PPRUF - LVMH: Limited Upside If Growth Slows

2023-06-16 14:17:23 ET

Summary

- LVMH's price increased by 70% between September last year and April this year, but its trailing twelve months GAAP price-to-earnings ratio is now over 30x, higher than its historical average.

- The company's forward P/E is 23.6x, which is more reasonable but still higher than the historical median P/E, and its net income margin may not improve this year.

- A comparison with peers indicates some upside, but the extent is not convincing enough to make LVMH an outright buy; I recommend waiting for the first half results due in July.

From its lows in September last year to April this year, the luxury giant LVMH ( LVMUY ) saw a massive 70% increase in price. When I gave it a Buy rating in October last year, the company’s fundamentals were so strong compared to its market multiples, I thought it was self-evident that it was only a matter of time before the price started rising.

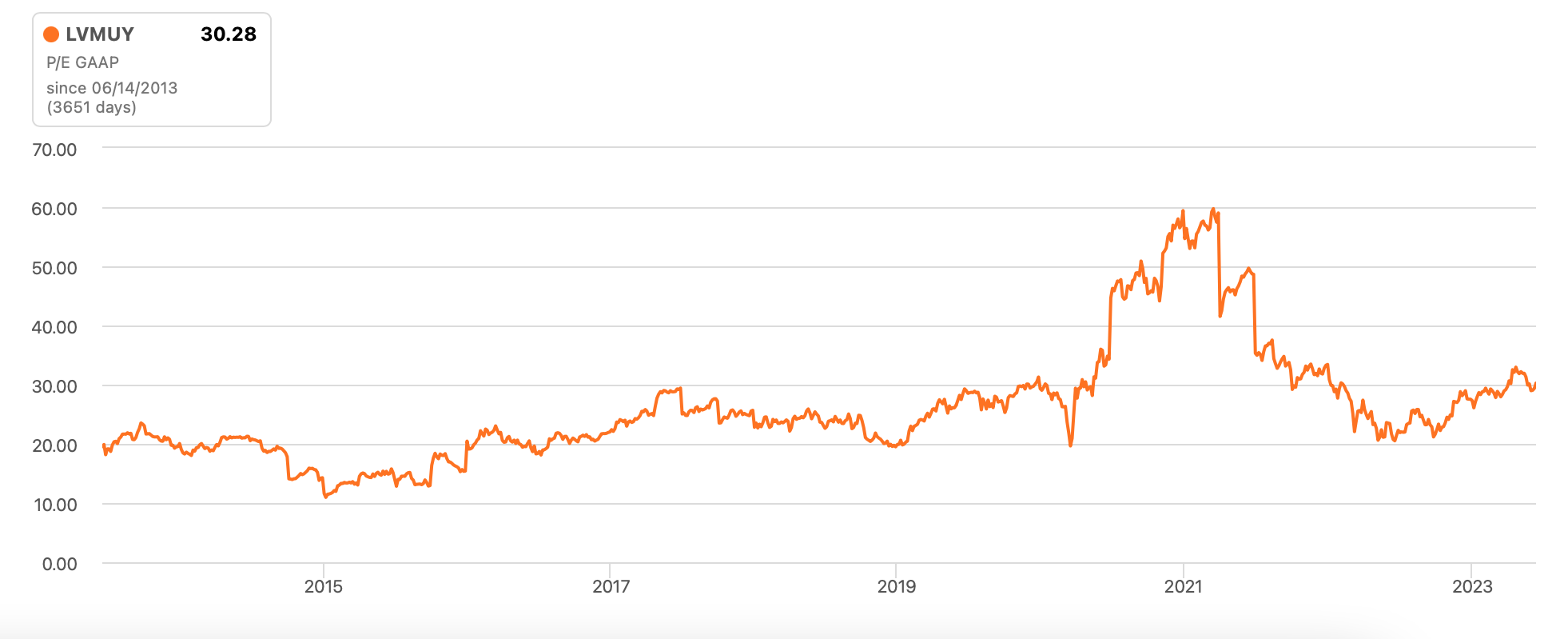

It has of course come a long way since. Even though its price has corrected by some 7% since the April highs, it’s still up by 55% since my article on it. As a result though, its trailing twelve months [TTM] GAAP price-to-earnings (P/E) ratio is at over 30x, which is higher than its historical average. This raises the question of whether there is more upside to LVMUY now.

