LVMHF - LVMH: I'm Strongly Buying Into This Massive Opportunity

2023-12-02 01:26:16 ET

Summary

- LVMH is a strong buy with a 48% stake held by the Arnault family, who consistently outperform and align their interests with shareholders.

- LVMH's diversification across industries, brands, and geographies mitigates the risk of losing relevance and allows for linear growth during recessions.

- The luxury industry is expected to grow, and LVMH's high margins, growing returns on capital, and solid financial stability make it an attractive investment.

- Family-owned businesses have a proven track record of outperforming over time, as discussed in the article, which delves into the reasons behind their sustained success.

- LVMH boasts the world's strongest brands, currently available at a reasonable price.

My Thesis

Well, I'm an investor who seeks out the best businesses worldwide. I prefer to invest in companies that exemplify the highest quality attributes. Additionally, I am committed to continuous learning. Following my recent article on LVMH ( OTCPK:LVMHF ), where I rated it as a buy, I embarked on a learning adventure through books, podcasts, and research on past winners. This exploration focused on understanding the significance of leadership and the people steering the organization.

I came to the realization that I hadn't fully appreciated the 48% stake held by the Arnault family. I failed to recognize the incentives they have to consistently outperform and to align their interests with shareholders. I am now more aware of the family's attributes and the quality of Bernard Arnault. Consequently, I believe I have enhanced my valuation model. As a result, I am upgrading my rating to STRONG BUY and am actively acquiring shares.

