LVMHF - LVMH: Limited Upside For Now

2023-08-29 11:13:59 ET

Summary

- LVMH's recent price decline has made its market multiples a bit more attractive than they were even a couple of months ago.

- The company's robust H1 2023 performance encourages optimism on its full-year numbers. But with an uncertain outlook for its key markets, there are risks to the downside.

- On balance, there appears to be a limited upside to it right now, but that can change if it continues to perform or its P/E drops to historical lows.

After a bullish thesis on luxury fashion’s leading company LVMH (LVMUY) starting in October last year, I turned cautious by mid of this year, prompting a Hold rating. The caution was for two reasons. First, its price had already run up significantly since late 2022 and second, there were signs of slowing demand from the US market.

Since then, LVMH is down by 10%, resulting in slightly more attractive market multiples. But do they look good enough to make the stock a Buy again? Or is there a further downside? Let’s figure out.

Latest developments

First, a quick look at the developments since I last wrote. The company released its results for the first half of the year (H1 2023), which have more to like than I had expected. Here are the key points:

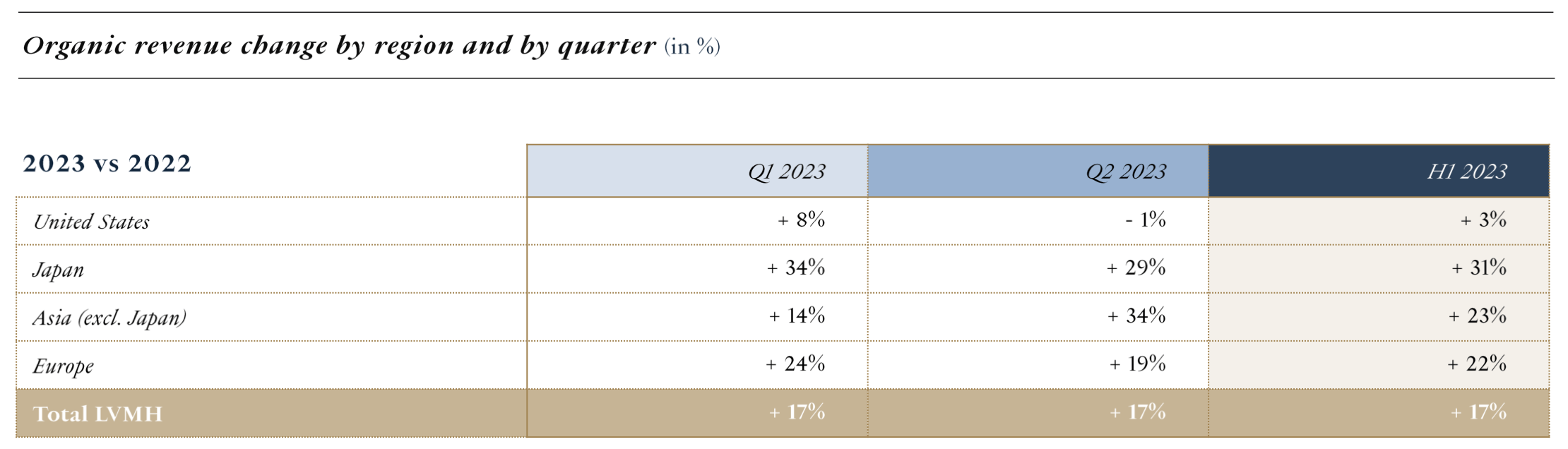

- LVMH sustained its organic revenue growth rate at 17% in H1 2023, the same as in the first quarter, on a growth jump in its Asia ex-Japan second quarter (Q2 2023) revenues to 34%. The market made up not just for the drag from the US market but also a correction in other significant markets like Europe and Japan (see table below).

- The gross margin rose to 69.4% (H1 2022: 68.9%), as the cost of revenues grew at a slower pace. The operating margin slightly declined to 27.4% (H1 2022: 27.6%) though.

