant outperformance in 2022.

Now, let's focus on the company's results, see how my projections fared compared to the consensus, and see if it's still an attractive investment.

H1-23 Highlights

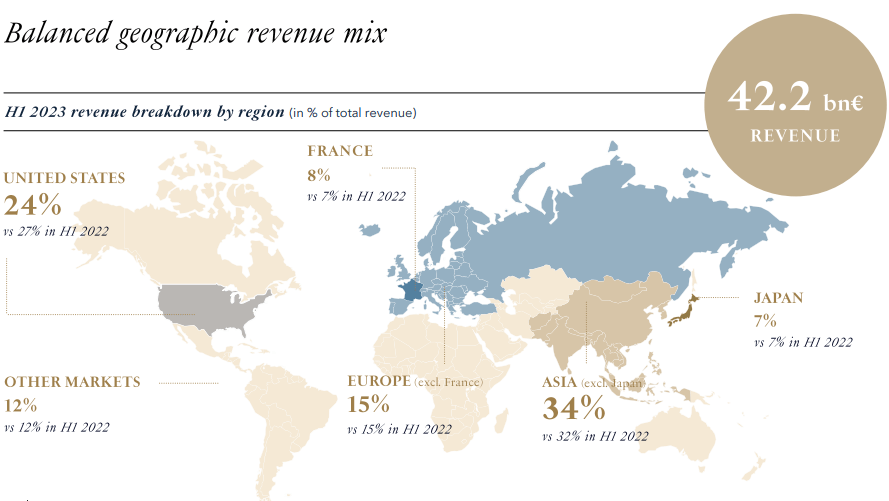

LVMH reported consolidated revenues of €42.2B, a 15.0% increase from the prior year. Based on its historical seasonality, the French conglomerate is on pace to deliver above 14.1% growth for the entire year. I'm very glad to see the company is on pace to beat consensus expectations of €85.3B for the year.

{kind=link}

Geographically, Japan grew by 29% in the quarter and 31% in the half, Asia excluding Japan grew by 34% in the quarter and 23% in the half, Europe grew by 19% in the quarter and 22% in the half, and the U.S. was the only declined with -3% in the quarter and 3% in the half.

Looking at the geographic sales dispersion, the U.S. has clearly declined compared to the faster-growing geographies.

{kind=link}

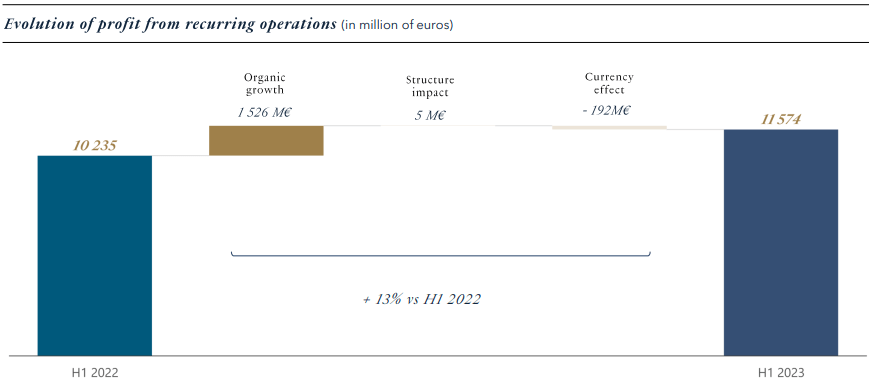

Switching on to profits, operating margins decreased by 17 bps, despite higher G&A costs which included material non-recurring items, and very high marketing activity, specifically in Fashion & Leather goods. Management expects margins to remain in line with 2022.

{kind=link}

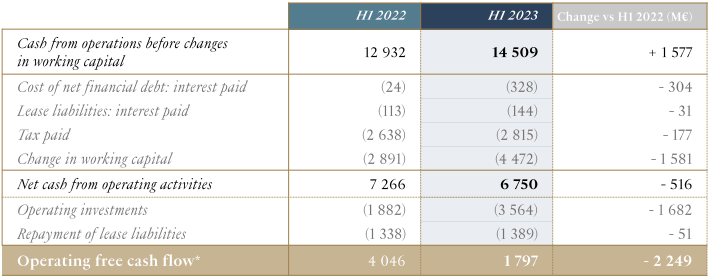

Looking at cash flows, operating cash flows decreased significantly primarily as a result of higher inventories and timing of debt repayments. Free cash flows decreased materially due to higher operating investments, as LVMH acquired and improved landmark properties like Tiffany 5th Avenue, during the half.

