LVMHF - LVMH Vs. Hermès: Only One Is A Buy Now

2023-10-10 11:43:16 ET

Summary

- Hermès is viewed, in my opinion, as the superior business due to its longer history, focus on its own brand, and its financial results over the last decade.

- LVMH is also a high-quality business with strong brand value and represents a prominent figure in the luxury industry.

- Both companies have demonstrated high returns on capital, double-digit revenue growth, and margin expansion.

- Only one stock at a buy point.

My Thesis

Both Hermès (HESAY) and LVMH (LVMHF) are exceptionally high-quality businesses. They demonstrate predictability, consistently deliver quality products, and possess strong brand value, and I would be delighted to own both of them. In fact, I currently do not hold any shares in either company due to their high prices. However, I do perceive an opportunity in one of them, particularly in the less favored but still exceptional business.

The Superior Business

I view Hermès as the superior business for several reasons:

1. Longer History: Hermès boasts a six-generation legacy of success without experiencing any significant failures. In contrast, LVMH may eventually face the challenge of transitioning to the second generation.

2. Focused on Its Own Brand: Hermès maintains a strong focus on its own brand, even when selling products under different brand names. LVMH, on the other hand, operates as more of a holding company, acquiring high-end luxury brands and integrating them into its extensive portfolio. Personally, I have a preference for organic firms.

{kind=link}

3. Emphasis on Craftsmanship: Hermès is widely considered to be the pinnacle of luxury, with a strong emphasis on craftsmanship and the exceptional quality of its products.

I'm not alone in this belief; Bernard Arnault, who made multiple attempts to acquire Hermès, shares the same sentiment. Hermès did not welcome those acquisition attempts.

Yet LVMH Is a Monster Itself

LVMH, led by one of the richest people in the world, is also a superb high-quality business and represents a prominent figure in the global luxury industry. It boasts strong brand value through Dior, Louis Vuitton, and a portfolio of other prestigious brands, including Tiffany, among others.

I believe that LVMH presents a buying opportunity, but we will delve into the details later in the discussion.

Both companies are massive compounders, outperforming the market over the last decade.

I believe this is due to several key data points:

1. High Returns on Capital: Both companies demonstrate excellent returns on capital, well above their cost of capital. Hermes, in particular, boasts higher figures, which I believe is one of the key reasons for its outperformance.

2. Double-digit top-line growth: Both companies have achieved substantial revenue growth with impressive CAGRs. This growth, coupled with their high returns on capital, positions them as formidable competitors in the market. While Hermès exhibits superior growth rates, it's essential to consider its smaller size when making direct comparisons.

3. Margin expansion and operating leverage are evident in both companies, with Hermès leading the way. This is understandable, as LVMH has a diverse portfolio, including a retail business like Sephora and various products such as alcohol and wine, each with different margin profiles.

Before we delve into valuation, let's perform a solvency check. Hermès presents a robust balance sheet with $10.2 billion in cash and total debt of only $2.1 billion, resulting in a current ratio of 4 and a very high Altman Z score, Hermès can cover its debt within one year of free cash flow. There's no danger here. LVMH presents a different picture. It holds $11 billion in cash but carries $40 billion in debt, which makes sense since LVMH frequently makes acquisitions that require debt financing. A notable example is Tiffany, which had a price tag of $15 billion . However, LVMH maintains a solid current ratio of 1.2 and an Altman Z-score above 3, indicating solvency. LVMH's predictability and diversified business portfolio allow them to take on more debt when needed.

In terms of returns to shareholders, both companies distribute dividends; however, neither of them has implemented a robust buyback program.

Hermès Valuation – A Glimpse at Its Premium Price

Let's proceed with a Three-Step Valuation: Historical Multiples, DCF Model, and Technical Analysis. We'll Begin with Multiples Valuation:

In general, while considering Hermès, which is not a typical company, I prefer to invest in businesses trading at current multiples lower than their historical averages. Ideally, significantly lower, as I discussed in my previous article on Evolution (EVVTY). It's important to note that historical averages are derived from a Zero Interest Rate Policy (ZIRP) economy, so one should anticipate some level of multiple contractions.

In terms of free cash flow yield, Hermès' 5-year average is 2.1% , while the trailing twelve-month ratio is 2.2%. Other multiples, such as EV/EBITDA, are slightly below their 5-year averages. I'd like to see those multiples lower before considering a buy.