- But the real surprise is the net profit margin which rose to 20.1% (H1 2022: 17.8%), helped by a positive net financial income compared to a loss on this account last in H1 2022. When I last checked I was doubtful if it would be able to surpass last year’s high margin, especially since sales were expected to slide. But the trends so far indicate that it might be able to pull off exactly that.

{kind=link}

It looks more attractive now…

With an improved net margin combined with its recent price decline, the question is whether its price-to-earnings (P/E) ratio looks improved. Let's start with the forward P/E. For this, I made two sets of quick estimates based on the following assumptions:

- The net margin stays constant at 20.1% through 2023, in continuation of the trend we saw in 2022 for both calculations.

- The first estimate assumes that revenue growth also remains constant at the reported level of 15% seen in H1 2023.

- The second estimate factors in a bigger revenue slowdown in 2023, because of a continued softening in the company’s key markets, especially as China’s demand can no longer be depended on as a definite growth source. It assumes that second-half revenue growth slows down to 7.5%, which This translates into a full-year 2023 growth of 11%.

The first estimate with unchanged revenue growth results in a forward P/E of 21.4x. And the second estimate yields a forward P/E ratio of 22.2x. Both these numbers are lower than my earlier estimate of 26.9x, which is an improvement. They are also an improvement over the past five years’ average forward P/E of 26x, indicating a 15-20% upside for the stock. But this is only one set of estimates at an uncertain time, which expects the high net income margin to continue.

