LVMUY - LVMH Is Dropping In Price - And I Am Buying In 2024

2024-01-15 20:14:17 ET

Summary

- LVMH has been outperforming other investments due to its low-cost basis, but its overall performance for 2023 is not as strong as expected.

- The company's upside potential is double digits with an AA-credit rating, making it an attractive investment.

- LVMH's top-line revenues have grown by 14% YoY, with strong performance in its leather goods and fashion segment.

Dear readers/followers,

Do you recall my investing in LMVH ( OTCPK:LVMUY )? This investment, because of my low overall cost basis, has been significantly outperforming many of my other investments. It hasn't reversed as much as I expected it to. In fact, it has underperformed many larger indices and stocks, alongside many other French stocks that I've invested in. Over the past 2 years, I've increased my exposure to French luxury and French stocks, as well as European stocks in a big way.

This is part of the reason why my outperformance for 2023 isn't as big as it could have been. That, and things like investing in Intrum and other stocks which are at a considerable weak point at this time. So, I have good expectations for the next few years when these companies, as I believe them to be likely to, start to turn around.

And few companies are as storied, as qualitative, or as interesting as LVMH. In an environment like this, we need to be careful about every premium we accept for a company.

Let's look at what we have here in terms of upside and thesis.

LVMH - The upside is double digits with an AA-credit

There are very few companies as good as LMVH, which by the way stands for Moet Hennessy Louis Vuitton SE. This was one of the very first companies I covered for iREIT® on Alpha. It's also one of the companies that I maintain one of my largest exposures, with one of the lowest yields out there.

I bought a significant stake at below €550/share in the native MC ticker both privately and for my commercial account.

The key, in my mind, to buying this company, is to decide on a long-term accepted premium , find an acceptable RoR based on the company's long-term conservative growth rate annually , and then invest when the company hits that.

For me, the company hits that 15% annualized upside when it goes below €700. The farther below €700 it goes, the more of the company I "BUY". In this article, we'll look at the latest set of results, see where we might go from here, and see how much more we could (or should) buy.

Remember, the company works and owns, among other things, the following brands.

-

Christian Dior

-

Louis Vuitton

-

Fendi

-

Marc Jacobs

-

Kenzo

-

TAG Heuer

-

Bulgari

-

Dom Perignon

-

Zenith

-

Sephora

These are called "maisons" by the way, if you want to be nitpicky. Fundamentals for this company are beyond rock-solid. This is something we can confirm in the last set of quarterly results. Those are 9M23.

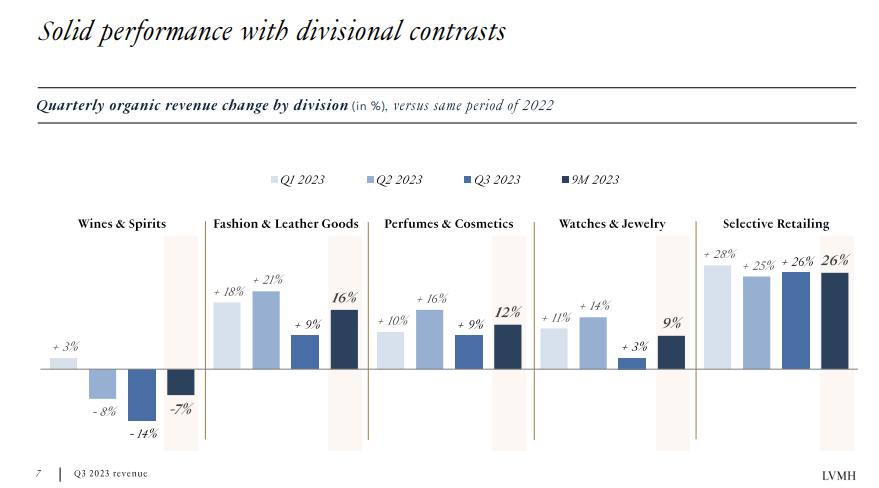

LVMH managed to not only grow, it grew top-line revenues by 14% YoY in what I would consider a very difficult environment. The company saw not only good growth in its leather goods but also in jewelry. The only part of the company, in fact, that saw any sort of significant downturn was the spirits segment.