Historical P/E (Source: Seeking Alpha)

{kind=link}

The answer to this question can be ascertained in two ways. The first is by analyzing its forward P/E in the context of its fundamentals. And the second is to measure its valuations against those of its peers.

The forward P/E

LVMUY’s forward P/E trades at 23.6x, which look more reasonable than the TTM P/E. It is also a shade lower than the historical median P/E of 24.5x . Underpinning this valuation, of course, are analyst estimates for 2023. Unlike revenue estimates, however, since we have only a single analyst’s estimates for earning per ADR available, I made a quick earnings estimate based on the revenue forecasts available and the net income margin for 2022 of 17.8%.

This yields a 26.9x forward P/E, which is not quite as low as the analyst’s estimate. Even going with the average of these two forward P/E estimates yields 25.2x, also higher than the historical average.

Can net income margin improve?

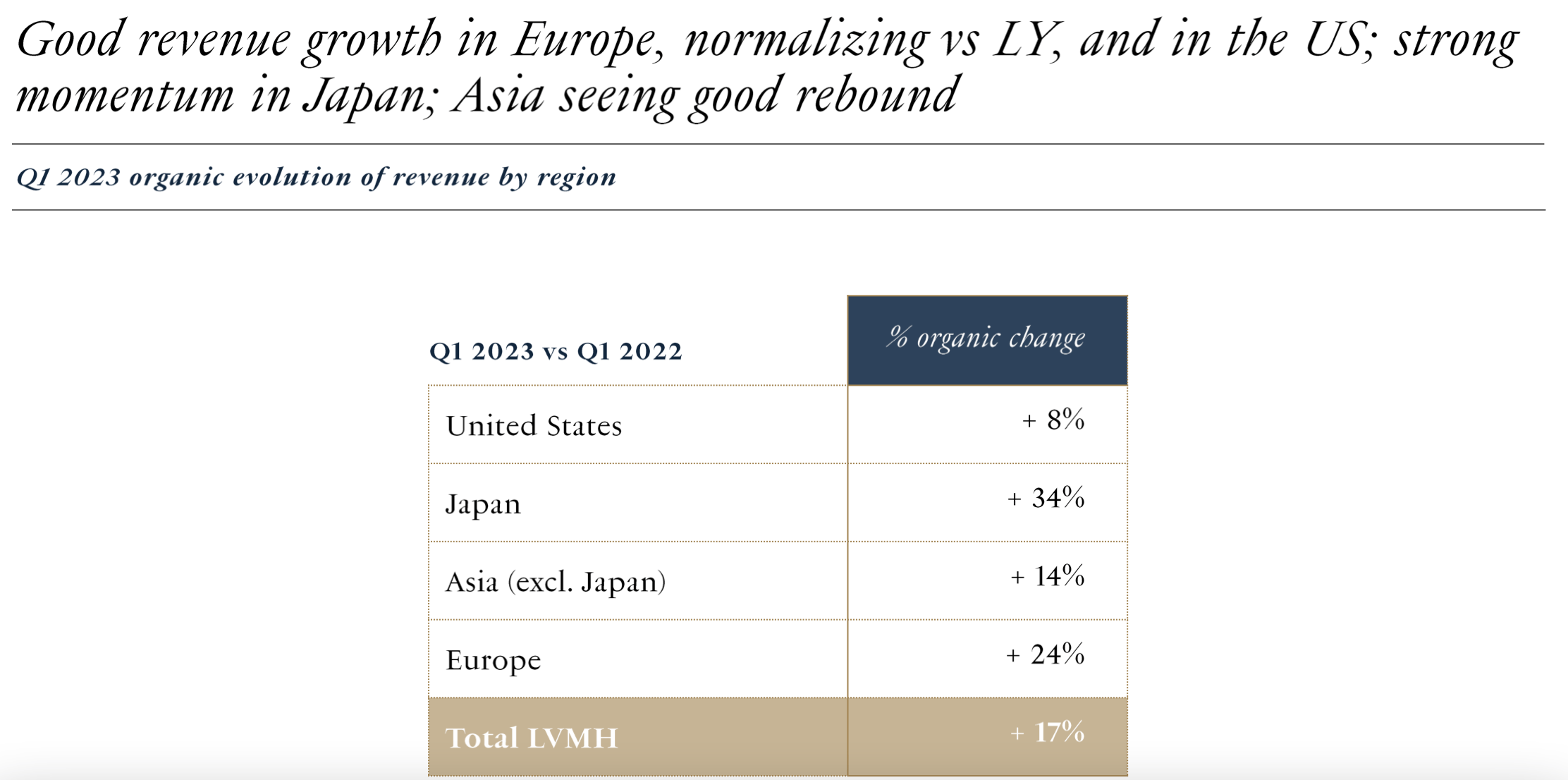

However, if the net income margin were to improve, we could have a case for lower forward multiple. This can happen if either revenue grows faster or costs decline significantly. On the revenue growth front, there is no doubt that LVMH continues to race ahead with a reported 17% year-on-year (YoY) rise in the first quarter of 2023 (Q1 2023) as per its latest trading update .

It has, however, slowed down from 23% in 2022. It can be argued that sales growth last year was strong on pent-up demand from the pandemic. But then the Asia ex-Japan market also suffered because of China’s COVID-19 lockdowns, resulting in zero organic growth from the region, even as all the others showed double digit growth.

Growth is back in the region this year, but the pull back is visible for its US market (see chart below), which has slowed down to single digit growth. And further slowing down could happen if a recession actually happens in the economy. This is also reflected in revenue forecasts that pencil in a far slower 13.7% YoY growth this year, indicating that LVMH could see softer growth in the quarters ahead.

{kind=link}

On the cost front, the cost of revenues did start showing a slight decline as a proportion of sales to 31.6% in 2022 from 31.5% in 2021. The same was not true for operating expenses though, which rose to 41.9% in 2022 from 41.6% in 2021, as a percentage of revenues. I am still hopeful on this front, though, with inflation already coming off in its key markets, and likely to decline further over the course of the year.