The Business

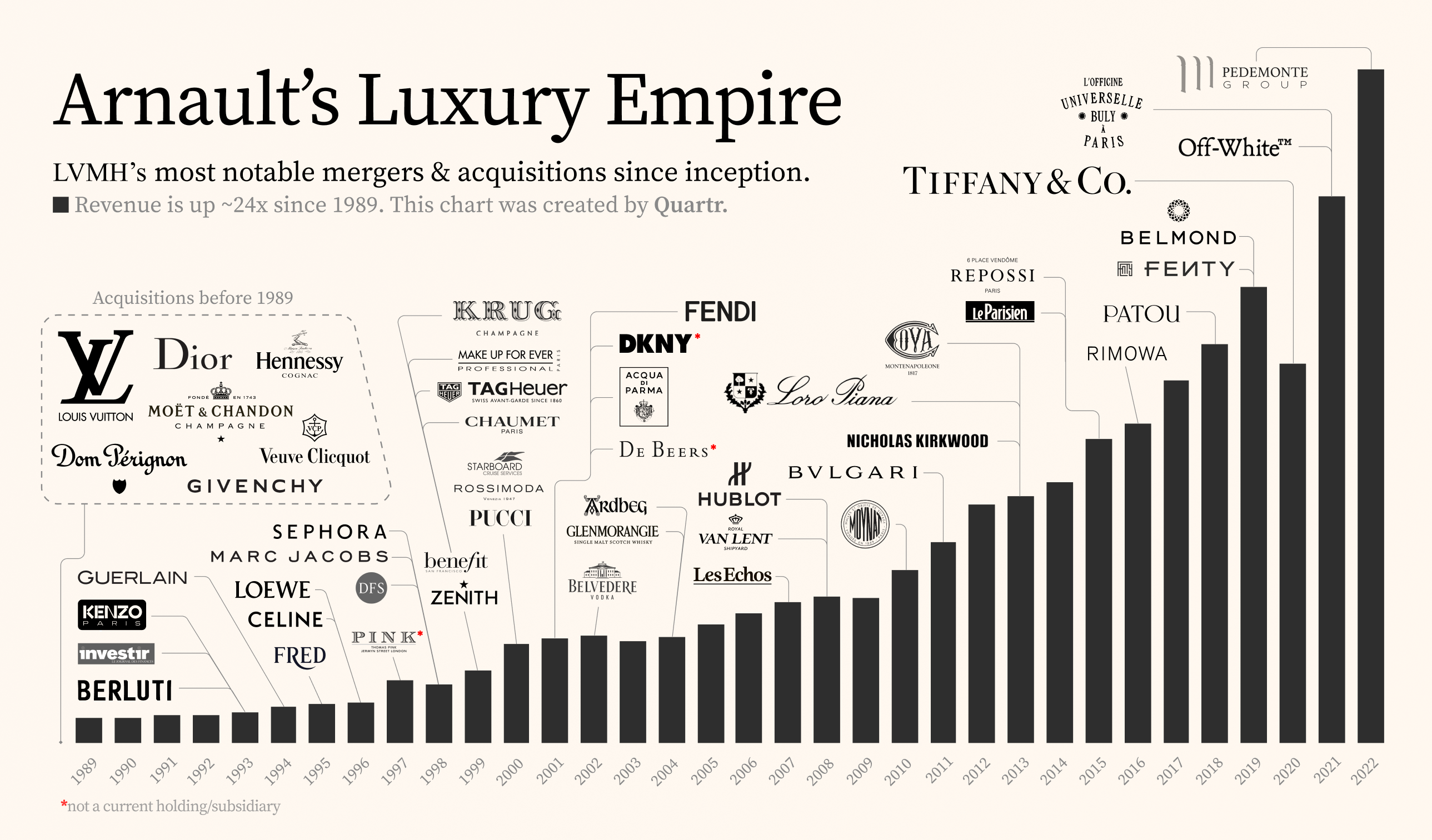

I'm sure you're familiar with most of LVMH's brands. In fact, when I reveal that all these brands fall under one umbrella, people are often astonished. Bernard Arnault's M&A ventures have propelled LVMH to own some of the best brands globally, making it the largest conglomerate of luxury brands in the world. LVMH, with its French prestige and luxury DNA, is truly the master of luxury. Its business is divided into eight market segments, with fashion and leather goods (primarily Dior and Louis Vuitton) leading with a 49% share. Selective retail (Sephora) follows with 20%, emerging as the fastest-growing segment at 26% growth in the last nine months. Watches and jewelry (Tiffany, Tag Heuer, for example) come next with 13%, and the remaining segments are depicted in the accompanying chart.

{kind=link}

M&A by LVMH (quarter)

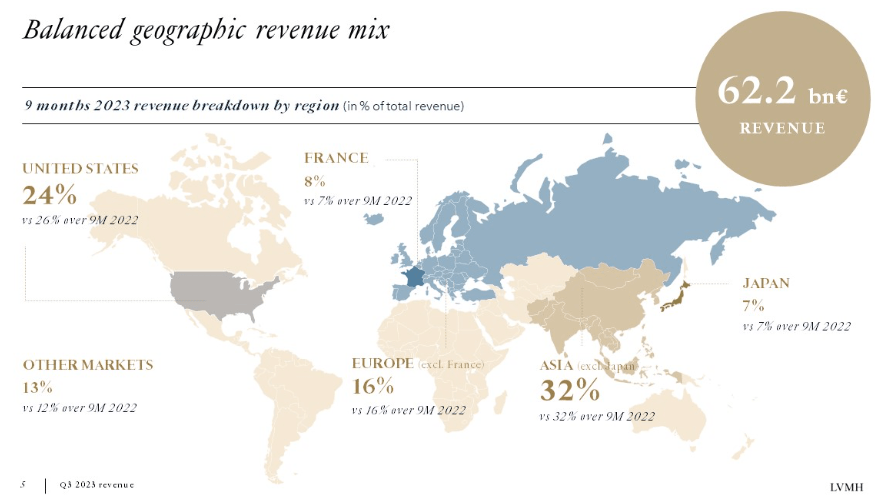

In contrast to other consumer brands, LVMH's strength lies in its diversification. While Dior and Louis Vuitton are timeless brands, there's always the risk of losing relevance, as seen in the challenging times faced by the long-lasting brand Estée Lauder ( EL ), for example. LVMH boasts significant diversification across industries, brands, and geographies (see charts). In the unlikely event that its core brands lose relevance, there are numerous backup plans to compensate. Furthermore, if there's a slowdown in one region, the impact won't be severe, given the company's revenue diversification.

{kind=link}

revenue by region (LVMH Q3 presentation)