{kind=link}

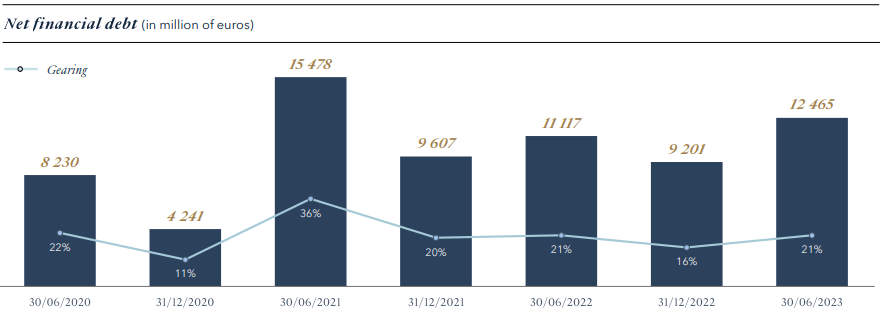

Net debt remained reasonable, with a slightly higher gearing percentage, as the group experienced higher operational investments in the first half.

Wines & Spirits

Created and calculated by the author using data from LVMH financial reports.

Wines & Spirits experienced a 4% decline (3% organic), whereas every other segment saw double-digit growth and above. The segment was dragged down by Cognac & Spirits, due to high inventory levels of distributors, and continued to suffer in China.

On the bright side, margins reached an all-time high, as the company pulled back marketing activities in light of weakening demand.

During the call, management said they have probably bottomed out in Cognac, signaling a return for growth. Furthermore, margins should slightly decline in the second half as marketing normalizes.

Fashion & Leather Goods

Created and calculated by the author using data from LVMH financial reports.

Fashion & Leather Goods continued its amazing performance, with 17% reported revenue growth (20% organic), and a steady operating margin despite highly elevated marketing, which we'll discuss further below.

Perfumes & Cosmetics

Created and calculated by the author using data from LVMH financial reports.

Perfumes & Cosmetics was strong, with 11% reported revenue growth (13% organic), and a 2.6 percentage point margin expansion.

Watches & Jewelry

Created and calculated by the author using data from LVMH financial reports.

Watches & Jewelry provided industry-leading performance, growing 11% reported revenue growth (13% organic), and a 1.0 percentage point margin expansion.

Selective Retailing

Created and calculated by the author using data from LVMH financial reports.

Selective retailing was the best performer in the first half, experiencing 26.0% revenue growth, led by Sephora and recovery in DFS. More importantly, operating profit doubled, fueled by revenue growth and a 3.3 percentage point margin expansion.

Bottom Line

Overall, I think investors including me were expecting a slightly better quarter. Namely, negative growth in the U.S. is worrisome, and Wines & Spirits declines are also disappointing.

On the flip side, there are clear reasons for those declines, which are non-recurring and don't reflect the company's long-term strength.

Important Notes From The Call

Margin in fashion & leather goods:

A slight erosion in profitability in the first half of the year, something like 80 to 90 basis points. This comes from two things. One is some reinvestment as you suggested into advertising and promotion. You must have noticed unless you’re living on another planet that we have done a few runway shows of a certain magnitude in the course of the period, for example, particularly the retail men's show in June, but there were many others during the quarter with a very good resonance, very good impact with clients. So, we are very happy with what they've done. But this comes unfortunately with a cost and this cost is reflected in our advertising and promotion expenses that rose slightly more than our sales.

The second factor which is unusual for LVMH is that if we look at the breakdown for business when we go the highest growth mainly in China and Japan is where we've seen more currency pressure. Despite some price increases to offset movements and we have not been really able to offset, and we had a little bit of pressure, something like 40-45 bps, usually it doesn’t happen because we’re able to increase prices pretty quickly, but we decided to postpone it a bit in order not to impair the momentum in those two geographies.

--- Jean-Jacques Guiony, Chief Financial Officer, H1-23 Call

Regarding the increased marketing, management discussed that the first half was an outlier in terms of spending. They definitely don't seem to regret it, but it was unusually high. So we should definitely expect increased margins in the second half and beyond, as F/X pressures ease and A&D normalizes.

We experienced an event of pressure with the American customer. We have a situation where by and large the experiential customer is suffering a bit. We are experiencing drops with entry-price products, online sales, and secondary cities, which is a clear sign that the more experiential customer is not shopping. And conversely, the rest of the portfolio is doing pretty well so fairly contrasted situation in the U.S.