…but not enough

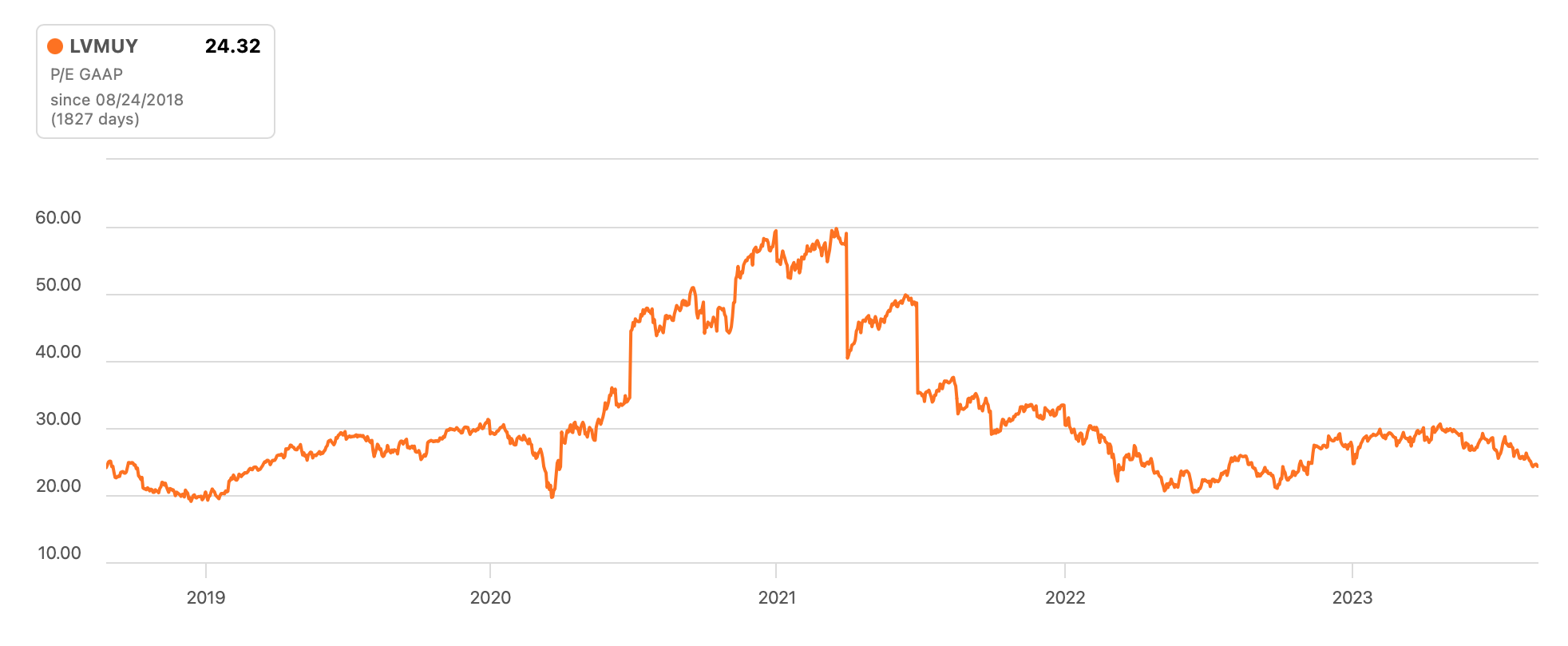

To get a more holistic picture, I also considered its trailing twelve months [TTM] P/E and compare them to its peers' performance. The stock’s GAAP, TTM P/E has declined to 24.3x from 30.3x it was at the last time I checked. As positive as this is, the stock is still just a shade lower than its 10-year average of 24.56x , indicating that the stock is fairly priced.

It doesn’t mean that LVMH will not fall further, though. In the past five years, the lowest this ratio has fallen is slightly below 20x during the start of the pandemic, in March 2020 (see chart below). Considering the present situation is unlikely to get as dramatic as that, the P/E is unlikely to go back there. But worst case scenario, if it does, then the price can fall by another 16%.

{kind=link}

Comparing to peers

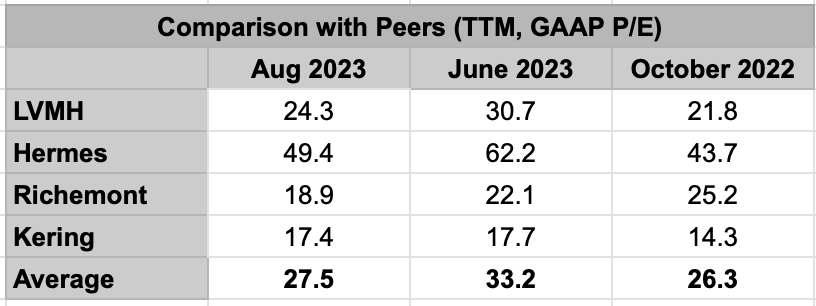

As has been the trend in the past, LVMH is trading at a lower TTM P/E compared to the average for the luxury sector. This, however, is essentially on account of Hermès (HESAY) being a standout stock that routinely has a much higher P/E than the rest. LVMH, in fact, trades at higher multiples than both Richemont (CFRUY) and Kering (PPRUY) (see table below).

{kind=link}

I see why it’s at a premium to Kering, going by its recent performance and management changes underway. But the continued premium to Richemont is harder to understand, going by the Swiss jewellery and watch manufacturer's solid financials and continued growth .

It can be said that LVMH has a longer history of good operating margins, while those for Richemont improved relatively recently after it sold off its stake in the e-commerce platform YNAP, so some premium is justified. Further, LVMH is also bigger and more diversified. At the same time, it’s worth noting that Richemont was trading at richer multiples than LVMH even last October. This implies that it’s not guaranteed that its P/E will stay north of that for Richemont.

But more generally, the peer comparison doesn’t make a clear case for upgrading LVMH to a Buy.

What next?

The clear indicators for where LVMH could head next are provided by its own forward and past multiples. Both the optimistic and realistic scenarios with regard to forward P/E indicate a substantial upside of 15-20%.

However, the TTM P/E indicates that the stock is fairly priced right now, and the worst-case scenario actually shows a 16% downside. Averaging all four of these outcomes yields an underwhelming price uptick possibility of under 6%. This isn’t any reason to change the rating on the stock for right now.

However, I’d keep a lookout for its third-quarter trading update due in October. If it shows robust growth yet again while its price continues to decline, it could call for a rating upgrade. I’d also watch its GAAP TTM P/E. If it falls below the historical floor of 20x, that would make LVMH attractive too. But for now, I’m retaining a Hold rating on it.

For further details see:

LVMH: Limited Upside For Now