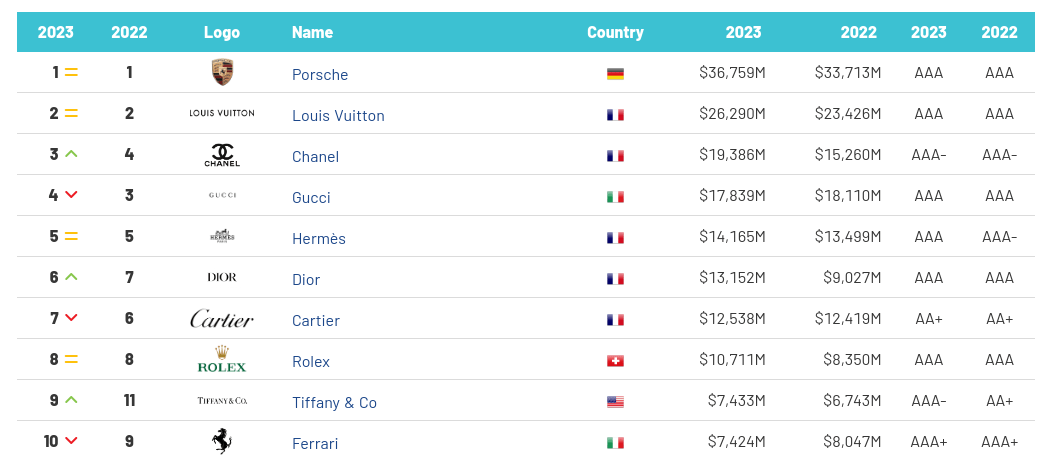

LVMH's brands dominate the luxury industry, with three out of the top 10 luxury brands by Brand Finance occupied by its brands. These brands, with a heritage spanning tens or even hundreds of years, suggest long-lasting resilience and a multi-generational customer base.

{kind=link}

3 brands in the top 10 (Brand Finance)

Another reason I favor the luxury segment is the pricing power it possesses and its resilience over time. Unlike other industries, luxury must remain special; it cannot be mass-produced, and it cannot lower prices to drive demand. Its primary mission is to maintain and enhance its luxurious profile. While LVMH's brands may not be as scarce as resources like the esteemed Hermes ( OTCPK:HESAF ), they are not ubiquitous, enhancing their pricing power. This pricing power is crucial, as LVMH's brands are nearly inflation-proof. For instance, a typical luxury shopper need not worry about a 5% inflation when purchasing a $1000 purse (although, sadly, this is not always the case). In the face of 5% wage inflation, LVMH can easily raise prices, which is less damaging than lowering them—again, the main mission is to preserve the brand's luxury.

Because the typical luxury shopper is less affected by economic downturns, we can anticipate linear growth or a less cyclical nature during recessions. This linearity is evident in LVMH's revenue history and is also apparent in the potential downturn in 2022-2023, where LVMH continues to grow, with a substantial 14% organic growth in the last nine months year over year.

Industry

LVMH operates in the luxury industry, which is expected to grow annually by 3.38% (CAGR 2023-2028), and the luxury fashion market is projected to experience annual growth of 3.39% (CAGR 2023-2028). Despite the exceptional growth witnessed in the last three years, it deviated from the typical trajectory. LVMH managed to achieve remarkable market share growth, nearly doubling its global market share from 12% to 22% between 2018 and 2023, according to Jefferies . However, we should not base our valuation solely on this kind of growth.

The recent downturn in the luxury industry is what, I believe, has presented us with this rare opportunity. Over the long run, we should anticipate high single-digit earnings growth. I believe that through acquisitions, LVMH will continue to gain more market share and also achieve modest margin growth.

