LVMHF - LVMH: Long-Term Investors Should Start Accumulating Shares

2023-11-10 09:24:10 ET

Summary

- The luxury fashion selloff didn't pass over LVMH, which caused many shareholders, including myself, to see their investment's outperformance in 2022 getting erased.

- The stock is down more than 20% off its April highs, after missing growth expectations in the third quarter.

- LVMH is now trading at a 10-year low P/E multiple at 20x, as investors overexaggerate what is a mere return to normality after three extraordinary years for the company.

- On the 4-year stack, LVMH is still sustaining its historical double-digit growth rate, and management reassured the company's 27% margins are structural.

- I rate the stock a Buy and encourage long-term investors to start accumulating shares in order to capitalize on the company's turnaround story, in addition to the long-term annual double-digit returns coming from EPS growth.

Many LVMH ( LVMHF ) ( LVMUY ) shareholders, including myself, have seen their massive outperformance in 2022 nearly evaporate in light of a tech-focused rally, and a material growth slowdown.

The stock is down more than 20% from its April highs, following a third quarter with less than 2% reported growth.

I have to acknowledge my analysis of the stock in previous articles was too optimistic, as portrayed by the underperformance compared to the market. However, the company's long-term trajectory remains intact and its fundamentals are much better than what the price movement suggests.

I believe long-term investors should consider accumulating shares at these levels, and reiterate a Buy rating.

Introduction

I started covering LVMH in March, claiming ' 2023 Should Be Another Stellar Year, It's A Buy '. As we all know by now, that was a mistake, as LVMH underperformed the market by 23% since that article was published.

However, my investment thesis in the company, described in detail in the March article, remains valid, in my view. LVMH does possess pricing power, its portfolio of prestige brands continues to gain share in their respective markets, and the company's management remains prudent with a long-term focus on desirability, not letting the near-term downswing influence their decisions.

On the flip side, I was wrong on two main aspects, which are the key factors that have led to the decline. First, the Chinese cluster did not recover as strongly as expected. Second, growth has slowed down more than expected, specifically due to FX headwinds. On an organic basis, LVMH is still performing nearly in line with my initial expectations.

Let's take a look at the company's Q3 results, before diving into my updated Buy thesis.

Third Quarter Highlights

LVMH reported consolidated revenues of €19,964 million, a 1.1% increase from the prior year. Based on its historical seasonality, the French conglomerate is on pace to deliver 9.0% growth for the entire year.

Organically, growth in the third quarter amounted to a much better 9%, reflecting a nearly 8 percentage point impact from foreign currency, as the Euro strengthened materially against the Japanese Yen, Chinese Yuan, and the U.S. Dollar, compared to the prior year periods.