--- Jean-Jacques Guiony, Chief Financial Officer, H1-23 Call

One of the "problems" with LVMH, is that, unlike Hermes (HESAY), it does have material exposure to the experiential consumer, which is a nice way of saying, the not extremely rich customer. This exposure is even more material in the U.S., so we're seeing downward pressure specifically from this cohort, as it lapses years of outright craziness, for lack of a better word.

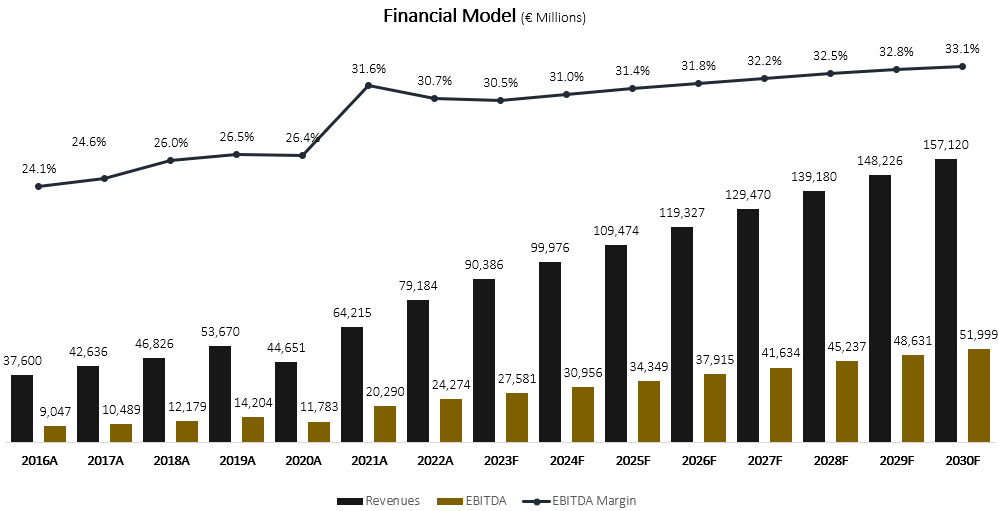

Updated Financial Model

In the April article, I provided my near-term projections for LVMH:

For H1-2023 I now expect €42.4B in sales, €13.4B in EBITDA, and €7.7B in net income. For the full year, I now expect €92.4B in sales and €33.6 EPS. Thanks to it being a European company, consensus estimates are still much lower, with expectations of €85.8B in sales and €31.9 for EPS.

As we can see, the results came below my expectations. Thus, I need to lower my full-year forecast. For the full year, I now expect €90.4B in sales and €34.5 EPS, as the company's lower revenues are more than offset by increased buybacks and higher net financial income.

For the longer term, I expect LVMH will grow revenues at an 8.2% CAGR between 2023-2030, which is higher than the consensus of approximately 7.0% growth, but below the company's past 7-year CAGR of 13.2%. I estimate revenues will grow at this pace due to constant price increases, continued store openings, new acquisitions, recovery in the lagging businesses, and steady organic growth. Additionally, I project EBITDA margins will increase incrementally up to 33.1% in 2030.

Created and calculated by the author based on data from LVMH financial reports and the author's projections.

{kind=link}

Taking a WACC of 7.6%, I estimate LVMH's fair value at €964 per share, which equals $1,063 per share of the company's ADR based on the current USD/EUR ratio. This represents a 24.8x multiple on my projected 2024 EPS estimate

Conclusion

I expect LVMH's stock to react badly to the results. We're already seeing a 4.0% decline in the company's ADR. The main reason is growth declining in the U.S. Investors were expecting a deceleration or even flat results, but negative growth is always tough to digest, especially after the amazing stock performance over the past few years.

Still, LVMH is a group that more than doubled its revenues in 6 years while improving its operating margins by almost 10 points and it's still growing at a high-teens pace. Its marketing efforts and operational investments in H1 have dragged down margins but still, they remained steady and should come in line with its all-time highs in 2022.

Therefore, I downgrade my rating to a Buy, but I want to emphasize, this should be a long-term investment at current levels, as the near-term should still be a little volatile.

For long-term investors, think about a company that brought in all-time high margins, and grew revenues by 15.0% Y/Y, nearly a 19.0% CAGR since 2019, and it disappointed investors. This, to me, reflects immense strength, and I'm comfortable buying this dip.

For further details see:

LVMH: Domination Continues In H1 2023 (Rating Downgrade)