LVMUY - LVMH: The Market Is Likely Wrong About This Stock

2023-10-19 05:29:04 ET

Summary

- LVMH's stock price has dropped 25% since May, but the company's long-term projections are encouraging.

- The market is overreacting to possible risks, as LVMH has shown resilience in previous recessions.

- Q3 revenues show a return to sustainable growth patterns, with strong performance in fashion, cosmetics, and jewelry segments.

Investment thesis

Since last May, LVMH has experienced a 25% drop in its stock price after reaching its historical highs. Nevertheless, the results for the first half of the year confirm that the business continues to operate exceptionally. However, the market is considering short-term risks for the company, which has prompted this notable decrease in its value.

From my perspective, I believe that investors are overestimating these risks. As we will detail in this article, the long-term projections for LVMH are very encouraging. While it is true that these risks could slow down short-term growth, this should have a limited effect on our valuations. This is because the value in this type of company lies in our ability as investors to anticipate their cash flows in the coming years rather than focusing solely on next year's results.

Before we begin, it is important to clarify that this article is aimed at long-term investors and is not intended to speculate on the short-term price of the stock in response to possible news that may affect it. The focus will be on understanding why the risks that the market perceives are not so significant and attempting to establish a fair price for LVMH shares.

The market is overreacting to possible risks

One of the main concerns in the market regarding this company is a possible slowdown in global consumption, especially in China . While it is true that there are many indications that we may be on the brink of a recession, especially in the West, I believe it is too risky to try to play in the short term based on these growth expectations. It won't be the first (or the last) time that a recession is forecasted but never actually happens.

However, let's consider the worst-case scenario: imagine a recession does occur. The first question we should ask is what kind of growth we would see in the top line if that happens. To answer that, we can study how LVMH has performed in previous recessions.

In 2003, LVMH's sales dropped by 5.5% , although from my point of view, this might not be the best comparison as the company today has a much higher degree of diversification due to its acquisitions in recent years. In 2009, sales only fell by 1% , which I find quite remarkable. During the worst consumption crisis in decades, LVMH only experienced a 1% drop in sales. Moreover, as mentioned earlier, the company is stronger today than it was back then. The crisis in 2020 should not be given too much weight due to its brevity and uniqueness; it's unlikely that a crisis of such nature will repeat itself.