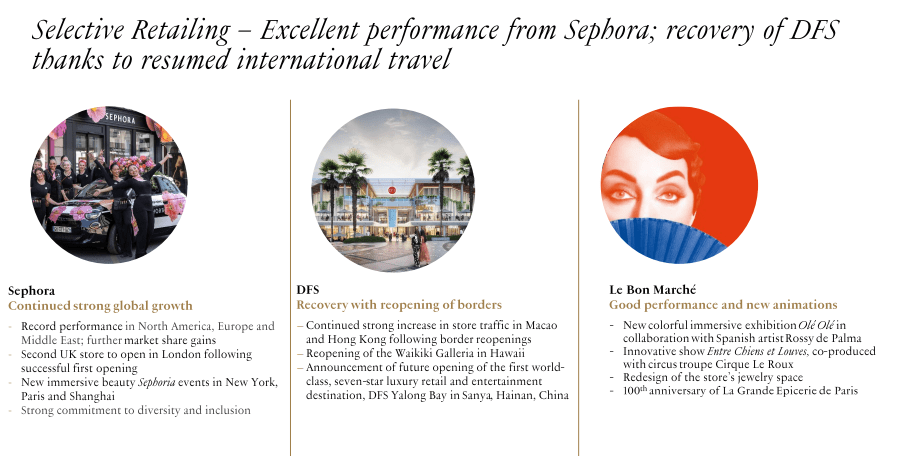

The company's leather goods and fashion segment was the star of the show here - that and Sephora, which saw absolutely exceptional performance.

Overall, if you invest in LVMH, you should at the very least understand the luxury sector. It's not an easy sector to invest in due to the premiums. But if you follow my targets and my considerations, I believe you have a good shot of coming out with a profit.

The company continues to be relatively Asia-heavy. Out of the company's 9M €62.2B worth of revenues, which grew at double digits, the company made 32% of Asia. If we include Japan in this, it's at almost 40%. Europe and France together is another 26%, and the US is 24%. The remaining markets are at around 13%. Top-line grew in Europe, Japan, and the Rest of Asia by over 10% each, with continued "okay" growth in the US segment, though somewhat hampered.

If you look at the company's sector-specific performance you can see the company's strengths and weaknesses, if they can be called such.

{kind=link}

LVMH IR (LVMH IR)

Yes, spirits are a weakness here, but the implication that I see is that it's momentary. The company's champagne subsegment is doing better, and Henessy is rebounding in Asia. Most of the problem is not in wines, but in cognac and spirits, declining around 14%, due to the US economy and the post-covid environment.

Meanwhile, any segment having to do with fashion or leather goods is doing with, superb performance out of Dior, Celine, Louis Vuitton, Loro Piana and Loewe. Perfume and cosmetics is up 12% here as well, with superb momentum. LVMH continues to elevate Tiffany's as well in the Jewelry segment, with good results from Bulgari as well. The brands that I don't like that LVMH has, specifically watch brands such as TAG, Hublot, and Zenith are doing so-so, not great. I've been clear that I believe the company should focus on its strengths - and being a timekeeper/watch business is not one of those things, because there are far better brands out there. When someone wants your typical luxury watch, they go for a Rolex or a Patek, just as your leather luxury consumer goes for LV. But these brands are, at least for the time being, part of the company, so I'll continue to follow them, even if I don't necessarily own any products from them - unlike other LVMH subsectors where I own company products.

Going forward, I continue to expect LVMH to grow at double digits. This is a rough company to evaluate properly, as evidenced by some analyst targets and fair values I will share with you at a later point in time. I managed to score my shares at a price that even Morningstar's conservative estimate considered to be fair value or undervalued, but what differs me from other analysts when it comes to LVMH is that I believe the company is worth more of a premium. Continued above-average growth is likely to come from things like growth in core from market expansion in new markets (non-Asia/EU), and growth in selective retailing - which we can already see at Sephora.

{kind=link}

LVMH IR (LVMH IR)

I expect the company to continue to perform well based also on graduate travel rebound, with China leading another recovery trend as well going into 2024.

Here are the risks and upsides I see to this company specifically at this time.

Risks and Upside for LVMH

The main investment risk for LVMH aside from the obvious valuation-related risk is the continued expansion of LVMH's brand portfolio. Any brand expansion that LVMH does, is likely to be done at a significant purchase premium , which ties up a lot of capital in goodwill and intangibles. These balance sheet items impact the company's capital returns. Also, if you look at the entirety of the company from a brand perspective, many of the smaller brands don't have as great margins as some of the more legacy brands. Finding the high-margin plays in this sector, even for LVMH, is not easy . And any sort of synergistic potential in these segments or subsectors is extremely limited. You can't make efficient a play between fashion and wine, or jewelry and leather goods. The businesses are too different.

So LVMH does need to balance things carefully to outperform - so far this has gone well.

And on the upside, let's not underestimate this company. LVMH completely controls its manufacturing and distribution network. This enables the company to in essence more than others control its margins, with operating margins in the 40% range, which is almost unheard of in any of these sectors. This retains the possibility of perception of value.

The historical growth trends for many of these brands, such as LV and some of the spirit and wine brands, are beyond good, with double-digit growth for decades in some cases.

Let's look at the valuation.

LVMH valuation - The upside is now 15% annually again.