{kind=link}

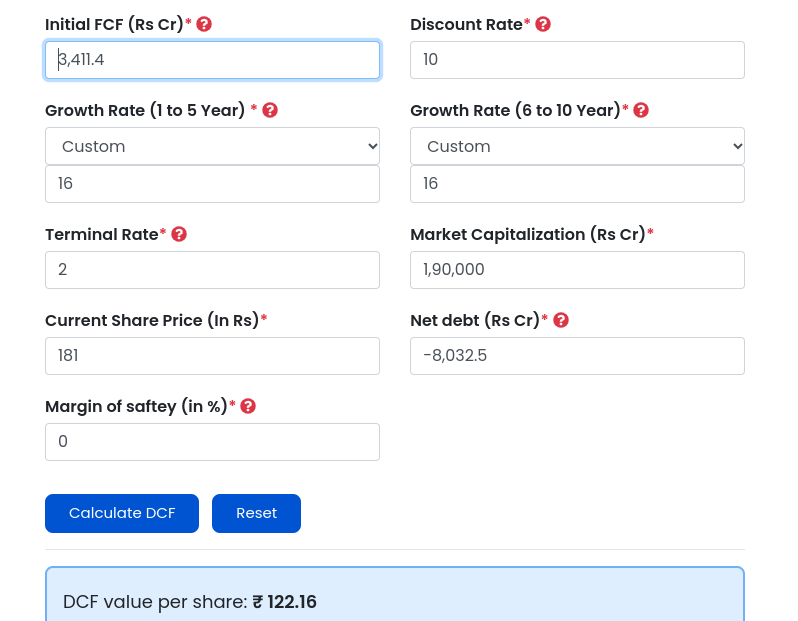

Let's proceed with a simple DCF (Discounted Cash Flow) model. I'm using a 10% discount rate, which is relatively solid given Hermès' highly predictable business nature. I've input a 16% growth rate, considering that this has been the average over the last five years. Since Hermès is not a cyclical business, it's reasonable to expect this growth to continue. The terminal growth rate is set at 2%.

The results from this analysis reveal an intrinsic value of $122. Consequently, the stock is overvalued by approximately 48%. The current price of $181 implies a growth rate in free cash flow of 22%, which seems somewhat unrealistic. Even though the average growth rate over the last 10 years has been 21% , it's essential to consider that the company has grown significantly larger now.

{kind=link}

I would like to emphasize that certain companies are of such high quality that the simple DCF model may not fully capture their intrinsic value. It's possible to have encountered such situations in the past where a DCF model did not indicate an undervalued stock and has historically been a massive compounder. While I cannot confirm if this is precisely the case with Hermès at this moment, I am confident that this is the scenario with LVMH, as we will examine shortly.

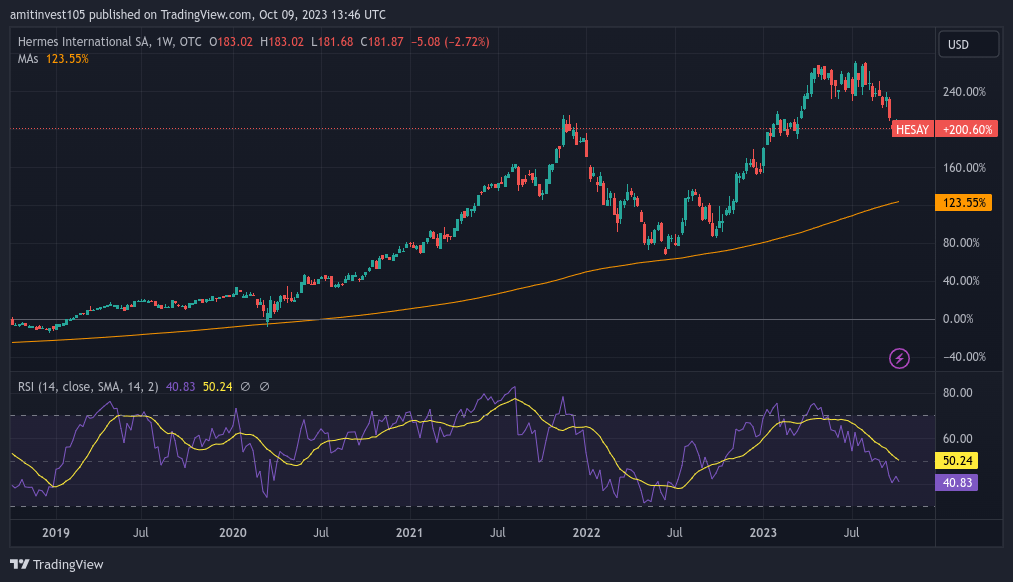

From a technical perspective, although I don't consider myself a technical analyst, I do favor purchasing companies when their stock prices are in proximity to their 200-day moving averages. Additionally, I look for a low RSI (Relative Strength Index) as an indicator. It's essential to consider these factors while the stock is not at its peak, and the RSI is displaying a downward momentum. I prefer waiting for the RSI to reach a lower level before considering an initiation of a purchase.