{kind=link}

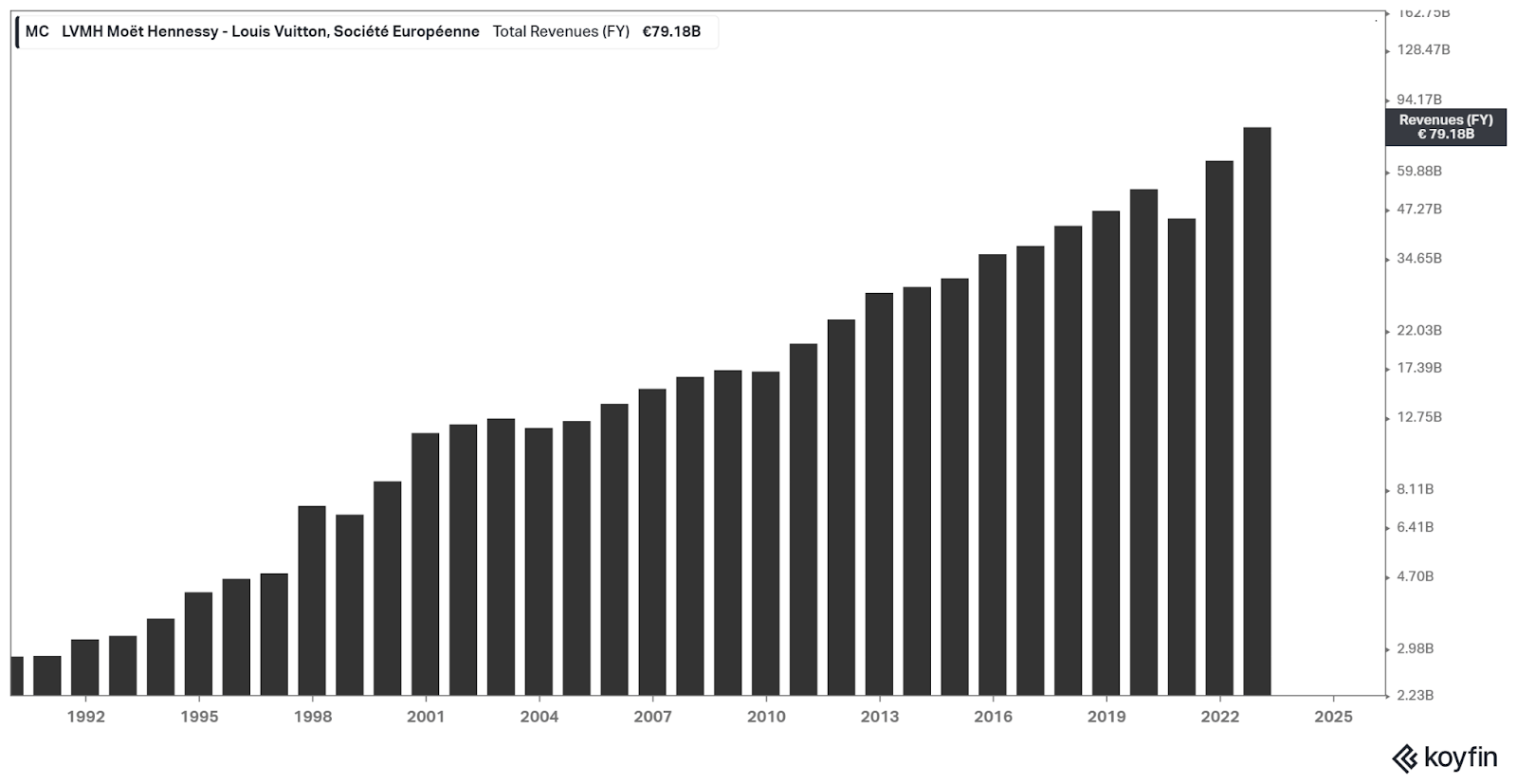

So, in the last two major recessions, LVMH's sales declined by an average of 3%. Considering that both were quite severe economic crises, I believe this demonstrates a resilience that very few other companies can match, especially in the consumer sector. Additionally, it's worth considering that they tend to emerge stronger from crises. Even with these two very severe recessions in between, LVMH has managed to achieve a compounded annual sales growth of 11% since 1990. Now, the next question we should ask is why LVMH fares so well during crises when its products are not basic necessities and are not accessible to everyone.

The answer, in my opinion, is precisely because they are not accessible to everyone. LVMH targets the highest echelons of society, whose purchasing power and financial knowledge enable them to maintain high levels of consumption even during times of crisis and even accept price increases on their products. However, it's worth noting that not all of LVMH's customers fall into this category; there are certain low-income consumers who save for months or even go into debt to access their products.

For luxury sector companies, it's important to know the percentage of each type of audience they have. Let's consider two examples: first, we have a company like Ferrari (RACE), whose product type is impossible for the average retail consumer to afford and is therefore very resistant during crises. On the other hand, we have a brand like Nike (NKE), where a significant portion of its audience consists of small consumers whose purchasing power is more affected during recessions.

In LVMH's case, it's challenging to determine the exact percentage of each audience type since it owns more than 75 brands, each with a mix of different consumers. However, considering that the highest-grossing brands within the company are oriented toward the high-end market (LV, Dior, Fendi, Tag Heuer, Tiffanys...), I believe we can place LVMH somewhere between Ferrari and Nike but closer to the former.

Therefore, I believe that based on these facts, we can assert that LVMH is prepared to withstand a period of recession or slower economic growth, and even better than in previous crises, given the larger number of top brands in its portfolio since those two crises we mentioned. So, the market's fears of a recession that has not even been confirmed yet, in my opinion, are being exaggerated.