Family Business and Management

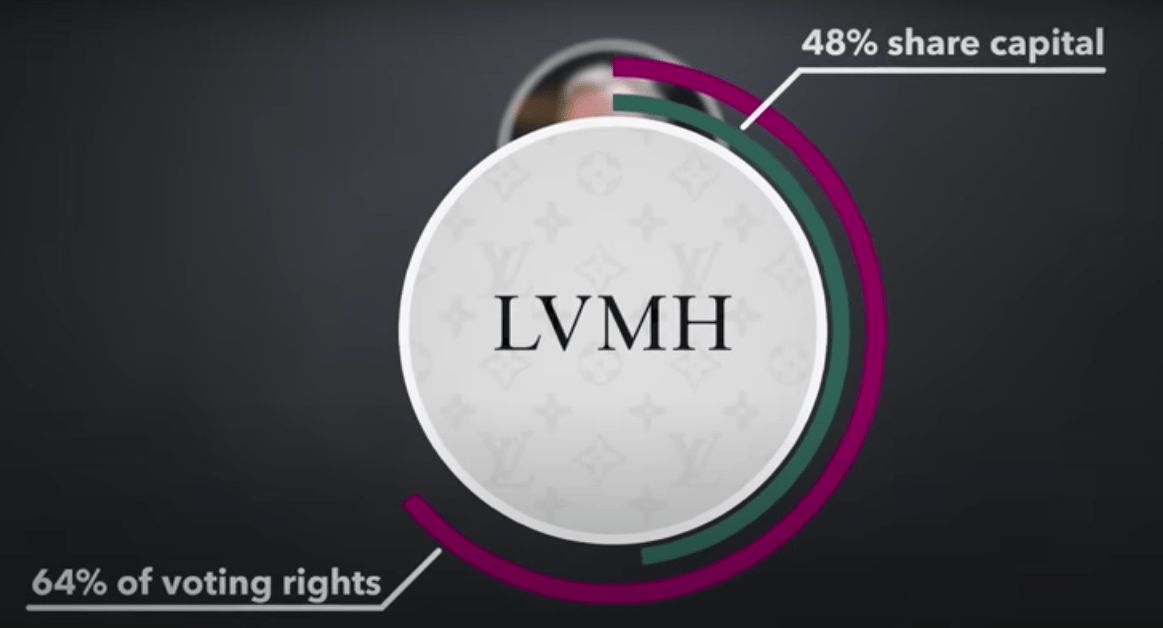

The main reason I've decided to upgrade my rating on LVMH is that I've gained a stronger understanding of the attributes of the family owners. The Arnault family owns 48% of LVMH and continues to consistently buy more shares. Additionally, the family holds over 60% of the voting rights. All five of Bernard Arnault's children play key roles in the company. They have a significant portion of their family's substantial fortune invested in LVMH, and I believe they are dedicated to nurturing its success. Take, for example, other French luxury brands like Hermes, which is a 6th-generation family business with family control, their results are impressive.

{kind=link}

Arnault family ownership (Bloomberg)

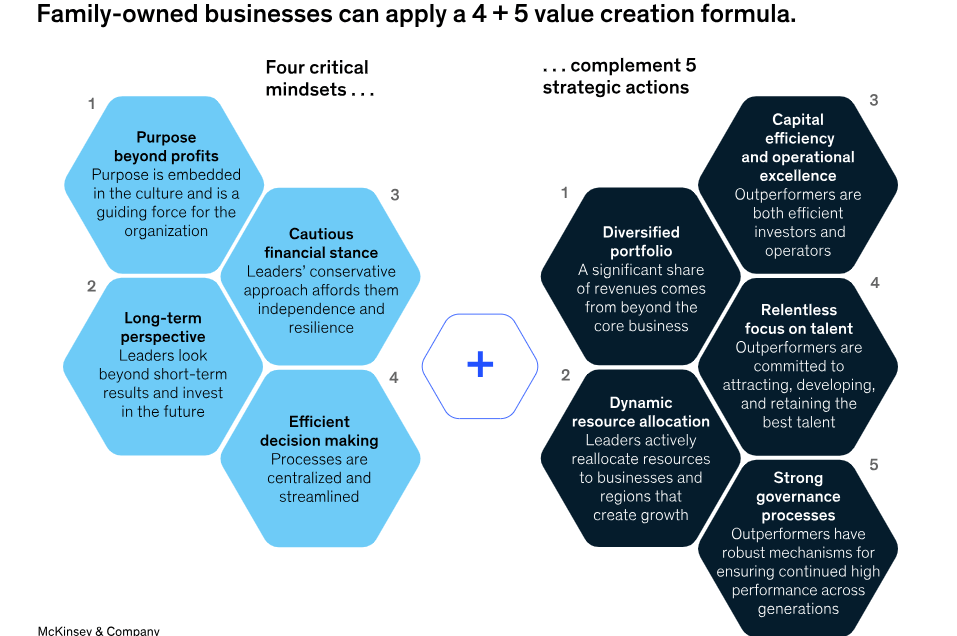

The reasons for the outperformance of family-owned businesses are well described in the following quote from McKinsey :

The critical mindsets are a focus on purpose beyond profits, a long-term view and emphasis on reinvesting in the business, a conservative and cautious stance on finances, and processes that allow for efficient decision making.

{kind=link}

Why FOB's outperform (McKinsey)

Moreover, despite recent media discussions about Bernard Arnault's successor, he continues to hold his position as one of the best and most formidable businessmen in the world, demonstrating a genuine concern for the business. For Arnault, compensation may not be of utmost importance, but rather a matter of protocol. The variable remuneration for the year 2023 is structured based on a 60% achievement of quantifiable objectives and a 40% achievement of qualitative objectives. The criteria for quantifiable objectives include revenue, operating profit, and cash flow, with each accounting for one-third.