{kind=link}

After evaluating Hermès through these three methods, I would consider it as a "HOLD." While it is trading at a better price compared to the past, it does not appear to be a bargain in my view.

LVMH at a Fair Valuation

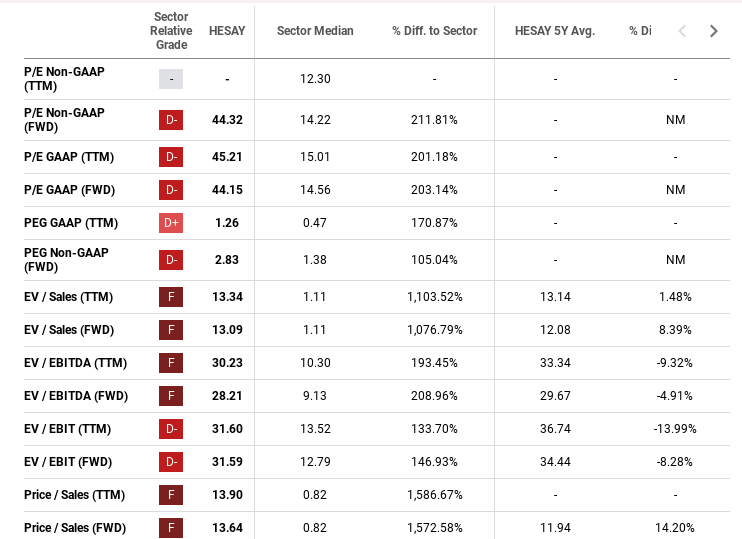

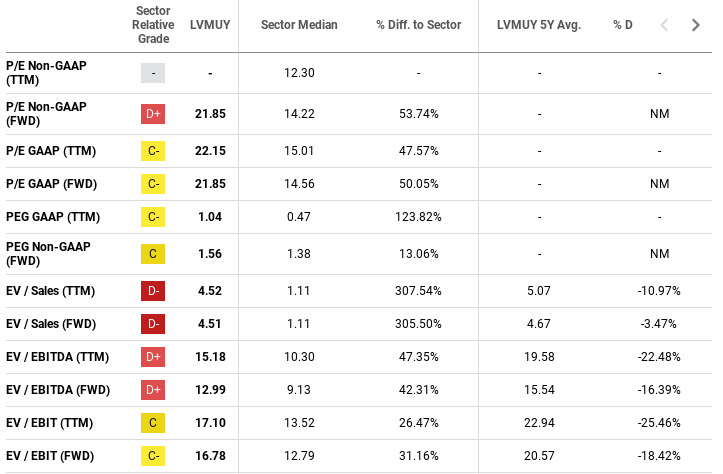

Let's do the same for LVMH: LVMH is currently trading below its historical multiple averages. Though, if I calculate the market capitalization based on the last 3 years' average free cash flow and divide it by that, I'd get a 3.1% free cash flow yield, which is below the historical average of 3.9% yield in the last few years. In terms of forward EV/EBITDA, it is undervalued by 16%. You can refer to the chart for other multiples.