Q3 Revenues

The company's most recent sales report , presented not long ago, precisely illustrates the resilience we mentioned in the previous point. In aggregate, the group's sales have increased by 9% when comparing this third quarter to the previous year. Some may consider this growth to be somewhat modest, falling short of Wall Street's expectations. However, in reality, it represents a healthier and more aligned trajectory with the company's long-term objectives. The growth rates witnessed in the past two years were influenced by the substantial post-pandemic economic expansion. The company's own goal is to maintain sales growth at 8-10% in the long term, and over the past 33 years, they have averaged 11.5%. Therefore, this deceleration is not negative; rather, it represents a return to more sustainable and robust growth patterns.

In fact, growth rates as high as those seen in recent years, exceeding 25%, are not necessarily positive. They can pose a long-term risk to the company's terminal value. It is crucial to consider that all luxury brands face the growth versus exclusivity dilemma. When a luxury brand focuses on maximizing growth, increasing sales volume, it risks diluting the brand's exclusivity. This could lead to a perception that the brand is no longer exclusive, undermining the key differentiator of luxury brands - the ability of upper-class consumers to differentiate themselves from the rest of the population. Therefore, prolonged periods of rapid growth, as observed in recent years, can potentially erode the brand's exclusivity and impact the company's terminal value.

Despite the slowdown and considering the macroeconomic environment we are currently in, marked by interest rate hikes worldwide, wars, and inflation, I believe that the sales growth has remained quite robust. Delving further into the details, we can see that the segment most affected is Wines & Spirits, primarily due to the decline in the cognac market, which is suffering globally due to its cyclicality and to which the company is highly exposed.

Meanwhile, the fashion, cosmetics, and jewelry segments continue to deliver strong growth rates of 9%, 9%, and 3%, respectively. Lastly, the Selective Retailing segment continues to experience remarkable growth, driven by the resurgence of tourism in Asia and the strong performance of Sephora.

Q3 Revenues per Segment (LVMH Investor Relations)

The importance of Bernard Arnault's vision

One of the most critical aspects to understand about this company's business is its CEO, Bernard Arnault. He views LVMH not simply as a stock or an investment, but as his own company. His top priority is ensuring the company's longevity and safeguarding the long-term value of its brands. He will never prioritize the company's growth over protecting the value of its brands, and this is precisely what has made LVMH such a successful company throughout its history.

In fact, Arnault's current primary concern is the issue of succession within the company - what will happen to his company when he is no longer at the helm? To address this concern, he has placed his children in high-responsibility roles, leading brands like Tiffany's or Dior. He understands that the most significant long-term risk for LVMH is succession, and he has seen firsthand how it can lead to the complete destruction of a company, as was the case with Gucci several decades ago.

On the other hand, it is highly positive to see that the Arnault family has practically 100% of their wealth invested in the company. Currently, they own approximately 50% of the company and reinvest all the liquidity they receive through dividends or other businesses back into LVMH. There are few companies where the CEO has so much of their personal wealth invested, and even fewer where they engage in as many purchases of their own shares. The chart shows each green point as a purchase made by the Arnault family in the company.

Insider's Transactions (Screener Insider)

Now, my reflection is as follows: Why is the Arnault family buying shares of their own company? The answer seems clear: they know it's the best possible investment they can make. They have a better understanding of their company than anyone else and are committed to growing their wealth in the long term. In fact, I am firmly convinced that if they could, they would turn LVMH into a private company and manage it entirely themselves. Fortunately, for now, this is not possible, and we have the opportunity to acquire shares in this wonderful company and benefit from the highly likely long-term appreciation of its stock.

Valuation

At the time of writing this article, the stock is trading at €660, which represents a 25% drop from its all-time highs. To attempt to determine an intrinsic value, I will perform two different types of valuations that are not typically used for valuing LVMH: first, a sum-of-parts valuation, and then a discounted cash flow analysis.

The idea behind the sum-of-parts valuation is to assess each segment of the company as if it were a standalone business, applying what we believe to be a fair multiple to each segment and then summing up all the segments to obtain an intrinsic value for the overall entity.