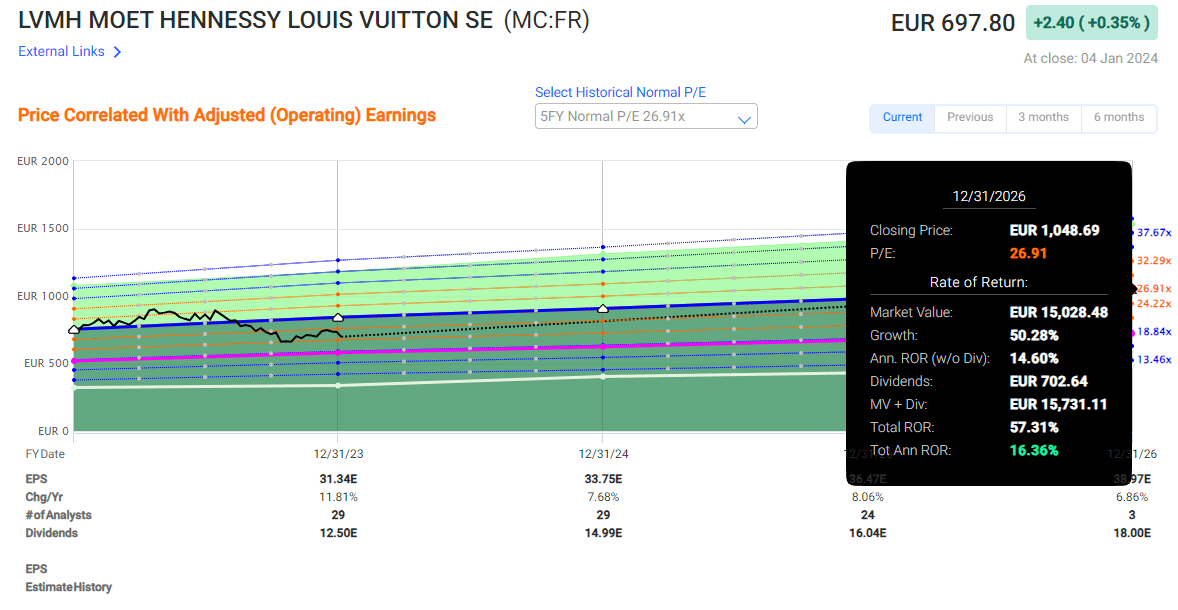

So, we have the company currently trading at around 23-25x P/E. That's as low as the company has been for some time, and it's an attractive price, as I see it. The company sees a 27x P/E average premium, which based on a 6-8% EPS growth rate gives us an upside of 16.3% annually for this company.

Before you say that this looks too low, remember that this business has a long-term debt of less than 26% to capital, and a credit rating of AA-, one of the very few companies anywhere to manage this. Even at a 1.8% yield, which is all you get at this time, it's still a great deal here, and likely to beat the long-term market returns.

LVMH has a good track record. It beats estimates over 30% of the time, and hits them over 40% of the time, giving them an over 74% positive historical likelihood of these estimates hitting. I also want to make it clear that the current native share price as I am writing this is closer to €680, making the current upside closer to 16.6% per year.

{kind=link}

LVMH Upside (F.A.S.T graphs)

That's more than good enough for me to declare the company a "BUY" here again.

An easy rule of thumb for LVMH here is that if the company is at below €690/share, you should be paying more and more attention to it. If the price drops below €600/share, this company becomes an absolute, no-nonsense-"BUY" sort of company for the long term, or until the share price goes to quadruple digits.

LVMH won't make you rich. But if you start out with good money, and you want safety , LVMH can make you richer without requiring you to take any sort of massive risk.

Anyone telling me that the company is a significant or a massive risk, please let me know what risks you see here, what you believe the likely price target is, and the justification for it.

Remember, the last time this company was at any valuation that can be called "cheap", was almost a decade ago and more.

At this point, I would consider this company a top-tier investment, and I would "BUY" it to a 3% allocation - which also happens to be my portfolio target for this company.

Here is my current thesis for the company.

Thesis

-

LVMH is the best luxury investment potential on earth, at the right price. The company's mix of segments, maisons, ownership, and growth potential is unrivaled across its peers, and I view it with great confidence, which is why it's my largest luxury position, even though I don't much invest in consumer discretionary otherwise.

-

The company has been on a good ride, returning market-beating returns in 2022-2023 if bought at overall appealing prices, and also bumped the dividend. I expect more good results and more dividend bumps coming in the next few years.

-

My PT is at €750 per share, with anything very attractive below €700, I still consider LVMH a "BUY" until it goes clearly above here, with a conservative RoR potential of 15%+ annually until 2025E.

Remember, I'm all about:

-

Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

-

This company is overall qualitative.

-

This company is fundamentally safe/conservative & well-run.

-

This company pays a well-covered dividend.

-

This company is currently cheap.

-

This company has a realistic upside that is high enough, based on earnings growth or multiple expansions/reversion.

The only issue is that LVMH is not cheap - other than that, it's a rock-solid investment here.

For further details see:

LVMH Is Dropping In Price - And I Am Buying In 2024