This Is Also The Main Risk

Well, Bernard Arnault is a shark; he built this business from scratch, mastered acquisitions, and knew how to be ruthless when the situation demanded, as seen in the Tiffany saga. At 74, he joins the ranks of CEOs well over 70, with Warren Buffett being the most extreme example, of course. However, we cannot be certain about how much longer he will remain in his role. There has been significant media speculation about who will succeed him. I believe it poses a risk, but, in my view, LVMH is a business that can succeed even if run by someone less skilled. I'm confident that Arnault will choose his successor wisely, and if so, I believe he will stay on the board to provide guidance, especially since most of his family's net worth is in LVMH.

Other than that, there are risks associated with the economic slowdown, which, despite being less harmful to the luxury industry, still has an impact, as noted by Chiara Battistini, Head of European Luxury and Sporting Goods at J.P. Morgan:

While the luxury sector is more resilient, we also note that it has never been immune to macro dynamics and has historically been late cyclical.

There is a risk of losing relevance in the Dior and Louis Vuitton brands, considering their substantial contribution to LVMH's revenue. Another risk arises from Sephora, which, while currently successful, faces competition from strong players like Ulta Beauty ( ULTA ).

Valuation is always a risk, but we will delve into that later.

The Important Numbers

While LVMH's growth has been impressive in the last couple of years, it's crucial to look ahead and anticipate future growth. As mentioned earlier, the market is forecasted to grow at a low single-digit rate, driven by factors such as the rise of the middle class, population growth, and the economic development of emerging countries. LVMH is expected to exhibit higher top-line growth through acquisitions and the organic growth of its own brands, like Sephora, for example. Analysts project a top-line CAGR of about 7% for the next few years. In the last decade, LVMH has consistently surpassed top-line estimates for most years, suggesting that this CAGR might be slightly higher, although not significantly. We can also anticipate a slightly higher Free Cash Flow per share figure, given the observed operating leverage in FCF growth. Since there is no consistent buyback program in place, we should not expect FCF per share growth to surpass revenue growth by a considerable margin.

LVMH also boasts high and growing margins, a testament to its pricing power, as it maintains stable pricing even amidst economic disorder. It's challenging to compare with other luxury players like Hermes, for example, given that 20% of LVMH's revenue comes from retail, which naturally carries lower margins. Nonetheless, the 68% gross margin showcases the luxury power, and the 26% EBIT margin represents the next most crucial figure, in my view, alongside top-line growth—returns on capital (ROCs). LVMH's ROCs are on an upward trajectory, a vital factor, as a recent study by Morgan Stanley revealed that a high and growing spread between a company's Weighted Average Cost of Capital and its Return on Invested Capital is a common trait among successful companies. These ratios become even more impressive when considering the diverse range of businesses within LVMH, suggesting that most of them likely yield high returns.

LVMH pays a modest dividend yielding 1.7%, exhibiting solid growth over the last 10 years with a 13% CAGR and a 22% in the last 5 years. In my perspective, as long as Bernard Arnault remains at the helm, much like Buffett, no dividend is necessary. I would prefer that he use this cash to fund quality acquisitions.

Solvency

LVMH is notably solvent, demonstrating the capability to settle its net debt within one year of free cash flow, particularly when factoring in the average free cash flow margin over the past five years. With the ability to cover its interest 34 times, a very low debt-to-equity ratio, and an Altman Z score exceeding 3, coupled with a current ratio above 1, LVMH showcases robust financial stability.

Valuation

Let's assess the value of this luxury monster. Considering the average free cash flow margin over the past five years, The FCF yield stands at 3.7%, which, in my opinion, isn't a bargain but appears quite reasonable given its quality. Additionally, when valuing it based on the price-to-earnings (P/E) ratio, it is trading above the averages, indicating potential for multiple expansion.

However, it's crucial to acknowledge that these averages were influenced by the zero interest rate policy (ZIRP) era. As a result, we shouldn't be surprised if the P/E ratio doesn't climb back to the 30 P/E area.