{kind=link}

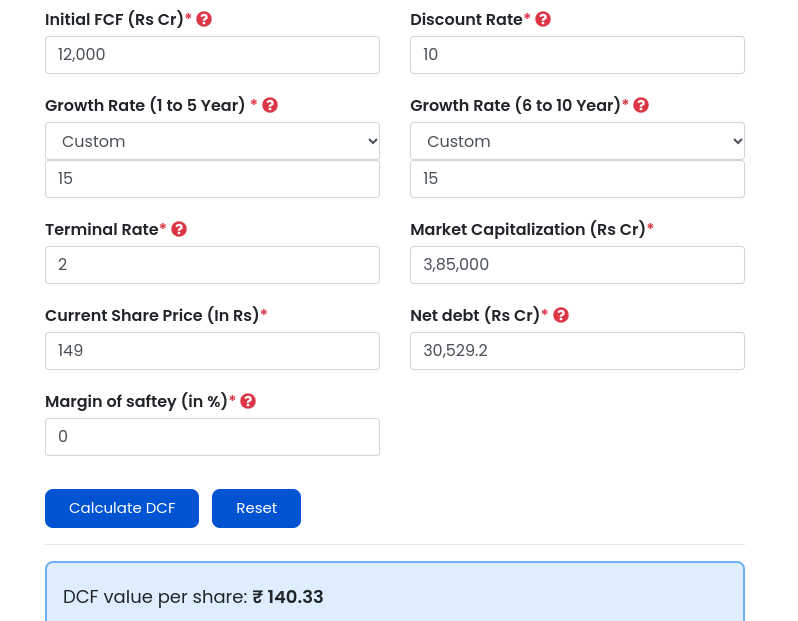

In the DCF valuation, I used a 10% discount rate, a terminal growth rate of 2%, and a growth rate of 15%, which is the 5-year CAGR and seems reasonable for the future. The stock price derived from the model is $140, which is essentially a little bit overvalued compared to the current price of $149. I used the 3-year average free cash flow.

Again, the DCF model can't always fully capture the quality of the company, and I believe that in stocks like LVMH, when the model suggests that the price is not unreasonable, the price is good. Unlike Hermès, where the model suggests almost a 50% overvaluation, LVMH seems to be reasonably priced.

{kind=link}

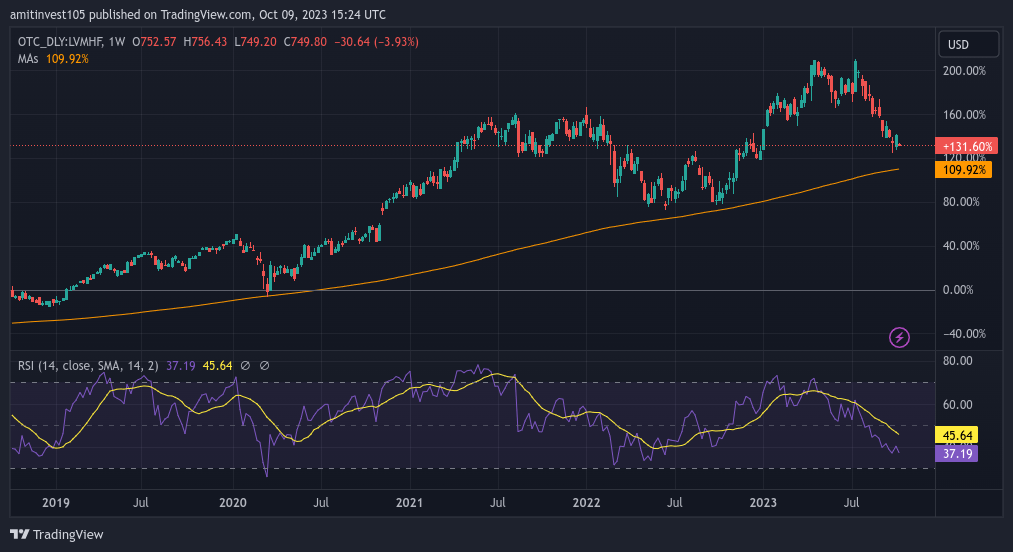

From a technical point of view, the stock appears to be close to the 200-day average, and the RSI is relatively low.

{kind=link}

After examining the three valuation methods for LVMH, I believe that the stock is currently at a reasonable price. While it may not be a bargain, it's unlikely to find such quality at a bargain price. Therefore, my rating for the stock right now is a BUY.

Conclusion

Both Hermès and LVMH are excellent businesses that I would love to own. However, I believe that only LVMH is currently in buy territory. One of my greatest mistakes in the past was buying stocks at high prices because of their quality, and I want to avoid making that mistake again. While I believe that Hermès is a superior business to own, I think it would be a more attractive buy at prices around the 130-140 range.

On the other hand, LVMH seems to be at a reasonable price, although not a bargain. I hold the belief that it's almost impossible to buy businesses of this quality at bargain prices. A notable example is ASML (ASML), which I wrote about in my first article . Therefore, I consider LVMH to be a stock worth owning at its current price.

I currently do not hold either of the securities mentioned in this article, as I have identified greater opportunities in the market right now. You can read my last article about Evolution to find bargains or Ult? .

I would appreciate hearing your thoughts on this matter.

For further details see:

LVMH Vs. Hermès: Only One Is A Buy Now