{kind=link}

LVMH Q3-23 Investor Presentation

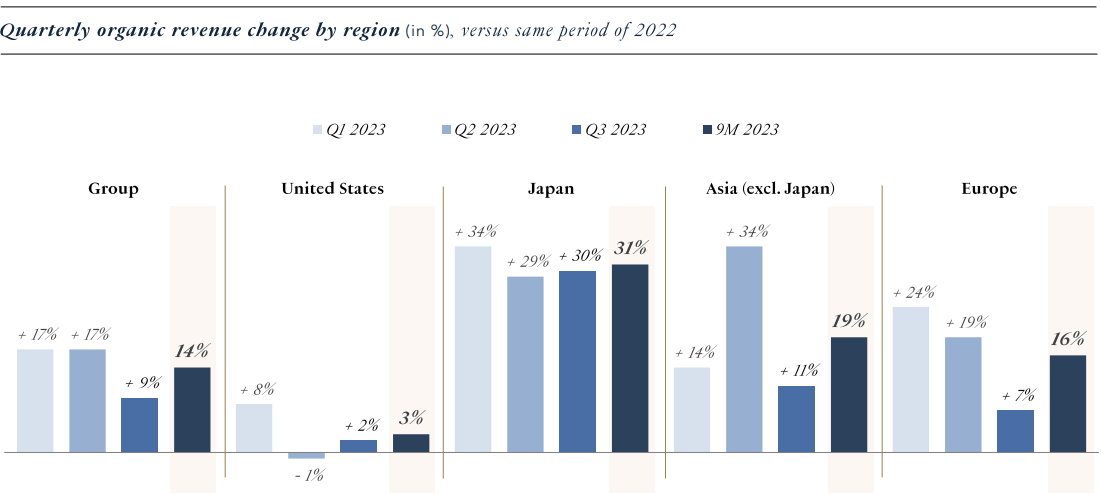

As we can see, Japan was the best performer in the quarter, with organic growth accelerating to 30%. The United States also saw a minor acceleration to 2%, although management commented that it isn't seeing a major improvement in the region just yet. Both Asia (excl. Japan) and Europe slowed down materially with organic growth dropping from 34% to 11%, and 19% to 7%, respectively.

{kind=link}

LVMH Q3-23 Investor Presentation

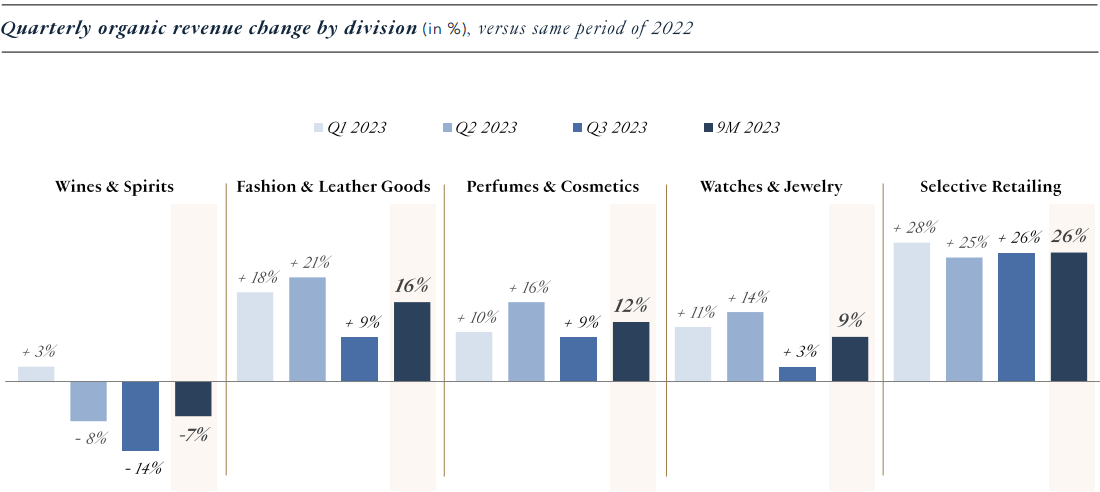

Looking at results by division, we can see Selective Retailing remains a major outperformer, with resilient organic growth in the quarter, as Sephora surpasses Ulta as the top beauty destination for teens. All other categories slowed down materially, reflecting management's comments on a weaker aspirational consumer, and a normalization after an extraordinary three-year performance.

Notably, Wines & Spirits is the only segment with negative organic growth, as the segment is still dragged by high inventories, specifically in the Cognac business. According to management, minor improvements on that front are already happening, but we're still a few quarters away from recovery.

Overall, LVMH disappointed investors and missed organic growth expectations by 2.5 points, primarily due to bad results from the Wines & Spirits division.

Updated Investment Thesis

There's one thing that investors seem to miss with LVMH, which reminds me of what happened to Alphabet ( GOOG ) in the past two years. Allow me to explain.

There are companies like Microsoft ( MSFT ), that constantly reach a new "floor" in terms of sales. What do I mean by that? When Microsoft signs a new customer in its core subscription-based businesses, that customer raises its revenue base. Unless that customer decides to leave Microsoft, which doesn't happen very often, every incremental customer the company gains the next year will contribute to growth. This means in a very simplistic general way, that if Microsoft doesn't gain any additional customers, its sales will remain flat.