But with slowing growth, whether the proportions can decline remains to be seen. The net margin was already elevated by historical standards in 2022, with a higher margin seen only during 2021 in the last decade. To me, this does not look like a year when LVMH can beat that. This really boils down the forward P/E staying around the current levels or even rising, which in turn makes little case for further rise in LVMH’s price.

Comparison with peers

A comparison with peers is more encouraging. I looked at LVMH against three big luxury companies, the Birkin producer Hermès ( HESAY ), Cartier owner Richemont ( CFRUY ) and Kering ( PPRUY ) of Gucci and YSL. The TTM GAAP P/E on average for all four companies has risen to 33.2x from 26.2x in October last year. In other words, investors value luxury stocks even more now than they did earlier. This is not surprising given their sustaining power in uncertain economic times in the key western markets and their potential as China, the second biggest luxury market in the world, becomes buoyant again.

There is a crucial difference for LVMH between then and now, however. At that time, its P/E was almost 17% lower than average, since it was trading at lower valuations than those for Hermès and Richemont. Now, however, it is trading at only 7.5% less than average, with its P/E having risen significantly above CFRUY and only behind HESAY (see chart).

Source: Seeking Alpha

As a result, even if the LVMH price were to increase to the peer average P/E, the potential price rise is only 8% right now. This can change of course, depending on peers’ performance, as we saw last year. The market multiple comparison last year had indicated a 20% upside to LVMH last October. In actual fact, it rose by 70%.

What next?

2023, however, is likely to be different. A strong base year for sales growth, high net margin and a growth slowdown in key markets like the US and Europe this year can potentially have an impact on LVMH’s financials. There is nothing to suggest that the company won’t show either healthy growth or continued profits. It’s just that there can be a softening in pace.

It doesn’t help that in the meantime its price has run up significantly, and is just coming off all-time highs reached a couple of months ago. While a comparison with peers does indicate some upside, the extent isn’t convincing enough to make it an outright buy. If its growth does continue to soften and costs remain relatively elevated, its net margin can correct from last year’s highs. This in turn can make its forward P/E less attractive too. I would wait for the first half results due in July to get a better sense of where LVMH is now at. Until then, I’m changing my rating to Hold.

For further details see:

LVMH: Limited Upside If Growth Slows