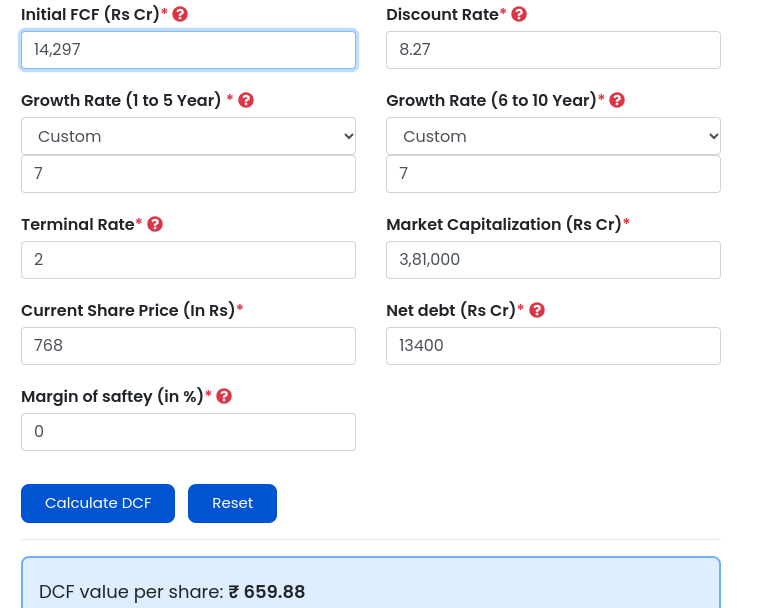

Now, let's delve into the discounted cash flow analysis. I believe my inputs are more accurate this time. I will be utilizing the average free cash flow margin over the last five years, standing at 15.2%, alongside an estimated revenue for 2023. The terminal rate is set at 2%, and given that LVMH operates globally, the terminal growth could be higher.

My discount rate, based on the WACC calculation, is set at 8.27%. The variable distinguishing each case will be the growth rate.

WACC (author calculation)

In the first scenario, I assume no margin expansion, aligning the growth rate with the forecasted revenue growth of about 7%. In this case, the stock is deemed overvalued by 16%.

{kind=link}

DCF (finology)

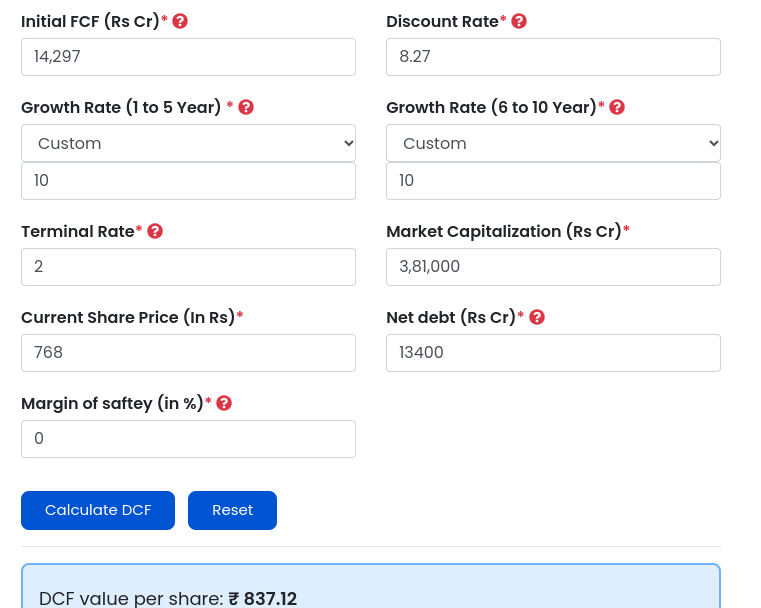

Conversely, in the second scenario, I opt for a 10% growth rate, mirroring the estimated EBIT growth for the next three years. Remarkably, in this case, the stock is undervalued by 8%. For me, this represents a reasonable price to own one of the best businesses on the planet. It's crucial to note that opportunities to invest in high Return on Capital Employed companies with such a wide moat at a reasonable price are rare. In most instances, such businesses are considered too expensive to own. Therefore, when such opportunities arise, seizing them and holding for the long term is, in my view, essential.

{kind=link}

DCF (finology)

In both scenarios, the projected future growth is slower than the past three years, which aligns with the exceptional performance LVMH experienced during that period.

Conclusions

LVMH stands out as one of the most diversified and dominant companies globally. I perceive minimal meaningful risks that could significantly impact its business compared to its competitors. The company boasts an exceptional management team deeply invested in its success, striking the right balance between growth, Return on Capital, and robust solvency.

While it may not be considered a bargain in the sense of being 40% under fair value, such a situation is likely rare and contingent on unforeseen negative events. In my perspective, a reasonable price for a company of this caliber is sufficient. Therefore, I categorize it as a STRONG BUY.

What are your thoughts on this conglomerate?

For further details see:

LVMH: I'm Strongly Buying Into This Massive Opportunity