With retail and LVMH in particular, that is not the case. There is no recurring business. There might be returning customers, but no customer has a monthly charge for a new leather bag. As such, LVMH does not have a floor, or, its floor is at zero sales. Every sale it makes is in theory, a new customer. As such, the fact that the company is able to continue to grow after three years of unreasonable growth is impressive. In my view. Let's take a closer look.

{kind=link}

Created and calculated by the author based on data from LVMH financial reports.

The above table shows the compounded annual growth rate of LVMH's sales compared to 2019, divided into quarters. We can see that since Q4-21, growth was pretty much steady in the 12.5%-14.5% range. This is, plain and simple, impossible to sustain. Historically, high-single-digit to low-double-digit growth has been the normal growth rate for LVMH, reflecting steady same-store sales growth, new store openings, and new acquisitions. Also, it showcases constant market share gains, as the luxury sector grows in the 6%-8% range, historically.

The luxury sector overall is experiencing a downturn driven by a widespread slowdown. Still, LVMH continues to significantly outperform peers, and take market share from the likes of Kering ( PPRUF ). The French conglomerate remains focused on the long-term, as evidenced by the recently announced acquisition of Barton Perreira, and the ongoing unique marketing campaigns.

In the third quarter of 2023, all that we are seeing is a return to normalization. This is very similar to what happened to Google post-pandemic, as a company that similarly to LVMH (in some way), doesn't have the "floor" attributes of Microsoft.

No, I don't think Google and LVMH are similar whatsoever, but the growth mechanism after out-of-the-ordinary years is similar. And as we've seen with the Google rebound in 2023, investors tend to overreact to normalization, just to then come back and buy the same stock at a similar valuation, missing the turnaround-story upside.

Another thing to note is that management was very certain of the company's ability to maintain the operating margins we saw in 2021-2022, referring to those as structural. Meaning the drivers of the margin improvement are here to stay.

To sum this up, LVMH experienced extraordinary growth over the past three years. This growth isn't sustainable, and investors shouldn't have expected it to be sustainable. I was wrong in assessing investors' expectations, as I thought the valuation reflected their understanding that a 20%+ growth rate isn't going to last forever. However, as we typically see in the stock market, when fundamentals take a negative direction, even if they remain good, a selloff is to be expected.

Valuation

This time I'll take a different approach to valuation and focus on the company's P/E ratio, as I believe it's the simplest and most reliable way to determine whether a stock is overvalued or undervalued compared to its historical levels.

LVMH is trading close to 10-year lows in terms of its P/E ((TTM)) ratio. The only period you see on the graph where the stock traded below a 20x multiple is due to a non-recurring earnings spike, and not a stock selloff. Undeniably, this is a historically low valuation for the company.

We know that management reiterated its guidance for the company's operating margins in the 27% being structural, as can be explained by product mix, operational leverage, and the maturity stage of each of the company's brands.

We also know that growth is normalizing on the 4-year stack starting in 2019, meaning that Q3-24 should be a major turning point, as the tough comparisons will materially ease.

Investors are already pricing in continued pressures over the next few quarters, despite the fact that in some regions and segments, comparisons and headwinds will begin to ease as early as next quarter. And remember, although it is exposed to aspirational consumers, LVMH's customer base is still much more resilient than average, meaning that even if the macro environment remains tough, LVMH should be able to outperform lower-level peers.

Conclusion

Investors (including myself), overestimated the company's ability to withstand the economic downturn and continue to grow after three years of fabulous growth. On the other hand, I estimate investors are overexaggerating the other way around. I expect LVMH's turnaround story to be a lucrative one, potentially leading to new all-time highs in the not too distant future.

In my view, long-term investors who will be able to withstand what I expect to be three-quarters of inferior performance should start accumulating shares at these levels.

I expect LVMH will return to its historical double-digit EPS growth rate sooner than expected, and expect that through EPS growth and multiple expansion back to historical levels, the stock is highly likely to provide market-beating returns for the foreseeable future. As such I rate LVMH a Buy.

For further details see:

LVMH: Long-Term Investors Should Start Accumulating Shares