My valuation will aim to be extremely conservative. First, we will calculate the 2023 sales for each segment by annualizing the first-quarter sales (which is already a very conservative approach, as the second quarter usually outperforms the first in terms of sales). Also, we will assume that the profit margins from the first quarter will be maintained in the second quarter. To apply the multiple to each segment, I will also take a conservative approach. I will assign an 18x EBIT multiple to the fashion segment, which is lower than some lower-tier competitors like Moncler, which trades at around 22x. The rest of the segments will be assigned a 15x multiple, and the retailing segment will be assigned a 12x multiple.

With all of this, we arrive at the conclusion that the fair value for a Louis Vuitton share today should be €800. I am aware that sum-of-parts valuations are not typically the most optimal approach for businesses of this nature. However, considering that we have been extremely conservative, the current stock price offers approximately a 10% margin of safety.

Author's valuation using data from seeking alpha (Author Own )

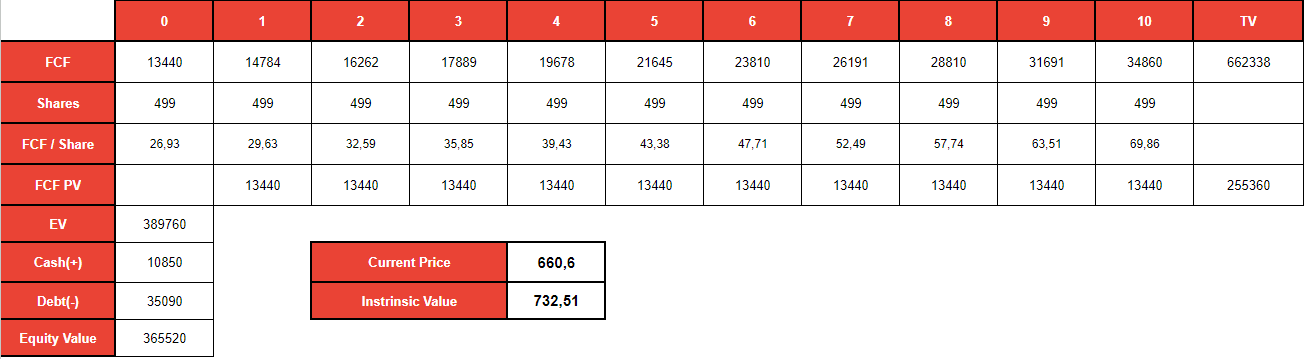

However, for this type of company, I prefer to use a discounted cash flow model, as it allows us to consider the terminal value of the company, which, as we have seen in this brief analysis, is key to this company. I have projected a 10% annual growth in free cash flow from year 1 to year 10 and a discount rate of 10%, which I believe provides a sufficient margin of safety for a company of such high quality as this one.

Regarding the terminal value, I have chosen to apply a rate of 4.5%. This figure may seem high in the case of traditional companies, but considering LVMH's strong ability to set prices, its relatively inelastic demand, and its operation in a sector with minimal disruption, I am convinced that LVMH, from its dominant position, can achieve sustained perpetual growth at this level.

Applying these numbers, we have an intrinsic value of €732, which also offers a margin of safety, similar to the sum-of-parts valuation.

Author's DCF using data from seeking alpha (Author Own)

{kind=link}

In conclusion, we have seen that the risks that the market is considering for LVMH are, from my point of view, being overestimated. We have also verified that the growth during the third quarter of this year has been quite good, even though it fell below market estimates. We have also understood the CEO's vision and the importance of his alignment with the shareholders, as he has his entire wealth invested in this company.

If we take into consideration all these factors, I believe we can assert that the market is overestimating the potential risks the company may face. Even in the event of a recession, LVMH has already demonstrated its impressive ability to handle them. Furthermore, by employing two entirely independent valuation methods, we arrive at the conclusion that the stock is undervalued, and therefore, I assign it a buy rating.

For further details see:

LVMH: The Market Is Likely Wrong About This Stock